Investor | Sharing Insights on AI & Stocks | Data Engineer | Believer in FIRE | Learner

Investor in $OSCR, $UNH, $NVDA, $TSLA, $RKLB, $ASTS, $AMD, $HIMS

NVIDIA DSX AIR is being installed

- $CRWV

- Lambda Labs

- Crusoe

- $IREN - Currently using DSX Air to simulate and validate the physical networking infra for an upcoming deployment of over 50K NVIDIA Blackwell Ultra GPUs.

- $NBIS

- Nscale

- Siam AI

- Yotta Data

- Firmus

A look into $AAPL supply chain for WWDC ;

$MU — Makes DRAM/NAND memory chips used in iPhones, Macs, and iPads.

$QCOM — Supplies cellular modems for iPhone

$AVGO — Provides RF chips, Wi-Fi/Bluetooth combos, and custom ASIC co-development with Apple.

$SONY — Manufactures the CMOS image sensors behind iPhone cameras.

$SWKS — Makes RF front-end chips enabling cellular connectivity; also losing share to Apple’s internalization.

Still think this US list from $MRVL to $ARM to $INTC was goated.

Just as a recap if new followers were wondering what US equities I like.

Especially because I've been talking about international companies recently.

@DollarCostAvg what is the cost of building 1MW datacenter capacity?, Also ongoing maintenance charges and GPU replacement cycle, this need to be priced in to understand accurate picture of this revenue.

AirTrunk just announced ₹3 lakh crore to build 5 GW of data center capacity in India by 2030.

That alone is more than 3x the entire country's operational capacity today.

The headlines will focus on the operator. But ₹3 lakh crore doesn't stay with the operator. It builds the shell and buys everything inside it.

So, the more useful question is: where does this money actually flow? Here's the full value chain 👇

India runs 1.5 GW of operational data center capacity today across 160+ facilities. Street estimates put the country at 5-8 GW by 2030. Market size: $10bn in 2025 → $22bn by 2030.

AirTrunk entered India, via the Lumina CloudInfra buyout, with a 600 MW starting pipeline across Mumbai, Chennai and Hyderabad. Backed by Blackstone and CPPIB.

The demand stack is broad:

🔹 AI training and inference

🔹 Hyperscale cloud (AWS, Azure, Google)

🔹 Data localisation (RBI norms, DPDP Act)

🔹 5G + 25GB+ monthly data per user

🔹 Digital payments and enterprise digitisation

India builds at ~$6-7M per MW, cheaper than Singapore or Japan. Cheap to build, captive demand, 20-year tax holidays. Structural, not cyclical.

⚡️ Why AI Data centers are a different from Traditional Data Centers.

A traditional rack draws 5-15 kW. An AI rack draws 30-130 kW. NVIDIA's GB200 NVL72 pulls 130 kW in one rack. A GPU burns 700-1,000W per chip. A CPU burns 150-200W.

That single fact rewrites the build:

🔹 Air cooling dies past 30-40 kW per rack. Liquid cooling becomes mandatory (handles 100-200 kW)

🔹 PUE matters more. Liquid runs 1.05-1.15 vs 1.4-1.6 for air

🔹 More fiber per rack for high-density, low-latency interconnect

🔹 Heavier power gear per MW. Transformers, switchgear, UPS

An AI data center consumes far more equipment per MW than a legacy colo. The spend concentrates below the operator.

The value chain, layer by layer

Land + build → operators

🔹 Anant Raj: 28 MW operational, targeting 63 MW by Dec 2026, 357 MW by FY32. DC + cloud revenue ₹176 cr in FY26.

🔹 Bharti Airtel (Nxtra), Reliance (Jio), Adani (AdaniConneX). Jefferies sees these three at 35-40% of capacity by 2030. Sify is the NASDAQ-listed pure play.

Power infrastructure → the real chokepoint

🔹 Hitachi Energy India: order backlog ₹29,000 cr. Data center was the single largest order-segment contributor in both Q3 and Q4 FY26. Just added ₹2,000 cr capex for a new transformer plant.

🔹 CG Power: order book ₹14,800 cr across transformers and switchgear.

🔹 GE Vernova T&D, Siemens Energy, ABB India sit in the same HV pool.

Backup power → gensets, batteries, UPS

🔹 Cummins India: in Q2 FY26 its power-gen segment grew 50% YoY, with data centers alone making up ~40% of that segment. Every 1 MW of IT load needs up to ~1.5 MW of standby diesel.

