Wow, the S&P Dow Jones Indices has just officially announced that they will NOT be changing their inclusion rules to make it easier for “MegaCap” companies (such as @SpaceX) to be fast-tracked into the S&P 500.

Their reasoning:

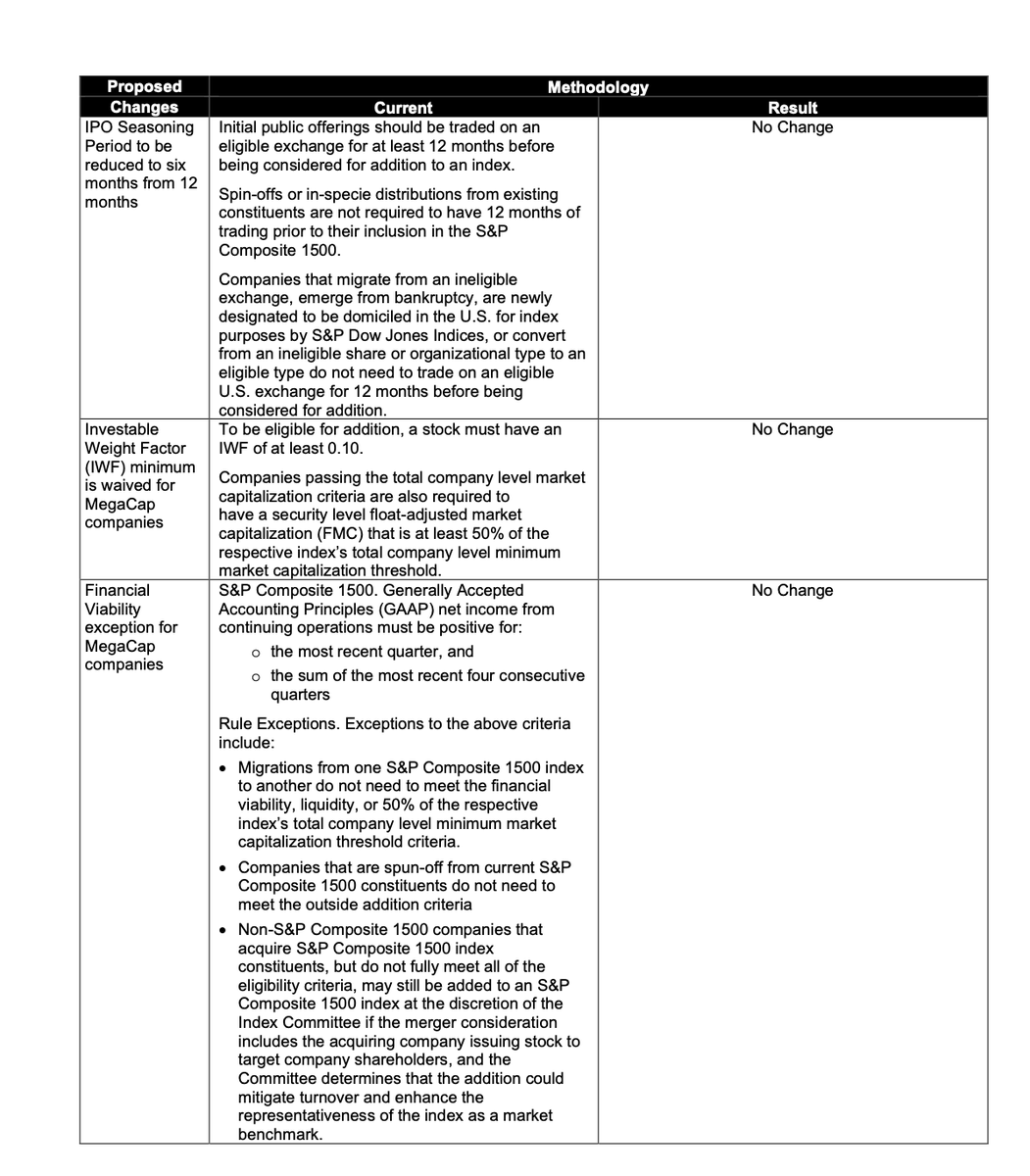

"S&P DJI determined that exceptions to the financial viability, seasoning, and IWF requirements should not be granted solely based on market capitalization. The decision not to adopt the proposed exceptions preserves core index principles by maintaining consistent application of these key requirements. Although there may be trade-offs between strict adherence to these eligibility requirements and broad representativeness, the current methodology provides substantial market coverage and sector balance. As a result, the indices can continue to meet their stated objectives while preserving their role as representative and investable benchmarks for the U.S. equity market.

No changes will be made to the eligibility criteria including financial viability screens, seasoning period, or minimum IWF, for the S&P 500, S&P MidCap 400, or S&P SmallCap 600 as a result of the S&P Dow Jones Indices consultation on the treatment of MegaCap companies. Accordingly, there will be no changes to existing methodology for this index family."

This means that the earliest @SpaceX could be eligible to be added to the S&P 500 would now be June 2027.

The requirements that will now remain in place are:

• No changes to S&P 500 eligibility rules for mega-cap companies.

• Mega-cap companies will still need to wait 12 months after their IPO before being considered for S&P 500 inclusion.

• S&P will not waive profitability requirements for mega-cap companies. The company must have positive GAAP net income in the most recent quarter, and the sum of the most recent four consecutive quarters.

• S&P will not waive minimum public float requirements for mega-cap companies. At least 10% of a company's shares must be publicly tradable ("free float").

The S&P rejected proposals that would have:

• Reduced the IPO seasoning period from 12 months to 6 months

• Waived profitability requirements

• Waived minimum public float requirements

@saxena_puru Most of his outperformance was also driven by the first four years of the fund, when it was EXTREMELY small… and when he was running triple digit turnover.

If you are having a bad day, remember that Mohnish Pabrai had 79% of his portfolio in Micron but sold the entire stake in the middle of 2023

