If you were wondering why Tulsi Gabbard would be put on a terrorist watch list, wonder no more. She is telling the truth about the system. Namely, that the government is ran by the unelected bureaucracy, MIC and intelligence agencies.

Bravo, Tulsi. Bravo.

BREAKING!!! @RepRalphNorman just told me on #WhatsBuggingMe on @Ricochet that @FINRA response on #MMTLP is inadequate. @SEC failed to respond at all. He now will ask Rep. Comer to subpoena SEC for share audit data FINRA says it can't supply. And push for public hearings.

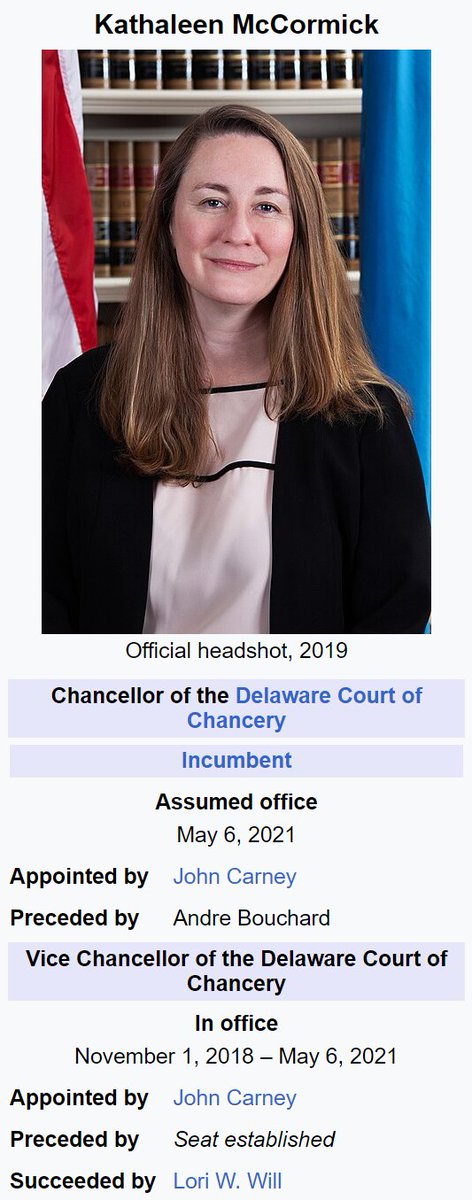

Judge Kathaleen McCormick rescinded Elon Musk's $55 billion Tesla compensation package, overturning the company's board and 80% of its shareholders.

McCormick also ruled against @elonmusk during his Twitter acquisition.

