I spent over a decade as a professional investor at various hedge funds. There's no alpha in getting up to par with what the market already knows, and yet it still took at least a day of reading initiatings, transcripts, skimming expert calls, etc.

What if that took only five minutes, so you can focus on the alpha-generating work? I co-founded CapRelay with @luyiest (co-founder of BamSEC) to make this a reality

Introducing CapRelay, the fastest way to find and iterate through ideas

Do you want click through buy-side bull-bear debates on every US-listed company, with no load times or prompt bars? Or screen based on your qualitative investment criteria, like cos with limited competition?

@luyiest STX scores also inflected before the stock was up 800%+. Never any guarantees, but sometimes, evidence / story changes before markets really notice

When I was in long/short equity, I looked for inflection points. We're introducing a new way to spot them.

Many investment firms already use @CapRelayHQ's proprietary, buy-side quality bull-bear debates for idea gen and monitoring pipelines.

We're now scoring these debates over time for whether the bear case or bull case has better evidence. Charting these makes it easy to spot potential changes in the investment story.

None of this generates alpha by itself. We don't think AI generates alpha, except in the hands of a sophisticated investor.

But with the right tools, investors can identify buy-side tension points, determine what's worth spending time on, and find inflections faster than ever before. Many leading-edge investors are doing this already.

Reach out to learn more, or start a free trial in seconds at our website.

Can LLMs spot inflections in the investment story?

CapRelay has proprietary, buy-side bull-bear debates for every US-listed company. Now, we're judging which side of the bull-bear debate has stronger evidence and charting these scores over time.

@GergelyOrosz Same applies to us. Regulated customers = we can't send anything to Fable

That said, GPT/Codex has always impressed us more than the equivalent Anthropic model since Sonnet-4.6 days, and it's not changing with GPT-5.6

GPT-5.6 -- NOW THE BEST FOR FINANCIAL RESEARCH?

There have been three major jumps in financial research capability:

-> GPT-4 -- the first glimmers of professional quality

-> Gemini-2.5-Pro -- the first model to break through into professional-grade research

-> Sonnet/Opus-4.6 -- more insightful, more capable

We run a large proprietary bench of financial research tasks across each new major model release.

GPT-5.6 is very good. But does GPT-5.6 belong in that list?

Some vibes from our evals:

1. GPT LOVES outputting numbers

The GPT family of models seems to love outputting a firehose of numbers.

I think its RL on finance tasks makes it think that numbers = quality. This isn't the case. Numbers, used correctly, carry weight and convey insight, but it doesn't do this by default.

Sonnet seems to understand the right balance and uses numbers to support qualitative points.

2. GPT is more terse; Sonnet is chattier

GPT has a very terse, to-the-point style. You can recognize it immediately, which is unfortunate.

Sonnet, by contrast, is very chatty. It's happier to spend sentences elucidating a point that GPT would've clipped to a few words. This makes Sonnet more expensive, but in my view, nicer to read.

3. GPT likes to balance out debates

GPT works hard to present a balanced picture. For example, if asked for a bull vs. bear debate, it likes to output the same number of points on each side.

By contrast, Gemini and Sonnet seem to better recognize reality: if the weight of evidence is one side (e.g. it's analyzing a company with clear momentum), it doesn't try that hard to invent an opposing point of view.

4. Differentiation is in what you build, not what model you choose

All of this said, GPT is clearly in the same class of intelligence as Claude models at this point. When investors ask me which model is best, I tell them to pick based on their personal vibes.

What differentiates investors in the use of AI at this point is the workflows they build, not the models they choose.

Our most sophisticated investment firms custom-build tools to automate industry coverage, and scale up idea generation. They do this using AI skills, internal data, and proprietary data connectors via MCP/API, like what we offer at @CapRelayHQ.

These investors think more about the work they'd like to automate, than the model they choose.

