Got my beautiful metal @ether_fi Cash card to complement the instant virtual version. Want one too plus 15% off food and drink?

1️⃣ Open an account via the link

2️⃣ Complete KYC

3️⃣ Activate at least one card

https://t.co/rWHoEtZXSf

Oh look… $NVDA CEO warned memory shortage is expected to persist for many years, due to massive scaling demand of AI infrastructure.

With further announcements tomorrow.

$MU and $EWY (Samsung/SK Hynix) operating profit projections aren’t looking too crazy anymore?

Sure, #1 thing is toxic financing structure/float dynamics.

Best example is current Neoclouds landscape:

- $IREN is basically trash, since they have $6,000,000,000 ATMs and virtually infinite dilution, likely selling into every rally (structural overhang)

- While $NBIS is now YTD 153%+, from optimal structures (eg. $NVDA direct funding, mix of convertibles, etc.).

- On the other hand, $CRWV has endless debt interest given they took out high interest rate loans to finance GPUs.

It's extremely nuanced, but you need to take a look at the float dynamics.

If they're legitimately a good company, then it might be a good idea to go long after all the existing holders get diluted to oblivion.

But if you care about your equity appreciation, it's a good idea to stay far away from toxic financing structures or toxic overhang (eg. debt interest, that eats away at a company FCF long term)

With smaller companies, they have this all the time, like

$SLNH, where there's new $500m ATMs on a $250m MC.

Or like $BKKT where there's endless dilution to fund executive pay.

With these companies you're basically transferring your money over to the company while influencers talk about them. So those are red flags.

With many software names like $SNAP, they mask stock-based compensation with profitability. So while the company optically looks profitable, you'll likely see the value of your equity decrease due to dilution.

There's endless types of these share structures you need to look when screening ideas.

The initial audits on the all new Aero are complete.

And we're excited to share that @sherlockdefi will be joining @chain_security as an audit partner moving forward.

The second phase of audits begin today and are expected to complete on June 19th. More to come, stay tuned. 🛫

Weekly Highlights👇

• Initial Aero audits are complete ✅

• Aerodrome, now available for AI agents

• $300B All-Time $ETH Volume

• Aero Ignition: $TEA takes off 🛫

• 190M $AERO Acquired & Locked

• Predictive Allocation TL;DR

• The @DromosLabs origin story

𝐕𝐞𝐢𝐥 𝐌𝐂𝐏 𝟎.𝟐.𝟎: 𝐏𝐫𝐢𝐯𝐚𝐭𝐞 𝐀𝐠𝐞𝐧𝐭 𝐏𝐚𝐲𝐦𝐞𝐧𝐭𝐬 𝐨𝐧 𝐁𝐚𝐬𝐞

@Veildotcash shipped MCP 0.2.0 which allows AI agents to make private x402 payments on base directly from the Veil shielded USDC pool.

Okay... just some more weekend shower thoughts about $XFAB.

I still feel like it could be the next $TSEM, just early stage at a $1.4B MC?

They kinda leapfrogged current gens (which $TSEM are getting volume from) to compete for H2 2027 CPO scale up inflection point ($ASX docs cite Xfab (aka. photonixFAB) as focusing on CPO)

By building out some black magic MTP (transfer printing) architecture for lasers w/ other stuff like TFLN.

Basically next-gen integration IP, they're still behind on yields, sure.

But $NVDA evaluating it for transceivers/switches to see if it can volume ramp. That $NOK sets the specifications/assembly for. (nvidia invested in nokia for this these switches/networking too btw).

And if their MTP supply chain works... (eg. with Smartphotonics providing lasers, EU players doing assembly).

It basically volume ramps with $NVDA just like why Nvidia signed long term agreements with $TSEM?

Downside risk?

Already below replacement book value, can always go lower yeah, but typically to a certain point.

Maybe more CHIPS act subsidies next few months from chips act 2. If it doesn't go well there's SiC (152% Y/Y Growth, 195% Y/Y SiC wafer shipment growth)/GaN power semi upside.

Europeans /LLMs will say "oh evaluations doesn't mean it's a future contract!".