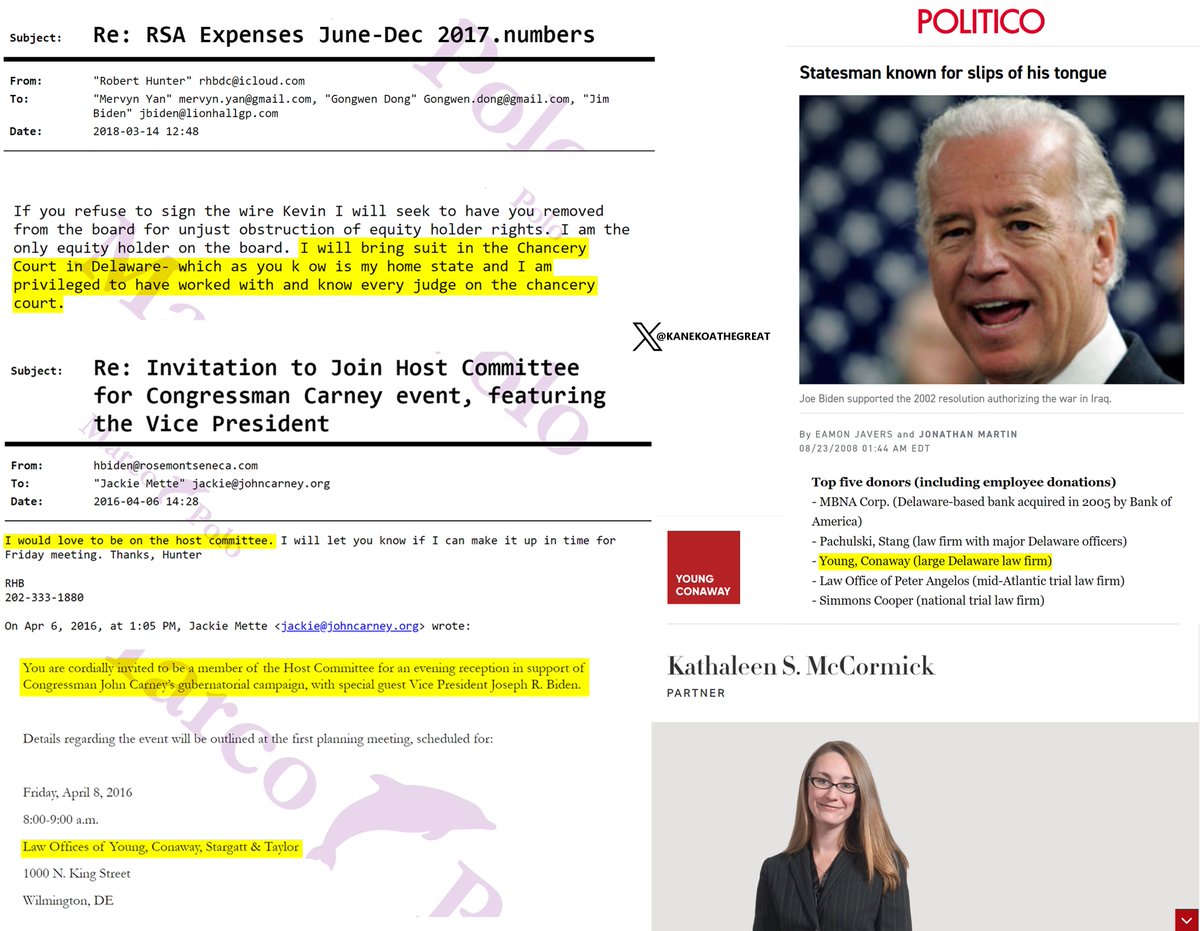

Before becoming the head of the Delaware Chancery Court, McCormick worked at a Delaware law firm called Young Conaway.

This firm and its employees have been major donors to President Joe Biden for decades.

