$KEEL is the most underappreciated AI infrastructure play right now.

Former Bitcoin miner → full pivot to HPC/AI. Over 2 GW of secured capacity in North America. Fresh $400M convertible notes just priced to fund buildout. Multi-billion dollar gov contract wins.

1/3

$533M in liquidity including unencumbered BTC on the balance sheet.

Yes, it's pre-profit. That's the point. You don't buy picks-and-shovels after the gold rush.

Analysts at B. Riley, Cantor, Chardan, and HC Wainwright all have Buy/Overweight. 1yr target: $10.20.

2/3

$KEEL

Bear case: “Dilution.”

Bull case: With $400M and said proceeds can be used for long-lead equipment deposits and collateral to accelerate data center expansion. In the AI infra race, you win with power, equipment, and capacity. Market is underestimating the financing,

Weak hands saw dilution.

Long-term investors saw growth capital.

The AI buildout isn’t slowing down, and neither is KEEL.

$KEEL #AIInfrastructure#DataCenters

4/4

Evenryone is focused on the red candle. I’m focused on what $KEEL just did.

$KEEL raised $400M at only 1.25% to accelerate its AI/data center expansion. The market saw “convertible notes” and sold. I see a company securing capital while AI infrastructure demand is exploding.

1/4

KEEL already has development underway at Panther Creek, Sharon, and Moses Lake, and reported over $500M of liquidity before this raise. Now the company has even more firepower to pursue its AI infrastructure strategy.

