it's not the tourists underwater this time.. it's the long-term holders.

~45% of $BTC LTH supply is now sitting in a loss, the same level reached at every cycle bottom in history & we're not even under realised price.

if the strongest hands haven't sold yet (besides @saylor), who's left to?

Robert Sapolsky es un neurocientífico de Stanford que demostró que el estrés es el asesino silencioso que los médicos ignoran.

Reveló 10 hábitos que haces todos los días y que te quitan años de vida.

1) Repasar conversaciones en tu cabeza

$MARA is the worst performer on this board and it's not close.

$HUT, $CIFR, $IREN and the rest each signed a hyperscaler or neocloud lease (Google, Microsoft, CoreWeave, Core42, AMD) and got re-rated as data centers.

Every one of them moved hundreds of percent the moment the market believed the pivot was real.

MARA's pivot is just as real a 505 MW gas plant via Long Ridge, an EDF-backed compute arm in Exaion, a 2.5 GW Starwood JV, but none of it is a signed, bankable lease yet. So the tape still prices it as a levered Bitcoin proxy.

***THE SHARPEST PART***

To be short $MARA here, you have to believe one specific thing - that this company never makes the pivot. Never signs a lease. Never closes a deal. Ever.

That's not a valuation call

It's a bet that the only management team sitting on gigawatt-scale power, an EDF-backed AI arm, and a Starwood JV somehow fails at the exact thing every competitor on this chart already pulled off.

You're shorting a flat tape to collect almost nothing while every name above MARA is a live preview of the payout the day the lease lands

$MARA MARA has an AI infrastructure investment that I think most investors are overlooking:

-MARA helped seed-fund Auradine, now known as Velaura AI, and owns roughly 15% of the company

-Velaura has since spun out Upscale AI (AI networking) and Aurascape (AI security)

-$MARA CEO Fred Thiel sits on the board alongside $INTC CEO Lip-Bu Tan

-Velaura is focused on next-generation AI infrastructure, including energy-efficient compute and data center technologies

-Upscale AI is focused on AI networking, the layer responsible for moving data between GPUs and AI systems

-As AI models become larger, networking is becoming increasingly important because GPUs are only as valuable as the data flowing between them

-When data movement becomes the bottleneck, performance suffers and expensive AI infrastructure becomes less efficient

-Aurascape is focused on securing AI systems, agents, and enterprise data as AI adoption continues to accelerate

-Through a single investment, $MARA has exposure to compute, networking, and security, three critical pieces of the AI stack

-I think investments like Velaura help explain why $MARA is becoming much more than what most investors think it is today

ÇOK GÜZEL BİR MİKRO HİSSE BULDUM - ABD

Yapay zeka veri merkezleri çok yakında elektriksiz kalacak. Bu krizi servete dönüştürebilecek gizli hisse $PPSI

Yapay zeka veri merkezlerinin en büyük yapısal sorunu ne? Enerji krizi. Şebekeler bu yükü kaldıramıyor. Peki ben bu ��irkete neden takıldım?

🔵Geçtiğimiz aylarda AI veri merkezleri için geliştirdikleri PRYMUS mobil enerji bloklarını tanıttılar. Ve Mayıs 2026'da dev bir lojistik firmasından 6 milyon dolarlık ilk PRYMUS siparişini kaptılar bile.

🔵Mikro ölçekli şirketlerdeki en büyük risk borçtur. $PPSI’ın banka borcu SIFIR. Kasasında 13.6 milyon dolar nakit var ve birikmiş iş hacmi 13.9 milyon dolara yükseldi.

🔵Son çeyrekte brüt kar marjını %2.2'den %13.6'ya fırlattılar. Ayrıca yıllık operasyonel giderleri 1.5 milyon dolar düşürecek agresif bir maliyet yönetimi başlattılar.

Şu an 4.10$ seviyelerinde işlem gören hisse için Wall Street analistlerinin ortalama hedef fiyatı 9.50$. Bu da demek oluyor ki %120+ potansiyel.

(Görsel Midas'tan alınmıştır)

$MARA is trading at a $4.8B market cap.

