Hi! back online to announce that @chi_s0ng and I are excited to launch CapRelay! https://t.co/45gp1OR2Rc is an equity research platform that thoughtfully uses AI to help analysts get up to speed on companies and uncover new insights / risks / interesting opportunities.

Always enjoy a good cyclical inflection story :). And I think the operational/back-office side of logistics is one of the areas where I think you can see concrete ROI from AI without too much imagination.

$RXO on changes in structural costs:

Trucking is one of the best performing sectors that has nothing to do with AI, with stocks up 60%+ over the past year.

The story (not investment advice):

Rewind to the last freight boom. In 2021 and early 2022, goods demand was strong, supply chains were messy, and trucking capacity was scarce. Rates spiked. That attracted a lot of new capacity into the market, especially small carriers chasing high spot rates.

Then, as all cycles must (except this memory cycle evidently), things turned. Retailers worked through excess inventory. Consumer demand tightened. Industrial demand and housing slowed as rates rose.

For several years, shippers had too many trucks competing for too little freight. That pushed pricing down and hurt almost every part of the ecosystem: truckload carriers, brokers, LTL carriers, and logistics providers. Management teams called it the longest and deepest truckload downturn in the company’s history.

But now, the cycle seems to be turning again, with a supply contraction normalizing the industry. Why?

Small carriers that entered during the boom spent the downturn running at low or negative economics. Insurance, equipment, maintenance, fuel, financing, and driver costs stayed high while rates fell. That eventually forced non-economic capacity out.

On top of that, there's a regulatory angle, with better enforcement around English-language requirements, noncompliant trucking licenses, carrier vetting, etc., pushing the lowest-cost trucking capacity out.

$RXO management said the freight market is improving because of “supply side tightening despite overall soft demand... capacity continues to exit the market.”

Pricing power is changing! Demand hasn't come back yet, and trucking earnings are hardly strong, but as usual, markets are way ahead of the curve and predicting an up-cycle.

Finally, the largest operators have driven cost out during the down-cycle, which likely results in strong operating leverage on the other side. Knight-Swift ($KNX) cut underutilized tractors, reduced non-driver headcount, exited facilities, and worked U.S. Xpress toward profitability. RXO took out more than $155 million of annualized costs since its spin and Coyote integration. ArcBest ($ARCB) cut unprofitable truckload volume. $XPO reduced reliance on outside linehaul carriers, pulling outsourced miles down to historically low levels.

Pictured: Bull case from @CapRelayHQ on Schneider ($SNDR) published in Oct. 2025, highlighting the potential for a turn in this cycle before the stocks ripped higher.

@chat_SBC I know the algo might flag this as spam bc of the link lol, but here's a unlocked temporary link to our bull case for $CRBS:

https://t.co/NlO29a6Bxu

@ExcessDefaults I think he's pretty meh on $JXN. My takeaway per last call (and some of the past others) is he's still a bit skeptical of Brooke Re assumptions & capital sufficiency. Don't read his notes though so could be off 🤷♂️

And if you want to dig deeper, check out the thread above where @chi_s0ng posted a pretty great deck overview of $BSP and some data & analysis on $ROP from @CapRelayHQ

