GM Builders,

We're thrilled to announce that our 3rd annual Web3 Builders' Summit is coming back to Da Nang this summer. 🇻🇳

With the recent regulatory shifts and crypto market gaining new momentum, this is the moment for local and global builders to connect, BUIDL, and prepare for the next phase of Vietnam's Web3 ecosystem.

But that's not all we're grinding on in Da Nang this May.

true structural edge usually hides in absolute simplicity. retail traders spend their capital optimizing complex indicators and chasing high frequency macro noise, completely ignoring the fundamental baseline.

Peter Lynch is pointing out the only variable that actually dictates expected value over a long time horizon.

in a market obsessed with narrative and short term sentiment, the raw generation of cash flow is the ultimate truth. earnings are the gravitational pull of asset pricing.

You either build your strategy around the deterministic reality of earnings, or you overcomplicate your execution until you become exit liquidity.

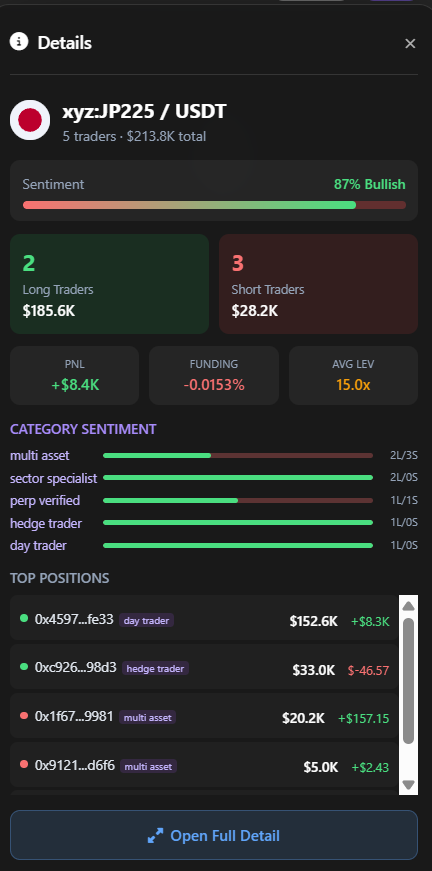

Data on @zonein_xyz reveals exactly how massive capital frontruns central bank liquidity. while a few retailers are attempting to short the market, smart money wallets have absorbed almost the entire long side of the Nikkei.

retail traders look at the Bank of Japan struggling to normalize interest rates and try to fade the ongoing equity rally.

the smart money looks at the exact same macro setup and realizes you do not step in front of a sovereign liquidity hose.

by aggressively stacking longs, these whales are forcing the smaller shorts to absorb the pain of a trade that is structurally supported by a weak Yen and accommodative monetary policy.

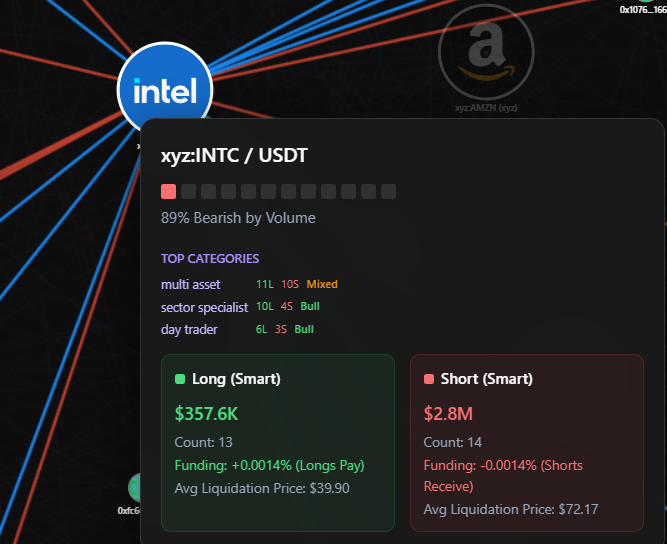

the insights for Intel shows exactly how the market prices in the loss of a decade long semiconductor race. smart money wallets are attempting to catch a falling knife by stacking long positions. meanwhile, a highly concentrated group of smart money has deployed massive capital to short them into the ground.

this is the physical reality of prioritizing financial engineering over an actual technical roadmap. retail participants look at a legacy tech giant and see a mean reversion value play.

institutional capital looks at the hardware supply chain and sees a company that completely missed the modern compute cycle. the overwhelming short volume confirms that the market views this structural rot as permanent.

you either trade the reality of the physical infrastructure layer, or your capital becomes the EV for the players who know the engineering edge is dead

the gold insights on @zonein_xyz reveals a massive imbalance. a highly concentrated group of whales is aggressively piling into the short side.

while the overall wallet count leans bullish, the capital flow tells the actual story.