Here is the math the market refuses to do:

→ 35,303 BTC in treasury = ~$2.2B (even with Bitcoin down 50% from ATH).

→ That leaves ~$2.6B for the ENTIRE operating company.

→ 72.2 EH/s of hash rate + 1.3 GW of energized power infrastructure roughly covers that on its own.

Which means the market is pricing at **ZERO**:

⚡ Long Ridge - 505 MW vertically integrated power campus, ~$144M annualized EBITDA, 76% contracted, ~$15/MWh operating cost, path to 1+ GW. Closing hurdle cleared 48 hours ago.

🇫🇷 Exaion - 64% of EDF's nuclear-powered AI compute arm. Sovereign French energy access. Unreplicable at any price.

🏗️ Starwood JV - hyperscale campus development where Starwood carries the capex, not MARA's balance sheet.

🤝 And management, on the record: "advanced conversations with multiple prospective tenants across multiple sites." Inbound interest from investment-grade hyperscalers. ~90% of owned capacity in active tenant discussions.

2.2 GW at closing. In PJM. In 2026. While hyperscalers fight over electrons.

Before the bears scream "debt", converts were cut 30% in ONE quarter. $1B retired at 91 cents on the dollar.

One signed lease changes the entire equation.

IREN traded like this once. Ask the shorts how that ended.

$PENG

"Why we are buying Penguin Solutions"

When executing a multi-factor validation process, the highest-conviction ideas rarely appear in a vacuum. Instead, they hit you as a trifecta of independent signals: a macro sector thesis, an algorithmic screener breakout, and major institutional validation. $POET's performance sent me down the rabbit hole for niche tech. My stock screener caught $PENG's relative volume. Trump's trading disclosures noted an accumulation of the stock (GREEN LIGHT!)

Here's a breakdown of why this is a mandatory investment based on the growing demands of the AI buildout and why $PENG is becoming an essential player...

1. Core Mechanics: Expanding the Capacity

MemoryAI™ Expansion: Leveraging CXL® (Compute Express Link) standards alongside partners like SK hynix and Micron, $PENG servers expand memory capacity up to 11 TB per appliance.

Decreasing HBM Dependence: By offloading the KV cache to specialized memory appliances, they reduce reliance on the expensive, supply-constrained HBM3e chips produced by SK hynix and Samsung.

Improving GPU ROI: This architecture ensures that high-cost chips from $NVDA (H100/H200) and AMD (Instinct MI300X) aren't sitting idle. They feed the "beast" faster through a larger pipe.

2. The Customer Base: Scaling the "Factories"

Hyperscalers: Providing validated rack designs for the "Big Three" (AWS $AMZN, Google Cloud, and $MSFT Azure) to help them scale without hitting the thermal limits of legacy data centers.

Sovereign AI & Enterprise: Recently selected by Deepgram to enable massive enterprise voice AI inference, and continuing long-term work with National Labs (Sandia, NNSA).

NeoClouds: Powering the new wave of AI-first cloud providers like CoreWeave, Lambda, and Volt, who need to deploy "AI Factories" faster than the traditional giants.

3. The 4-P Execution Strategy

Pipeline: Doubled FY26 growth guidance (6% to 12%) as the market moves from buying chips to building full-scale data centers.

Product: The OriginAI® Platform—a turnkey solution that integrates Intel Xeon or AMD EPYC CPUs with high-density GPU clusters and specialized liquid cooling.

Partnerships: A flagship 3-way alliance with $AMD and Shell to create immersion-cooled clusters, alongside a $200M strategic investment and collaboration with SK Telecom to build AI Data Centers (AIDC).

Photonics: The long-term "light-speed" play. By working at the intersection of optical interconnects—the same space occupied by $POET Technologies and Coherent—$PENG is removing the copper bottlenecks currently stalling data transfer.

