🌀🌀🌀🌀‼️‼️‼️‼️‼️✅✅✅✅✅✅✅✅SORTEO CURSO.OPCIONES DELUXE WINTER EDITION👻👻👻👻👻👺👺👺👺👺👺👺❎🔰🔰♻️🈯️🈯️

SORTEAMOS 2 LUGARES ENTRE RT Y LIKES

Bueno, después de que lo pidieran sacamos otra edición en vivo de CURSO.OPCIONES con @tomiechecopar y esta vez se suma a explicar FUTUROS @gordoggal. Para el cierre tenemos a @gregorechi y @Roodri91 de Operando lotes con rodrigo para contarnos como operan ellos !

TODA la info en mi twit fijado o en https://t.co/5qBUESHJSV

OPCIONES, ESTRATEGICAS, SINTÉTICAS, FUTUROS Y SIEMPRE DE GENTE QUE VIVE DE OPERAR ! NOS VEMOS AHÍ

$MU and homebuilders are more similar than you might think.

Everything about a home builder is basically a commodity product.

It is often taught that commodity products cannot maintain high returns, but if you look at the ROE of many home builders you’ll see many in the 20%+ range. Sometimes much, much higher.

These businesses have a product that anyone can produce, but the reason why their economics are maintained is because demand outstrips supply.

There is more demand for (moderately/ low priced) homes than we create. Thus virtually every home that gets built gets sold—and at a price that provides ample margin for the builder.

When these businesses do poorly is when demand temporary sags and the carrying cost of inventory (construction loan interest expense) weighs on returns. Aggressive financing on the builders parts, could result in bankruptcy in such situations.

Generally though, demand for homes is only going to go up overtime and will continue to outstrip the pace of building—at least in the U.S.

The situation is different in China for instance where supply increases has resulted in very soft home prices and phantom cities.

The point I wish to make is that competitive moats are only pertinent to a business when supply outstrips demand.

If you can differentiate your product sufficiently, the consumer preferences you are fulfilling are unique enough that the business itself is the sole supplier.

They have escaped the rat race of commodity competition where any business can build what they build. If you want an iPhone, there is only one seller. If you want fast delivery on millions of items through a high trust seller, there is only Amazon (in the U.S.)

The less emphasized point though is that even if your product is undifferentiated, so long as supply runs below demand, you can have a strong business.

We are seeing this phenomenon in memory chips, energy supply, and data centers. The demand is overwhelming and so many business that fit the bill of being a commodity product can reap stellar margins and returns on capital—for now.

Micron posted 68% operating margins. 3 years ago they were as low as -63%.

With capacity constraints and capital flooding into the data center build out, they certainly have strong tailwinds to continue to post such stellar margins.

However, the problem with such businesses comes from the fact that these high returns draw in incremental capital and eventually growth in supply will overshoot demand.

While a cycle can take years, it doesn’t change the fact that memory is not a differentiated product the same way a Nvidia GPU chip or Arista network switch is. (That doesn’t mean they can’t also have their own cyclically though—just that by and large the market for Nvidia GPUs, is different than the market for “GPUs”)

Investing in such businesses becomes a bet on the capital cycle duration and a bet on the rationality of multiple players. It works so long as demand is higher than supply, but when the situation reverses, the commodity-like returns of an undifferentiated product returns. (Memory investors are basically betting that AI demand has resulted in a paradigm shift where demand will continue to outpace supply for many years—perhaps a decade… but Wall Street only tends to model 3-5 years out).

Building constraints in the U.S. has prevented economic deterioration in the home building industry. (Even in a weak year like 2021 a small home builder— Dream Finders Homes had a 12% ROIC, higher than most businesses). The time it takes to build new fabs has prevented this from immediately correcting in the memory industry, but it is inherently a more precarious competitive position to be in because the businesses do not control their destiny. Apple can control the production of iPhones, but Micron cannot control the supply of HBM.

This is not to say this is a “wrong” way to invest—there are many ways to make money. But just that the timing of such investments are much more critical than say investing in a Red Bull or Monster. The customers of those business’s only want a “Red Bull” and alternatives (by and large) will not do. Thus the vectors of competition move from trying to create a better Red Bull rather than simply supplying an energy drink.