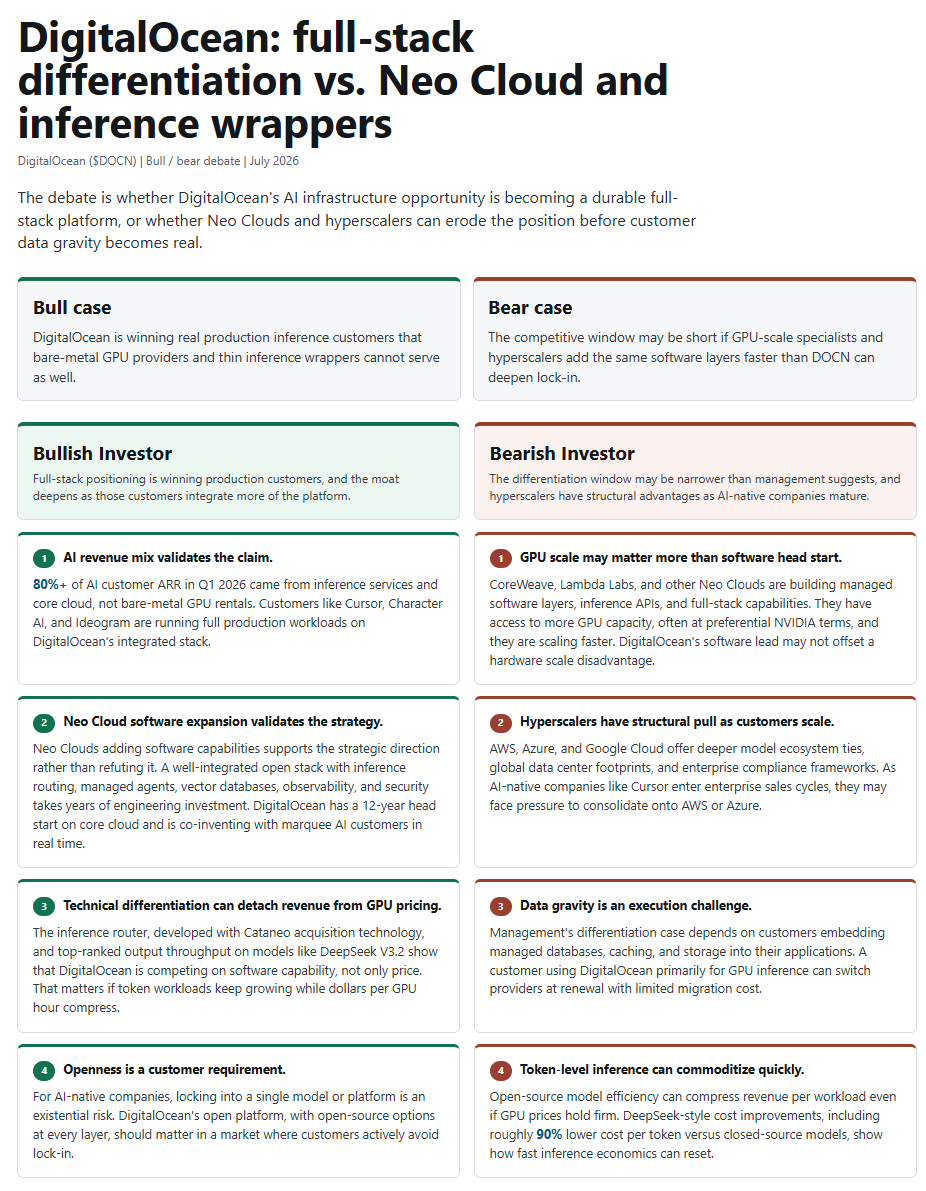

Takeaways from one of the first earnings season reads on AI infra demand: DigitalOcean ($DOCN) pre-announced today.

Strong results: DOCN expects Q2 rev growth of ~29% YoY, continued accel vs. 14% in the same quarter last year. RPO up more than 10x YoY.

Two stories:

1. HOW DIGITAL OCEAN 4X'D

DOCN is a cool case study because it started as a developer tools company, struggling to compete with the hyperscalers. Then it executed well in AI, and the stock more than 4x'd, despite ostensibly being a software company!

How did DOCN differentiate? AI-native companies need GPUs, but they also need the surrounding cloud stack: databases, storage, networking, routing, observability, and orchestration. DOCN is trying to package that together instead of only renting GPUs.

This is working: DOCN's growth accelerated dramatically. 80%+ of DOCN's AI customer ARR is inference services and core cloud products. Bare metal rentals is small and shrinking.

The market recognized this, and DOCN's multiple went from 3x to 13x 2026 sales.

2. READ-ACROSS TO OTHER NEOCLOUDS

CoreWeave and Nebius are the bigger, pure AI infrastructure bets. Both have far more scale, far more backlog, and far heavier capex requirements.

DOCN started from software and moved down the stack into GPU services. CoreWeave and Nebius are coming up the stack.