>62% of the total volume is heavily bearish. heavy capital has stacked >$40m into short positions, overpowering the $24m on the long side.

These heavy shorts are already capturing significant yield. The short side is sitting on $369k in PNL, while the long liquidity continues to bleed out.

Smart money is positioning with massive conviction against the broader crowd.

while protocols spend millions auditing smart contracts to protect their yield, state actors are simply frontrunning the security layer by infiltrating the human capital supply chain.

this is an asymmetric attack vector with massive expected value. the DPRK is not brute forcing the network from the outside.

they are exploiting the information gap in remote work to position themselves directly inside the execution layer.

they learn your infrastructure, map your bottlenecks, and orchestrate the exploit from within. Tether freezing a payment address is merely a reactive latency check, not a solution to the structural rot.

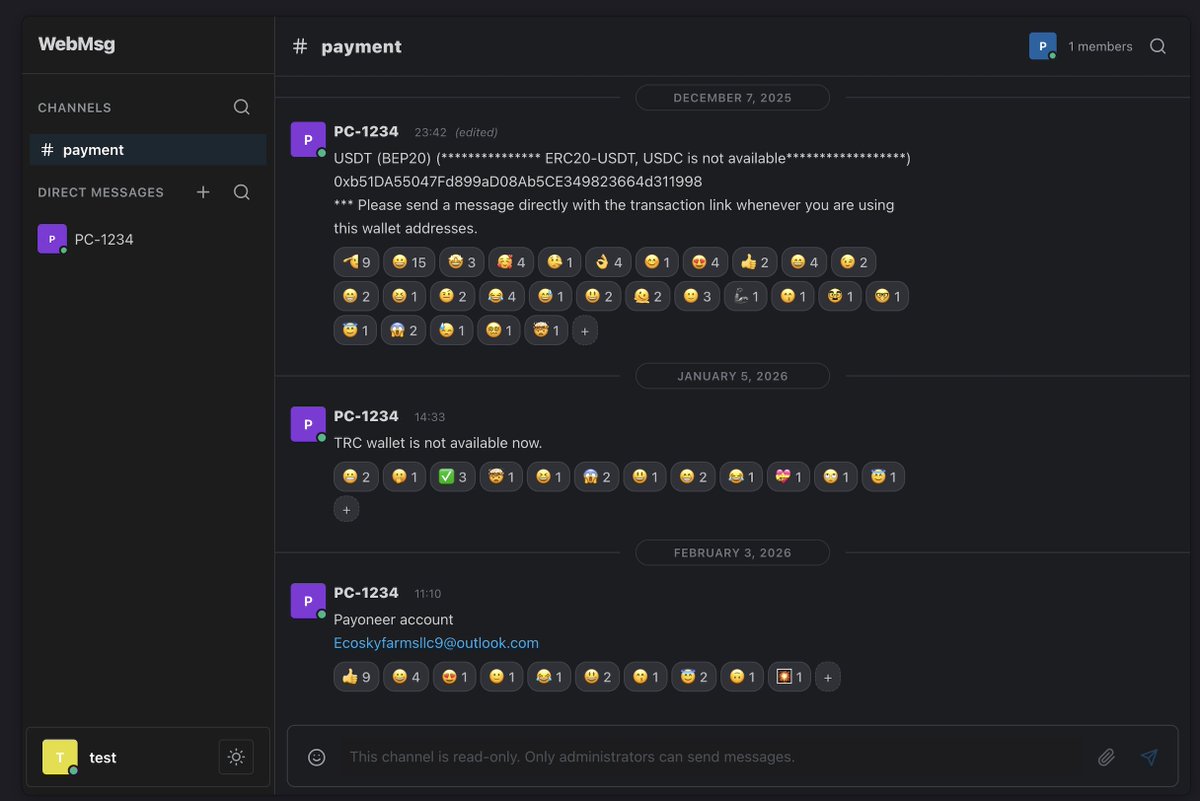

1/ Recently an unnamed source shared data exfiltrated from an internal North Korean payment server containing 390 accounts, chat logs, crypto transactions.

I spent long hours going through all of it, none of which has ever been publicly released.

It revealed an intricate ~$1M/month scheme of fraudulent identities, forged legal documents, and crypto-to-fiat conversion.

Enjoy the findings!

this confirms the liquidity vacuum has finally flushed the macro tourists out of the ecosystem.

what looks like a bear market is actually a brutal but necessary structural reset of the supply and demand for venture capital.

founders clinging to obsolete valuations are fundamentally mispricing their own equity. When easy money disappears, technology and first-mover status immediately revert to their true value as mere commodities.

the severe pessimism around tokens is simply the market realizing that printing a governance asset does not fix broken unit economics.

the only teams surviving this drawdown are the ones treating crypto as a harsh business environment rather than a perpetual motion machine for early stage fundraising.