This is kinda different since the European Union is behind this effort and $XFAB for soverign photonic supply chains.

Not your typical company + hyperscaler evaluation, since $NVDA wants to be nice to Europe's regulators. They'd prob be pissed if nvidia just stayed in US/Taiwan/China.

So if they can make this MTP black magic work with mass production, feels almost for sure nvidia/nokia volume ramp on some tiny $1.4B silicon photonics foundry or at least throw them a bone with smaller contracts.

In terms of timelines, maybe just a months early since it volume ramps H2 2027/H1 2028 (which happens to be in line with CPO scale up timelines)...

Or just unknown because they named their project something stupid like photonixfab?

Like XFAB Photonics would have been better? so institutions/screeners can connect the dots when looking at CPO silicon photonic foundry players?

Automotive should also coming out of a slump medium term, sped up by self-driving (TSM Chairmain comments yesterday said ai automotive was TSM's growth vector alongside robotics). So their core business also should pick up speed too medium term.

Obviously markets/europeans want a "Nvidia signs $2B+ contract, XFab volume ramping 2027!"

But by then it will be a $9B+ company and you miss out on all the upside. And especially since everyone analyst/institution is blind to volume expectations for these....

Normally don't invest in companies in evaluation stages, but this just seems very de-risked by EU sovereignty + Gov backing, and you have Nvidia + Nokia there for volumes if they can make the IP work.

I think markets are probably missing something here... there's almost 0 value being assigned to being CPO exposure in Europe as their long term upside.

Near-term BTC price action is going to be heavily dependent on one thing:

Did Saylor sell enough BTC this past week?

If he sold zero, that’d be a massive mistake on his end and we’re probably cooked.

If he sold $1B of BTC, that helps, but realistically I don’t think it’s enough and we probably continue lower.

If he sold at least $2B, that’s where it gets interesting and sets up a bounce.

The more he sold, the harder we bounce.

My base case is that he sold at least $2B. I also think there’s a decent chance BTC bottoms into Monday if the market starts pricing in that he sold some.

Rationale:

Selling none is my lowest probability scenario. He needs the money.

He already did that weird 32 BTC “test” sale and I have a hard time understanding the purpose of it. If he was planning on selling more, all the test did was give him worse execution. If he wasn't planning on selling more, then he nuked the market for no reason. The latter seems completely ridiculous, so my guess is it was indeed a test and he was planning on selling more.

A tiny sale ($500m) is the worst of both worlds. It damages the “never sell” narrative without solving the liquidity problem. If you’re going to sell, sell enough to matter.

That’s the key here.

A material sale does two things at once. It adds real cash runway, but it also sends an important signal to STRC buyers: he is willing to sell meaningful amounts of BTC to keep funding the dividend.

That signal matters a lot.

Strategy has roughly $871M left in its USD reserve. Against the current preferred + debt cash burden, that’s only about 6 months of runway.

If he sold $1B, that takes runway from ~6 months to ~13 months. Helpful, but probably not enough. 13 months is enough to reduce near-term stress, but not enough to make STRC feel like a self-sustaining issuance product again. STRC buyers are still underwriting a shrinking cash cushion and hoping the market rallies materially within that window. I think it becomes very hard for STRC to get back to 100 in that scenario.

If he sold $2B, that takes the reserve to ~$2.9B and extends runway to roughly 20 months. That is a very different setup. At ~20 months of coverage, blow-up risk gets pushed much further out, STRC buyers can believe the dividend is properly covered by cash on hand, and the product has a real chance of trading back to 100.

It also changes how STRC buyers think about the balance sheet. They’re not just relying on new issuance to get paid. They’re backed by a massive BTC treasury that Saylor has now shown he is willing to selectively monetize to support the credit stack.

Once STRC is back at 100, the flywheel can restart.

This is the “sell to buy” point.

A large BTC sale does not just create cash runway. It can increase his ability to issue STRC, which then gives him the ability to buy more BTC than he sold.

So the hierarchy is simple:

Selling zero is the disaster scenario.

Selling too little helps, but probably does not fix the flywheel.