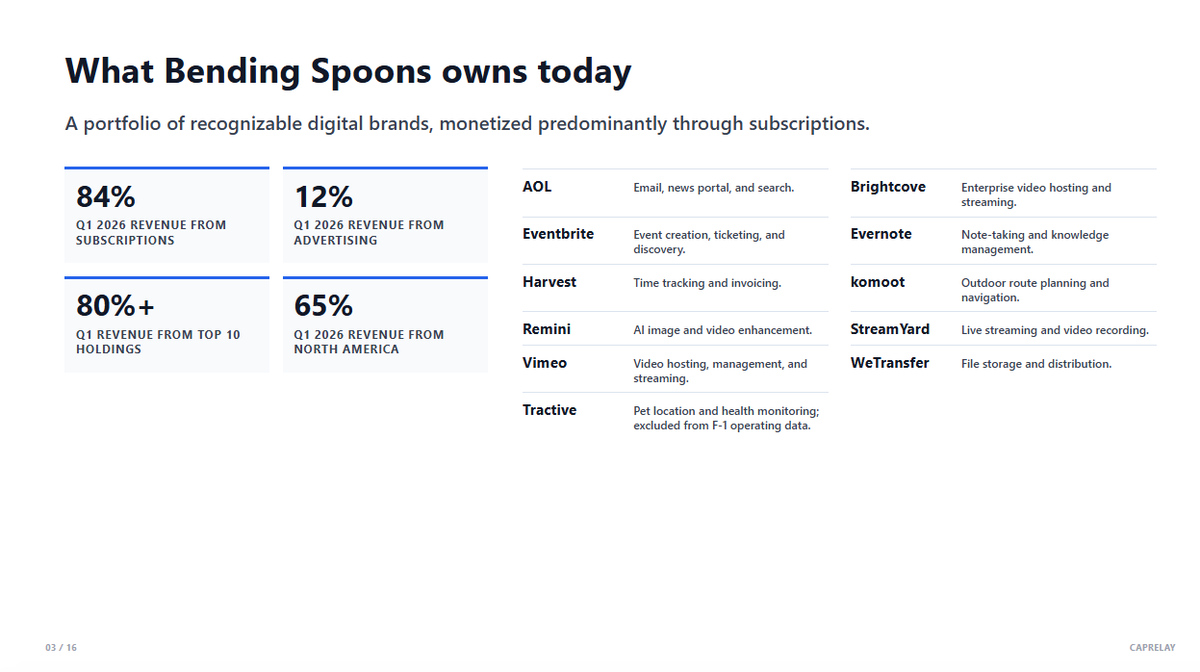

Worth comparing $BSP's planned IPO valuation vs. existing $ROP and $CSU comps... there's a pretty big gap.