🔹 Kirloskar Oil Engines: KOEL Green, the other large listed genset name.

🔹 Amara Raja: largest share in India's data center battery segment (VRLA / UPS).

Cables (power + EHV)

🔹 Polycab: Data centers named as a core driver under its ₹6,000-8,000 cr "Project Spring" capex.

🔹 KEI Industries: EHV cables + US data center exports.

Cooling

🔹 Aeroflex Industries: Just entered AI data center liquid-cooling skid assemblies, 5% of FY26 sales, management guiding to 20-22% in FY27 as it scales capacity from 2,000 to 15,000 skids a year.

🔹 Blue Star, Voltas: precision cooling and chillers. As liquid cooling scales, this layer shifts from commodity HVAC to mission critical.

Connectivity → optical fiber

🔹 Sterlite Technologies (STL): order book ₹7,309 cr in FY26, Enterprise + DC is 20% of revenue, guided to 30%. Its Celesta cable packs 864 fibres in a sub-12mm diameter, built for AI data halls.

🔹 HFCL: optical fiber + telecom equipment.

Compute → servers, GPUs, AI cloud

🔹 Netweb Technologies: AI segment grew 460% YoY in Q4. Won a ₹1,734 cr sovereign-AI order on NVIDIA Blackwell under the IndiaAI Mission.

🔹 E2E Networks: the listed GPU-cloud play. 3,900 NVIDIA GPUs, deploying Blackwell B200 clusters, empanelled under the IndiaAI Mission, hosting capacity at L&T's Chennai facility.

📌The opportunity ahead:

India’s data center opportunity is moving from 1.5 GW today to 5–8 GW by 2030.

But the real opportunity is not just in operators. It is in the layers beneath them: power, cooling, fiber, equipment and compute infrastructure.

As AI workloads rise, every MW needs more equipment intensity than before.

Digital India was earlier an app story. This decade, it becomes a hard-infrastructure story.

📌Disclaimer: This is for educational purposes only and is not a buy or sell recommendation. Please do your own research.

Nuclear bulls, you might want to pay attention to this.

During a live event at the Oval Office today, a reporter asked about small modular reactors. Energy Secretary Chris Wright responded by emphasizing just how important SMRs are to America's energy future.

Then he casually dropped this:

"Before the sun goes down today, you'll see a BIG announcement in the nuclear space."

I've been pounding the table on nuclear for months now. Let's see what they've got cooking.

$ASPI $BWXT $CCJ $IMSR $LEU $NNE $OKLO $SMR

@DollarCostAvg What is the cost of building 1 MW capacity ? I read it takes 40-50 billion to build 1 GW capacity if that’s correct it cost 4-5 million / MW.

