Conviction pays:

$WBT paying

$AYA now approaching 10x from start

1 more Peasant level conviction

Other high conviction building

Many small ideas in the work

That’s why doing the work matters.

As a long term investor

You don’t need 20-30 stocks

You need 4 or 5 high conviction picks that you can get in with size,

knowing they’ll pay.

That’s what my work is all about.

Converting dozens of ideas out there into a handful of gems that I can really believe in and get behind.

I’m working on many ideas now but only 1% of what I look at becomes a high conviction pick.

$CSL has bounced 23% in 11 trading days since hitting an intraday low at $90. Now starting to fill that $10 gap into $120. Thats my useless tid bit for today😆

$MFG been building a stage 1 base here for the past 4yrs. I've traded the range a few times over that period but I'm thinking I should start holding onto a core position now in light of the recent changes with the Barrenjoey acquisition. The stock is inexpensive here and pays a decent yield so i don't think it will take much good news to kick this thing out of that base. One to keep an eye on...

The Tale of Two SaaSApocalypse : Xero & Promedicus

https://t.co/C43lIJgPKo

The chair of Xero David Thodey

is sounding out institutional investors to rebase the options for CEO Sukhinder Singh Cassidy, who is among the highest remunerated CEOs on the ASX. Xero has lost 60% of its value in recent times.

So... Apparently good governance means....

If the company performs the CEO gets a windfall from free options.

If the company does not perform the CEO gets a windfall by rebasing free options so they become in the money.

You win, she wins

You lose, she wins

Apparently the goal remains...

"Singh Cassidy’s options were intended to give her a stake in the company equivalent to 1 per cent of Xero’s market capitalisation"

Keeping in mind this is a company that even now is worth $13.6 BILLION. I wouldn't mind that deal, I'm sure I could have overseen the value of the company drop 60%.

I have another suggestion for institutional investors.

Kick her out.

She has not performed, the remuneration was excessive, rebasing it is not going to improve your share price but merely delivers a windfall should it return to the mean.

The reality is this company is genuinely in trouble with AI because there is no barrier to entry. It's terrible software to use and I do use it. Most of us would jump at another option especially without the $70 per month rent seeking fees.

Compare that with another favourite ProMedicus. This company I think is immune to AI, and if anything will benefit from AI which it is integrating into its tools. It is led in a quiet way by founders that know their business and are not asking anybody to rebase their options. It has an extensive moat built on 100% contract renewal, significant regulatory barriers for new entrants, and a market penetration of only a couple of percent so there is still a blue sky.

I thought it was total shenanigans when that Xero pay packet was originally proposed and this is one reason why I will not have my money managed by institutions because if they were doing the right thing they would send her packing.

All of this is reflected in the price.

What to do with the new tax settings.

I've been trying to figure out what you should do as an investor with the new tax settings. I'm going to consider a falling hierarchy of scenarios. This is not advice this is discussion, some of it may be wrong, but together we will form a plan....

1. The family home - unlike a number of countries Australia does not tax capital gain on your principal place of residence. You do not get land tax on your home. You do pay council fees. You do not get deductibility of your mortgage interest but that no longer matters as neither does it happen with investment properties unless they are newly built. Overall the compounding benefit mandates that you should find the largest and most valuable home available to you. It is the only remaining untouched investment class. As a passing note I've always found it ridiculous that our tax system discriminates if you are married, two single people can have two CGT free assets, whereas as soon as you get married your opportunities halve. It's discriminatory against your choice to choose love over money. The only sensible thing to do really is to tie that one CGT free asset per individual. However this gets no airtime at all. But moving on, the best thing is to invest in your home, a very very very very big home. This is not a new idea and many of us realised this many years ago.

2. Superannuation - I would say the next most valuable asset is your superannuation which is favourably taxed. You still get the 50% discount on CGT, which is already favourably taxed which would bring it down to 10% on capital gains anyway. There are two problems, the first is that you cannot access it until you are old, with a few rare exceptions such as misadventure. The second is that the government has attempted to pillage superannuation recently with taxing unrealised gains and has been successful in chipping away at the benefits, as their target audience is middle income. If you are higher than the median income earner you are probably going to hit the $3 million threshold. Incidentally based on historical returns I would suggest an SMSF should hold one asset which is the S&P 500 which has historically outperformed almost every other index. This is what I do. I caution that it does look very expensive at the moment but you can't choose your timing. You can also do an industry fund with the ability to select ETFs which may be more cost-effective. Because of balancing stock within the fund, and the automatic balancing that occurs with ETFs weighted on market capitalisation, you don't have the same extreme taxation of portfolios as would occur for a diversified portfolio in a private name. Even with these advantages superannuation is not as advantageous as your primary residence. However one hidden benefit is that nobody can take it away, if you get sued or bankrupted or have some other misadventure, you're superannuation is safe. Untouchable. Something to keep in mind.