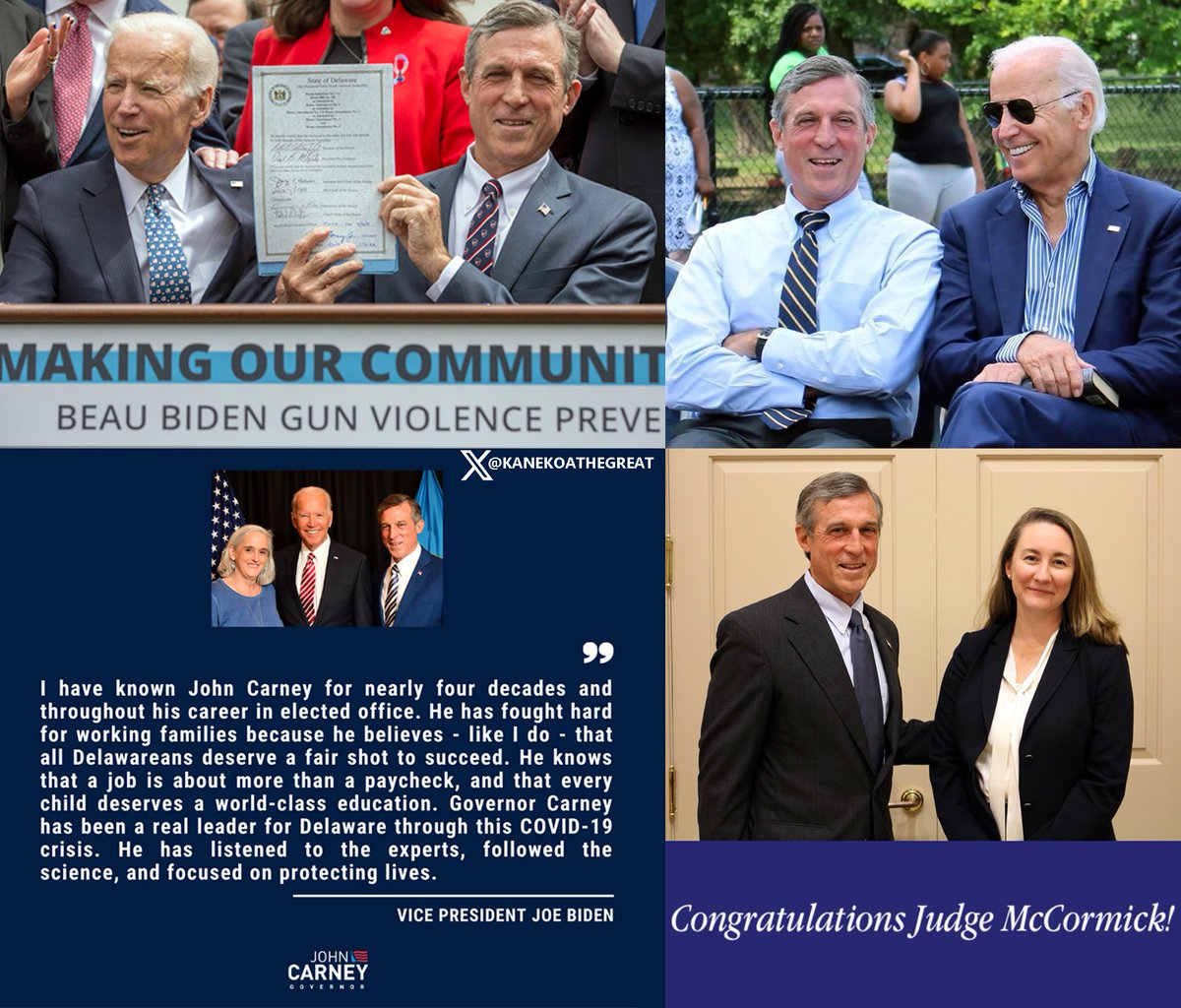

In 2016, Hunter Biden hosted a gubernatorial campaign event for Congressman John Carney, with then-Vice President Joe Biden as the guest speaker.

This event took place at the Law Offices of Young Conaway in Wilmington, Delaware.

Carney, a close friend of Joe Biden for the last four decades, later became governor and nominated Kathaleen McCormick, a partner at Young Conaway, to her position on the Delaware Chancery Court.

In a March 2018 email, Hunter Biden claimed to personally know every judge on the Delaware Chancery Court while threatening legal action against his Chinese business partners.

"I will bring the suit in the Chancery court in Delaware - which as you know is my home state and I am privileged to have worked with and know every judge on the chancery court."

After Elon Musk purchased Twitter with the stated goal of restoring free-speech, President Biden called for a federal investigation into Musk on the podium at the White House.

Following this, the Biden Department of Justice, Securities and Exchange Commission, and Federal Trade Commission initiated legal actions and investigations against Tesla, SpaceX, and X.

This recent decision by Judge McCormick, who worked with Biden's top donors and was nominated by Biden's close friend, to override Tesla's board and the majority of its shareholders is another clear example of the Biden administration and its allies weaponizing the American legal system against their political opponents.

Hey @joerogan & @JamieVernon, what if I told you there was an urgent situation that can literally prove that the American people are being robbed on a massive scale & Congress NOW KNOWS ABOUT IT!