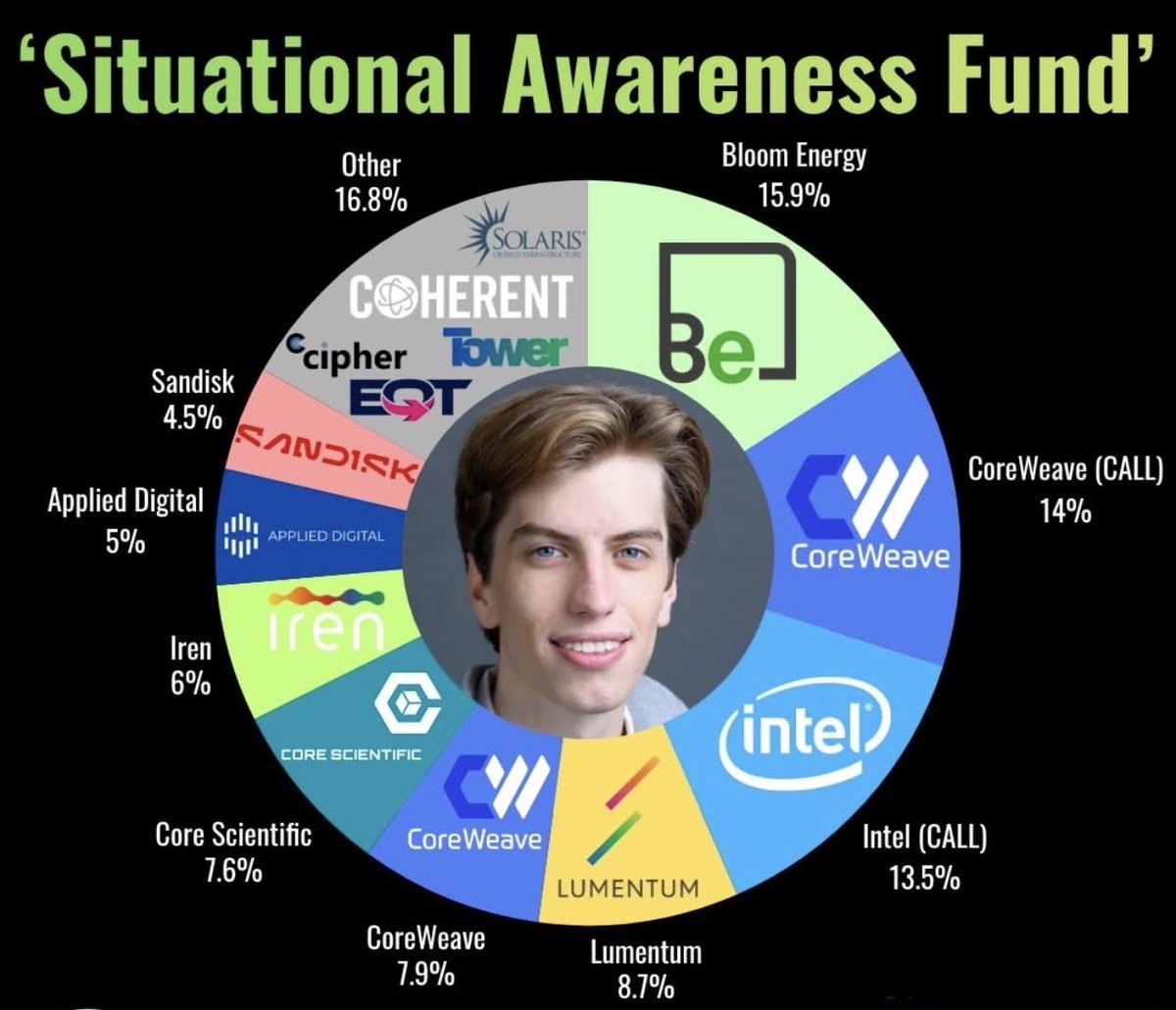

McKinsey says AI will need 219 gigawatts of data center power by 2030. That's nearly 3x today's capacity.