3. Stocks or ETFs? We now get to the tricky area of investments. I think having a portfolio of shares is now dead in a personal name not only because of mandatory loss ordering but the fact that the skew of the returns in a portfolio may expose you to tax of 70%+ in real terms. The only sensible approach now is to have an ETF where all of this is done at the ETF level and not exposed to pernicious taxation. I'm doing some modelling to try and establish which ETF, whether high dividend paying or still high growth, with others saying go for high dividend growth but I am not so sure. More on that soon.

4. Companies- The company shield for any stock is now mandatory, as it will eliminate your 47% tax drag as a high income earner, and you will be restricted to 25% as long as you can argue that you are below 50 million and that you are not just passive income, you will have to figure out how to do that. Even in the worst case it's 30%. It effectively halves your tax burden which allows you to compound the difference between the top tax level and the company rate. The ATO has certain requirements for doing this and that's one for the accountant. Keep in mind that is the tax drag of getting money cut out each year or it's 3 months by the government that kills long-term returns and anything you can do to avoid that will increase the amount that you have in your pocket at the end. You still get screwed by the government taking 47% of your equity at the end while contributing nothing.

5. Fixed term deposits- this is insane in a high-tax, high inflation environment with the exception of those that need money and accept that the real value of that money will deteriorate with time. I used to have a significant fixed term deposit which was taxed as a BAS every 3 months which interferes with compounding, and the real return was negative. I don't have that anymore. The banks also screw you and give you headline rates which are not retained. You can buy bonds or listed entities that do high yield bonds, but in an high inflationary environment the realisable value wil go down. Most think inflation will grow and interest rates will rise. Avoid unless you have to....

6. Trusts - I'm finding it very difficult to imagine any scenario where trusts now have a purpose. I think that was by intention by the government to remove trusts and the various advantages that go with them. That's unfortunate to the million plus people who have family trusts. It's a disaster for those currently on testamentary trusts for the disabled. The killer on trusts is the mandatory 30% taxation. This is still better than 47% but less than the 25% on offer with a company structure. I recognise that with a company you still need to distribute to shareholders at some point but the assumption here is that it is held for some time so a smaller tax drag will advantage capital gain.

7. Charitable donations - we live in a more hostile world and you do not get the tax benefit that you used to given the 30% mandatory tax on capital gains through a trust or directly. It used to be you could donate half that capital gain pay no tax and the charity would get the full benefit. Any charitable donation you make needs to be reduced by 60% if you use this method.

8. Investment properties - I think this is the dead end these days. The current yield is less than you would get on risk-free returns. Legislation places all the benefits for the tenant, Eg in NSW you can't raise your rent more than once every 12 months. You have a land tax burden. Your interest payments are only deductible against rent and you cannot negatively gear. There is unlikely to be capital appreciation in the next few years in fact it's likely to be depreciation. People will say you can buy a new property and obtain these benefits, well, I've got the capacity to build 70 of these new properties and it's not sensible either to build or to own. The build doesn't give a yield, to own you lose on rapid depreciation relative to any benefit from the tax incentives. The only advantage in this investment class is if you build, not if you own, not if you develop, because you can still get a good return while others make a loss. It's a dead investment class which was the whole purpose of the legislation.

9. Tax residency - you only pay tax as a tax resident. When you eventually realise all of this money on a one hit it might be a good time to go live overseas for a year or two so you are no longer an Australian tax resident. That won't allow you to avoid the tax drag each year but it will allow you to not be taxed to the full extent on the eventual realisation. I suggest Singapore, Hong Kong, or Dubai. This does get a little complex with your home but you can retain it as a CGT-free asset for up to 6 years under certain circumstances, or indefinitely if it's not producing income, but it's hard to argue that you are a foreign tax resident If you retain a home. That's one I have yet to unwind properly. The alternative is that you just sell your home prior to leaving as a CGT free asset and simply leave and live your life away from Labor's socialist society. After all we are all heading the way of Victoria and I don't think any of us want to live in Machete Land.

These are just ideas for a discussion and I would welcome people to engage on them because ultimately we need to know what to do with the rules that we have to best advantage ourselves.

At least until we can vote these cretins out.

Robert De Niro on Donald Trump: “He’s a punk. He’s a dog. He’s a pig. He’s a con. A bullshit artist. A mutt who doesn’t know what he’s talking about. Doesn’t do his homework. Doesn’t care. Doesn’t pay his taxes. He’s an idiot. He’s a national disaster. He’s an embarrassment to this country.”

