Michael Howell's Fourier cycle model has called every major liquidity swing since 2000.

Right now it says the peak won't arrive until mid-2027.

That's the time-anchored framework most investors don't have. But the mechanism behind the current slowdown is the part worth understanding.

Global liquidity is trending lower and central banks are not the reason. The real economy is consuming the capital. AI capex is running at 6 to 7% of GDP. Firms are running down their treasury departments and deploying cash into physical infrastructure instead of holding financial assets. Capital that would normally flow into equities and bonds is going into chips, power grids,and concrete.

That is the structural drain.

Paper markets are competing against the real economy for the same pool of capital and the real economy is winning.

Howell's framing for where we sit in the cycle:

Dance near the door because the music is coming to an end. Late-stage speculation historically rewards commodities and gold over equities.

Mid-2027 is the peak. The path between now and then runs through real assets.

@crossbordercap

‼️THIS IS INSANE:

46 of 68 global central banks are currently overshooting their inflation targets.

The US is running +1.8 percentage points above its 2% target, and the Eurozone +1.2 percentage points above.

Meanwhile, markets are pricing a 98% probability of a 25bps rate cut from the ECB on June 11th and an 83% probability of a 25bps hike from the Bank of Japan on June 16th.

The first FOMC meeting under new Fed Chair Kevin Warsh follows on June 17th.

If the outcome is too dovish, the long end of the Treasury market heads toward 6%; too hawkish, and the S&P 500 pulls back toward 7,000.

Central banks are historically failing to fulfill their most basic mandate.

WATCH: @edzitron absolutely destroy the AI narrative by explaining these AI companies have no way to be profitable.

(My personal theory is Elon Musk is rushing to take SpaceX public because he plans merge with Dario's Anthropic as a way to destroy Sam Altman)

Why hasn't oil hit $150 yet?

The US has been quietly dumping its emergency oil reserves.

66m barrels drained from the SPR since the Iran war began & stocks are now at 349M bbls - approaching Biden-era lows.

That would be the lowest level since 1983.

It won't last forever.

The US equity market bull market bonanza is a fiat money illusion. Priced in gold The S&P500 has halved since 1970 and is down 70% since the 2000 peak.

Equity supply is about to go “off the charts.”

Frankly, nothing in market history has come close to what is about to be done. Furthermore, once “lockups” expire, a flood of shares will begin to hit the already overvalued market.

Stay vigilant!

Source: Bank of America

Another record has been set.

The US stock market cap-to-GDP ratio is up to a record 238%.

This comes as the stock market's value surged to an all-time high of $75.7 trillion, far exceeding the ~$31.8 trillion size of the US economy.

This ratio has surged +38 percentage points since the March 30th bottom in the S&P 500.

This metric is also now +90 percentage points above the 2000 Dot-Com Bubble peak of ~148%.

Since the 2008 Financial Crisis, the US stock market has grown at 5x the rate of the underlying economy.

Asset owners are winning more than ever.

Energy requirements for data centres currently in the Scottish planning system is between 4450 MW and 4950 MW, which is larger than the winter peak electricity demand for the whole of Scotland.

The Scottish government is putting power for the tech giants before people.

Nasdaq down 4% Friday and then Trump talks about AI stakes from government after the close.

If this was planned before Friday fine…if not then it shows how important this market is to the administration.

Our first weekly X review join us next Frisday 12pm

Have you noticed how closely correlated the Move Index is with Treasury government bond buybacks? Markets are subject to "discretionary" influences.

https://t.co/elyytOclbi

US small business hiring intentions are plummeting:

Just 9% of small business owners say they plan to hire over the next 3 months, the lowest since May 2020.

This percentage has HALVED over the last 6 months.

This is now in-line with the levels seen during the 2001 recession and at the beginning of the 2008 Financial Crisis.

At the same time, just 29% of small firms said they have job openings they can not fill, also the lowest since May 2020.

~13% of firms cited labor costs as their single most important problem, the highest in data going back to the 1970s.

Small businesses are pulling back on hiring at an alarming rate.

The 2-year real interest rate has now climbed to its highest level since the Trump administration took office.

At the same time, we are living through the deepest and longest drawdown in the history of the Bloomberg US Aggregate Bond Index.

We are moving in the wrong direction and I doubt Scott Bessent is thrilled about either development.

This is the exact opposite of inflating your way out of a debt problem.

Yet investors are increasingly pricing in the possibility of another rate hike.

I suspect policymakers will be forced to address that reality.

When they do, the implications for hard assets could be substantial.

https://t.co/CErNysNiBQ

NVIDIA IS BUYING ITS OWN CHIPS AND CALLING IT REVENUE

And your retirement account is secretly holding the bag.

This scheme is literally straight out of the Enron playbook...

In January 2026, a special purpose vehicle called Valor Compute Infrastructure was created with one purpose:

Buy Nvidia's chips so Nvidia could book the sale as revenue.

Valor raised $5.4 billion and purchased over 100,000 of Nvidia's GB200 GPUs.

But $1.9 billion of that money came FROM Nvidia itself.

Nvidia invested $1.9 billion into the shell company, then sold that same shell company $5.4 billion worth of its own chips and booked every dollar as revenue.

It's the Girl Scout whose dad bought all the cookies and then she wins the sales contest because Dad was the customer. Except this Girl Scout is a trillion-dollar company and the cookie sale is $5.4 billion.

But it gets MUCH worse:

The remaining $3.5 billion in financing came from Apollo Global Management. Apollo structured the debt, packaged it into securities, and then sold those securities to Athene.

