AppLovin $APP isn’t a household name, but it quietly powers a large share of mobile apps by helping developers market their apps and match them with advertisers.

What makes this sell-off so jarring is that the company’s results are blowing away expectations.

On Thursday, the company reported strong fourth-quarter results. Yet the stock plunged nearly 20% and is down roughly 44% over the past month.

More on this in my latest free newsletter ⤵️

https://t.co/jXigeig96s

Many believe bond yields are rising only because investors are freaking out over inflation. But that’s not the whole story.

There are two types of yields: nominal yields (the ones you see in headlines) and real yields (which are the "headline" yields minus inflation expectations).

You can calculate them for yourself. Take a 10-year government bond yielding, say, 4.6%, and subtract the average inflation rate investors expect over that period (aka breakeven inflation rate)

What’s left is the real yield. And what it effectively tells us is how much investors want to be paid for lending money after inflation.

So if Hormuz-driven inflation were the only concern, real yields should more or less stay put. But that’s not what is happening.

Since the first missiles landed on Iran, the U.S. 10-year yield is up about half a percentage point. And most of that move came from higher real yields. (h/t Padhraic Garvey (@MarketsGarvey) of ING)

Perhaps even more interesting, that’s not really the case almost anywhere else in the world.

Here’s a breakdown of how much of the yield increase is coming from inflation expectations vs. the real cost of borrowing. (h/t @Bloomberg).

- 🇺🇸 U.S.: Mostly the real cost of borrowing. Real yields are up 46.8 bps vs. 15.3 bps from inflation expectations, meaning investors want more compensation to hold U.S. debt

- 🇬�� U.K.: A bit of both. 38.0 bps comes from inflation expectations and 28.4 bps from the real cost of borrowing

- 🇯🇵 Japan: Almost entirely inflation. 58.7 bps of the 64.3 bps move comes from inflation expectations

- 🇩🇪 Germany: Mostly inflation. 35.6 bps comes from inflation expectations vs. just 3.9 bps from the real cost of borrowing

- 🇫🇷 France: More like the U.S., but not to the same extent. 18.5 bps comes from inflation expectations and 26.2 bps from the real cost of borrowing

- 🇦🇺 Australia: Mostly inflation. 17.2 bps comes from inflation expectations and 9.9 bps from the real cost of borrowing

That means even if Hormuz reopens today, yields may not come back to pre-war levels as quickly as many expect. And that means interest rates may stay higher for longer.

Or at least that’s the new narrative I’m seeing pop up more and more in my inbox.

Commentary by our editor @danrunk

#iran #hormuz #inflations #bonds

Workday will open 10% higher this morning, suggesting the worst of “SaaSpocalypse” may be over.

The software stock jumped in after-hours after earnings showed its AI adoption went from empty boardroom buzzwords to actual money.

On the call, CEO Aneel Bhusri said Workday had its best first quarter for annual contract value growth in five years, and that the company is getting closer to $500 million in annual recurring revenue from agentic AI.

So that’s Workday, but there’s more.

ServiceNow jumped 8% this week after Bank of America brought back its Buy rating, saying the software company is simply “too entrenched” in enterprise to be replaced by DIY agents.

Then the market is finally waking up to the fact that AI may be one of the biggest cybersecurity risks right now, with all the data these tools can access with few guardrails. CrowdStrike and Palo Alto Networks are up 13% and 5%.

But there are also cases where investors are still 50/50. One of them is Salesforce.

On one hand, Salesforce’s AI solutions like Agentforce and Data 360 ARR are growing on steroids. On the other hand, AI can gut the company’s per-seat pricing model because it's supposed to makes everyone more productive.

Investors still can’t wrap their heads around how that math will work out.

Adobe is another head-scratcher where investors are still on the fence. On one hand, the company is growing revenue and rolling out AI. On the other hand, leaner competitors like Figma and Canva are beating it on speed.

And finally, you have the poster kid of SaaSpocalypse, https://t.co/iMnnUPognP, which has lost 75% of its value since mid-last year. The company is up 10% this week.

Although the company is dying to be an AI company and is beating earnings and all, the truth is that the stock had been so crushed that it probably didn’t take much.

So every company that’s now part of this “SaaS renaissance” falls into one of these three realizations: 1) it’s too embedded in enterprise; 2) it can become an AI company or monetize AI; 3) it’s just been beaten down too much.

Quite a few bargains may be up for grabs.