CoreWeave and Nebius are growing faster, but DOCN is actually trading at a higher forward multiple. Could it be that the market is rewarding DOCN's stickiness, which comes from its customers' broader adoption of Digital Ocean's software offerings?

Could it be that software... remains valuable?

Research and attached bull-bear debate point via @CapRelayHQ

A practical guide for investors on how to think about AI agents: Brains + hands.

The brain is the model: Claude, ChatGPT, Gemini. Which model is mostly a distraction; we spend a lot of time evaluating models, and they're all very good.

The hands are the real differentiator. These are the tools and data you give it: screeners, filings, transcripts, market data, estimates, research systems, and your own internal context.

How do you give your model a hand? (PUN INTENDED)

1. Give the agent access to your own data

If you're bringing on board a new junior analyst, what would you give them for background reading?

Consider:

- A memo on your strategy or firm

- Your watchlist or coverage universe

- Examples of memos and thesis docs

- Models

- Meeting notes and call notes

The easiest path is to create a clean Drive or OneDrive folder for the project and connect it to Claude or ChatGPT.

For a small task, just upload a project pack.

2. Give the agent third-party tools and data

All modern agents have web search, which is a good start, but not enough for financial research. You wouldn't give your junior analyst a task and say "go search Google". "

You could also download every sell-side report, every transcript, every model, and every podcast you care about into a folder and point your agent at that. But you probably don't want to!

This is where MCPs come in: they're the specialized tools and data the agent uses to do finance-specific tasks.

For example, over 50 investment firms use CapRelay to give their agents access to tools like screeners and buy-side quality proprietary data.

3. Write prompts with GOALS and TOOLS.

GOALS: What do you want the agent to get one?

TOOLS: What tools do you think the agent should use to do this?

Bad prompt: "what changed for LMT and other defense primes since i looked a yr ago"

-> Unclear goal, insufficient tools and context

Good prompt: "output an analysis of earnings power changes and trends among defense primes since my last thesis memo a year ago. The thesis memo is in google drive, and use caprelay"

-> Clear goal. The agent will search for your thesis in Google Drive, identify what you care about, and use CapRelay to analyze earnings and industry trends within the industry to create the right output

On July 4th, you might choose to grill a hot dog from one of the stranger public companies in America: Nathan's Famous.

Nathan’s Famous ($NATH) began in 1916 as a nickel hot dog stand in Coney Island.

Today, it is a $450M public company, built around hot dogs, and still tied to the same corner of Brooklyn.

This tiny Coney Island restaurant succeeded by making food IP, turning an otherwise undifferentiated product into a premium, national brand.

Nathan's built an event around the July 4th occasion. Every Independence Day, the original Coney Island location turns into the set for the Nathan’s Famous Hot Dog Eating Contest. Last year, Joey Chestnut ate 70.5 hot dogs in 10 minutes (!) and won his 17th contest. For one day every year, a small hot dog company gets pulled into a national holiday.

This premium brand position manifests in $162M of revenue, with a 22% EBITDA margin:

-> Nathan's has four company-owned restaurants, 221 franchised locations, and 476 ghost kitchens for delivery.

-> But the real money comes from branded foodservice: Nathan’s sold $106M of hot dogs to venues like stadiums, movie theaters, amusement parks, and restaurant operators.

-> Licensing is the second driver. Nathan’s generated $37M of licensing royalties. Smithfield Foods makes and distributes Nathan’s retail hot dogs into retail, while Nathan’s collects royalties on the brand.

Smithfield Foods is process of acquiring Nathan's. The company already manufactures and sells Nathan’s products under a license that runs through 2032. Smithfield's strategy is to mix-shift from commodity production into higher-margin consumer brands, and acquiring Nathan's was a tentpole initiative.

I love quirky companies like this, that made it big in the world's greatest capital market.

Happy 4th of July, and happy 250th America!

Trucking is one of the best performing sectors that has nothing to do with AI, with stocks up 60%+ over the past year.

The story (not investment advice):

Rewind to the last freight boom. In 2021 and early 2022, goods demand was strong, supply chains were messy, and trucking capacity was scarce. Rates spiked. That attracted a lot of new capacity into the market, especially small carriers chasing high spot rates.

Then, as all cycles must (except this memory cycle evidently), things turned. Retailers worked through excess inventory. Consumer demand tightened. Industrial demand and housing slowed as rates rose.