EthCC 2026 Takeaways 👇

VC and Fundraising:

• Extremely low VC attendance, used to be the biggest crypto VC event just 1-2 years ago

• >90% of founders are out of touch with valuations (still) - hurting their fundraises

• We're in the early innings of startups and VCs not being able to come back to market expect another 6-12 months of this

• VCs with Fund 2 and above are raising relatively well in Europe, LP interest is still here

Founders and Builders:

• Many OGs have left. The ones still around are either building or involved with the most interesting projects

• The best teams are uniquely balancing an ambitious long-term vision with a practical bear market GTM

• Tech and first-mover advantage are not moats anymore - I still get pitched this by a lot of founders

• People are extremely bearish tokens - tend to agree although some of the best products that haven’t been built yet will still have tokens imo, pessimism seems overblown

Crypto x AI

• Agents are still early but showing promising signs of generating higher yield than regular DeFi products

• Critical infrastructure is being built that is necessary for its future growth

Ethereum ecosystem:

• There’s still a lot of people building startups in the Ethereum ecosystem - remains to be seen if these builders are business-oriented enough to make it work

• DeFi in Ethereum is clearly working and is here to stay long-term - almost all of the best early-stage teams are working in this category

• EF Founder success team has done a great job with providing ecosystem support - the foundation needs to focus more on this or else projects will migrate

Overall, I’m cautiously optimistic on the Ethereum ecosystem. Only serious people are left. The market is forcing better ideas and more valuable / sustainable products.

The best teams are taking the biggest swings, hungry to win, look / feel institutional and are finding early traction with extremely limited resources - good signs of long term durable businesses.

If I missed you at @EthCC and you’re keen to pitch us @frachtisvc, send me a DM

ZachXBT is exposing the exact compliance arbitrage that institutions use to virtue signal while ignoring market realities.

Everyone assumes stablecoins are neutral infrastructure, but the actual mechanics of censorship are asymmetric and completely dependent on back office risk models.

Tether operates like a highly responsive execution engine. They froze the Lazarus Group funds immediately because their protocol prioritizes operational speed over optics.

Circle is playing a different game. They are optimizing for traditional finance integration, which ironically paralyzes their ability to act during a live exploit.

By hesitating on a massive 1.5 billion dollar hack, Circle effectively became the latency layer that allowed state actors to route stolen liquidity out of the system.

Decentralization is a marketing term. In reality, your capital is only as secure as the centralized counterparty willing to flip the kill switch.

You either understand the underlying incentive structures of your stablecoin issuer, or you are simply providing the exit liquidity when the exploit happens.

1/ Welcome to the Circle $USDC files.

$420M+ in alleged compliance failures since 2022, including fifteen cases of the US-regulated stablecoin issuer taking minimal action against illicit funds.

the global financial system is a deterministic machine built to farm your idle capital

the public is distracted by token volatility while the actual players are fighting a quiet war over the risk-free spread

treasuries are currently yielding around 3.89 percent, yet legacy banks only pass on 0.39 percent to everyday savings accounts.

the banks simply pocket the massive difference. When stablecoin issuers attempted to pass that native yield directly back to holders, regulators stepped in with the GENIUS Act to explicitly ban it.

this is a state-sponsored blockade designed to protect the fractional reserve banking model from a structural funding collapse.

now, traditional banks and crypto firms are racing to control the exact same digital infrastructure from opposite ends of the regulatory spectrum.

Stablecoin issuers have become one of the largest holders of U.S. treasuries.

Treasuries pay close to 3.89%, the average savings account returns 0.39%, but banks keep that spread.

The GENIUS Act already banned issuers from passing yield directly to holders, and regulators keep expanding those restrictions to cover the workarounds that have emerged since.

Meanwhile crypto companies are going after bank charters and banks want to issue their own stablecoins. They're all building toward the same financial infrastructure from opposite ends.

Charlie Munger called it a long attention span, but in modern market microstructure, it is simply time horizon arbitrage.

The entire financial ecosystem is optimized to monetize your impatience.

Retail traders and macro tourists play a high frequency game of noise. They constantly cross the spread, absorb latency costs, and bleed their expected value through overtrading.

They are the foolish gamblers Munger identified, driven by the dopamine of the next tick.

The patient investor understands that real alpha is found by extending your holding period beyond the collective attention span of the broader market.

They lock in structural advantages and let the compounding flywheel do the heavy lifting.