Commentary by our editor @danrunk

#saasrenaissance

U.S. stocks snapped a three-day losing streak on Wednesday, with the S&P 500 climbing 0.8% as technology and consumer discretionary stocks led the advance.

Investors were encouraged by renewed hopes for a U.S.-Iran peace agreement and continued signs of strong demand for artificial intelligence infrastructure.

The S&P 500 now sits within 2% of its previous record high.

#StockMarket

NVIDIA dropped after blowout earnings but set off the biggest Asian tech rally in six weeks. And that tells us the AI trade is entering a new stage.

Nvidia had plenty of good news yesterday and addressed some of Wall Street’s biggest concerns.

The company delivered another monster quarter, beat expectations, guided for another strong quarter, talked up its customer base beyond ���just hyperscalers,” and touted its vertical integration into CPUs.

Nvidia also made it clear that it’s generating so much cash that it can keep funding the AI arms race and still send more money back to shareholders.

The company boosted its quarterly dividend from 1 cent to 25 cents and added an $80 billion buyback authorization. AND YET, the stock fell after hours.

Meanwhile in Asia, investors woke up to a very different story today.

Asian tech stocks are having their biggest rally in six weeks. LG Electronics and Hyundai Mobis both surged more than 10% in Seoul. Memory chip giants Samsung and SK Hynix also jumped 8% and 11%.

Nvidia may still be the face of the AI boom, and it’s still growing at a ridiculous pace for such a large company, and the stock is now 2x cheaper than it was just a few years ago.

But there's a creeping worry that peak GPU growth and hyperscaler spending may be behind us. That’s why investors are now flocking into companies that sit upstream, downstream, and adjacent to Nvidia.

And there may be no better market for that than Asia because it's the factory floor of AI: from chips and memory to components, robotics, and manufacturing.

For example, LG Electronics and Hyundai MOBIS soared because Jensen Huang said “physical AI” and robotics could be the next major growth story for AI.

Meanwhile, Samsung Electronics and SK hynix are the more obvious picks-and-shovels winners. Nvidia showed that AI infrastructure demand is still through the roof, and that should keep memory backlogs full for a long time.

The irony is that Nvidia’s AI gospel may now be doing more for the companies around it than for its own stock.

Commentary by our editor @danrunk

$NVDA #nvidiaearnings

Meta says it fired 8,000 employees this morning to become more “efficient” with AI. Translation: Someone has to pay for all those GPUs.

Here’s the official statement that has been circulating inside Meta:

“We’re now at the stage where many orgs can operate with a flatter structure with smaller teams of pods/cohorts that can move faster and with more ownership,” said Meta’s Head of People Janelle Gale, Ph.D..

AI can absolutely make some roles more productive and reduce corporate slack. But the bigger problem for Meta isn’t efficiency.

Meta has pledged to spend $600 billion on AI over the next few years, with $160 billion expected to be deployed this year alone. And that changes how investors think about companies like Meta.

For most of this century, Big Tech was a low-capex, high-margin sector that could grow fast, carry little debt, and still look fairly resilient during economic downturns.

AI broke that narrative. Now companies like Meta have little choice but to spend hundreds of billions just to keep up with the competition.

In other words, tech companies have gone from printing money to burning it.

And for the first time in recent memory, hyperscalers, including Amazon, Meta, and Microsoft, are expected to post negative free cash flow in at least one quarter this year.

Investors are worried that for many of them these investments may never fully pay off. So now Big Tech is scrambling to offset at least some of that spending by cutting costs elsewhere.

And what’s one of the biggest expense lines at a tech company? People.

See the chart below. It’s not just Meta. There’s a clear trend where tech companies are replacing labor costs with higher AI spending.

From 2017 to 2024, people cost roughly 2x capex. But by 2025, the lines crossed. This year, capex is expected to surpass labor costs by $50 billion. (h/t Santanu Bhattacharya)

A lot of this is being framed to investors as “AI innovation” and “efficiency gains.” But at the core of it, these companies are desperate to cut costs and keep free cash flow positive.

The problem is that it’s hard to cut jobs at the scale needed to offset hundreds of billions in AI spending.

By Evercore’s estimates, this layoff round will save Meta around $3 billion, which is a sliver of Meta’s AI investment this year alone, never mind everything it plans to spend beyond that.

So these layoffs look less like a true cost fix and more like AI signaling ahead of the next earnings report.

Commentary by our editor @danrunk

#layoffs $META

Most investors are watching the S&P 500 and oil prices, but a far more important number for your portfolio right now is the 10-year Treasury yield.