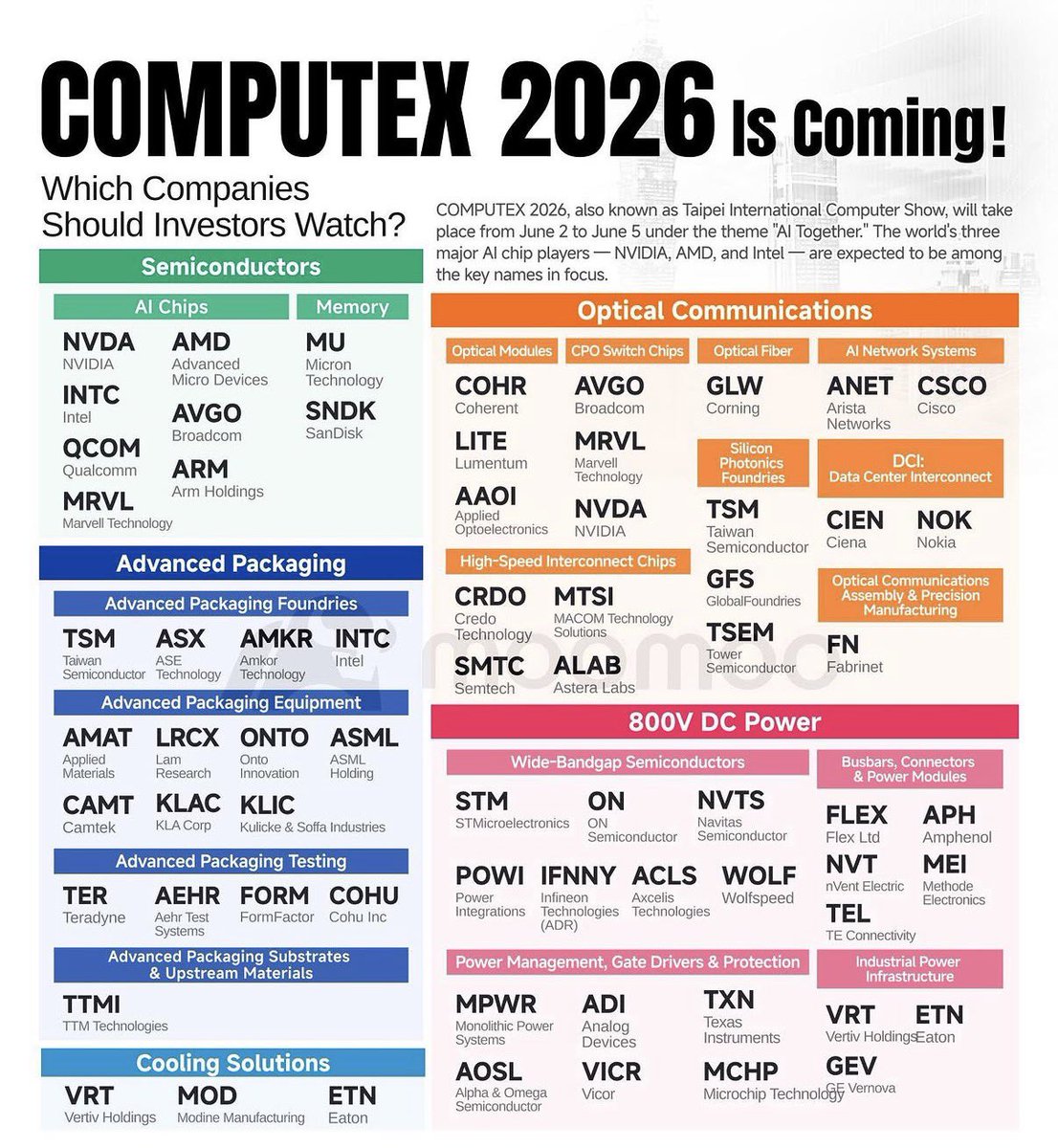

10 stocks to watch during Computex 2026. These are key data centre related stocks :

$MU — HBM4 36GB delivering 2.6x inference throughput; memory bull case just got louder.

$MRVL — Jensen called Marvell the next trillion-dollar company; CPO chips confirmed future.

$VRT — Rack power hitting 180kW; Vertiv’s power and thermal management demand accelerating fast.

$LITE — Named as relevant across optical modules and fiber alongside Coherent; CPO wave rising.

$ARM — RTX Spark is Windows on Arm; Nvidia just validated Arm’s PC architecture ambitions hard.

$AAOI — Makes optical networking components (lasers, transceivers) for data centers and telecom.

$AOSL — Designs power semiconductors (MOSFETs, gate drivers) for consumer electronics and EVs.

$POWI — Makes energy-efficient power conversion ICs for appliances, IoT, and industrial use.

$GLW — NVIDIA partnership locks Corning into AI factory fiber supply; 10x US manufacturing capacity.

$ANET — Capturing majority of 800G and 1.6T switch upgrades as AI clusters shift to open Ethernet-over-Fiber.

$ON — No direct Computex presence found. ON Semi is a Computex spectator, not a headliner.

NVIDIA is telling you exactly where to invest with its new 800V DC power architecture.

The old 48V system can't keep up. 800V reduces copper usage by 45%, cuts the power chain from 5 conversion stages to 2, and cuts power delivery losses in half.

These 7 companies are building the power layer underneath it all.

1. $ON - onsemi

SiC and GaN chips for high-voltage power conversion across AI and EVs. AI data center revenue nearly doubled YoY and is expected to double again in 2026. The key number: their content per AI rack scales from $15,000 today to $115,000 in next-gen 800V architectures. A 7.7x increase per rack deployed.

$NOW can easily triple from $125 by Jan 2027.

Remember, token use is expected to 2800% in 5 years says $GS.

So these 24 stocks can still 10x-20x:

(COMPUTE / GPU)

1. $NVDA — Every token touches a GPU. 24x tokens = 24x chip demand, full stop.

2. $AMD — MI300X gaining enterprise traction. Second GPU source as hyperscalers diversify suppliers.

3. $INTC — Gaudi AI accelerators + x86 CPUs running inference at the edge and enterprise.