The history of businesses that do not have moats is brutal. Capitalism will eventually compete down those returns. But that doesn’t mean an investor can’t make money if they time the capital cycle right—they should just be aware that is the bet they are making.

Que va a pasar mañana? Ni idea, pero mira las 2 imagenes.

Ayudin: La probabilidad de que el Costo del Bull sea menor que hoy es de 100%. No dije por cuanto, dije que va a ser menor. Veremos.

De paso agregue en Historicos el Modo Strat, para ver el grafico que comparto siempre.

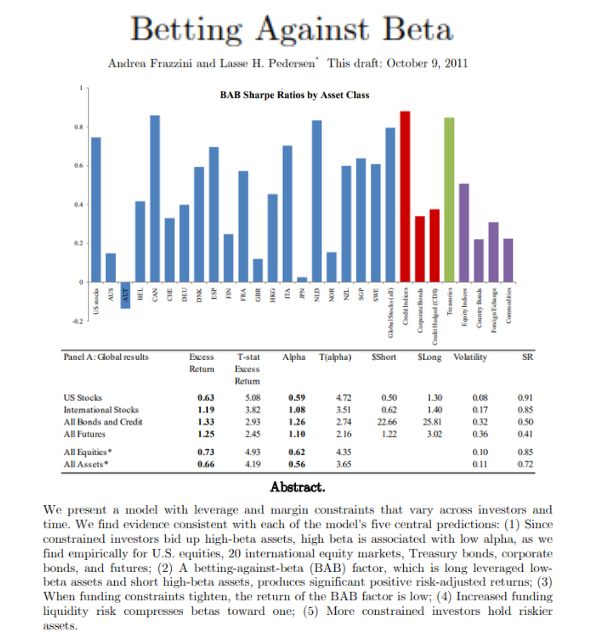

🔥 "Betting Against Beta" El paper que rompió el CAPM y explicó matemáticamente cómo gana Warren Buffett

Frazzini y Pedersen (AQR Capital + NYU + Copenhagen Business School) publicaron esto en 2014 en el Journal of Financial Economics. 86 años de data, desde 1926 hasta 2012

Testearon la estrategia en acciones US, 20 mercados internacionales de equities, bonos del Tesoro, corporate bonds, futuros, FX y commodities

La teoría del CAPM dice que a más riesgo (beta), más retorno esperado. La realidad muestra lo contrario: las acciones de bajo beta tienen mejor retorno ajustado al riesgo que las de alto beta

¿Por qué? Porque la mayoría de los inversores (pension funds, mutual funds, individuos) no pueden apalancarse fácil, entonces compran high-beta para tener más exposición. Eso infla el precio del high-beta y deja al low-beta barato

La estrategia es simple: comprás acciones low-beta apalancadas hasta beta 1 y vendés en corto acciones high-beta desapalancadas hasta beta 1. Eso es el factor BAB

Los números son una bestia:

- Sharpe 0.78 en US equities (1926-2012), casi el doble que value

- Sharpe positivo en CADA uno de los 4 sub-períodos de 20 años

- Funcionó en los 20 mercados internacionales testeados

- Sharpe 0.85 en bonos del Tesoro

- Retorno positivo en TODAS las clases de activo

Lo más interesante: en un paper hermano ("Buffett's Alpha", 2018), los mismos autores agarraron 30+ años de Berkshire Hathaway y mostraron que el alfa de Buffett se vuelve estadísticamente insignificante cuando controlás por BAB + Quality

Berkshire opera con leverage de 1.7x usando el float de seguros como financiamiento ultra barato. Sharpe de Berkshire: 0.79. Casi idéntico al Sharpe del factor BAB

Buffett no es magia. Es BAB + Quality + leverage barato

Link al paper en el primer comentario.

ATRAPAMOS AL LÍDER RUSO DE LAS FAKE NEWS

Dmitrii Novikov entró como turista, pero venía a operar, desestabilizar y atentar contra nuestras instituciones. Una amenaza para el orden democrático.

Lo detectamos, lo detuvimos y lo vamos a expulsar.

Reglas claras. Ley y orden.