Since the beginning of the Iran war, that yield has climbed from sub-4% to 4.6%. Last week alone, it added 0.3 percentage points, getting dangerously close to the dreaded 5% mark (more on that in a moment).

So why should you care about a few basis points in bond yields, even if you’re all in on stocks?

Because the 10-year Treasury yield is the closest benchmark we have for the “cost of money.”

And that price affects your stock portfolio both directly and indirectly.

For starters, the 10-year yield is one of the most important numbers that goes into stock valuations.

At the most basic level, a stock’s value is the sum of all future cash flows discounted back to today’s value, and the 10-year yield is the most common input in that discount rate.

That means the higher the yield, the lower the value of the company’s future earnings… and the lower the valuation investors are willing to pay.

Then there’s the question of optionality. There are two main asset classes fighting for a place in every investor’s portfolio: stocks and bonds.

As a rule, bonds are safer investments that give you steady income with a relatively low risk of losing your money. The catch is that bonds usually don’t pay much.

Stocks can earn you more, but they have a way of crashing once in a while. That’s why investors demand a higher return from stocks as compensation for taking that extra risk.

That extra return is called the equity risk premium. So when bond yields rise, they eat into that premium, making stocks less attractive by comparison.

By most estimates, 5% is the threshold where investors may start seriously rethinking stocks and moving more money into bonds, which is why it’s so closely watched.

And last but not least, basically all credit, including mortgages, credit cards, personal loans, corporate bond yields, is benchmarked against the 10-year yield.

So the higher this number goes, the higher borrowing costs across the whole economy, which can weigh on growth and spending.

And lower growth and weaker spending usually mean lower earnings, which feed back into lower stock valuations. Rinse and repeat.

Commentary by our editor @danrunk

On Saturday, Fox News TV political anchor, Bret Baier, got Donald Trump tangled up in his own argument on Iran.

Trump: “‘We're gonna go get it [uranium]. We're not gonna let you take it.’ They said, ‘We can't take it. We don't have the capability of taking it.’ I said, ‘Why?’ He said, ‘Because it was hit so hard.’ I mean, the mountain literally collapsed on it, a granite mountain.”

Baier: “So why isn't that good enough?”

Trump went on babbling about “Space Force,” trying to change the topic until Baier cut him off and asked point-blank:

Baier: “Why are we where we are? Did you underestimate Iran’s pain tolerance?”

That question lands at the core of Trump’s Catch-22. Iran does not stand much of a chance against Washington, but the regime appears willing to fight to the bitter end.

Bluffing or not, that makes it very difficult for Washington to end this conflict on its own terms.

There’s only so much you can do by shelling from the skies. Boots on the ground would be a big political risk. And even if Trump backed off, Tehran appears intent on making the world pay through Hormuz.

Meanwhile, the Hormuz crisis is giving Trump a double headache: one for the economy and another for the stock market.

➡️ On the economic side, headline inflation rose 3.8% in April, the highest level in three years. Gas prices hit $4.52 a gallon nationally, up 50 cents in just a month. Six states are now paying over $5 a gallon.

Most of the inflation is still “in transit,” though, because higher energy prices are feeding through supply chains. (In fact, wholesale inflation is at its highest since 2022)

➡️ On the stock market side, the 30-year Treasury yield crossed the 5% mark last week for the first time since 2007. That’s bad for stocks in three ways:

- Higher borrowing costs, the most obvious one

- Higher discount rates. A stock’s value is essentially the sum of all future cash flows discounted back to today’s value, and Treasury yields are the biggest component of that discount rate

- Higher yields could trigger a flight to bonds because earning a virtually guaranteed 5% suddenly looks very attractive again

So far, the strongest earnings season in roughly 20 years has offset rising yields, but that kind of growth won’t last forever.

All of this is making the Iran war about as politically unpopular as the Vietnam War became in the 1970s. Not exactly the kind of backdrop you want heading into the midterms. And Iran knows that.

Commentary by our editor @danrunk

#iran #hormuz

At the very last minute, NVIDIA CEO Jensen Huang boarded Trump’s Air Force One bound for Beijing.

Earlier yesterday, multiple outlets reported that Huang was not joining Trump’s China delegation. Then, during a refueling stop in Alaska, Huang made a surprise appearance.

@CNBC and @semafor both cited sources saying Huang was indeed invited ad hoc. (Trump later dismissed those reports as “fake news.”)

Now CEOs of this caliber don’t get emergency-flown to Alaska to join the first presidential delegation to China in nearly a decade for no reason. And there are a few theories floating around.

