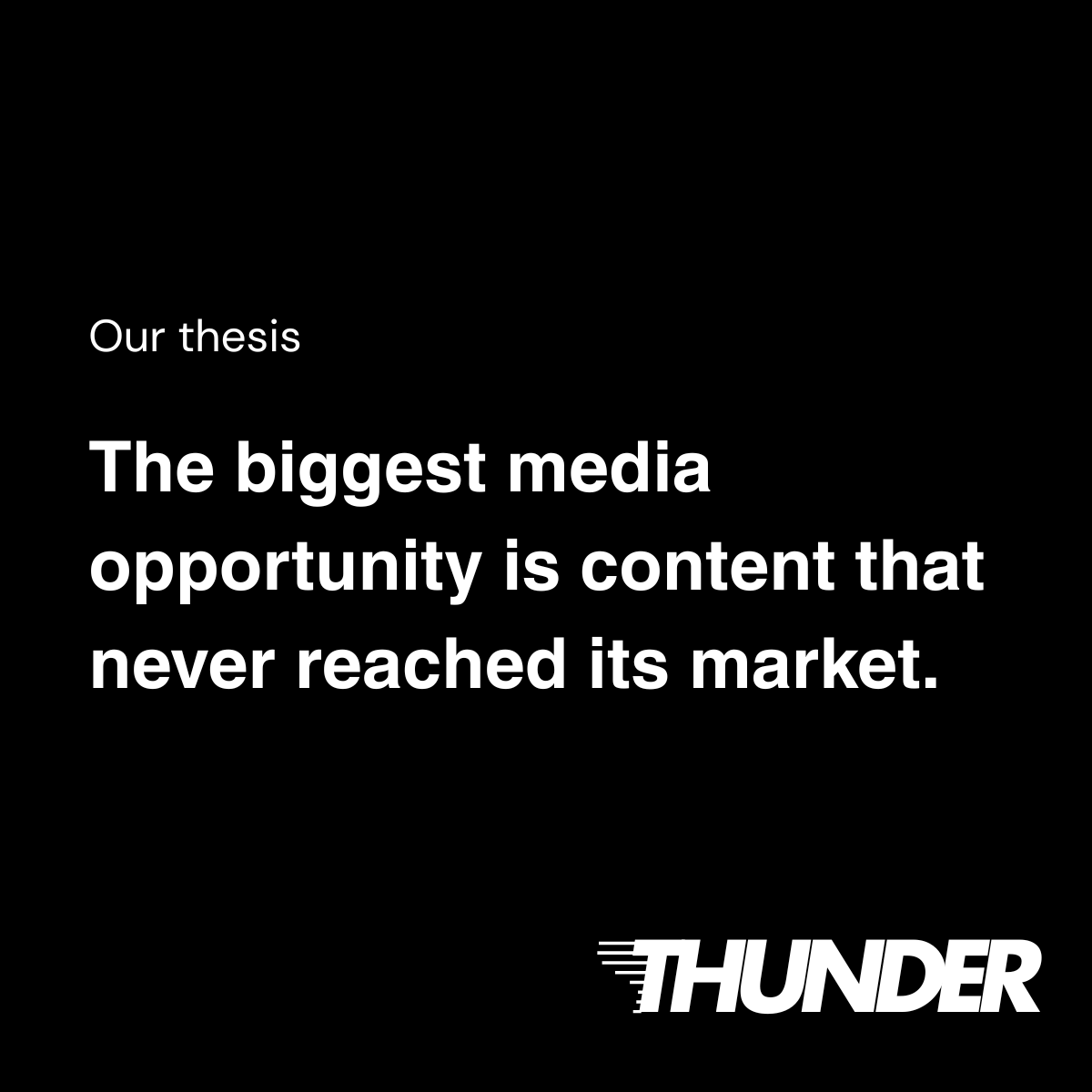

interesting to see how much valuable IP already exists, and how little of it is actually distributed where demand lives. spent the last year looking at the structural problem behind it.

the last decade solved content creation. every rights holder, publisher, studio and brand now sits on vast archives of IP. the constraint is no longer supply.

distribution, however, has fragmented. audiences have moved across YouTube, Shorts, TikTok, OTT, FAST, international platforms. most IP portfolios are still mapped to 1-2 channels while demand exists across much more.

this creates a structural inefficiency: value is not lost because content is weak, but because it is not placed correctly. distribution has become the bottleneck.

historically, media companies optimised for production and licensing, not continuous distribution. content was released, monetised once, then archived. the idea of IP as an always-on asset never fully emerged.

the result is a growing gap between existing IP and realised revenue. the underlying assets are there. the distribution is not.

This raises a new set of questions…..

🌪 how do you map where a set of IP is not currently distributed?

🌪 how do you identify which platforms are missing from a portfolio?