This is so incredibly good:

Economist Joseph Schumpeter warned that capitalism weakens when prosperous societies become so comfortable they forget where prosperity came from – and begin resenting the entrepreneurial class that created it.

A country might survive high taxes for periods of time. What becomes dangerous is something deeper: the moral suspicion of ambition itself. The creeping belief that commercial success is inherently exploitative, that profit is morally dubious, or that founders should quietly accept punishment for surviving years of uncertainty.

Prime Minister Anthony Albanese and Treasurer Jim Chalmers should think carefully about the signals embedded in this budget. Tax policy communicates values. This budget signals that founders are not viewed as partners in national prosperity, but simply reservoirs of revenue whose success is viewed with suspicion...

Civilisation advances because some people are willing to bet on tomorrow before tomorrow exists. Australia should be doing everything possible to encourage those people to build businesses here. Because once a society begins treating ambition as something suspect rather than admirable, it eventually discovers that no nation can remain prosperous after teaching its most ambitious people that they are unwelcome.

https://t.co/nxmwyx9aZc

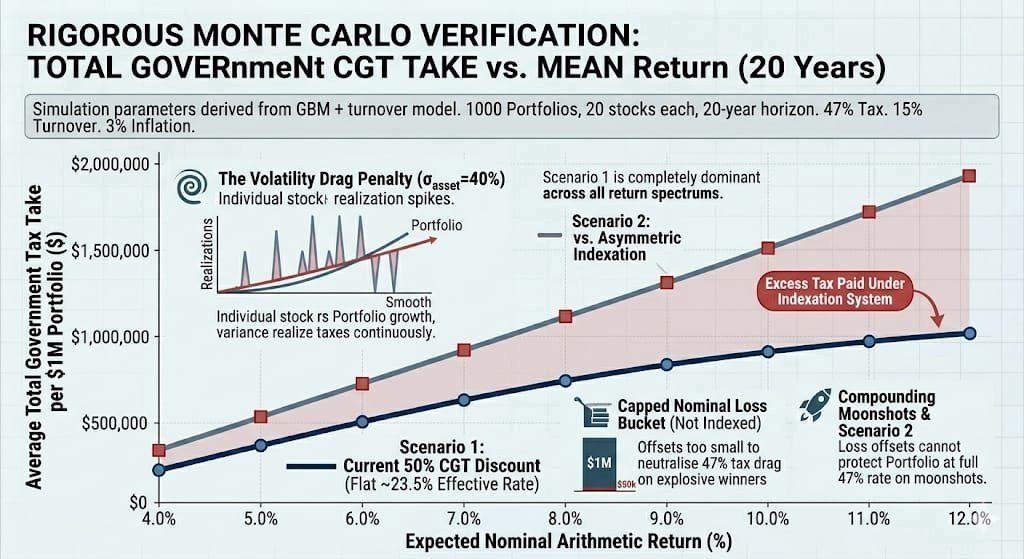

Small Cap Investing is Dead with a 77% spike in Tax Collection

I have run 1,000 Monte Carlo simulations of portfolios of 20 Small Cap Stocks with the New Inflation Corrected CGT model versus the existing 50% CGT discount model.

The results are devastating.

The bottom line is that small caps are highly asymmetric bets where your small number of winners are meant to compensate you for your many losers. Mining companies are a good example of this situation and are a fundamental pillar of our national wealth. However if you tax those few winners at 47% with the trivial relative inflation correction you effectively wipe out the ability to offset your losses. This is because the tax drag on your few multi baggers is so high that it changes the entire logic of the investment process.

It's become a loser's game.

1. The Moonshot Tax Penalty:

Because Australian small caps rely heavily on a right-skewed distribution (a few massive winners offsetting many losers), the Indexation framework introduces a devastating tax penalty. For a stock that goes from $50,000 to $400,000, a 3% inflation adjustment on the original $50,000 cost basis is completely negligible. Under Indexation, you forfeit the 50% discount and pay a flat 47% on nearly the entire gain.

2. The Turnover Trap:

With a 15% annual turnover, small-cap portfolios realize taxes continuously. Under the current system, every partial sale triggers a flat 23.5% effective tax rate, leaving more money inside the portfolio to compound. Under indexation, those early wins are hit at a full 47% clip, severely dampening the portfolio's forward compounding engine.