Selling enough to matter is what gives STRC a path back to 100 and gives BTC a reason to bounce.

Sigh.

I keep telling retail + Swedish Hedge Funds how important $SIVE is to CPO, but people don’t listen.

Enough retail holders got shaken off, and

now JP Morgan managed to buy up a massive stake in Sivers (purely institutional).

JP Morgan went from .4% ownership last month to 5%+ ownership this month…

What just happened?

The S&P 500 just erased nearly -$2 TRILLION of market cap just hours after 3rd strongest US jobs report in 18 months.

Meanwhile, Bitcoin is officially down over -50% from its record high in October 2025.

What's happening? Let us explain.

(a thread)

NVIDIA CEO Jensen Huang stood on stage at COMPUTEX and called $MRVL the next trillion dollar company. When the most powerful man in tech says that about a stock you already own, you pay attention.

Here is why this is not just hype.

Huang did not say it casually. He explained exactly why. As AI computing problems get broken into thousands of pieces and spread across an entire data center, the one thing that makes it all work is connectivity.

The networking and custom silicon that lets thousands of chips talk to each other fast enough to function as one machine. That is what Marvell builds. That is why Huang called it essential.

And NVIDIA is not just talking. Earlier this year they put a $2 billion investment directly into Marvell.

The most valuable company on earth backing Marvell with real capital, then publicly anointing it the next trillion dollar company. That combination is extraordinarily rare.

Now the numbers behind the story. Marvell just guided its custom chip business to surpass $10 billion in revenue by fiscal 2029. The data center segment is exploding. Custom silicon demand from hyperscalers building larger and larger AI clusters keeps accelerating.

The stock is up massively this year and just posted its biggest single day gain ever on Huang’s comments.

Marvell sits at roughly $264 billion today. To hit a trillion it needs to roughly quadruple. That is the upside Huang is pointing at.

Connectivity is the bottleneck of the entire AI buildout and Marvell owns one of the most important positions in it.

When NVIDIA invests $2 billion in you and then calls you the next trillion dollar company, the path is laid out in front of you.

This looks like a no brainer to me here.

