“There are two kinds of forecasters: those who don't know, and those who don't know they don't know.” John Kenneth Galbraith

No amount of sophistication can allay the fact that all of our knowledge is about the past and all our decisions are about the future." Ian Wilson

[Zf]

MCKINSEY PUT A NUMBER ON THE NUCLEAR COST GAP. THE US BUILDS AT 2.4X SOUTH KOREA. FRANCE, 2.9X.

WHERE THE GAP COMES FROM

· MGI's levelized cost benchmark puts South Korea at $65 per megawatt-hour for a Gen III+ reactor, with China essentially on par at $63, the UAE at $79, the United States at $154, and France at $190.

· Construction is the biggest driver, adding $50 to $60 per megawatt-hour in the US and France versus Korea, with US construction labor about 80 percent more expensive adjusted for productivity and US concrete prices 200 to 250 percent higher.

· The report's proof point for closing the gap is Barakah, where a Korean-led consortium building four identical APR1400 units with the same Tier 1 suppliers cut costs roughly 40 percent from the first unit to the fourth.

· The US currently has no large reactors under construction, while MGI's net-zero scenarios show global nuclear capacity doubling or tripling to as much as 1,200 gigawatts by midcentury.

OE READ

The gap is not technology, since everyone in the comparison is building Gen III+. It is program structure: design frozen early, the same suppliers unit after unit, and serial builds that let learning compound. That makes Barakah the most important data point in the report for the planned AP1000 fleet, because 40 percent compression is real, but only for programs disciplined enough to stop redesigning mid-build.

If the cost gap is execution rather than physics, what would it actually take for the US to run a Barakah-style program?

After reflection, this new narrative by Palantir is probably much more consequential than people may assume.

Palantir is basically being the canary in the coal mine announcing the death of two major assumptions propping up the US economy right now:

1) that AI labs will be able to extract significant economic rent - as opposed to AI models being mere commodities

2) that other countries can accept structural dependency on US technology and services without pushing back on sovereignty concerns

Why are Palantir specifically starting to be vocal about this?

First off, major middle-powers, even US “allies”, are one by one showing them the door. In June, France announced that the DGSI - its domestic intelligence agency, which had relied on Palantir since the 2015 Paris attacks - would replace it with French firm ChapsVision, with Prime Minister Lecornu explaining (https://t.co/SLhEGprBZC) that France “cannot accept new strategic dependencies in the digital sphere” and shouldn't depend on the goodwill of companies “capable of turning off the tap.”

Germany moved even earlier: its domestic intelligence service, the BfV, also selected ChapsVision over Palantir (https://t.co/pDZVj4SYUY), and the German military has said it will no longer use Palantir at all. Then, just this week, Spain instructed state-controlled companies - including strategic firms like Telefónica, Indra and Navantia - to avoid signing any new contracts with Palantir (https://t.co/0ik4UAFrT7).

Even in the UK, Washington's most loyal vassal, the NHS's £330 million data contract with Palantir is under review following parliamentary pressure (https://t.co/uJl6g4BMsW), and London Mayor Sadiq Khan blocked a proposed £50 million Palantir contract with the Metropolitan Police.

Palantir making a lot of noise around them caring about sovereignty makes a lot of sense: it's damage control since they keep being told they're a sovereignty risk.

I doubt it will work - because it's true: they are a sovereignty risk - but the fact that they feel the need to be vocal around this tells you where the wind is blowing: they're not shaping the narrative, they're reacting to one they're losing.

What they're saying against closed-source AI (basically a broadside attack on OpenAI and Anthropic), is again highly self-serving. Palantir's sudden love of open-weight AI models conveniently coincides with them launching 2 days before a partnership with Nvidia to sell exactly that: open models models (NVIDIA's Nemotron) in sovereign environments.

So it's essentially a product launch.

It doesn't make what they're saying wrong: it is factual that the value proposition of closed-source AI labs looks increasingly unsustainable. I mean: you're paying 10X the price of Chinese open-source AI models for something that's not really better (or just marginally) and on top of that you have zero control over your data, or the models themselves.

When Palantir says that "the architecture that maximally preserves sovereignty is one that enables institutions to own their tribal knowledge, and to compound it as alpha," they're right. I'd add that this also means you shouldn't trust Palantir either with that "tribal knowledge"... they obviously left this part out 😉

When you take a step back, these two things have major implications on many other US companies.

SpaceX - which just went public at the largest IPO valuation in history - is one clear example as I describe in my latest article on the new space race with China (https://t.co/JK3ELAyEVO).

If countries like France concluded with Palantir that they couldn't depend on a company “capable of turning off the tap” when it’s merely analyzing their data, what should they conclude about a company that aims to literally control their entire connectivity - at one man's whim, from space?