Please take the time to Listen to these recent broadcasts:

@LauraLoomer interview clips:

https://t.co/yeolpNWhSr

@joshua_t_white, (Former SEC Economist, Professor of Finance) discusses $MMTLP:

https://t.co/r047QFwDry

@denniskneale, (Former Managing Editor of FORBES, CNBC, Fox Business)

& @JohnnyTabacco, (Host of WISE GUYS on NEWSMAX and Expert in Securities Lending & Stock Loan) discuss the #MMTLPFiasco

(Two "quick clips" that include a direct link to FULL INTERVIEW):

https://t.co/MuUwXW851z

https://t.co/QSNouvlcH9

@MMTLP_Studios mini documentary "Collusion" :

https://t.co/6AoycssbtI

Please, for more information Contact @KarmaCollects to have a more in depth discussion about it!

Dear, @TuckerCarlson@TCNetwork@joerogan@elonmusk@MariaBartiromo@MarioNawfal@bennyjohnson@cvpayne@dbongino@RealAlexJones@DineshDSouza@GenFlynn@TomFitton@denniskneale@michaeljburry@wolfofwallst

The $MMTLP story centers around an oil and gas company called Torchlight Energy that traded under the ticker symbol TRCH on the Nasdaq exchange. As you know, one of the major storylines in 2020 was the global spread of Covid-19. The subsequent lockdowns sent the global economy into a tailspin and crashed the demand for oil and gas. Companies like Torchlight found themselves in a perfect storm where their primary asset (oil) had little to no value and many companies including Torchlight had to get creative with their strategies to preserve shareholder value. In Torchlight's specific case, they also found themselves in a situation where justified or not they were the second most heavily shorted stock on the Nasdaq exchange. It is believed that a significant portion of these short positions were originated through the illegal practice of naked short selling AKA counterfeiting.

In response to this perfect storm, the board of Torchlight did something a little unorthodox, they opted to merge with a company that had zero interest in their oil and gas assets but rather was looking for a means to access the capital markets. In effect they sold the only asset on their books of value during Covid, their Nasdaq listing. The company that they merged with was a Canadian nanoparticle company called MetaMaterials. The merger ultimately occurred in June of 2021. As part of this merger, the Torchlight board negotiated a special accommodation for the TRCH shareholders which would entitle them and only them to the proceeds from the future sale of its oil and gas assets once the economy recovered. This was accomplished by issuing a dividend of one Series A preferred Share for each of the 165.4 million shares of TRCH that existed at the time of the merger and paying that dividend only to the Torchlight shareholders. By prospectus these dividend shares were simply non-tradable vouchers that would sit in shareholder accounts with no value until the oil and gas assets were sold. These non-traded dividends were in addition to the shares of MetaMaterials (Nasdaq ticker MMAT) that were exchanged into at the time of the merger.

Several weeks before the merger the OCC (Options Clearing Corporation) started trading derivatives on TRCH. On June 21st of 2022, the OCC issued a memorandum to firms indicating

that settlement of these derivatives was uncertain and mentioned that it was possible that the Series A Preferred shares (which were one component of the derivatives in question) may begin trading on the OTC or OTCBB exchanges even though the issuer had not given permission for such a listing and the prospectus specifically stated that it would not trade on any exchange. It is suspected that this memo was a "dog whistle" of sorts letting firms know that accommodations were being made to allow short positions to remain open even though under normal circumstances those liability positions would need to be closed at the time of the merger.

Amazingly enough, in early October, without permission of the issuer, the non-tradable Series A Preferred shares became tradable on the OTC exchange at the request of unknown parties and was assigned the ticker symbol MMTLP. Upon discovering this fact, John Brda, the former CEO of Torchlight called the OTC markets to inquire about how and why non-tradable shares were trading and to suggest to them that the application was likely fraudulent. The representatives of the OTC market declined to answer his questions and referred to FINRA. Similarly, FINRA declined to identify the parties that had made application to make it tradable and further that they were not going to stop it from trading at that point. They also noted that the documentation supplied by the unknown parties was 9 years old and identified Mr. Brda as an executive of the company. In fact, he was no longer an executive with the firm at the time of application and was in no way involved in the application. Mr. Brda told FINRA that he believed that the application was likely fraudulent in nature. FINRA declined to address the issue in any meaningful way.