3. The Asymmetric Loss Failure: in small-cap investing, a stock can only ever lose 100% of its value, but explosive winners have unlimited compounding upside. The government’s asymmetric tax system completely devastates this dynamic: by replacing the flat 50% CGT discount with inflation-indexing for winners only, it leaves your nominal losses capped and completely unable to counteract the massive tax hike on your multi-baggers. Because a 3% inflation buffer barely dents a 400% moonshot gain, you end up paying a brutal, un-discounted 47% tax rate on the very winners that drive a small-cap portfolio's success, causing a 77% spike in total government tax take overall.

Even in investing we see the socialist government wants us all to be the same. Communists.

(Technical notes: Model executed using Gemini Pro with 1,000 portfolios of 20 stocks each with the volatility and median return typical of this class of small cap stocks over the last 10 years, using a geometric mean process to step forward each portfolio each year).

There are two other dire consequences of this budget that nobody is talking about. The first is that the budget’s introduction of an effective capital gains tax of up to 45 per cent - 47 per cent – previously capped at 23.5 per cent for assets held more than 12 months – hits younger savers hardest, precisely because they have the highest portfolio exposures to high-growth assets such as listed global equities, Australian shares, crypto, venture capital and private equity.

When anyone builds a portfolio for younger investors, they rationally load them up with the highest-growth and most volatile assets on the basis that a long investment horizon allows them to weather the inevitable volatility storms.

As investors age, these portfolios shift into more stable and income-rich asset classes such as cash and bonds, which are net beneficiaries of the CGT increase, because their post-tax returns now look more attractive relative to growth assets.

As many investors have noted online, why would you allocate to a bunch of high-risk growth companies when Albanese and Chalmers are going to take almost half the upside while wearing none of the downside? Rather than helping younger generations, the highest CGT rate in the developed world will hammer them.

And it is a double whammy because the many early-stage companies that have historically employed 20- and 30-somethings will now consider moving overseas. Their investors will simply not want to trade away half of their upside to the public oligarchs.

If you allocated $10,000 to bitcoin after the March 2020 pandemic shock – which many young punters did, and which would now be worth approximately $92,000 – the new CGT regime imposes vastly higher amounts of tax.

A self-funded retiree on the tax-free threshold would go from paying nothing to almost $24,000. Somebody earning between $18,000 and $45,000 a year would see their tax bill jump from $7400 to $23,900 – a 222 per cent increase. Those in the $45,000 to $190,000-plus tax brackets would have their bill rise by 93 per cent.

Since the new CGT regime is, by definition, much more costly on higher-growth investments, it will punish younger investors who have much greater risk appetites and lower average incomes.

https://t.co/MJKvQZXvKw

$MLG.AX

I’ve re-entered in the low 80 cents

Sold off heavily in recent weeks, presumably relating to diesel shortage fears

NTA is over $1 and not expensive as a multiple of earnings either

$PWR.AX

Peter Warren Automotive

Share price today: $1.17

Market cap: $207m

Land and building value at 31/12: $230m

Net debt at 31/12: only $61.5m

The business is long term profit making ($8m in half year profit for 1H26) and pays divs too

This will get back to $2 + in my view

Far cheaper than larger listed peer $APE.AX Eagers Automotive

I hold

$AYA.AX — Applying Verbalized Sampling to Scenario Forecasting in Valuation

A recent paper on Verbalized Sampling (Zhang et al, 2025) shows that Large Language Model (LLM) outputs collapse toward a small set of "typical" answers after Reinforcement Learning from Human Feedback (RLHF) training - a phenomenon called mode collapse.

The paper shows this can be avoided by asking the model for a distribution of possible answers with probabilities, rather than a single best answer, which can thereby recover diversity that post-training had suppressed.

We are all familiar with a simplified version of this result, viz if you ask a Large Language Model "is X true?" it will often agree with you even when you're wrong. Asking instead for a probability-weighted set of outcomes forces it to articulate alternatives it would otherwise suppress. It's considerably more impartial and therefore more useful.

I applied this to $AYA.AX by feeding Claude Opus 4.7 a knowledge base of every announcement back to 2023 and asking it to construct a probability tree of future outcomes - It identified eight distinct pathways, each with a probability and a price target. The probability-weighted average came out at AUD$4.71 versus a current price around AUD$4.07.

The conclusion is either that 1) markets are weakly efficient, which we know; or 2) the Large Language Model may have unconsciously anchored on the current price when assigning probabilities, which is a real risk with this method.

The more interesting output is the shape of the distribution. It's right-skewed - the upside tail extends to AUD$15, while the downside floors near the raise anchor at AUD$2 for most scenarios. That's the geometry of every early-stage growth story, and it's exactly why venture capital works as a portfolio strategy but is dangerous as a single-stock bet.

This isn't a position to size for conviction; it's a position to size for variance.