$CURE.AX $XBI Biotech index up over 5% this morning. Thesis continues to play out nicely

I'd expect at the index level we should test (& eventually break) the 2021 highs considering the structural tailwinds behind the sector, & now some strong reflexive momentum feeding in too

this market is very narrow. there is a lot doing very badly and a few things doing very well.

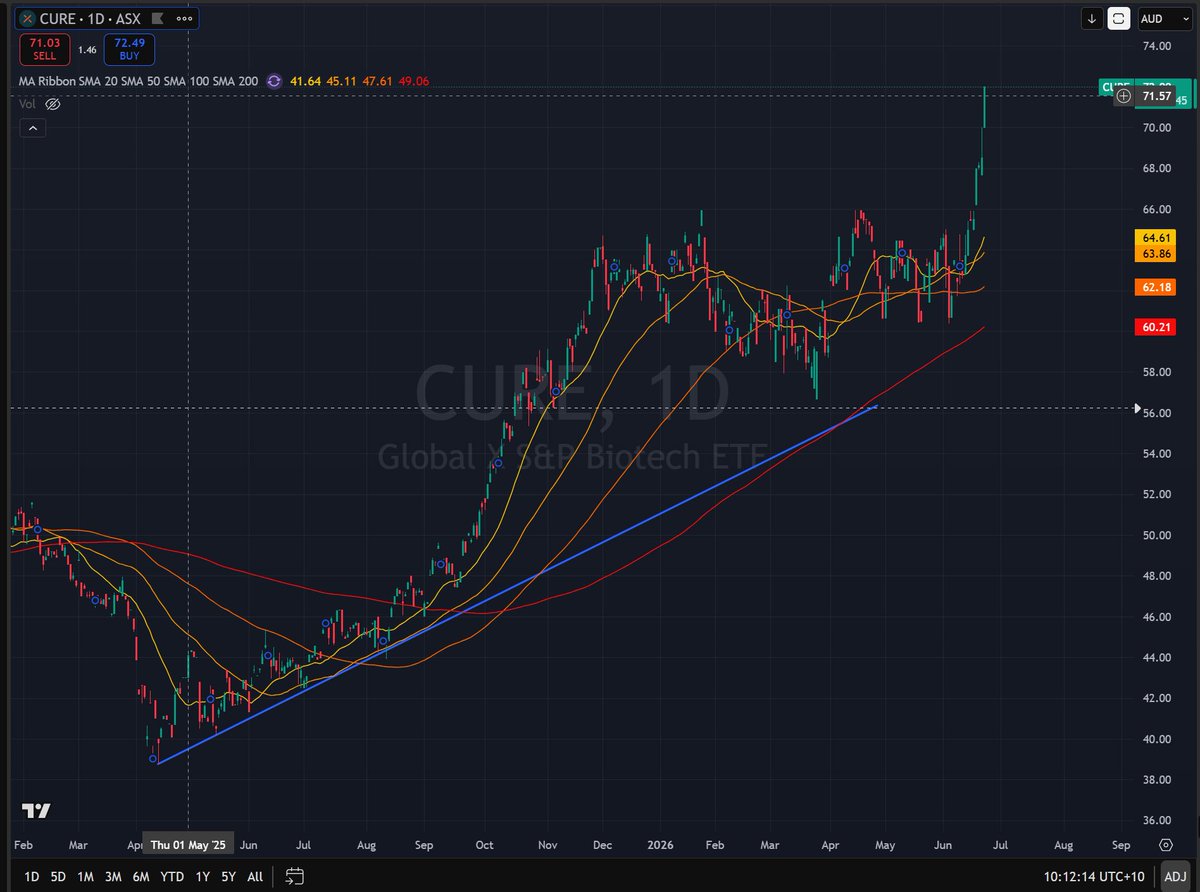

$XBI $CURE.AX biotech ripping to a new cycle high

i have no view of this from a micro level, beyond my capacity to have an edge analyzing biotechs

but from a macro level you could argue AI's true monetization frontier lies in revolutionizing molecular drug discovery, predictive healthcare diagnostics, and clinical monitoring

& so i've been happy to be long this at an index level since last year. the price action seems to be validating the simplistic macro thesis

$GLD $SLV

Goldman Sachs:

"We now expect the gold price to rise to $4,900/toz by December 2026 (vs. $5,400 previously). Our gold price views remain structurally constructive but tactically cautious with near-term downside risk and medium-term upside risk."

"Continued central bank diversification remains the main structural driver of our constructive base case for gold prices....we view the ongoing diversification trend as structural. A recent World Gold Council survey supports our view: a record 45% of the 76 central banks surveyed between February and May expect to increase their own gold reserves over the next 12 months."

token expenditure dropping -25% in the last month. it looks like $UBER & a few other high profile names put the tokenmaxxing theme to bed

$MSFT taking it a step further and potentially ramping up cheaper Chinese model collaborations (with deepseek). it was only a matter of time (at current cost) in what is becoming a commoditized product.

especially now under so much pressure to do something productive for shareholders, other than burn vast piles of cash into oblivion

implications ? $MSFT & $META, need to cut capex in order for their share prices to recover. if they can provide ai using cheaper models at a fraction of the cost, does it mean they don't need to spend as much?

yes and no, but ultimately it's the capex worries that are hurting these specific stocks & it seems like for the vast majority of ai - we probably don't need the most expensive frontier models

saying that cheaper tokens doesn't equate to less capex, as cheaper tokens can and most likely will drive an increase in usage

https://t.co/zgSITsnLHV

$ACN $IGV

brutal sell off in Accenture

This price action should send shivers down the spines of any tech services/saas investors

we really are starting to see the ai winners/losers theme playing out in real-time

Names like $SNOW, $INOD, $MDB, Cyber that might benefit from ai buildout seem to be doing ok. But others like $ADBE, $CRM, $INTU, $SAP getting absolutely crushed!