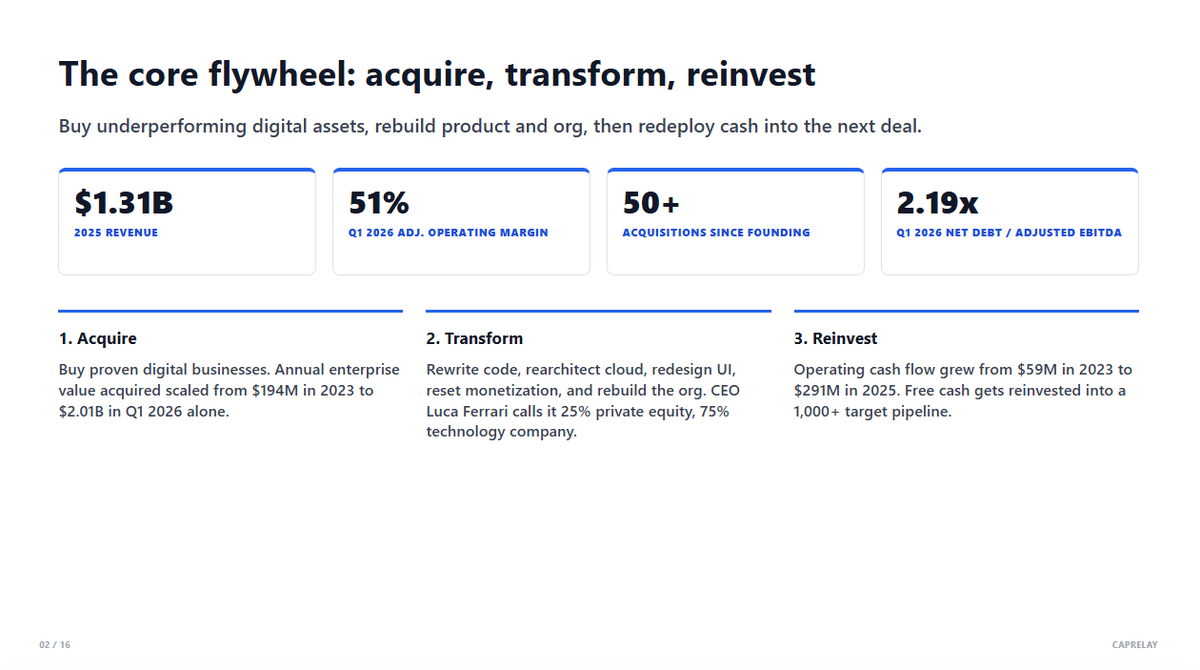

Ppl are discussing a $BSP IPO valuation of ~$20B(!) . They did $1.3B in 2025 Revenue, but while technically true, no, I don't think it's quite right to say they are IPOing at 15.4x sales. Their large recent acquisitions mean it's better to just take Q1 2026 Revenue of 601mm and annualize... plus there's Eventbrite... so let's say ~$2.7B is a more accurate picture of their 2026 sales.

So with the $20B target valuation (and ~$2B in net debt post-IPO), we get EV/Revenue: ~8.2x.

Meanwhile... EV/Revenue for $ROP and $CSU:

$ROP: 5.4x

$CSU: 3.8x

... And these are off of 2025 sales, the multiples should prob be even ~10-15% lower if based off of 2026E!

Of course one of the big narratives driving $BSP's valuation is that it's a more modern roll-up that can more efficiently rebuild tech stacks and leverage AI. There might be something to this - based on 2025 figures, it's $2.57m(!) in revenue per Spooner vs. the $200-$400k range of revenue/employee at $CSU and $ROP.

It's still quite a valuation difference to say the least... and you have to wonder if $ROP and $CSU and competing acquirers will get better at adopting some of the efficiencies $BSP has seemed to be able to. But the investor/software engineer in me will def. be watching how $BSP evolves with great interest!

$CSU is up 15,643% since IPO. Is Bending Spoons $BSP a younger, more aggressive Constellation?