The first is that the delegation suddenly needed Huang’s physical presence because semiconductors became the actual sticking point in negotiations.

That theory rests on two undeniable truths: AI is the new oil, and Nvidia’s chips are now so systemically important that Huang himself has become part diplomat, part industrial-policy asset similar to Saudi oil ministers in the 1970s.

The second theory is that Trump wanted to counter a growing rumor about his possible beef with Nvidia after nearly every major tech CEO got invited except Huang.

That matters because Nvidia is too important to fail on a national level. It sits at the center of the AI trade, which is pulling in trillions of dollars and driving most of the economic growth.

If anything happened to Nvidia, AI-bound capital would quickly dry up, and the economy would very likely slide into recession. That also matters on a national-security level because less capital means slower progress and more chances for China to catch up.

So the administration may simply not want to take any risks.

Either way, there’s a good chance we get some AI news out of Beijing in the next few days.

Commentary by our editor @danrunk

$NVDA

Micron may be the next big AI infrastructure trade. 🚀

DA Davidson and Deutsche Bank both see the stock reaching $1,000, as AI demand puts more pressure on memory chips and data center capacity keeps expanding. 📈

$MU

eBay just shut down a massive takeover attempt from GameStop CEO Ryan Cohen. 🚫

The $56 billion bid valued eBay at $125 per stock, but the company called it “neither credible nor attractive.” 📉

$EBAY

$GME

Akamai just landed a $1.8 billion AI infrastructure deal and investors are paying attention. 👀

The news sent $AKAM up 25% in premarket trading, with the stock now up 37% over the past 12 months. 🚀

The company says rising AI demand is driving growth as it expands its cloud infrastructure business alongside major model developers. 🤖

@Akamai

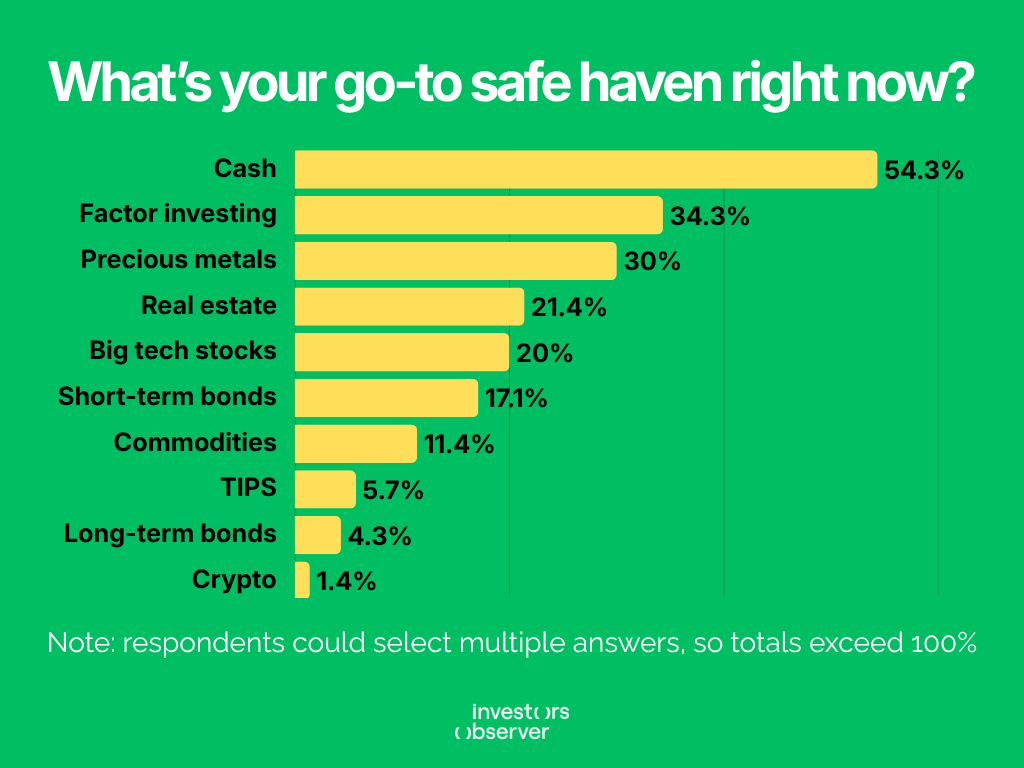

What’s your go-to safe haven right now? 🛡️📈

We asked Observers, and here’s where investors are hiding out:

💵 54.3% – Cash

📊 34.3% – Factor investing

🪙 30% – Precious metals

🏠 21.4% – Real estate

💻 20% – Big tech stocks

📉 17.1% – Short-term bonds

🌾 11.4% – Commodities

🛡️ 5.7% – TIPS

📆 4.3% – Long-term bonds

₿ 1.4% – Crypto

The biggest takeaway?