And guess who Athene is? Apollo's OWN insurance subsidiary. The one that sells fixed annuities to American retirees as safe, conservative retirement products.

Follow the chain:

Nvidia funds a shell company with $1.9 billion. The shell company buys $5.4 billion in Nvidia chips. Apollo finances the remaining $3.5 billion. Apollo sells the debt to its own insurance arm. That insurance arm packages it into annuity products and sells them to retirees who think they're buying something safe.

The retirees have no idea that their retirement savings are now backed by 100,000 computer chips sitting in some data center that will be worth pennies on the dollar in three years.

Now look at what's happening inside Athene:

$74.2 billion in US reserves but $217 billion in assets have been shifted to a Bermuda-based captive insurer, outside normal US regulatory oversight.

$103 billion of that portfolio (roughly 35%) is classified as Level 3 assets. That means there is no observable market price.

These assets are valued by internal models, not by actual markets.

And sitting on top of all those unpriced assets? 16.6x leverage.

If you're getting flashbacks to 2008, you should be.

Back then it was mortgages bundled into securities that nobody understood, sold to investors who had no idea what they were holding, rated as safe by agencies that never looked under the hood.

Today it's GPU-backed securities. Computer chips bundled into structured credit instruments, routed through an offshore insurance subsidiary, and sold to you as a retirement product.

The collateral is 100,000 GPUs leased to a single customer through an xAI subsidiary. If xAI stops making lease payments for any reason - financial distress, a pivot in strategy, anything - the entire structure unravels.

And Nvidia releases new architectures every year, so each generation delivers dramatically more compute per watt. A 5 year lease on technology that's obsolete in 2 years creates a mismatch that should terrify every annuity holder in America.

Every single step in this chain is technically legal. The SPV is legal, the lease is legal, Nvidia's equity stake is legal, the securitization is legal, and the Bermuda transfer is legal.

But legality and legitimacy are not the same thing.

I've seen every trick Wall Street has ever pulled in my 45 years of doing this.

And what I'm looking at right now is a pipeline that takes AI infrastructure risk, launders it through 8 layers of financial engineering, and deposits it in the retirement accounts of Americans who never agreed to fund Elon Musk's data centers.

In 2008 it was mortgage-backed securities.

In 2026 it's GPU-backed securities.

Different asset. Same greed. With the same ending.

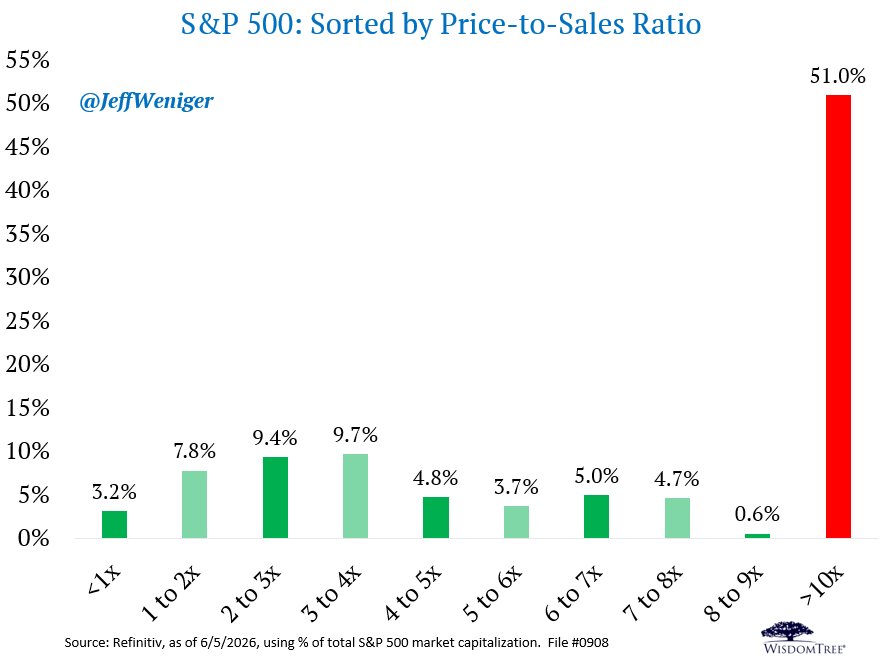

More than half the S&P 500's total value is now in stocks priced above 10x sales. This was once considered an outlandish valuation, as it leaves little room for error. The list includes Nvidia, Apple, GOOG, MSFT, Broadcom, Tesla, Micron, Eli Lilly, AMD, Oracle and 57 more.

Just heard during a financial television interview on equity investing: “ANY pullback is an opportunity to buy.”

This echoes quite a broad market belief -- conditioned by years of policy puts and outcomes-- that has increasingly ensured market corrections are remarkably limited in both magnitude and duration.

Yet the deeper this belief is embedded in the system, the greater the risk of unsettling volatility in the event of a serious challenge, whether from fundamentals, technicals, valuations, or all three.

#markets #investing #investors

We spent a good bit of time on yesterday's show discussing the massive underperformance of Low Beta and High Quality stocks vs High Beta stocks. While "this time may be different" the eventual rotation back to "quality" likely won't be.

h/t @ISABELNET_SA

Google ($GOOG) upsized its first equity offering in more than two decades to $85 billion amid strong investor demand, ending a decade of buybacks.

This adds to the equity issuance already slated by the coming mega-IPOs.

Dude, Where’s My AI-Driven Productivity?

If AI is the most revolutionary technology in history as many predict and markets increasingly price in, it’s odd that 4yrs in developed world macro productivity data shows no change in previous trends.

https://t.co/tbhRinaC5Q