@patienceisking@haloaerospace I thought their earnings were pretty strong. Think it was bid up on the increased wildfire activity YTD, but as they have demonstrated, their earnings are increasingly uncorrelated with acres burned.

@Sher_East_ Ever since they suspended calls their earnings have been a snoozefest. The only notable event this Q is the Somalogic cash hits their books, so it will finally screen as cash rich vs proforma.

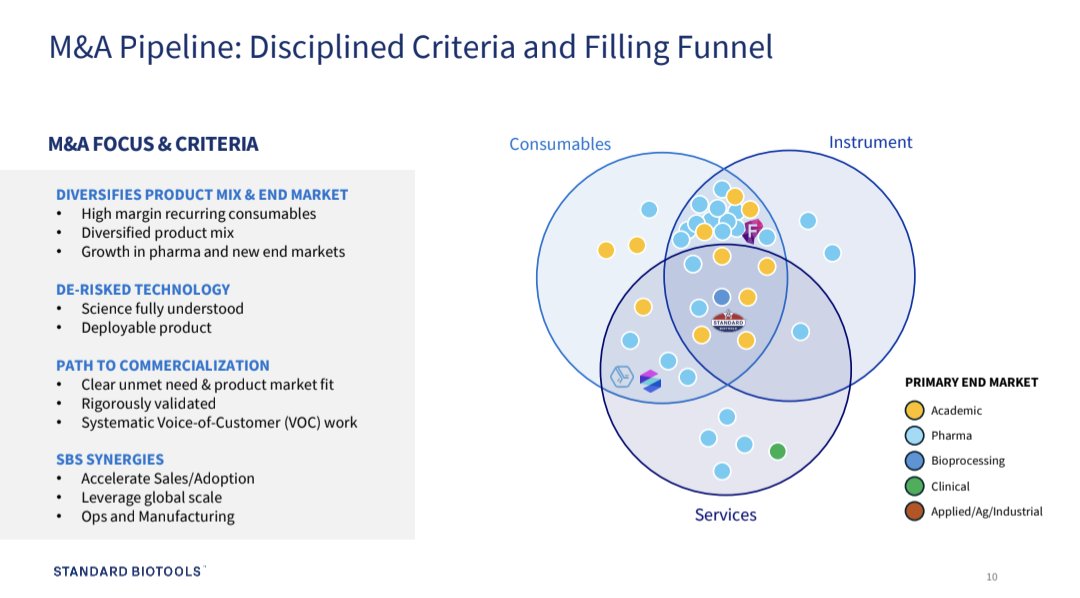

Any $lab owners out there? Standard Biotools, f/k/a Fluidigm, was recapped by Viking and Casdin in April ’22 after a failed sales process. Viking/Casdin backed a private vehicle led by Dr. Michael Egholm (former CTO of Danaher LS) to build a platform for high-impact, sub-scale tools. Their first deal was injecting $250m to reset the business and pursue M&A. 1/

@xiangtaner Couldn't really speculate. They can go in a lot of directions from here. They disclosed a small stake in a VC backed co last Q, otherwise very little info on targets.

@unciacapital@rsandler21969 I cold emailed @rsandler21969 as a badger alum ~15 years ago to get advice on how to break into investing. He was one of the few alums who called me and was super generous and helpful. Thanks Ricky, great run.

Hard to lose money *permanently* - we're down to 98 cents, 30-35% discount to cash per share inclusive of 2026 burn. Exiting '26 at breakeven on flat revs and already operationalized cost outs.

The key factor is what do they buy and could they destroy so much value via M&A that the margin of safety erodes? I think unlikely given the depth of their pipeline, years of cultivation, the multi-year slog in LS tools putting pressure on balance sheets and bringing in bid/asks.

More likely they buy cash burning tools that take time to work to breakeven, and valuation remains depressed through the digestion period. This sideways case is my downside case, I can't imagine capital impairment from these levels.

I think their experience with Somalogic will push them towards underwriting where the cost outs / lean outs do the heavy lifting.

$lab

I agree with your take. I think the most interesting part of this set-up is that you can kitchen sink their guide and still get to $7-8 per share in 2029.

Assumptions:

-HA revs decline $20m and stay flat

-Dev rev small step up, then flat

-Base FF ~inflation like growth -7m lost customer

-Alcon contracted step-up is pushed out and feathered in through '30

-ZERO Phase III trials converting

-ZERO new business

Gets me to ~$160m in revs / $36m in EBITDA in 2029. Implies only 35-40% utilization and thus a higher multiple would be appropriate to compensate for the under utilized lines. But even 15-17x multiple gets you to $7-8/share. + a call option on execution to their base case.

@TheNarrenschiff@DivinelyLevered They also have 8 Ph III programs? And a commercial base business with contracted step-up. One med-device program with higher PoS that could do +$25m in revenue by 2030...you can really kitchen sink this thing and still get to $8-10/sh.

@FundamentEdge I built a risk dashboard with Claude code today. Fetches broker and price data, charts p&l by name, flags anything outside of risk parameters I set…vscode is my go-to, very easy once set-up.