3/4

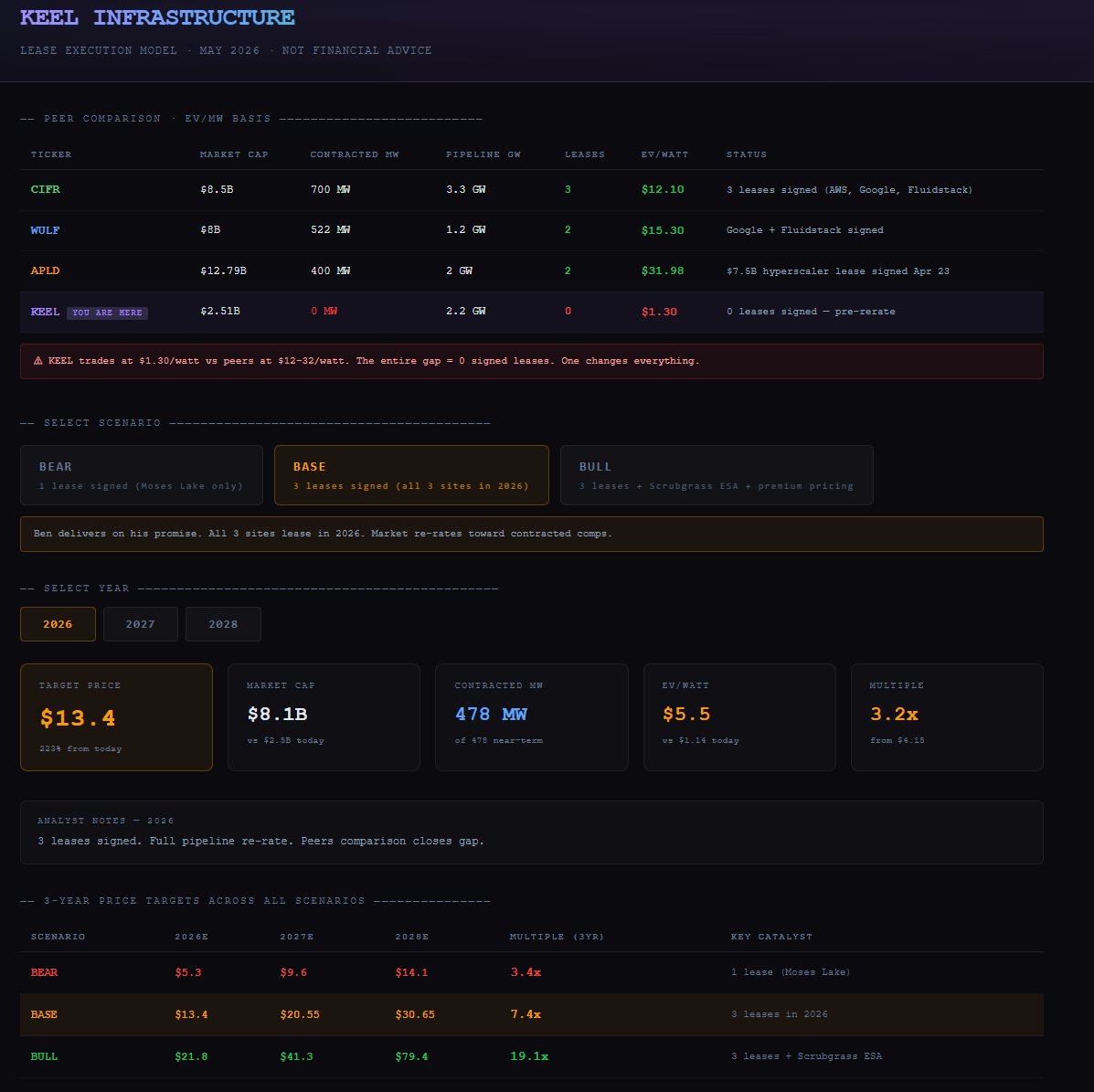

$KEEL -we built a full 3-year pricing model.

Based on real peer data. Three scenarios. Interactive.

Here's what the comps say today:

$APLD — $12.8B market cap. $32/watt. One lease announcement.

$WULF — $8B market cap. $15/watt. Two leases signed.

$CIFR — $8.5B market cap. $12/watt. Three leases signed.

$KEEL — $2.5B market cap. $1.30/watt. Zero leases. Three promised.

The gap is entirely explained by one thing: no signed lease yet.

Ben Gagnon. On the record. Three leases. This year.

🔴 Bear (1 lease): $14 by 2028. 3.4x

🟡 Base (3 leases): $30 by 2028. 7.4x

🟢 Bull (3 leases + Scrubgrass): $79 by 2028. 19x

$KEEL hasn't executed yet.

$KEEL 🏗️⚡

DYOR. NFA. Model built on public data.

$KEEL --- $KEEL is no longer a pure cryptocurrency mining firm. It has fully transformed into a pure-play North American digital and energy infrastructure platform. The company controls a total of 2.2 gigawatts (GW) of power pipelines and established grid interconnection assets across Pennsylvania, Washington and Quebec, Canada, focusing on colocation services for AI and HPC data center infrastructure.

For its flagship AI data center sites located in high-demand, power-constrained regions across North America — Panther Creek, Sharon and Moses Lake — all land planning and zoning approvals have been secured. These projects are now in full-scale development, with formal lease agreements expected to be signed in 2026.

1.Power Grab Premium in the AI Era

For major global tech giants including Microsoft, Amazon and Google, the biggest bottleneck is no longer server hardware, but grid interconnection capacity. A mining operation with approved access to 2.2 GW of grid power carries far greater intrinsic value than traditional crypto mining. By repurposing undervalued mining facilities into high-value AI data centers, $KEEL is poised for a full Wall Street valuation re-rating.

2.Fundamentals Fully De-Risked, Institutional Capital Flows In

Previously tied to cryptocurrency exposure, Bitfarms was off-limits to many large mutual funds and sovereign wealth funds due to compliance rules. Following the rebranding and restructuring into KEEL, a standalone U.S. infrastructure company, the firm has completely shed its crypto label. It is now investable for institutions as a pure play on AI power and digital infrastructure. Institutional holdings have quickly climbed to over 43%.

#keel $KEEL

Closed at $5.13.

Institutions loaded up on the dip!

133.79 million inflow

93 million of it was institutions(large orders).

57.15 million outflow.

Only 28.49M of it was large orders.

This shows retail was selling, while institutions where buying up all the dip.

The whole market dipped 10-15%, not just keel. Keep your head up and in the game!

#keel $KEEL

I don't think people realise how massive these dark pools are for such a small stock.