🌪 how do you quantify the revenue gap between current state and optimal distribution?

instead of asking "what content should we create?", the question for ceo's and boards becomes: where should this IP exist, and what is the revenue potential if it does?

🌪 Read more about Thunder’s 2026 thesis on https://t.co/QOKWNqTwKi

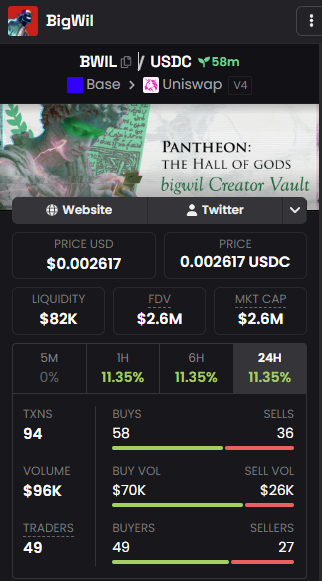

Okay... My creator index on @pantheonvaults on @base is officially live for public trading!

$BWIL ca: 0xd830cAb9F54618a111aa1197d480885e8AA9f289

Enjoy!

Some interesting signals from Snap’s latest earnings:

• Spotlight posters up 74% YoY in the US

• ~$600M annualised content & creator partner spend

• growing investment into creator monetisation

BUT!!! Discover businesses are not set up currently to capitalise on this.

I wrote a few thoughts on the monetisation economics, the current publisher transition risk, and the $600M creator land grab happening right now inside Snap’s ecosystem.

https://t.co/COgw4g3nev

This was not a content or editorial story. Not an agency story either. It was a commercial innovation story.

It showed how much leverage there was in understanding infra shifts earlier than the rest of the market.

BuzzFeed’s sale made me think back to 2019.

I was part of a small team tasked to build up a FB distribution business built around UGC licensing + aggressive global distribution which at its peak generated around $19M in ad revenue.

https://t.co/xQig5z8u1Y

In-house team? 3 people.

What's interesting is that it didn't really start as a content idea. It started more as a commercial partnership model with emerging content creators.

Having worked on Discover Shows for years, including helping to launch amongst some of the first ones outside of the US, one thing that stands out to me from Snap’s latest earnings is how much the company is investing into its content / publishing ecosystem, despite years of industry conversation suggesting Snapchat Discover is fading away.

Size of market seem to be $135M / quarter (“content & developer partner costs”) = around $600M per year

Feels like the publishing side of Snapchat is materially larger than most people think.

Today, we announced our Q1 2026 earnings results, where we shared that Snap’s global community has grown to 956 million monthly active users, and revenue reached $1.53 billion.

Full report: https://t.co/nDlIAzA3uH

Most brands can't afford a shortform video team.

So we built one that runs on a single prompt.

Script. Voice. Visuals. Edit. Done in minutes.

This video? Made with VidGuy. Start to finish.

This is what live selling actually looks like in 2026. Just stepped into one of the biggest TikTok Shop operations in Asia and out of nowhere, got pulled into a livestream.

What stood out was the scale behind it rather than the content.

🌪 700 people running live commerce like a sales machine

🌪 Playbooks imported straight from China

🌪 Europe still massively under-monetised, particularly for FMCG brands

🌪 Everything optimised for and driven by GMV and ROAS

Most brands still think this is social. It’s not. It's brutal operational discipline, logistics, dozens of parallel streams and high volume of coordinated content output - 24/7.

Virtuals ACP is facilitating more agent commerce through x402 than any other endpoint today. Build on ACP and operate where agent commerce is happening.

Crazy to see.

- BuzzFeed as a digital newsroom was built to optimise for platform engagement rather than traditional editorial standards. but it still had the cost structure of a newsroom + very headcount heavy. paying salaries in LA/NY/London.

- seems like content production is becoming even cheaper and faster, especially with AI.

- which weirdly makes me more interested in a lab model. small teams constantly testing formats, narratives and characters directly in feeds on platforms. in 2026 you'll barely need any budget to set this up in a scrappy way.

- the role of the company / creator / 'micro-studio' becomes discovering signals early, scaling what works, and turning it into social first IP rather than running a large publishing operation manually. from creative-first to demand-first.

https://t.co/suzQ8xfJqE

Your brand is invisible to the fastest-growing economy in the world.

AI agents now have wallets. They negotiate. They transact.

But if your brand is built for human eyes only, it doesn’t exist to them.

We just published a whitepaper on fixing that. 🧵👇

Meta just paid for a social network where humans can't even post.

194k agents. 2M conversations. 13M decisions being made.

Your brand isn't in any of them.

Mythos changes that.

Launching Thursday on @virtuals_io#Mythos#Moltbook#AgentEconomy#Meta#A2A