For several years, shippers had too many trucks competing for too little freight. That pushed pricing down and hurt almost every part of the ecosystem: truckload carriers, brokers, LTL carriers, and logistics providers. Management teams called it the longest and deepest truckload downturn in the company’s history.

But now, the cycle seems to be turning again, with a supply contraction normalizing the industry. Why?

Small carriers that entered during the boom spent the downturn running at low or negative economics. Insurance, equipment, maintenance, fuel, financing, and driver costs stayed high while rates fell. That eventually forced non-economic capacity out.

On top of that, there's a regulatory angle, with better enforcement around English-language requirements, noncompliant trucking licenses, carrier vetting, etc., pushing the lowest-cost trucking capacity out.

$RXO management said the freight market is improving because of “supply side tightening despite overall soft demand... capacity continues to exit the market.”

Pricing power is changing! Demand hasn't come back yet, and trucking earnings are hardly strong, but as usual, markets are way ahead of the curve and predicting an up-cycle.

Finally, the largest operators have driven cost out during the down-cycle, which likely results in strong operating leverage on the other side. Knight-Swift ($KNX) cut underutilized tractors, reduced non-driver headcount, exited facilities, and worked U.S. Xpress toward profitability. RXO took out more than $155 million of annualized costs since its spin and Coyote integration. ArcBest ($ARCB) cut unprofitable truckload volume. $XPO reduced reliance on outside linehaul carriers, pulling outsourced miles down to historically low levels.

Pictured: Bull case from @CapRelayHQ on Schneider ($SNDR) published in Oct. 2025, highlighting the potential for a turn in this cycle before the stocks ripped higher.

Comcast ($CMCSA) shares up 7% intraday on big news: Comcast is spinning out its media assets, undoing two decades of consolidation.

Why's Comcast doing this? Because the business is under competitive pressure on all fronts. Shares have gone nowhere for 10 years. At this point, the broadband business and the media business need different paths forward. It's wartime.

The story (not investment advice):

Comcast’s peacetime industrial logic was that broadband would consistently grow ARPU and subs, throwing off excess cash. Investing this into media gives Comcast programming, sports, bargaining power, and ways to monetize IP via businesses like parks. The conglomerate could fund Peacock to compete in streaming, buy sports rights, build theme parks, and still return capital.

Then the industry changed:

1. Broadband competition = less cash

Comcast added 2M broadband subscribers in 2020 and 1.3M in 2021.

Then competition increased: T-Mobile and Verizon pushed fixed wireless home internet. Starlink created a satellite alternative for rural areas, but increasingly suburban.

This meant that broadband, which investors (including me!) thought of as 10+ year secular growth story, began to shrink! Comcast broadband subs -66K in 2023, -411K in 2024, and -711K in 2025.

Pictured: Bear case on broadband, via @CapRelayHQ

So Comcast went from raising broadband prices 3-4% consistently to finding ways to defend the customer relationship: Comcast *cut* broadband pricing, and entered into 1- and 5-year price guarantees.

On top of this reversal, Comcast is spending cash as well to grow a wireless business, which hurts near-term ARPU and EBITDA, but better defends subscribers and is a way to hurt the fiber overbuilders. Xfinity Mobile grew from 2.8M lines in 2020 to 9.3M by year-end 2025, then 9.7M in Q1 2026.

2. The media business became even more capital-intensive

Comcast bought NBCU in 2011, when cable was growing and streaming was nowhere (Netflix tried to split off its DVD by mail business then)!

Now cable and linear TV are shrinking, streaming is eating media, and tech giants are competing for sports rights.

NBCUniversal must compete as well. There are some good assets: Peacock reached 44M paid subscribers by year-end 2025 and 46M in Q1 2026. Universal opened Epic Universe in 2025. Parks and film IP can can still grow.

But growth requires investing in NBA rights, Olympics, NFL, Premier League, studio output, Peacock, parks, and Sky. They're all hungry consumers of capital.

3. Shedding the anchors

Brian Roberts said today that when Comcast bought NBCUniversal in 2011, “the industry looked very different.” The new requirement is “focus, speed and strategic flexibility.”

Across telecom and media, the conglomerate model has been unwinding for years. AT&T separated WarnerMedia. Verizon retreated from AOL/Yahoo.

Both sides of the business -- cable and media -- are in difficult fights, with mounting requirements for capital and agility. This is Comcast's answer.

Claude and ChatGPT are the new front doors for financial research. But they love to rely on consumer finance websites, which is... not ideal.