Fast forward to the summer of 2022...the pandemic is largely over; energy demand has come back and the price of oil rebounds to over $120 a barrel. The executives a MetaMaterials decide (again to maximize TRCH shareholder value) that rather than having a fire sale with the 137,000 acres of land adjacent to the coveted Permian Basin in west Texas that it now made more sense to keep the assets and spin them off into a stand-alone private company. In the summer of 2022 MetaMaterials files a S-1 with the SEC notifying them of their intentions to spin off the assets currently trading under MMTLP into a private company which will be called Next Bridge Hydrocarbons.

There are 4 rounds of SEC comments and adjustments to the document. In late October of 2022 the SEC finally approves the S1A4 associated with MMTLP. This S1A4 once approved notified the financial world that the assets currently represented by MMTLP would be going private and would be exchanged in a 1:1 ratio for Next Bridge Hydrocarbons private shares on December the 14th of 2022. It went on to state that shares of MMTLP would trade through the close of business on the 12th of December and anyone that wanted to be eligible for the 1:1 exchange of shares needed to be the shareholder of record at the close of business on December the 8th of 2022.

Now that the SEC had approved this document it was now FINRAs obligation to disseminate this information to the brokerage firms and eventually the shareholders through their issuance of a document called a Corporate Action. For unknown reasons, FINRA procrastinated on this duty for the next 5 weeks. It was not until Rep. Pete Sessions (TX) wrote them a letter requesting that they fulfill this duty that they ultimately did so on December the 6th of 2022 by forwarding the Corporate action to the DTCC for further distribution to the brokerage firms and the shareholders. The DTCC had some questions about the distribution of the Next Bridge Hydrocarbons shares and requested a meeting with representatives of the company and FINRA which was to be held on December the 7th. All parties except FINRA showed up to this meeting. The next day, FINRA modified and reissued the corporate action that had been approved by the SEC without consulting the issuing company, something they are not supposed to do. According to the FINRA website, if FINRA finds a corporate action to be deficient their only recourse is to return the corporate action to the issuing company for modification. On the morning of December the 9th FINRA issued a U3 halt on MMTLP. U3 halts are 10-day cessations in trading utilized when an "extraordinary event" has occurred and have only been utilized 3 times in the history of the OTC market. In the case of the other 2 issuances, the "extraordinary events" in question were resolved and the companies in question began trading again. In the case of MMTLP this U3 halt effectively ceased trading in MMTLP forever due to the fact that the assets ultimate went private on the 14th of December. One consequence of this halt was that a significant number of short and potentially naked short shares were not forced to close out their liability position during a full reconciliation of shares back to the issued amount of 165.4 million shares. A great analogy for this is an oversold flight. It appears that in the case of MMTLP there were millions more tickets sold than there were seats available on the plane. By halting trading, FINRA relieved the airline (in this case the brokers) of the obligation to buy back the oversold tickets. As a result, investors are all still sitting in the waiting area a year later without their money or their shares. Additionally, Next Bridge Hydrocarbons still does not have a full accounting of who actually owns shares in the company.

An additional consequence is the fact that anyone who was holding shares of MMTLP in certain types of qualified accounts would ultimately be forced to recognize a distribution from that account since many of these types of accounts do not allow ownership of private companies inside of the plan. These distributions on paper have created significant tax burdens for people that took FINRA , the SEC and the OTC at their word that they would have two additional days to exit the trade to mitigate any potential tax obligations.