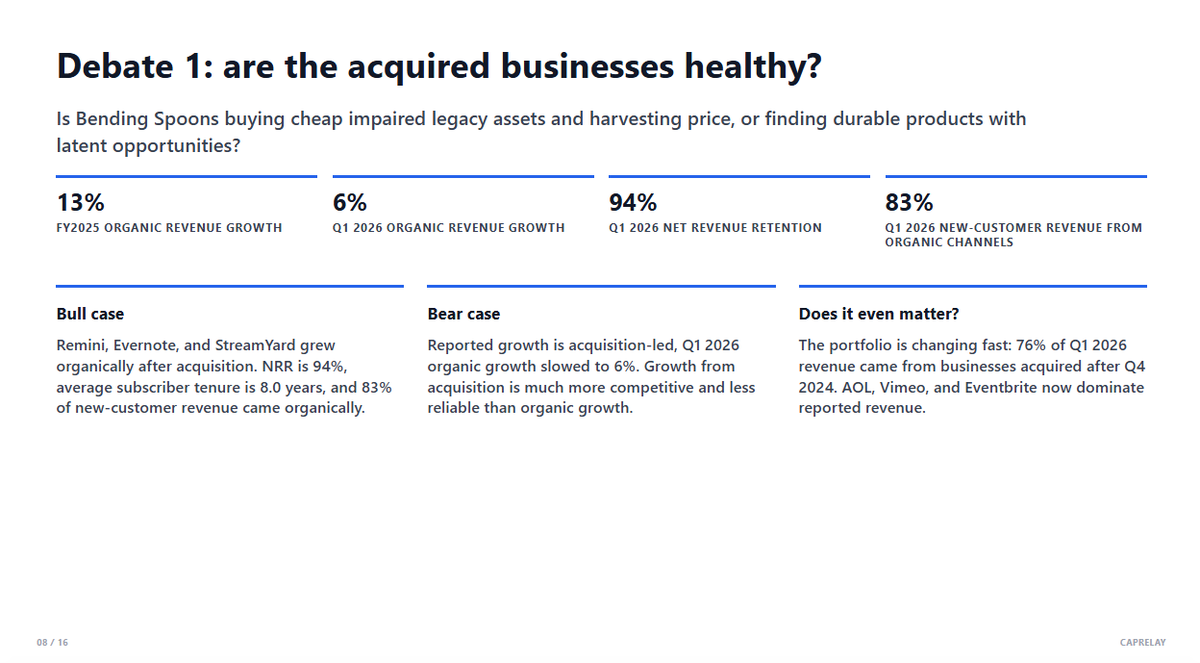

This pre-IPO S-1 breakdown deck on Bending Spoons covers:

-> The core business and its value creation engine, rolling up and improving legacy tech assets

-> What the key investor debates are ahead of the IPO, like the health of its core businesses

Link to full deck in next comment

@ExcessDefaults Eventually, more stupid stuff will be done, but am more in Tom's camp that priv. credit prob. isn't going to be the immediate next cause of a major blow-up. At least not in isolation. Good articulation imo of how post-GFC liability workthrough has created a nice thematic opp.

@typesfaster - Too much focus on lifestyle sneakers vs athletic roots, then lifestyle really softened

- Shifted too much towards DTC and pissed off wholesale/retail partners

- China has been weak/lackluster

- Tariff headwinds, not a huge neg. but haven't hleped

A few months ago we noticed that AI agent traffic had grown to 30%+ of CapRelay's traffic. It soon became clear that creating our own MCP server would be the best agent-native way to allow AI agents to use CapRelay.

We knew this would improve how agents worked on investment research tasks... But it really is one thing to know in theory and quite another to actually see an Claude or Codex agent seamlessly run qualitative natural language screens on CapRelay, filter through our bull-bear debates, and synthesize the information in ways that a team of investment analysts would take days to do.

Now, we're excited to release our MCP server and share these capabilities with our users! See the video below from @CapRelayHQ to see an example of how our MCP + AI agents can result in better real-world results for investors. MCP access is available during your CapRelay trial too - so you can try it out yourself in just a few minutes!

Your financial research agents can do better than relying on consumer finance websites.

CapRelay's MCP is now available for https://t.co/iTzArJTWYR, ChatGPT, Claude Code, Codex, Cursor, or wherever you do you investment research today.

The below video covers the highlights.

It's not perfect, but the SEC maintains the best and most transparent system of filings in the world imo. It has played a small but real part in helping the US maintain its capital markets leadership. Makes no sense to backtrack and remove quarterly reporting.

Checked in on the comment letters on @SECGov proposal to eliminate quarterly earnings. With about three weeks left to go, there's now over 1,100 individual letters and nearly 2,000 form letters. So far, a whopping 96% of those are against the proposal! Comments open until 7/6.

Good convo & interesting to consider why this is more of an issue now... Think a lot of folks get that AI tools can increase eng productivity. So the ceiling is higher for an engineer, and thus the gap btwn below-avg/non-motivated & top engineers is magnified more so than ever. But I think a really good corollary that @thdxr brings up is that not only is there an impact gap... but the engs that are checked out can now much more easily cause a real negative drag on your top engs through slop PRs etc w/ AI.

Dax is saying unless a dev has meaningful equity in a startup, don’t expect they’ll use AI gains to improve the business (too much). Why would they?

Checks out to me. Also why founders and AI labs and AI startups go all-in on AI tools (they have large ownership + upside!)

Crotchety value Investor me: Will frontier AI labs end up like airlines - transforming our world but being businesses with poor returns on capital?

Technologist me: Does that analogy really hold when it seems like every so often one of the labs seemingly goes from instantly operating a fleet of turboprops to jets?

🤔

@LeylaKuni Makes sense. I know there's lots of interest in applying AI there. Real potential but also good marketing: if you do a rollup with AI, it's no longer a boring PE investment, congrats, it's VC!