$XBI $CURE.AX biotech ripping to a new cycle high

i have no view of this from a micro level, beyond my capacity to have an edge analyzing biotechs

but from a macro level you could argue AI's true monetization frontier lies in revolutionizing molecular drug discovery, predictive healthcare diagnostics, and clinical monitoring

& so i've been happy to be long this at an index level since last year. the price action seems to be validating the simplistic macro thesis

$QOR.AX trying to get my head around this one a bit here to see if there is anything to do

see some large institutional tickets e.g. Norges Bank, Regal etc which you'd think given their resources, have put some work into this and see some value to extract around current market prices ??

the price action is pretty disgusting tbh, a crash, & now a slow death grind lower, noting some other aussie saas names rebounding quite strongly ($TNE.AX, $SDR.AX)

this chart from data trek illustrates to me how futile it would be trying to call/time tops in the market, especially when (right or wrong) we are in a capex cycle unlike anything we've seen

the only thing worse than sitting out a raging bull market, is being in it & not managing risk appropriately

deciding how much drawdown you are truly willing to take and for how long should be front and centre of your thoughts

people say they are fine with volatility. it's one thing taking a 50% hit on a portfolio, but taking that and sitting with it for a few years is a very different matter altogether

UBS analyst agreeing on the consumer trade below

Should add that a hawkish FOMC as we had overnight is not going to help anyone near term

UBS: "The risk/reward in consumer discretionary is beginning to shift from the doldrums seen as recently as two weeks ago. The SPDR S&P Retail ETF (XRT) versus front-month crude oil (CL1) suggests there is still further upside to the discretionary trade, given crude's move lower this morning. Lower yields should also provide incremental support.

Consumer staples were the second-best performing sector last week (behind materials), and I would expect some residual relief today—particularly within the household and personal care space."

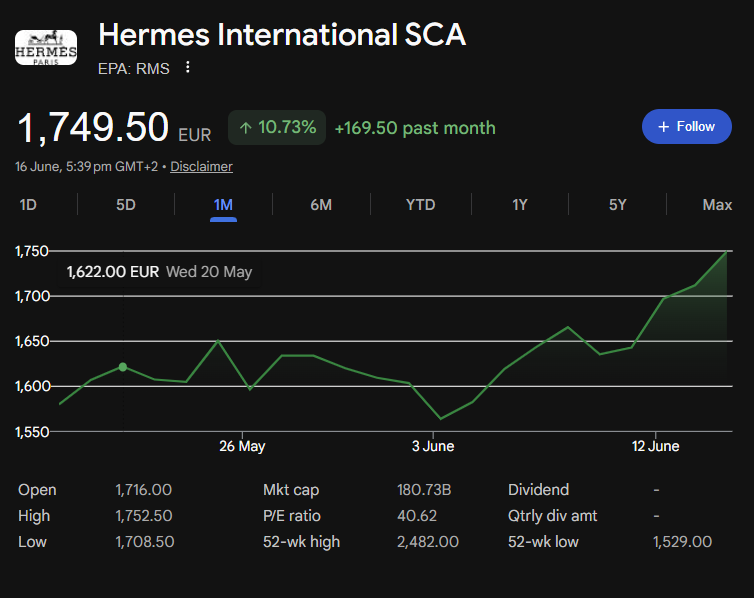

$RMS.FR a quick 10% move higher, not bad for a stock of this nature in less than 2weeks.

consistent px action across quite a number of consumer cyclical names. we now have what looks potentially like a proper exit path on Iran/US war, rates lower, oil lower

we might have some structural tailwinds coming into play for the much beaten down consumer sector

$EQR.AX one of the few Australia based stocks getting very strong attention from the global community on X. bullish push higher in the stock price today

the thesis seems mostly driven out of geopolitical focus on critical minerals and specifically tungsten in this case

financials are pretty rough to look at (on a backward-looking basis). You are not buying a proven quality here. this is high risk high octane stuff. the company has been a consistent loss-maker for quite some time.

you are betting on the future story here not the past. but seems like it might be worth more work, as you have a few things working for you in terms of narrative/catalysts,

lastly worth pointing out Oaktree Capital (Howard Marks) owns ~17% of the company and UBS took a 4.33% position in June. whether this is validation of a thesis or not is to be seen.

https://t.co/zjiE6QEvGe

$EQR.AX one of the few Australia based stocks getting very strong attention from the global community on X. bullish push higher in the stock price today

the thesis seems mostly driven out of geopolitical focus on critical minerals and specifically tungsten in this case

financials are pretty rough to look at (on a backward-looking basis). You are not buying a proven quality here. this is high risk high octane stuff. the company has been a consistent loss-maker for quite some time.

you are betting on the future story here not the past. but seems like it might be worth more work, as you have a few things working for you in terms of narrative/catalysts,

lastly worth pointing out Oaktree Capital (Howard Marks) owns ~17% of the company and UBS took a 4.33% position in June. whether this is validation of a thesis or not is to be seen.

https://t.co/zjiE6QEvGe