After the halt, FINRA did not reasonably explain their justification for the halt but rather hid from the investing public for almost 4 months before issuing a superficial FAQ that created more questions than it answered . During this time frame tens if not hundreds of thousands of complaints were made to FINRA, the FINRA Ombudsman and to the SEC by investors seeking clarity. One investor got a lucky break when he filed a FOIA request to the SEC seeking emails that may have discussed MMTLP during the relevant time frame. The cache of emails that was returned was very damning to both FINRA and the SEC. It seems that as early as November of 2021 FINRA and the SEC were communicating about potentially fraudulent activity in MMTLP but did nothing to address it. The most incriminating email however was written on the morning of December the 5th by Sam Draddy, the head of FINRA's fraud division to 3 redacted counterparts at the SEC. In this email Mr. Draddy coveys the fact that MMTLP has hit FINRA's radar screens and that he knows it has also hit the SEC's radar screens. He is suggesting that perhaps it is time that the two agencies cooperate on the issue. He goes on to say that he has already pulled the electronic blue sheets for MMTLP to investigate the issue further. Electronic Blue Sheets are ledgers that all brokerages are required to maintain on all transactions in all shares held by customers. As a result of this email, we know that on the morning of December the 5th Mr. Draddy knew exactly how many extra tickets had been sold for the MMTLP/ Next Bridge hydrocarbons flight. Rather than addressing this issue, both FINRA and the SEC allowed investors to buy more shares/tickets for another 4 days before permanently grounding the flight and not offering to issue any refunds or credits or explanations.

As a result of the perceived apathy and/or regulatory misconduct by FINRA and the SEC, many investors have turned to their representation in Washington DC to try and compel these regulators to do their job. Over the course of roughly the last 9 months over 200 congressional offices have met with constituents that believe they were harmed by the U3 halt. In total 89 members of the House and Senate have signed their names to letters demanding transparency and clarity from FINRA and the SEC. Just last month an open letter authored by Representative @RepRalphNorman garnered 74 bipartisan signatures from members of the US House.

Viewable here: https://t.co/y2pBHLMPwm

Additionally, time has been allocated by both members of the Senate Banking Committee and the House Financial Services Committee to question Gary Gensler and representatives of FINRA under oath during committee hearings. There have also been questions for the record submitted by other members of these committees. Unfortunately, all of these inquiries have been met with stonewalling tactics and very few answers to important questions.

@TuckerCarlson I met you at this year's Heritage Foundation & u were intrigued by our tragic story. Yes, the one where Wallstreet stole Billions from innocent #MMTLP investors, & yes 1 yr. later we still haven't received our $ back; We need you, please! https://t.co/WNtb38NMUz

$MMTLP Another 🧵in response to the November 6th, 2023, FINRA MMTLP Supplemental FAQ attempting to explain their actions regarding the corporate actions and trading halt.

https://t.co/4TqV14Z2TM

FUN FACT: @FINRA has used the "Investor Insights" content section of https://t.co/7LDOwaEkWv to provide educational tools catered to retail investors for 8 years. Guess how many "articles" have ever been centered around a single ticker? TWO and both were addressing #MMTLP. Ticker based FAQ's from FINRA are even more rare than a U3 Halt.

Link to prior #FINRAfraud FAQ rebuttal:

https://t.co/y9Zs2d3za5

While FINRA attempts to cast blame on the issuer and their corporate action, what they fail to address, or intentionally ignore, is the issuer’s Corporate Action was submitted with ample time for an exhaustive review, and then rewritten by FINRA at the eleventh hour; an action FINRA declares they lack authority to do in their various communications and publications. Conveniently absent from all of FINRA’s FAQ’s, the corporate action’s instructions were so confusing to the impacted parties (including, among others, the DTCC), FINRA failed to appear at a scheduled meeting meant to provide guidance and clarity to those parties. Coincidentally, FINRA took these actions knowing there was possible fraudulent activity in the trading of MMTLP, as evidenced by their email correspondences with the Securities and Exchange Commission (SEC) beginning in late November 2021 through the morning of December 5, 2022 when they reviewed of the Electronic Blue Sheets (EBS) – none of which they have publicly admitted to as of yet in any of their FAQ’s.

FINRA continues to receive questions regarding the circumstances surrounding these events because of the lack of real transparency with both the investing community and the multitude of Congressional inquiries to FINRA and directly to SEC Chair Gary Gensler. Instead, FINRA elicits more suspicion by the complete lack of transparency, misdirection of the core issue of the MMTLP situation (were investors defrauded with counterfeit shares), and finally, their refusal to provide a certified audited share count of the 105 broker/dealers holding open short and long positions in MMTLP, something recently ordered, in an unrelated case, by a federal judge in In Re Sorrento Therapeutics, Inc.