The stock is +1400% since then

Imagine you spent 40 years doing the boring, responsible thing.

You opened a 401k at 23. You contributed every paycheck. You ignored the noise. You bought the index because Bogle told you to, because Buffett told you to, because every honest piece of financial advice for 30 years told you the index was the safest, most diversified, most rules-based way to own America.

The whole point was the rules.

The rules said: a company must trade for 12 months before joining the S&P 500. The rules said: it must show four consecutive quarters of GAAP profitability. The rules existed because in 1999 the index quietly bought a lot of stocks at the top, and pensioners paid the bill.

After the dot-com crash, S&P tightened the rules. Nasdaq tightened the rules. FTSE Russell tightened the rules.

For 23 years, those rules held.

Then SpaceX filed for IPO.

And the rules changed.

The S&P 500 waived the profitability requirement. Nasdaq cut its trading-history window from 90 days to 15. FTSE Russell cut its to 5.

Bloomberg Intelligence estimates the major index funds will absorb between 19% and 24% of SpaceX's float within six months. That's over $30 trillion of passive 401k and retirement money, mechanically buying a single newly public company at IPO valuations, because the rules said they had to.

Except the rules used to say they didn't.

Here's the thought exercise:

If you spend 40 years building a system designed to protect ordinary savers from buying overpriced stocks, and then you waive the protections the moment a sufficiently large stock asks you to, what was the system actually protecting?

Most of investing is about understanding what's a rule and what's a guideline.

A rule binds the rule-maker.

A guideline binds the saver.

You're allowed to find out which is which only after the fact.

$PETS write up by @ExpectedValues

The stock definitely has an “ick” factor to it, but imo it’s unreasonably cheap by a country mile.

https://t.co/vIaNe5QiK2

Not all of us can cook the books at a software company during the 90s dot-com bubble, sell it for $4b based on fraud, wipeout $2b in shareholder value in one day while selling our own stock at peak, get fired within six months and see our company resold for just $27M a year later

FETTERMAN CONFRONTED: “I’m a breast cancer survivor, I had a double mastectomy, and the Trump administration took my health care away… And you’re standing with him.”