What percentage of SpaceX's crazy market cap is based on the assumption that foreign governments will not do to Starlink what they're currently doing to Palantir?

And SpaceX - or Palantir - aren't alone: a significant proportion of the top US tech giants, who rose in a world where no one questioned American technological hegemony, now face an environment that's much less conducive to the kind of lock-in their business models - and valuations - depend on.

When you pair this with the fact that it increasingly looks like the US made a wrong bet with closed-source AI - an extremely expensive wrong bet - the picture that emerges is of a country that bet its economic future on two things - proprietary AI and captive allies - and is losing both at the same time.

And to compound the problem, it doesn't help that the official narrative of the US government - via the voice of Jacob Helberg, the Under-Secretary of State (https://t.co/Z1rotPl9Ee) - is to be vocally opposed to "AI Sovereignty": essentially telling everyone "you know what, your worst fears are real, our tech companies are really out to undermine your sovereignty."

Read Helberg's post (the one I linked) and put yourself in the shoes of - say - a European or Asian leader and ask yourself how you'd react to being told that building your own AI capabilities is "marching in perfect formation into the past," that your pursuit of sovereignty is really just "synchronized mediocrity," and that your only path to the future runs through American technology.

If it was me in a position of power, I'd read this as a massive wakeup call: when another country's official position is that your sovereignty is a problem, history says you're about to need it.

So yes, it looks like - unexpectedly - Palantir, of all companies, is being quite the canary in the big tech mine. Yes they obviously do this for self-serving and cynical purpose, and yes they're of course also very much part of the problem and not the solution. But it doesn't make them wrong: sometimes it takes a vulture to tell you something is dying.

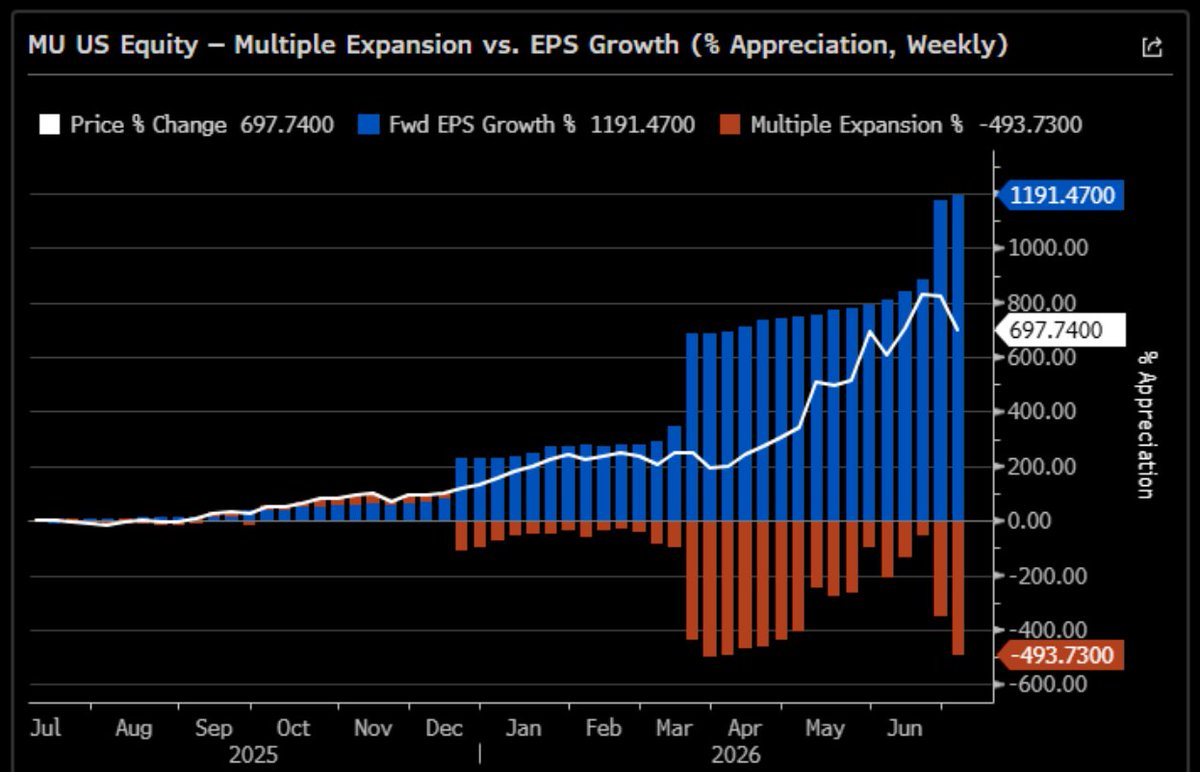

2/ Micron Valuation

1) Forward P/E vs SPX and SOX

MU's forward PE has compressed sharply from ~47x in late 2023 to ~6.7x today as earnings estimates have surged far ahead of the stock price; relative to both the S&P 500 and the SOX median, MU now trades at a historically deep discount — a pattern typical of memory names at peak cycle, where the market prices in mean reversion.