From the outset, FINRA attempts to disparage the grassroots retail community that evolved out of the MMTLP situation’s central issue and feigns a lack knowledge of what is meant by the term “counterfeit shares.” Rather they describe the situation using the more innocuous industry term “naked short selling” as if to imply the selling of US Securities without having a proper locate somehow legitimizes the actions of market participants and magically makes the practice legal and viewed as normal market mechanics. It doesn’t. 🤨

Investors’ concerns are further legitimized as broker/dealers (FINRA’s members) have made attempts by shareholders of MMTLP to transfer their shares to Next Bridge Hydrocarbon’s transfer agent confusing and prohibitive with untruths, conflicting instructions, exorbitant fees, and excessive timelines, with many even refusing to transfer the shares at all. More egregious are documented occurrences of FINRA’s member firms terminating customer relationships and closing accounts of shareholders requesting transfer of their MMTLP shares to the issuer’s transfer agent, a process that enables their shares to be directly registered in the shareholder’s name, in book entry, with the stock issuer. This is particularly ironic given the SEC’s recent publication outlining the benefits of direct registration of US Securities.

The following response provides a rebuttal to FINRA’s FAQ and calls on them to definitely address the questions posed to them by MMTLP investors and Congressional Representatives.

Just got a chance to read the @Forbes article regarding

$MMTLP $MMAT

Man that is SOO misleading.

Seems they didn’t care to do real DD. Also, they didn’t care to mention how it Illegally was traded, even after they were informed about it from @TRCHEnergy@Metamaterialtec@palikaras@johnbrda.

Or, how we have emails from Finra about the U3 “extra ordinary”

2day early Halt.

Remember, the 505 codes, them finally starting to get caught from all the $TRCH market manipulation with share shortage.

Still waiting on $mmat $MMTLP merger to be covered.

Didn’t care to mention the multiple lawyers fighting for bluesheet data from a year old delisted ticker.

Or who created $mmtlp/trade.

Why no comment or picture on this 0.00% market transparency retail has gotten since last year.

No mention of $MMAT average 60% off exchange. Yesterday was 73.19%

I thought you were suppose to be credible.

Very disappointing..

#NakedShorting #Darkpool

There is discontent among some members of Congress about the behavior of specific individuals in the #MMTLP community on social media. #MMTLPFiasco

However, this does not change the fact that fraud was committed in the equities market. 📊

We, as shareholders, were not part of any leadership or organization when we came together. It is not a top-down decision structure. This is a decentralized movement! 🗣️🗣️

The halt on December 9th, 2022, led us to unite out of necessity. We found comfort in knowing that we were not alone, and through social media, we were able to channel our pain into action, working towards a resolution for all shareholders. 📲📲

Congress has difficulty getting its 535 members to work together, even though they all work in the same location and have the liberty of meeting face to face.

Nevertheless, they expect us, a diverse base of 65,000 investors, to control the language of our community members? 🙃🙃

Just as there are congressional members who make inflammatory statements (regularly), we cannot control what each individual says. No more than Congress could control what our previous President would say.

Congress must recognize that freedom of speech is deeply ingrained in the American identity. It is unrealistic to believe we can regulate the speech of shareholders who have endured hardships for nearly a year due to this issue. Many individuals are currently facing real challenges as a result of this situation. 🇺🇸🇺🇸

Although we should focus on taking action rather than creating drama, we must remember that we are a community of 65,000 shareholders.

While we should all maintain a sense of decorum, it's also crucial for Congress to fulfill its duty and address the significant injustices in the equity markets, regardless of any words online. 🗳️🗳️🗳️

There have been nefarious actions against the investing public that need to be addressed and resolved before they become widespread in the press and the world realizes what is happening with the American stock market. 📰📻📺