Fetterman can barely talk. Painful to watch as usual.

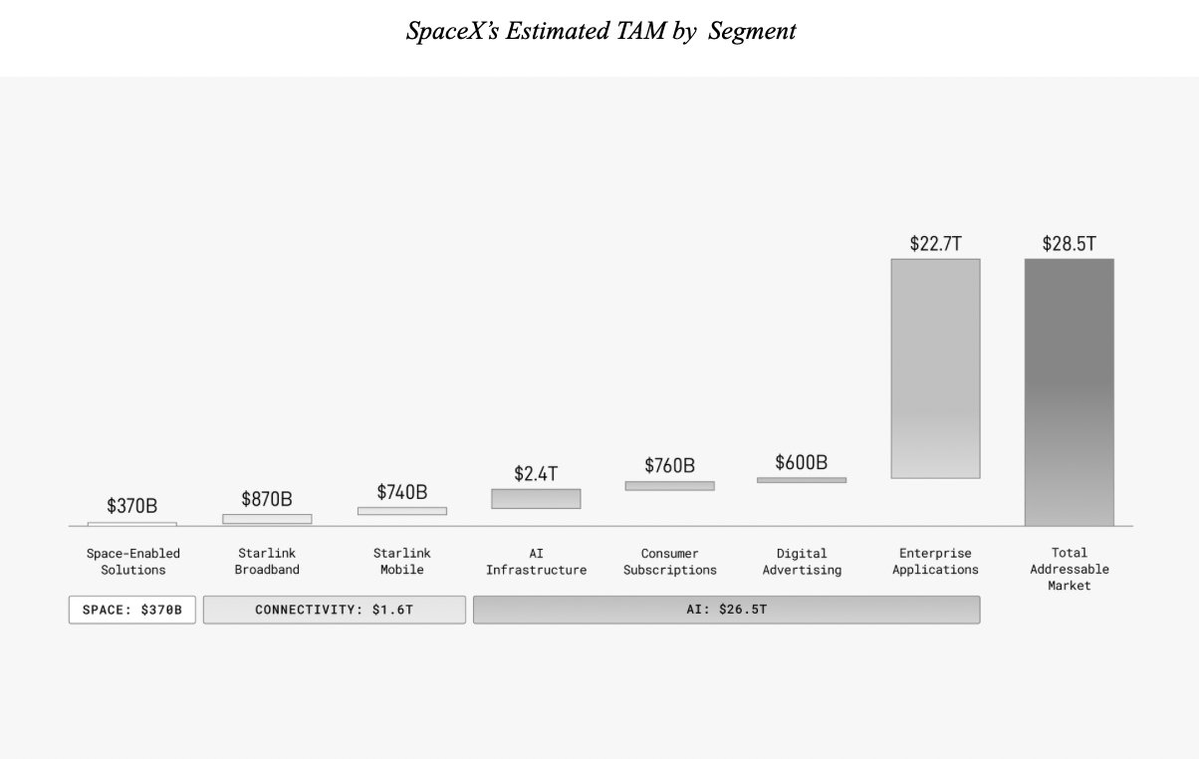

SpaceX wins the trophy for most ridiculous TAM analysis in public market history.

Saying your market is "$28.5 trillion" is the typa shit you see in F-tier startup pitch deck

There is no more effective critique of the failures of modern multiculturalism than a few days in Tokyo, immediately followed by a few days in NYC.

I will die on this hill.

Wrote about my 10 years at Disney. Mostly focused on their mismanagement of the FiveThirtyEight brand with more detail than I've spoken about publicly before. Not gonna lie, this felt kind of cathartic.

https://t.co/MedV52G2CC

What evidence is there that it works? Ackman is a nepo baby, and I'd expect him to underperform index funds absent inside information and possibly even *with* inside information given how much of a tool he is.