Rocket Lab Robotics is coming 🤖

Our acquisition strategy is proven and effective: identify the best space technologies that have struggled to scale, and bring them into the Rocket Lab ecosystem.

That’s what we’re doing with Motiv Space Systems, adding Mars-proven robotics heritage to our rapidly expanding capabilities. As leaders in motion control systems and precision mechanisms, Motiv will also bring in-house traditionally costly and supply-constrained spacecraft components including solar array drive assemblies, antenna and propulsion gimbals, filter wheels, focus mechanisms, and precision drive electronics.

For the 85th time, Electron is vertical on the pad and ready for launch - but this time with its first dedicated mission for the European Space Agency @esa.

T-4 hours to liftoff for 'Daughter Of The Stars'.

Everyone is talking @SpaceX IPO. But, what if there’s a better way… 💡

@TeslaLarry has an alternative theory that would allow Tesla, SpaceX and all of the other Musk Companies to raise $1T+ in new funding

A stock swap 🪄

And now is the perfect time. Tesla could dilute about ~33% of its shares to acquire large stakes in all of the Elon companies (while keeping Elon’s ownership above 50%).

The new company would have a ~$1.8T market cap, but control 1/3 of SpaceX, Neuralink, Boring and XAI (rough estimates)

I love the big vision of this proposal. Even though it’s unlikely and SpaceX will probably IPO the traditional way, there’s something about the stock swap that I can’t stop thinking about

It gives Elon the strongest ‘bank’ to raise capital. If he’s serious about Optimus, Orbital Datacenters and a Chip Fab he may need $1T+ in fresh funding.

@Tesla could then become the ATM to fund all these ambitious projects 💵

This would give America a technology powerhouse to make $100B+ decisions without approval … the same speed at which China moves. Making us have a chance to compete on the global scale for AI and Robotics …

Loved this conversation and so curious what your thoughts are :) Thanks Larry for scheming with me!! ⚡️ $TSLA

timestamps:

0:00 Why Consolidate The Musk Empire? Elon Needs

$1T+

6:28 Why Did Elon Decide To IPO SpaceX Now?

10:02 Would Elon Like This Tesla Share Swap Idea?

12:05 The Bank of Tesla

13:17 Elon’s Control of The Muskonomy

17:19 Muskonomy Post-Elon Musk

22:38 How The Ford Family Handled Succession

23:39 Will The Public Revolt Against Elon Musk’s Wealth

34:13 Tesla Stock Swap Accelerates The Musk Economy

39:37 Would Be A HUGE Win For Tesla

41:57 Eventually Tesla Acquires All Musk Companies

42:31 Larry’s Elon Musk + Apple Theory

45:14 Muskonomy’s Strategic Importance To America

Interesting contrarian take by @chamath for 2026:

"I don’t think @SpaceX will IPO, I think it will reverse merge into Tesla and I think Elon will use it as a moment to consolidate control and power of his two seminal assets into one cap table.”

I don’t see that happening.

BREAKING: 🚨Oklo $OKLO and Meta Platforms $META announced a partnership to develop a 1.2GW nuclear-powered energy campus in Ohio to support Meta’s regional data centers. The agreement allows Meta to prepay for power, helping fund Oklo’s Aurora powerhouse deployment, with phased development starting in 2026 and initial capacity targeted as early as 2030.

The "InP Chokepoint": The Bottleneck of the AI Buildout explanation:

The future of $NVDA Blackwell, $META MTAI, $GOOGL TPU, and $MSFT Maia ramp is tied to:

A $700M small cap $AXTI and $SMTOY.

The AI "Growth" story ends in 2026 if there's no solution to InP.

Here's why:

The AI industry started its migrating to photonics for future ASIC/GPU deployments, because copper is hitting a physical limit.

However, in doing so, hyperscalers traded the common material for InP (Indium Phosphide), when there's only a few factories capable of producing 6-inch InP wafers at the purity levels required for lasers.

Let's take for example Google and their TPU v7 Ironwood program:

Google uses Optical Circuit Switching (OCS), in simpler terms, switchboards made of light. For every one of those TPUs in the pod to talk, they require InP-based lasers. $LITE, which works with Google on this, largely depends on InP substrate (eg. AXT/Sumitomo) to make them.

If they don't have it Google's entire Ironwood program doesn't just "slow down", it hits the wall.

Modern ASICs/GPUs from $NVDA GB series, $AMZN Trainium, $MSFT Maia, $META MTAI have all made the same bet: Light is the way forward.

Now, here's the issue.