The market is a deterministic machine designed to transfer wealth from the hyperactive to the focused. You either extend your time horizon and solve the game, or your dopamine addiction becomes someone else's exit liquidity.

“In America they call it - Long attention span. They can keep their mind on a game for a long time until they’ve solved it.”

"The world is full of foolish gamblers and they will not do as well, as the patient investor.”

- Charlie Munger. 2018

Most of yall look at Elon Musk and see a tech guy.

A quant looks at him and sees a masterclass in frontrunning the physical order book of an entire industry.

Stackelberg leadership in trading means sweeping the available liquidity before the momentum crowd arrives, forcing them to pay your spread.

By locking up the capped supply of TSMC packaging and Nvidia GPUs early, Elon did exactly this. He widened the spread for OpenAI and Anthropic, forcing them to pay a massive premium just to enter the trade months late.

His announcement of Terafab is pure Nash bargaining. He does not actually need to manufacture a better chip than Nvidia. He just needs an outside option. In market microstructure, the player who can walk away from a toxic fill always captures the surplus. Nvidia knows he can leave the ecosystem, so they are forced to give him better allocation today.

While other tech labs trade in straight lines and burn external capital, his cross-domain flywheel across SpaceX and Tesla creates a self-sustaining compounding engine.

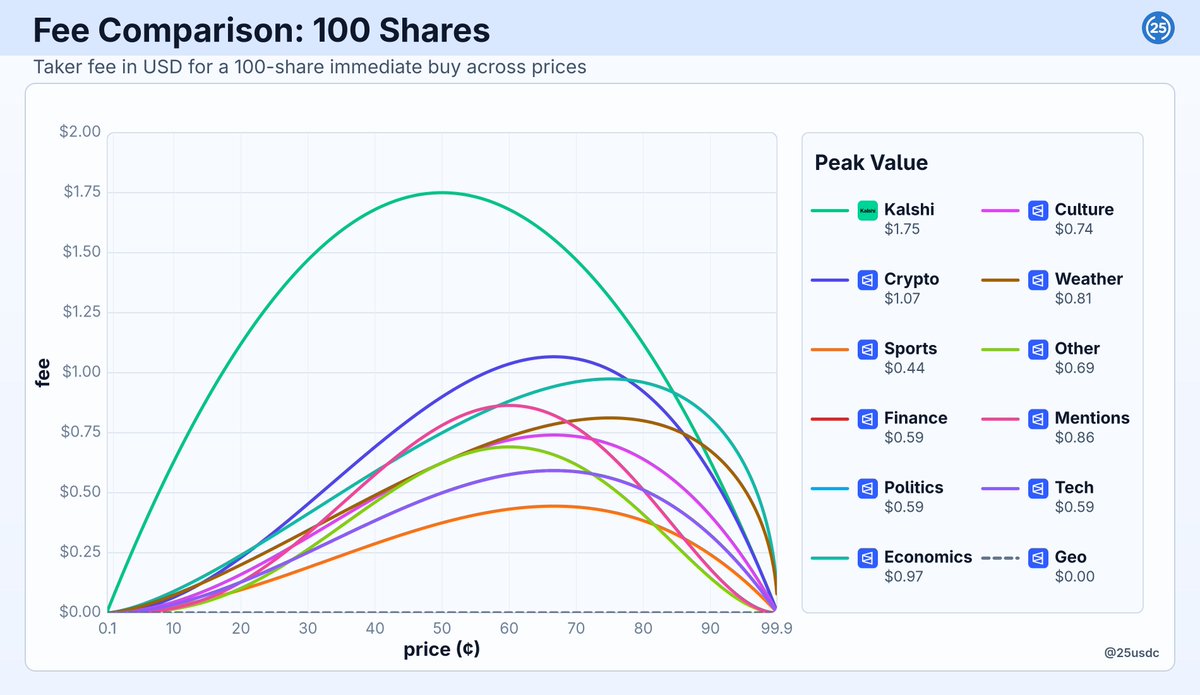

polymarket charging fees is the end of the "free ride" era for retail takers. the game is shifting toward a maker-rebate model where being the liquidity provider is the only way to earn a 20%+ return before the trade even settles.

the fee structure is designed to punish aggressive market orders while rewarding limit orders with substantial rebates.

geopolitics and global events stay fee-free for now, making them the last refuge for pure directional bets without a rake.

polymarket's fee curve is structurally different from kalshi, especially when looking at the $100 market buy impact across different price levels.

Polymarket soon charges fees

Understanding how they work is key to trading profitably

Fees apply only to takers, while makers earn 20%+ rebates. Geopolitics and global event markets remain fee-free

Here is a comparison across categories, including Kalshi (different fee curve)