Here are 10 stocks powering the AI buildout:

1. $TE - T1 Energy

Manufacturing solar modules in Texas using high-efficiency TOPCon technology. Q1 revenue $177.6M, up 232% YoY, with record adjusted EBITDA of $9.1M. G1_Dallas facility running at 5 GW nameplate capacity. G2_Austin Phase 1 (2.1 GW solar cell fab) broke ground in December and targets production by end of 2026 with over 60% domestic content. Signed a 900 MW supply deal with Treaty Oak Clean Energy. Leopold Aschenbrenner's Situational Awareness fund just disclosed a 10M share position - roughly a 3.6% stake.

Anthropic a publié une Formation complet de 2 HEURES sur la construction d'agents Claude.

Animé par l'ingénieur qui construit Claude Code.

Gardez-la précieusement en Signet🔖

de A à Z : Structurer un agent qui se gère sans supervision. Lui donner accès au terminal pour exécuter, lire, corriger. Gérer sa mémoire via le système de fichiers. Bloquer les hallucinations avec des Hooks. Faire tourner un agent sur un gros codebase sans tout casser.

À la fin : vous utilisez Claude comme un pro et vous monétisez vos compétences. Débutant ou avancé, tout est là en un seul endroit, ce cours couvre tout.

Ça vaut plus que tous les cours à 500$ que t’as failli acheter.

Why Leopold Aschenbrenner is betting big on these 6 stocks ?? :

1. $LITE (Lumentum)

Core product: EML lasers, OCS (Optical Circuit Switches), CPO lasers

$LITE Thesis: order book is SOLD OUT through 2028

→ $2B Nvidia investment + purchasing deal

→ OCS backlog >$400M, 150% CAGR to 2028

→ CPO: new multi-hundred-million $ order just landed

2. $COHR (Coherent)

Core product: 800G/1.6T transceivers, InP lasers, OCS, CPO

$COHR book-to-bill just hit 4x. Demand is obliterating supply.

→ $2B Nvidia deal for U.S. optics manufacturing

→ 10+ OCS customers, CPO mega-order just received

→ Supports SiPh, InP & VCSEL — hedged for types of Hyperscalers

3. $CRWV (CoreWeave)

Core product: GPU cloud for AI workloads (Nvidia H100/B200 clusters)

$CRWV just locked in a $21B deal with Meta through 2032.

→ 850MW active today → 1.7GW by end of 2026

→ $66.8B total backlog

→ First Nvidia Vera Rubin deployments included

4. $CORZ (Core Scientific)

Core product: AI/HPC data center hosting (high-density colocation)

$CORZ went from Bitcoin miner → AI infrastructure landlord.

→ 590MW contracted with $CRWV = $10B+ over 12 years

→ $2B in infra installed across 4 sites in 2025

→ $CRWV acquisition pending ($9B deal)

5. $APLD (Applied Digital)

Core product: AI data center campuses (long-term leases)

$APLD has $16B in contracted lease revenue across 600MW.

→ $11B, 15-yr deal with $CRWV (Polaris Forge 1)

→ $5B, 15-yr deal with undisclosed hyperscaler (Polaris Forge 2)

→ Revenue up 250% YoY last quarter

6. $BE (Bloom Energy)

Core product: Solid Oxide Fuel Cells (SOFCs) — behind-the-meter power for AI data centers, deployable in 90 days vs years for grid connections

Latest deals:

∙Oracle agreed to purchase up to 2.8GW of fuel-cell power from Bloom to supply AI data centers, with 1.2GW already contracted

∙$5B strategic partnership with Brookfield Asset Management to deploy SOFCs for AI infrastructure globally

∙$7.65B in data center contracts secured in a single 90-day window in early 2026

∙Total backlog ~$20B, up 65% YoY. Product backlog ~$6B, up 140% YoY.

📈2026 revenue guidance: 50%+ growth

∙Recently delivered a hyperscale AI factory order in 55 days against a 90-day commitment .

$NVDA CEO keeps telling you to buy $NOW

He is literally saying ServiceNow will 100x

In 2025 he called:

$NBIS at $22 → +600%

$INTC at $23 → +500%

$SNDK at $275 → +400%

$CRWV at $40 → +200%

$TSM at $240 → +80%

Are you going to ignore him again?