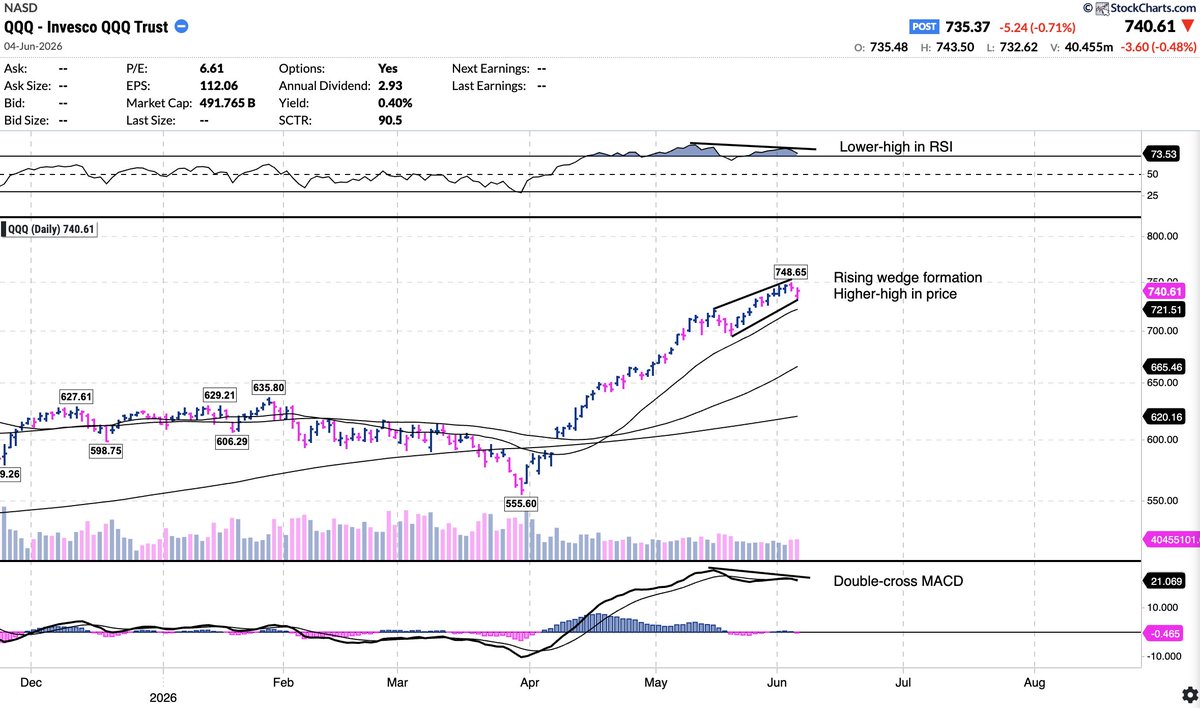

Listen to ME. I MADE you millions. Now I will SAVE you millions. You need to stay careful here.

$QQQ and the tech-sector is STARTING to show signs of LATE-cycle movements.

With each new MARGINAL high comes more and more BEARISH-divergence.

Bulls are getting VERY greedy at these levels.

What should you do?

For AI winners like $ARM, $AMD, $NBIS, etc.:

1. HOLD and KEEP

2. But I've TRIMMED my AI winners by 20% to lock-in gains

3. I've also started to HEDGE 15% of my portfolio (3-month puts, inverse ETF, etc.)

4. This helps ABSORB potential volatility

For lagging sectors:

1. We are OVERweight in $XLV and healthcare (doing very well for us)

2. We are OVERweight in bottoming sectors like software $IGV (doing great for us)

3. We are OVERweight in contrarian buys like consumer staples

For defensives:

1. Core positions in defensive sectors can HELP and maybe even OUTPERFORM the next few months

2. Think consumer defensives, utilities, and industrials

Overall, KEEP your AI winners!!!! We are still EARLY in AI.

But make sure you hold your gains by balancing your portfolio for the next 3 months ahead.

Reminder: @Veildotcash has been audited by Sherlock, the original build (TC Nova) was also audited too.

But security is not a one and done process. An audit is a snapshot in time, it tells you the code was solid on that day.

We continuously monitor for new bugs and vulnerabilities, and leverage new AI models and tooling as they become available.

Protecting your funds and your privacy is ongoing work, and we treat it that way.

The most interesting part of the $ADEA story is hybrid bonding, and the company is growing it faster than almost anyone realizes.

Hybrid bonding is a way of joining two pieces of silicon face to face using thousands of tiny direct connections instead of relying on larger external wires.

The result is smaller, faster, more energy efficient processors and memory stacks. As AI chips push against the physical limits of traditional packaging, hybrid bonding is becoming the path forward.

It is how the industry keeps advancing Moore’s Law in the AI era.

And $ADEA owns the foundational IP. Over 1,100 patents around it, acquired for $39 million a decade ago.

Here is how fast they are growing it.

Their patent portfolio went from roughly 9,500 at separation to over 13,750 today, an increase of more than 35%, driven primarily by internal R&D.

Their hybrid bonding technology was awarded Best of Show for Most Innovative Technology at the Future of Memory and Storage Conference.

And the adoption is broadening across the entire industry.

The CEO laid it out directly. AMD is already in production with hybrid bonded products.

Intel, Broadcom, and Marvell have all publicly disclosed roadmaps that will use hybrid bonding.

And on the memory side, Micron, Samsung, and SK Hynix are all making multibillion dollar investments into the high bandwidth memory and NAND that increasingly rely on it.

That is the entire AI hardware ecosystem migrating toward a technology $ADEA owns the foundational patents on.

And the financial engine behind it is elite. Record Q4 revenue of $182.6 million. Full year 2025 revenue of $443.4 million. 62.6% adjusted EBITDA margin.

Non-pay-TV recurring revenue up 81% since separation. Debt cut by $60 million. Credit upgraded.

Every major chipmaker on earth is moving toward hybrid bonding. $ADEA built the toll booth and they are expanding it every quarter.