Take this task: "find 100 non-tech companies under $10b of market cap that have quantified some benefit from using AI internally as part of their business operations, and summarize in a table"

Try it: an AI chatbot can't do this alone. But with the right MCP, the agent delivers a thoughtful, sourced, 100-row workbook with real insight.

Did you know the sectors where management teams have best quantified internal AI benefits are:

- Freight brokers

- Real estate brokers

- And travel agencies

The non-tech business model leading in AI adoption so far is... brokerage!

If this is interesting, it takes about 2 minutes to give your Claude and ChatGPT agents the professional-grade data and tools they need, with a free trial of @CapRelayHQ. Link in comments.

Why do Claude and ChatGPT agents do better financial research with MCPs? Human analysts need the right context and tools to do great work, and so do AI agents.

Here's what's going on behind the scenes

Google fired an engineer for developing one of the tools I always recommend to investors :(

Justin built the Google Workspace CLI, which allows agents like Claude Code to interact with Google Sheets, Docs, Gmail, and other Workspace tools.

Leading-edge investors we work with use agents to sort through their emails, determine what news or research they received is incremental to their thesis, surfacing these as priority items, and archiving the rest. I always recommend Google Workspace CLI for this workflow.

(If you're a finance professional and want this, we'd love to help!)

Leaders asked what they could learn from it. Legal asked why the Google logo and brand colors were in the repo, when it wasn't an "official" Google project. Justin was dismissed.

Meanwhile, I always thought this unapproved CLI was a major differentiator for Google Workspace. I felt sorry for our Outlook / Microsoft customers who didn't have something as powerful.

It seems like Justin landed on his feet is building a new company. Best wishes!

Two months ago I was fired by Google for creating the Google Workspace CLI. It went viral, hit #1 on Hacker News, gained thousands of GitHub stars and many thousands of actual users in just a couple days.

It was an incredible, confusing journey, from directors and leaders asking what they could learn from the tool to getting grilled by legal about why the Google logo and brand colors are on the Google Workspace GitHub code repositories.

I think the cause was that Workspace and certain leaders (and projects) were afraid of being disrupted. But the fear wasn't specific to my CLI, it was a broader fear in what agents meant for Workspace. Either way, the irony of my termination was the announcement at Google Cloud Next two days before I was fired that an official Workspace CLI was coming.

I want this out there because it is easier for me to explain my story and it is an experience I want to fully own. It's also part of my healing.

Nearly 7 years at Google was an incredible opportunity for me and I was fortunate to have wonderful teammates and a manager that fully supported me through these last few months. Thank you.