2) Multiple Expansion vs. Earnings Growth

Virtually the entire ~+700% price appreciation over the past year has been driven by forward EPS estimate revisions (blended forward EPS up ~+1,190% from the start of the period), with multiple contraction acting as a persistent drag — the market has consistently discounted the durability of the earnings cycle even as estimates have continued to rise.

👨🏫I hope U understand the significance of this historic break-out of the monthly Long-term contract #Uranium price to a level never seen before.📈⬆️💥

The Long-term price reported by the 2 #Nuclear fuel consultants TradeTech & UxC is the lowest supply contract offer price by a seller within each reported month. That price plateaued in 2007 & 2008 at $95 and now TradeTech is reporting their June 2026 Long-term price at $97, the highest ever reported since Uranium began trading!🌋😎

🧾The Long-term market is where 85% or more of uranium procurement is transacted between producers and Nuclear utilities under signed supply contracts, as opposed to the Spot market which is primarily for making small discretionary purchases and the daily swing trading of small lots between traders trying to pocket small profits on price volatility.🔃

Hence, the Long-term price is our primary supply vs demand gauge, confirming through its steady rise to a new all-time high that we are indeed in a structural supply deficit.📈↕️🌡️ We wouldn't see Nuclear utilities signing fixed-price contracts at $97 and above if there was no supply deficit!⚠️

Now that Spot Uranium traders are seeing that fuel buyers are willing to pay over $95/lb in the term market, they will begin moving the Spot price up to at least $95 to capture significantly higher profits from the material they currently hold.🤑 We saw the Spot price get ahead of the Term price by spiking to over $100 and now the Term market is catching up to that $100 level, so it is only a matter of time now before the Spot price races to catch up and likely pass the Term price in the coming months and years.🏎️🔥

The supply deficit is confirmed, the price trend for both the Long-term and Spot Uranium prices is pointing to far higher prices incoming amid soaring demand and faltering supply.↕️🗜️ That will drive U mining stocks higher, also to levels far higher than in the prior bull market that peaked in 2007/2008, imho.📈 Good luck!☘️🌈💰🤠🐂

I scored every wall street upgrade and downgrade since 2011. sector-adjusted, held week by week.

Trade JPMorgan's ($JPM) calls and you're red for 12 weeks straight. doesn't dip and bounce, just bleeds. Argus and Wedbush right there with em.

Stephens and BTIG go the other way and compound past +2%.

The bank with the biggest research desk on the street has the worst calls on the board.

This chart provides some good context for where we are today. You can see a few anomalies on the chart.

Two examples include 2018 and 2020. In 2018, failed expectations of material inventory draws in Q4 2018 led to the largest long liquidation in money manager positioning in history.

In 2020, massive demand destruction led to a supply glut that quickly translated to much lower oil prices down the road.

Today, the market is essentially pricing in builds to reverse from 1.05 billion bbls (expected) back to 1.2 billion bbls in the US.

Over the past 6 months Chinese households have paid off CNY 253bn a month ($32bn). That's the annual equivalent of 2% of GDP.

At the same time private investment is shrinking at a record pace and the rate of retail sales is at a record low (ex-pandemic).

These would be catastrophic numbers in any normal economy. But China is growing at 5%...yeah, right.

For those of you curious, these threads don't exist for the purposes of dunking later.

One of the biggest utilities I have found with X that has stood the test of time (and a top reason I even keep this active anymore) is there are rare moments where we get what I call "The Pile On."

1/7

This Saturday marks the 125th anniversary of the Panic of 1901. In a rampant bull market coming out of the recovery from the panic in 1893, steel, iron, and railroad companies began to make huge advances on the exchanges.

In an effort to gain voting control of the Northern Pacific (NoPac) Railway, JP Morgan and James J. Hill, the president of the Great Northern Railroad, began buying blocks of NoPac on the open market. But they weren't the only ones looking for control of NoPac.

Edward Harriman, president of the Union Pacific Railroad, also wanted to control the company.

The result was an all out battle of attrition to see who could throw more money at the stock for ultimate control. In early May, JP Morgan and Hill won control and announced they would merge together NoPac, the Great Northern, and the Burlington railroad, three of the largest railroads of the day.

Traders had been selling the stock short on its relentless march upwards, believing the stock to be far overvalued. On May 6, 1901, they collectively saw their financial souls exit their bodies and rise up to the great brokerage in the sky when NoPac shares erupted skywards nearly 20% the day the merger was announced.