The entire Western AI roadmap is currently tethered to a $700M small-cap and a single Japanese company that produce majority of the world's InP substrates required for photonics.

It's currently a duopoly (rough estimates majority supply ~60% between AXT + Sumitomo), with recent estimates of ~70%+ coming from Sumitomo Electric, AXT, Freiberger, JX, and Visual Photonics Epitaxy (filling in the gaps).

Regardless, the entire future AI supply chain is thinner than a needle:

- Moomoo Research: InP market is in a state of "global scramble" and "serious supply shortage" NVIDIA GB200 rollout (scale-out still requires tons of InP, not NVL72 within-the-rack comm).

- Demand for high-speed transceivers today probably exceeds the supply by almost a factor of two (LightCounting)

- Seeing record booking, but explicitly "supply-constrained by InP lasers" ( $COHR CEO Q3 ER)

- McKinsey: 40% to 60% shortfall for 800G modules and a 30% to 40% shortfall for 1.6T modules.

And these reports are likely understanding + very conserative given the demand ramp. Even going off Microsoft's projections on Maia ramp, ( est. 1M+ Maia by 2027 on UBS $MRVL note), with 2 million+ units of 1.6T transceivers over the next year, this volume is so large it represents a double-digit percentage of global substrate output.

The projected "exponential growth" of AI is about to collide with the reality of critical material production. So, the "Ironwood", "MTIA" and "Maia" ramps aren't just ambitious, they may be impossible under current material constraints.

Even if $COHR, JX Nippon, Sumitomo, $AXTI, and others, ramp up at maximum capacity (eg. $COHR / JX -> 6-inch InP wafers for 4x capacity), they still might not be able to meet the increasing demand from hyperscalers. Especailly with demand spikes occurring, eg. just for $NVDA alone (GB200/GB300 revisions).

There are technical solutions like silicon photonics is one solution to bridge the gap, but this still largely requires an external InP laser as the light source. TFLN or quantum dot lasers are many many years away.

There's probably no escaping the InP requirements for the next few years.

So, the mismatch between chip design and material availability has created a strategic chokepoint, where if you go to the very bottom of the supply chain, very few companies control a majority of allocations, pricing, and supply. This is especially dangerous when compounded with geopolitical risks on US/China relations + export controls.

That being said, here's what's probably what's going to happen:

- Price Spikes: Prices from $AXTI, JX, Sumitomo will spike significantly -> $LITE, $COHR, Innolight (also increases prices from pass down)

- Hyperscalers will directly stockpile materials, bypassing traditional component procurement and buying InP substrate inventory from $AXTI, JX Nippon, Sumitomo, and directly to consign to transceiver manufacturers like $LITE.

(eg. Meta would bypass transceiver companies and go directly to AXT or Sumitomo)

- Hyperscalers will buy out production allocation ( like $NVDA that has already aggressively "locked in" EML capacity (manufactured on InP substrates).

Buying a substrate manufacturer or production allocation would become a necessity to so others like $NVDA or $GOOGL doesn't starve them out.

As TPU v7 and and as other hyperscalers ramp up in 2026-2027, we will likely enter a "hunger games" phase for substrates where only each hyperscaler will be cannibalizing each other's growth for resource allocation.

Companies like $NVDA (with record amounts of pre-allocation), might ramp be okay for the time being, but others programs would likely face major delays.

Thoughts:

1. Some hyperscalers might be fine ( $NVDA). Others like $GOOGL and $MSFT will need to buy out materials + allocation before others do.

2. Industry needs to double down on engineering shifts like copper life extension and more material efficient ways like SiPh.

3. Move to 6-inch wafers for yields (eases things, but still not enough to meet demand)

So the way things are now, the multi-trillion dollar AI scaling are tethered to some obscure $700m company $AXTI and $SMTOY. It seems inevitable that AI will hit the physical ceiling because of InP substrate capacity unless architectures change.

In 2024, the bottleneck was GPUs. In 2025, it was HBM. In 2026, the primary constraint will likely be the optical interconnect, and specifically, the InP substrates that power them.

This has now become the hidden bottleneck of the AI buildout.