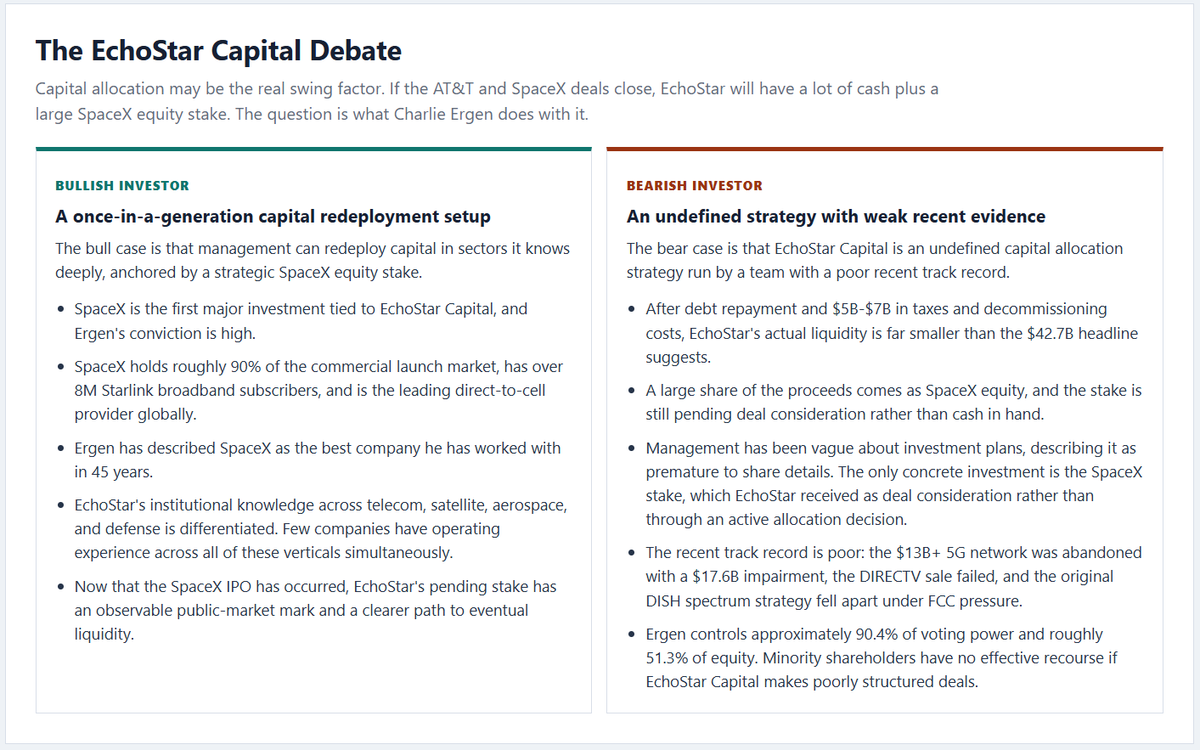

EchoStar ($SATS) is up 334% over the past year because it's set to receive a ~2% stake in SpaceX ($SPCX), which could be worth more than EchoStar’s entire $31.6B market cap.

How did this happen?

EchoStar's path to riches ran through a failed wireless gamble.

Backstory: Charlie Ergen founded EchoStar in 1980 selling C-band satellite systems (the big backyard dishes people used to receive satellite TV before today’s smaller consumer dishes). EchoStar launched its first satellite in 1995 and built DISH into a national satellite-TV provider.

DISH and EchoStar split in 2008. DISH kept the consumer TV business, or “pay-TV”: subscription TV bundles customers pay for monthly. EchoStar kept the satellites and technology. DISH bought spectrum, later launching Sling TV in 2015 and buying Boost Mobile in 2020. Boost is a prepaid wireless brand: customers buy phone service without long-term contracts, typically at lower price points, and Boost pays AT&T and T-Mobile for network access.

The two companies recombined at the end of 2023.

Then Ergen tried to build a fourth national wireless carrier, using Boost's customer base and EchoStar's technology.

The plan was to use Boost’s customer base, build a new cloud-based 5G network, move Boost customers onto that network, and stop paying and using AT&T and T-Mobile. This could bootstrap EchoStar into becoming a full wireless career, which could be a $100B+ opportunity.

EchoStar built much of the network required. The commercial side never caught up with the capex and debt.

By FY25, EchoStar had 7.5M wireless subscribers, but wireless revenue was only growing mid-single digits, and the segment still lost $495M at the operating level. EchoStar took $17.6B of impairments tied to the failed 5G and spectrum strategy.

The FCC forced EchoStar to pick another strategy.

In 2025, the FCC reviewed whether EchoStar was actually using its wireless spectrum: the licensed airwave rights needed to carry phone and data signals. That review collided with debt maturities and liquidity pressure. These forces pushed EchoStar to monetize the spectrum.

AT&T agreed to buy some of EchoStar's spectrum for $23B, and SpaceX agreed to buy the rest for $19.6B, including up to about $11.1B in SpaceX stock. SpaceX wants the spectrum for Starlink Direct to Cell, its plan to connect ordinary phones directly to satellites when terrestrial cell towers are unavailable.

Then, as SpaceX IPO'd, EchoStar found itself sitting on the most valuable asset it's ever had: SpaceX stock.

EchoStar's future depends on several factors:

1. Deal close. The AT&T deal had FCC/DOJ approval but had not closed, and the SpaceX deal is targeting a November 2027 final close. Until proceeds arrive, EchoStar's debt presents a real liquidity problem.

2. Boost economics and legacy businesses. EchoStar still runs a mobile business, TV business, and a broadband business, which seem to be in decline. Ironically, EchoStar is a direct competitor to SpaceX's connectivity businesses, which are taking share!

3. Capital allocation and governance. This may be the real swing factor. If the AT&T and SpaceX deals close, EchoStar will have a lot of cash plus a large SpaceX equity stake. The question is what Charlie Ergen does with it.

EchoStar announced a new internal division called EchoStar Capital on November 6, 2025. The company has not laid out a mandate, but WSJ reported that EchoStar Capital would pursue new business lines using proceeds from the recent spectrum deals.