More than half of respondents still see cash as the safest place to ride out uncertainty, while riskier assets like crypto barely registered.

Which safe haven are you leaning toward right now? 🤔

Want to be part of our community and receive daily “before the bell” newsletters? Join here: https://t.co/LIep4MRKOZ

Palantir Technologies shares fell nearly 7% on Tuesday despite reporting strong first-quarter results that beat on earnings and revenue.

The weak spot was U.S. sales, where commercial revenue fell short of expectations, raising concerns about growth in its core market.

$PLTR

Michael Burry just exited GameStop after its bold $55B bid for eBay raised red flags. 📉

He warned the deal could push leverage to ~7.7x EBITDA, calling it incompatible with his “Instant Berkshire” thesis. ⚠️

$GME

Two big developments today that could take the Iran conflict to a whole new level.

Starting today, Washington is supposed to begin an “evacuation” of trapped oil tankers in the Hormuz. Iran responded threatening the end of a ceasefire and attacks on U.S. warships.

That’s a big about-face from a few months ago when the U.S. military said it was “not ready” to accompany vessels where it could come under fire.

There’s very little detail on this operation, but it suggests that negotiations on Hormuz are likely going nowhere, or at least not in the way Trump wanted.

Meanwhile, for the first time in recent memory, China publicly defied Washington’s sanctions after ordering its firms to trade with U.S.-blacklisted refiners

This move sends two important messages.

For China, Washington has crossed a red line and it has to respond even at the risk of retaliation against its banking sector. On the other hand, this may be a pre-calculated move to build up bargaining power ahead of Xi’s meeting with Trump on May 14.

For Trump’s part, China throws a wrench into his plan to quickly choke off Iran because sanctions were supposed to wean Iran’s biggest buyers off its oil, but that only works if China complies, which it isn’t.

This is going to be an eventful week.

Commentary by our editor @danrunk

#projectfreedom #china

When will the Strait of Hormuz reopen under pre-war conditions? 🚢

We asked 200,000 Observers, and here is how the numbers shook out:

☀️ 42% – This Summer

🌱 24% – End of Spring

❄️ 18% – Winter

🚫 16% – Never

That’s two-thirds of our community betting on a reopening by summer's end.

Which crowd do you side with? 🤔

Want to be part of our community and receive daily "before the bell" newsletters? Join here: https://t.co/LIep4MRKOZ

Hedge funds now hold about 8% of the U.S. Treasury market, a record share, according to Apollo data. But this isn’t a traditional “safe asset” allocation. It’s a tool for an arbitrage trade.

In simple terms, funds borrow cash using Treasuries as collateral, then use that borrowed money to buy more Treasuries while hedging with derivatives, typically futures, to capture small price differences between the two.

The borrowing behind these kinds of arbitrage trades now exceeds $6 trillion.

You may ask why this matters. If borrowing costs rise or Treasury prices move against these trades even slightly, funds may be forced to unwind positions quickly.

If that happens at scale, it can push Treasury prices down and send yields higher across the market.

Continue reading in our latest edition ⤵️

https://t.co/fnwbL7ofyy

Tesla signals major shift with $25 billion investment in AI and robotics infrastructure. 🤖

This heavy spending will pressure near-term free cash flow but positions Tesla $TSLA as more of an AI/robotics infrastructure play long-term.

h/t Bloomberg

@TeslaNewswire

Asian markets stumble even as Wall Street celebrates record highs 📈

Asia-Pacific stocks opened broadly lower as oil prices slipped and geopolitical uncertainty lingered, despite a ceasefire and U.S. President Donald Trump saying the Iran conflict “should be ending pretty soon.”

Brent crude fell to $98 while Japan’s Nikkei 225 dropped nearly 1%, Hong Kong’s Hang Seng declined over 1%, and China’s CSI300 edged lower, underscoring how fragile sentiment remains across the region.

Meanwhile, the S&P 500 just logged its 12th straight gain, its longest winning streak since 2009, highlighting a widening gap between U.S. momentum and global caution.

Is this divergence sustainable?

$NIKKEI $SPX $HSI $CL