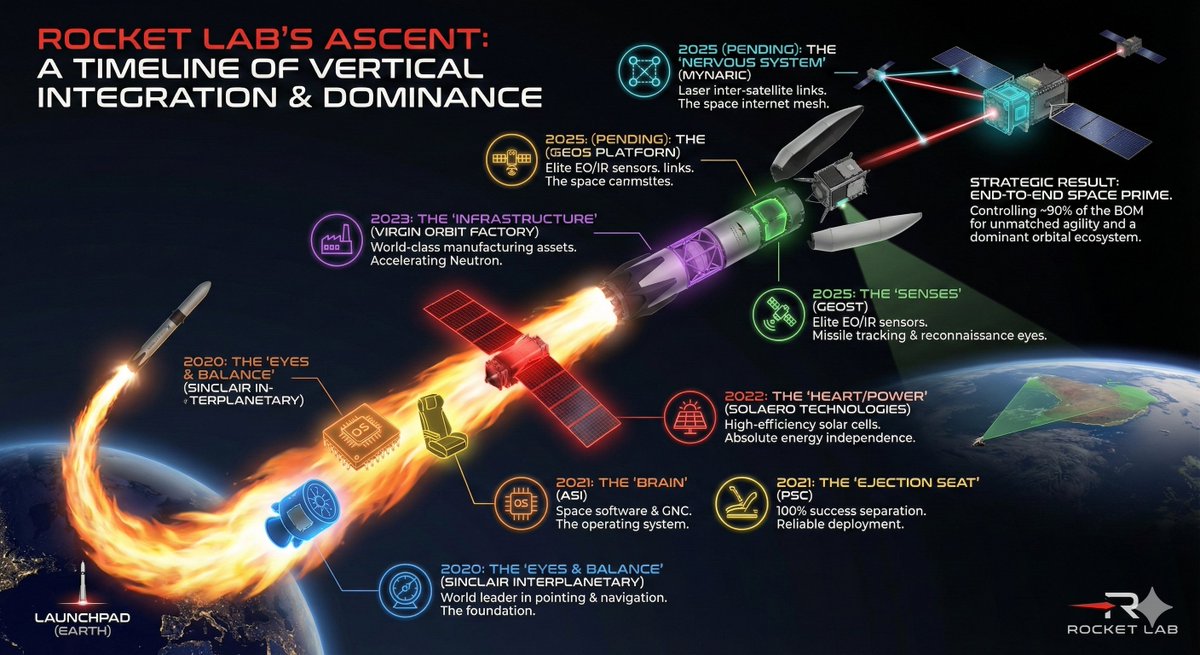

$RKLB Rocket Lab’s 7 Acquisitions: Building the "Amazon of Space" ♟️🚀

I’ve spent the last few days dissecting the history of Rocket Lab ($RKLB), and the realization is staggering. Peter Beck isn’t just building rockets; he is following the Jeff Bezos Playbook: use strategic acquisitions to own the entire infrastructure of an industry.

Just as Amazon acquired Kiva Systems for robotics and Whole Foods for physical reach, Rocket Lab has executed 7 strategic moves to control the Bill of Materials (BOM) for the entire space economy.

🧐 The 7 Pieces of the Empire: A Portfolio of Dominance

The "Eyes & Balance" (2020) - Sinclair Interplanetary:

Acquired the world leader in reaction wheels and star trackers. Every satellite needs these to point and navigate.

The "Brain" (2021) - Advanced Solutions, Inc. (ASI):

Acquired the masters of off-the-shelf space software and GNC (Guidance, Navigation, and Control). They provided the "Operating System" for the Photon platform.

The "Ejection Seat" (2021) - Planetary Systems Corp (PSC):

Acquired the gold standard in satellite separation systems. They have a 100% success record across 100+ missions.

The "Heart/Power" (2022) - SolAero Technologies:

The biggest move yet. Acquired one of the world's leading producers of high-efficiency space solar cells. Absolute energy independence for every RKLB mission.

The "Infrastructure" (2023) - Virgin Orbit Factory:

Not a company acquisition, but a genius asset buyout. Beck secured 144,000 sq ft of world-class manufacturing space and machinery for pennies on the dollar to accelerate the Neutron rocket.

The "Senses" (2025) - Geost:

A massive $275M deal for elite EO/IR (Electro-Optical/Infrared) sensor capabilities. RKLB can now build the "cameras" for missile tracking and reconnaissance.

The "Nervous System" (2025 - Pending Approval) - Mynaric:

The final piece of the puzzle. Laser communication terminals for inter-satellite links. Note: Currently clearing German regulatory hurdles (BMWK). Once complete, RKLB owns the space-based internet mesh.

The Strategic Result: The End-to-End PowerhouseRocket Lab now controls ~90% of its own supply chain. While competitors wait 18 months for parts, Peter Beck simply walks downstairs to his own factories.

With BlueBird 6 successfully in orbit for ASTS today (featuring that game-changing ASIC chip), we are seeing the dawn of new technology. But for Rocket Lab, the "Amazon Era" of space—where one company owns the truck, the cargo, and the delivery route—is already here.

