Primarily a fundamental investor running my own book. Mix in Macro and technical trades for alpha generation and hedging. All opinions are my own dyodd.

@mzahara@Convertbond@elonmusk@DOGE Wait till tax revenue collapses now as well. Literally 100’s of billion in capital gains gone as well. What a brilliant strategy.

One illustration of this. Both of these trailers were completed in the last couple weeks

Customer: Trimac

On the left: Advance Engineered Products Group

Made in Drummondville, Quebec 🇨🇦

On the right: Polar Tank Trailer

Made in Holdingford, Minnesota 🇺🇸

This feels like puking. Need to make moves on a day like today. Here are a few moves I've made:

1. Sold REITS in registered accounts I've held for years.

2. Bought $META and $AMZN

3. Closed my eyes and bought $SHOP and $RH

Ugly, but you have to make moves for the long term.

$tvk.to $trrvf

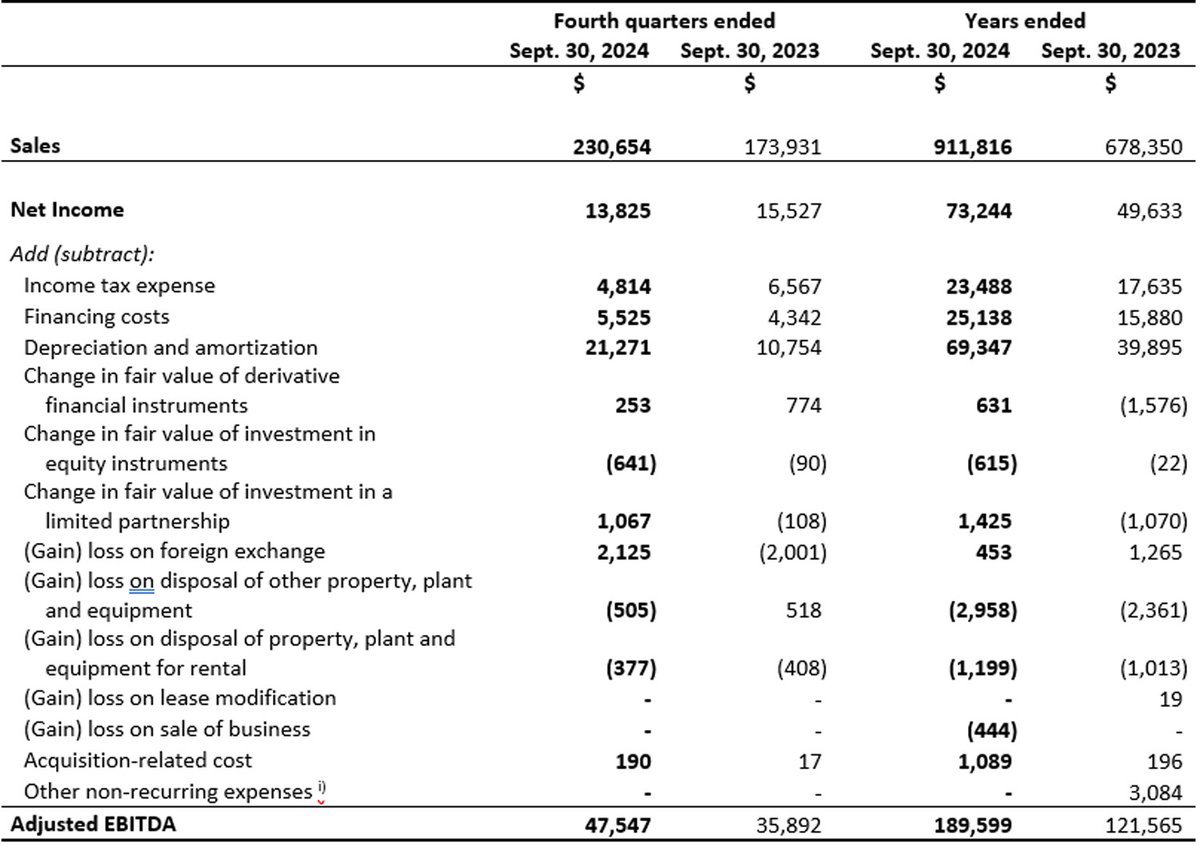

Key Observations (Amounts in Millions):

Sales Growth:Quarterly: Sales grew from $173.9M in Q4 2023 to $230.7M in Q4 2024, a 32.6% increase.

Annual: Sales jumped from $678.4M in FY2023 to $911.8M in FY2024, a 34.4% increase. This reflects robust top-line growth.

Net Income:Quarterly: Net income decreased slightly, from $15.5M in Q4 2023 to $13.8M in Q4 2024, down 11%.

Annual: Net income increased significantly from $49.6M in FY2023 to $73.2M in FY2024, up 47.5%, indicating strong profitability improvement over the year.

Adjusted EBITDA:Quarterly: Adjusted EBITDA grew from $35.9M in Q4 2023 to $47.5M in Q4 2024, a 32.4% increase.

Annual: Adjusted EBITDA surged from $121.6M in FY2023 to $189.6M in FY2024, an impressive 55.9% increase, reflecting strong operational efficiency.

Cost Drivers:Higher depreciation and amortization and financing costs contributed to the slight quarterly decline in net income.

Non-recurring items like acquisition-related costs and foreign exchange (FX) changes were relatively minor but should be monitored.

Updated Bullish Factors:

Annual performance is highly bullish: Revenue, net income, and EBITDA all grew significantly.

Operational improvements: The EBITDA margin appears to be improving, reflecting better cost management and scaling.

Quarterly performance still positive overall: Despite a slight dip in net income, revenue and EBITDA grew significantly, indicating that the core business remains strong.

Concerns:

The quarterly dip in net income suggests some short-term pressures, likely from rising costs.

The reliance on adjustments (e.g., depreciation, fair value changes) to highlight profitability should be evaluated over time.

Final Verdict:

The company’s financials indicate a bullish trend, driven by strong annual growth in sales, net income, and Adjusted EBITDA. The slight quarterly decline in net income is a minor concern in the broader context of its strong annual performance. If the company can address cost pressures, it could sustain this momentum.

$CL I've added some Crude Calls out to January. I'll keep trading this range of roughly 68-72 until it moves one way or the other https://t.co/9WWJ16eu6S

$CL Oil spiked on news of potential Iran retaliation. I exited this position with a nice gain. I've found that selling on rumor has been the right trade the last 6 months. May consider adding if price pulls back. https://t.co/3J3aIw7lnk