These are mostly buys!!

I've attached ondas dark pool just for reference.

I also checked #hive a similar stock. 0 dark pool trades.

Checked #cifr, 0 dark pool.

Checked #wulf, 4m worth of dark pool.

As I'm writing this, more is coming in.

It is at 70m worth of dark pool 👀

Is there going to be a deal soon🙈

My prediction for $KEEL :

June -> Moses Lake lease signed with Neocloud

July-> Sharon lease signed with large enterprise(Jane street, Citadel, etc.)

August/September-> Panther Creek signed with Hyperscaler ( $MSFT, $META, $GOOG, $AMZN)

It’s time for me to talk about $KEEL

First, do I like that they raise money via convertible senior note, before any lease announcement?

No, I was caught off guard by the timing as well. The standard is to announce a deal, stock run up, then raise at a euphoric premium.

Now the question is why would management do so, after already emphasising that the balance sheet is strong enough to support the 3 lease executions?

“As I noted, we have the liquidity to reach lease execution across all 3 sites without the need to tap into debt or equity capital markets. That said, we will remain opportunistic if attractive opportunities arise.”

- Jonathan Mir, CFO

Three possible reasons:

1. Tenant requires capital pre-positioning as a condition of lease execution

2. Multi-site framework deal scope expanded beyond original capital plan

3. Genuinely opportunistic — taking advantage of strong convertible market while it’s open

The ideal scenario is that it’s due to all three reasons above. Remember Moses Lake can be expanded to 28MW (from 18MW). Could it be that customer wants the additional 10MW? Maybe it’s Panther Creek or Sharon?

For management to take the unpopular route, they must’ve thought the contract/tenant is worth it.

Lastly, I know some of us have PTSD from the $BITF days, when the convertible offering last year sent us into a downward spiral. However, the promise of 3 high quality execution this year is worth the short term pain.

$KEEL The market saw dilution. The filing said "we're building now."

May 11 — Ben: "$520M is more than the CapEx budgeted to GET US TO A LEASE." CFO Mir: "Construction funded by equity-linked offerings." Ben: "Designing to customer specifications." "NTP is the last thing standing between us and a signed agreement."

May 29 — Ben on X: "129 investor meetings since May 11. All of 2025 we did 168. Pump the brakes on calls. Back to work."

June 4 — $350M convertible notes. Use of proceeds: "equipment deposits and letters of credit for expanding and accelerating data center projects."

The CFO already told you equity-linked offerings fund construction. This $350M is that. You don't put down equipment deposits and post letters of credit without a customer on the other end. Market sold it off as dilution. The use of proceeds is telling you they're building right now.

If this helped you out, follow for more.

$KEEL is printing beautiful long green candles.

Momentum is building, buyers are stepping in, and the chart is starting to look exactly how bulls want it to.

$KEEL as of this morning the 11 straight day streak is in jeopardy. What an amazing stretch. A pull back was imminent and is healthy. The stock will hit new highs later this year once deals are announced.

I will be using this opportunity to re-enter and buy back the shares I sold.

$KEEL daily update. That was a clear double double top at $6.45. Price closed again below the stacked fibs. Third rejection.

The 4H chart also looks pretty clear.

Now, the question is, where are the whales going to buy the pullback?

I would watch the daily 8/9 (daily 8 at $5.66 for now, almost there premarket). A break under and reclaim could be a positive sign.

Another level I would watch is the previous support, the $5.34-5.40 area.

The whole market has pulled back yesterday, today premarket, a lot of tickers are deep in the red, and a pullback for KEEL has been expected for quite a long time now.

A pullback all the way to do daily 21 (now at $4.85) wouldn't surprise me either. Maybe not today (that would be a deep dip) but over several days.

As always, just reading data as it comes, everyday.

$KEEL Funds are going to begin accumulating for the Russell Index inclusion. There is a huge discrepancy between our market cap and the other 5 or 6 companies with contracts. That's about to change.

Like if you STILL believe $KEEL.

You can follow me,I'll be updating you with the latest info on KEEL and more related content.