If you resonate with the long-term value of this "one-stop" vertical integration strategy, please Like and Retweet😊😊.Thanks for your support! 🙏

#RKLB #RocketLab #PeterBeck #AmazonOfSpace #VerticalIntegration #SpaceEconomy #Investing #Neutron #Photon #Geost #Mynaric

$RKLB The 2026 Master Manifest

RKLB 2026 Mission Roadmap: The Industrialization of Space is Here 🚀🛰️

I’ve conducted a "nuclear-level" check on the Rocket Lab ($RKLB) 2026 manifest. If 2025 was about setting records, 2026 is about scaling a monopoly. We are looking at a calendar packed with interplanetary science, national security, and the most anticipated rocket debut of the decade.

Here is the definitive mission-by-mission breakdown for 2026:

1. Jan 2026: NeonSat-1A (Bridging the Swarm) 🇰🇷

Status: Confirmed delay from late 2025 to Jan 2026.

Details: Launching from LC-1 in New Zealand, this is the first verification satellite for South Korea’s mass-market micro-satellite constellation. It sets the high-frequency tone for the year.

2. Q1 2026: Neutron Maiden Flight (The Big One) 🏗️

Status: Confirmed for Q1 2026.

Details: The hardware is targeted to ship to Virginia’s LC-3 in Q1 for its first flight. This medium-lift beast is designed to challenge the Falcon 9 and unlock massive government (NSSL) and commercial contracts.

3. March 2026: The "Triple Threat" Month 🧪🛰️

NASA Aspera: A Pioneer program mission using Electron to study the formation and evolution of galaxies by observing the intergalactic medium.

ESA LEO-PNT Pathfinder A: A mission for the European Space Agency to deploy two verification satellites for a future low-orbit navigation constellation.

LOXSAT 1: Part of NASA’s "Tipping Point" program, this mission uses a Photon spacecraft to verify cryogenic fluid (oxygen) management in orbit.

Synspective (StriX Launch 8): Continuing the 21-launch agreement with Japan’s SAR constellation leader.

JAXA Innovation: The "Kakushin Rising" mission for Japan's space agency, demonstrating new satellite technologies.

4. June 1, 2026: The Venus Probe 🌌

Status: Targeted for the June 1 launch window.

Details: The world’s first-ever privately funded interplanetary mission. An Electron will send a probe to search for signs of life (phosphine) in the clouds of Venus.

5. Q2/Q3 2026: Victus Haze (Tactically Responsive Space) 🛡️

Status: Confirmed for mid-2026.

Details: A mission for the U.S. Space Force demonstrating the ability to launch on just 24-hours' notice. It showcases RKLB’s unique ability to support urgent national security needs.

6. Sept 2026: SDA Tranche 2 Beta 📡

Status: Deployment begins in Sept 2026.

Details: A massive leap in business scale. RKLB is not just the launcher but is building and operating 18 satellites for the Space Development Agency’s secure communication layer.

7. Dec 2026 & Ongoing: The Constellation Machines ⚙️

Synspective (Launch 12): Wrapping up another high-volume year for the StriX constellation.

iQPS: At least 5 dedicated missions throughout 2026 to continue building their SAR network.

HASTE (MACH-TB 2.0): Continued suborbital/hypersonic testing missions for the DoD.

TBy the end of 2026, RKLB will have transitioned from "Rocket Company" to "Space Utility." The diversification into satellite manufacturing (SDA, Globalstar, Varda) and deep-space science (Venus) creates a moat that is nearly impossible for competitors to cross.

welcome to add or point the mistakes😊

#RKLB #RocketLab #SpaceEconomy #Investing #FinTwit #Neutron #Electron #NASA #ESA #BlueBird #NewSpace #SpaceX #Starlink #TechAnalysis

NEWS: Today, Trump signed an executive order committing the United States to return to the Moon by 2028, build a lunar outpost by 2030 and prepare for the journey to Mars.

Everything in the Executive Order:

• Return Americans to the Moon by 2028

• Begin building a permanent lunar outpost by 2030

• Make U.S. space superiority a core national priority

• Expand commercial launch, lower costs, increase cadence

• Develop next-gen space-based missile defense by 2028

• Detect and counter threats in LEO and cislunar space

• Rapidly modernize national security space architecture

• Deepen allied cooperation in space security

• Grow the U.S. commercial space economy

• Target $50B+ in new space investment by 2028

• Support a commercial successor to the ISS by 2030

• Enable space nuclear power for lunar and orbital missions

• Improve space weather forecasting

• Lead on space traffic management & debris mitigation