That creates the key debate: does EchoStar Capital become a disciplined telecom, space, and defense investment arm, or does it become a capital-allocation black box inside a founder-controlled company? The stock is probably discounting capital allocation somewhat.

EchoStar spent years assembling spectrum to launch a fourth national carrier, which didn't work. But along the way, EchoStar ended up with some valuable assets, which it traded for the most valuable asset of all: SpaceX stock.

Research and bull-bear debate here via @CapRelayHQ

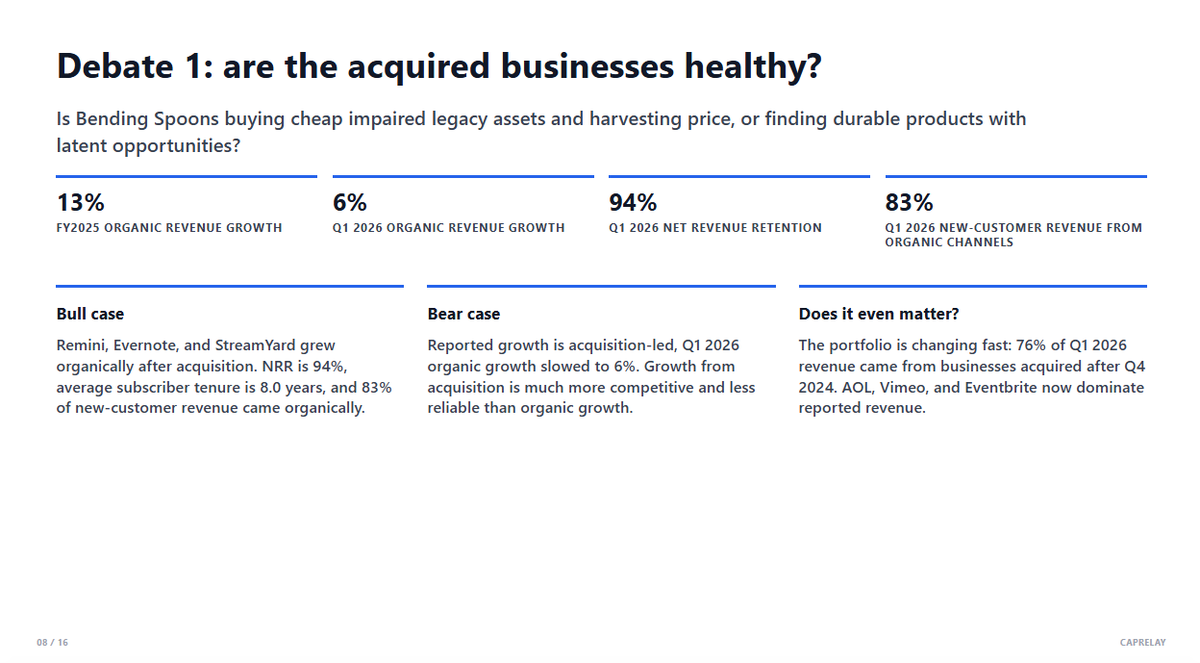

@CapRelayHQ FWIW, my view on these debates for $BSP:

- Acquired businesses are probably fine

- Returns will defs compress with scale, but still could be very good depending on execution