Sensing the impending doom, investors and traders sold, or were sold out of other positions in an effort to shore up capital to pay for their exorbitant losses in NoPac. But the carnage had only just begun.

The very next day, May 7, 1901, the stock rose another 12%. The day after, it reached 25% higher intraday. Then, on May 9, 1901, the wildest day that Wall Street had seen in its 100+ year history to that point caused sheer panic and pandemonium as shares of NoPac, which traded as low as $16 in 1898, and closed at $160 the prior day, reached highs between $700-$1000 in some transactions.

Short-sellers, desperate to save their financial lives, were willing to buy back their borrowed shares at almost any price. The chaos sent shares of many other stocks down violently. The higher NoPac soared, the lower other stocks fell.

US Steel, which had only began trading as the most valuable company in the world just over a month earlier, saw its value drop over 45% intraday.

While the bull market didn't completely die that day as stocks like Missouri Pacific and General Electric soon reached new highs, most stocks didn't have a significant rally for a number of years. US Steel eventually collapsed to $7 in 1904 before returning to a strong rally but it didn't make a new high until 1908.

The corner of NoPac essentially marked the end up the bull market in spectacular fashion. The bull market of 1897-1901 was also the last great railroad-driven speculative boom on the exchanges. All future bull markets would be dominated by industrials like steel, copper, automobiles, and others.

There are many periods in history where improving jobs coincided with higher rates and falling stock prices. What we’re seeing in the interaction between stocks and rates in recent years isn’t a new normal, it’s the old normal (ie pre-1998).

One of my rules: don’t look at the chart when it’s at the bottom, focus on fundamentals. Don’t argue about fundamentals when it’s at the top, focus on the chart.

This, as margin debt is soaring, levered ETF are seeing record inflows, P/C skew is blowing out and equity positioning reaches multi-decade highs (cash at ATL's)

What could go wrong

FT: "Goldman Sachs analysts are predicting total US equity supply of $1.175t in 2026, consisting of $225b of IPOs, $450b of other corporate stock sales, and another $500b gradually dribbling out from corporate executives and early investors in the IPOs...This has understandably led to fears that the market could suffer severe indigestion. Even one of these big IPOs could be enough to cause a mild case, but the combination could prove painful. That big IPO years tend to presage big downturns has exacerbated those concerns."

As I dissected in my February report on "Price Discovery" (https://t.co/kEx5Z4BJH7), relative market resilience since the GFC has been in part predicated on passive investing reducing equity supply against persistent demand. Less AUM in the hands of active managers means fewer shares traded based on price moves. Meanwhile, passive flows have stayed constantly positive. This has reduced the elasticity of stocks. To quote an Economist recap of one study into this:

"The paper, by Xavier Gabaix of Harvard University and Ralph Koijen of the University of Chicago, sets out their 'inelastic-markets hypothesis.' This contradicts the textbook argument that money flowing into stocks should barely raise prices, since if it did, demand would fall and return prices close to their starting level. In fact, the paper’s authors find that stock market demand is not 'elastic' in this way. It is inelastic, and does not fall much as share prices rise. As a result, an investor who buys $1-worth of stocks using fresh cash (or the proceeds from selling other assets such as bonds) pushes up aggregate market value by $3-8…Most important, funds that maintain fixed allocations can push up prices. Suppose you exchange cash for new units in a fund promising to keep 80% of its assets in shares. The number of shares in existence does not change, but demand for them has risen. The fund can buy shares from another type of investor, but in practice flows between investor groups are low. (This also implies inelasticity, since if demand were elastic, groups with different beliefs, about future earnings, say, would act differently, boosting trading.) The only way to put the cash to work, if all similar funds are to also meet their mandates, is to buy fewer shares at a higher price."

Which, of course, begs the question: what will a flood of new supply mean if demand doesn't spike to meet it. Difficult question to answer given we've not seen an IPO wave of this scale at a time when passive vehicles control this much AUM. I'll be digging in for answers in the days and weeks to come. But as I warned in the report: "The benefits of inelasticity on the upside could do the equal and opposite on the downside."

Learn more about Sage Road Research here: https://t.co/Wgwz2xnvR6. Interested in subscribing? Message me.

FT link: https://t.co/0mb9o48ZWR

Useful information for anyone betting real amounts on Polymarket. You have to be correct to win, but also you need to hope you don't get rugged. Too much bullshit / unmeasurable risk on that platform.

Correct. And just like the shale boom, the entire industry is stuck in a prisoner’s dilemma where every player must keep spending or risk beeing seen as a laggard in the race to zero

If you want to visualize the next decade of big tech returns, just plot the $xle from 2012 - 2021