(NETWORKING)

4. $ANET — AI clusters need ultra-low latency switching. 24x tokens = 24x network traffic routed.

5.$AVGO — Custom AI ASICs for hyperscalers. Token volume drives ASIC and switching orders higher.

6. $CSCO — Data center fabric and ethernet switching. Every agent call crosses Cisco infrastructure.

7. $CIEN — Optical networking backbone connecting AI data centers. Bandwidth demand scales with tokens.

(MEMORY / STORAGE)

8. $MU — HBM3E stacked on NVDA GPUs. More inference = direct memory bandwidth demand explosion.

9. $WDC — Flash storage holds model weights and KV caches. Agent scale drives NAND demand structurally.

10. $STX — Hard drives store cold AI training data. Data center storage TAM expands with every model.

(POWER / COOLING)

11. $VRT — More tokens = more heat. Liquid cooling demand explodes alongside data center power density.

12. $ETN — Electrical infrastructure for AI data centers. Power management is the #1 buildout bottleneck.

13. $GEV — Gas turbines and grid solutions powering new data center campuses requiring gigawatt-scale energy.

14. $VST — Power generator selling directly to hyperscalers. AI energy contracts already locked in long-term.

(CLOUD PLATFORM)

15. $MSFT — Azure hosts majority of enterprise agents. Token spend flows straight through its cloud margin.

16. $AMZN — AWS Bedrock is the enterprise agent backbone. More agents, more API calls, more revenue.

17. $GOOGL — TPU infrastructure + Gemini API. Every token processed on Google Cloud prints margin.

(ENTERPRISE AGENT LAYER)

18. $NOW — Enterprise agents run on its platform. Every workflow automated burns more tokens daily.

19. $CRM — Agentforce deploys AI agents across sales, service, and marketing. Per-action token billing scales.

20. $PLTR — AIP platform runs AI agents on enterprise and government data. Token volume is its revenue driver.

(AI INFRASTRUCTURE)

21. $NBIS — Pure-play AI infrastructure at ground level. Token supercycle lifts the entire compute ecosystem.

22. $SMCI — Builds GPU server racks for data centers. Every NVDA chip needs a SMCI chassis to run.

23. $DELL — AI server sales to enterprises exploding. Token growth drives hardware refresh cycles faster.

24. $ARM — Chip architecture inside every mobile and edge AI device. Royalties scale with token proliferation.

$NOW is the most undervalued right now. This is why Jensen Huang says the market has made a mistake on it.

♻️ RESHARE this post and write 1 comment, I'll DM you the best $NOW contract to buy and hold.

Without these chips, the AI power problem has no solution. Introducing Power Semis :

$ON — Power chips for EVs and AI data centres that convert electricity efficiently.

$WOLF — The only pure-play maker of silicon carbide chips that handle extreme voltages.

$POWI — Tiny chips that convert wall power into usable electricity for devices and equipment.

$MPWR — Regulates voltage inside servers and AI hardware so components don’t fry.

$NVTS — Next-gen chips that charge faster using less energy, expanding into EVs and data centres.

The next bottleneck is POWER ⚡️

$VST — Power plant operator. Profits rise when electricity prices spike.

$VRT — Keeps data centers cool. Sells thermal management hardware.

$OKLO — Pre-revenue startup building small modular nuclear reactors.

$CCJ — World’s largest uranium miner. Feeds nuclear power plants.

$ETN — Makes breakers, transformers, and switchgear that distribute electricity

$POWL — Builds custom electrical systems for refineries and industrial plants/data centres.

I’ll say this one last time: these 10 companies will mint millionaires by 2030.

My top picks for May:

1. $SATL(Satellogic) — $10 → $16 2.

2. $IREN(Iren) — $64 → $120 3.

3. $ASTS(AST Spacemobile) — $126 → $320 4.

4. $RKLB(Rocket Lab) — $146 → $210 5.

5. $NBIS(NEBIUS) — $226 → $375 6.

6. $NOK(Nokia) — $15 → $24 7.

7. $USAR(USA Rare Earth) — $27 → $43 8.

8. $LUNR(Intuitive Machines) — $42 → $74 9.

9. $BKSY(BlackSky) — $51 → $78 10.

10. $NOW(ServiceNow) — $100 → $180 Come back to this post at the end of 2026, & you’ll thank yourself that you listened…

@Venu_7_ True, people only make money with their own convictions and not by the ticker somebody discovered first. Thesis helps, but most folks who develop convictions do their own research before committing big amount..