- AI is two-edged sword, depends on execution

- No clue on real earnings power, margins are awfully high

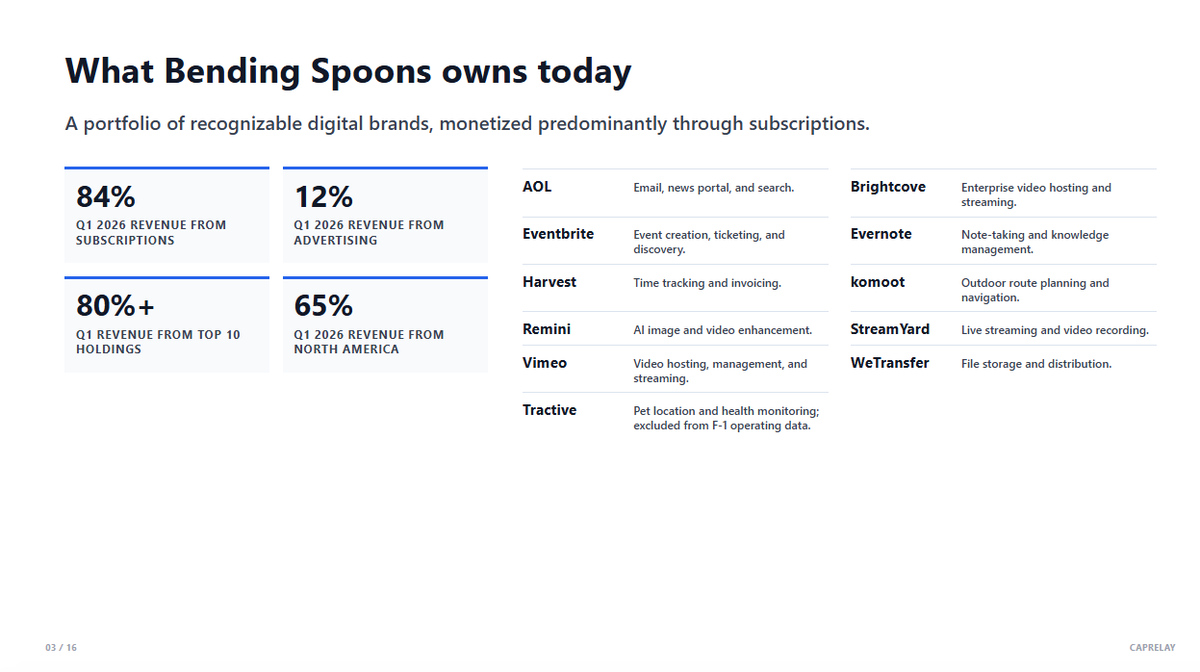

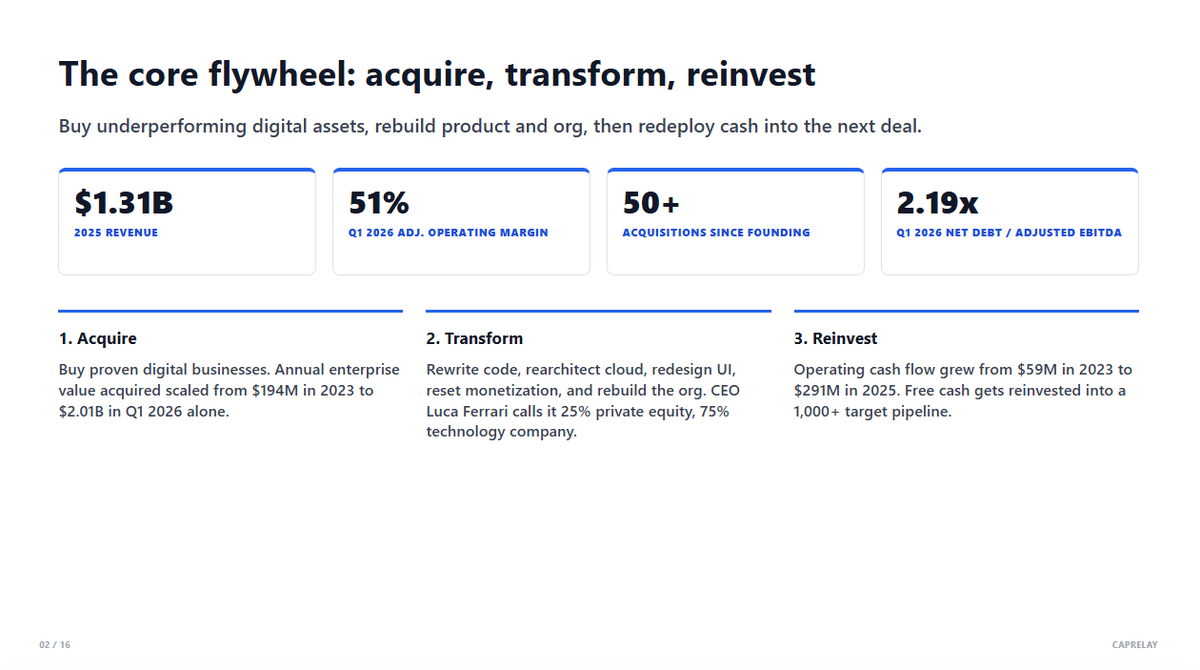

$CSU is up 15,643% since IPO. Is Bending Spoons $BSP a younger, more aggressive Constellation?

This pre-IPO S-1 breakdown deck on Bending Spoons covers:

-> The core business and its value creation engine, rolling up and improving legacy tech assets

-> What the key investor debates are ahead of the IPO, like the health of its core businesses

Link to full deck in next comment