@leadlagreport It's not disinflationary if the US now has significantly higher tariffs than it did five weeks ago. It still has 30% on China and 10% on the whole rest of the world. The bond markets have noticed but somehow the stock markets haven't.

Brilliant news for Harland & Wolff – we have been named as preferred bidder by the Falkland Islands Government (FIG) to provide a replacement of the islands’ port facility, known as FIPASS. The contract is valued at between £100 and £120m.

You can read more about this exciting development here: https://t.co/qVd0kJ3dFr

#makingwaves🌊

#i3e - AECO gas prices are what matters here. So far YTD it is up 45% from $1.65 to $2.40 today.

They’ve just announced a Q4 dividend of 0.25p, if this is maintained then a yield of 10% pa.

Dividends are FCF linked. 📈

@GeordiePhilUK@TarzanTrader1#HUM is planning to pay off $70m in debt next year off the back of 200koz production.

A gold price above $2,000/oz delivers confidence they can do that. In today's money that must add 9.2p to the SP just to keep the EV the same.

A stark illustration of the abject madness of investors sometimes - Wildcat #WCAT mkt cap almost the same as Corcel #CRCL. One co has @ £300k on balance sheet & no assets. The other has pro forma cash due of @ 70% market cap, 3 blocks in Angola with estimated OIP of approaching

Insane.

The current Nasdaq-to-Treasuries ratio stands 70% higher than its level during the tech bubble's peak.

This chart puts into perspective how, despite ongoing issues with Treasuries, the more relevant question now is whether overall equities can remain as overvalued as they are in today's interest rate environment.

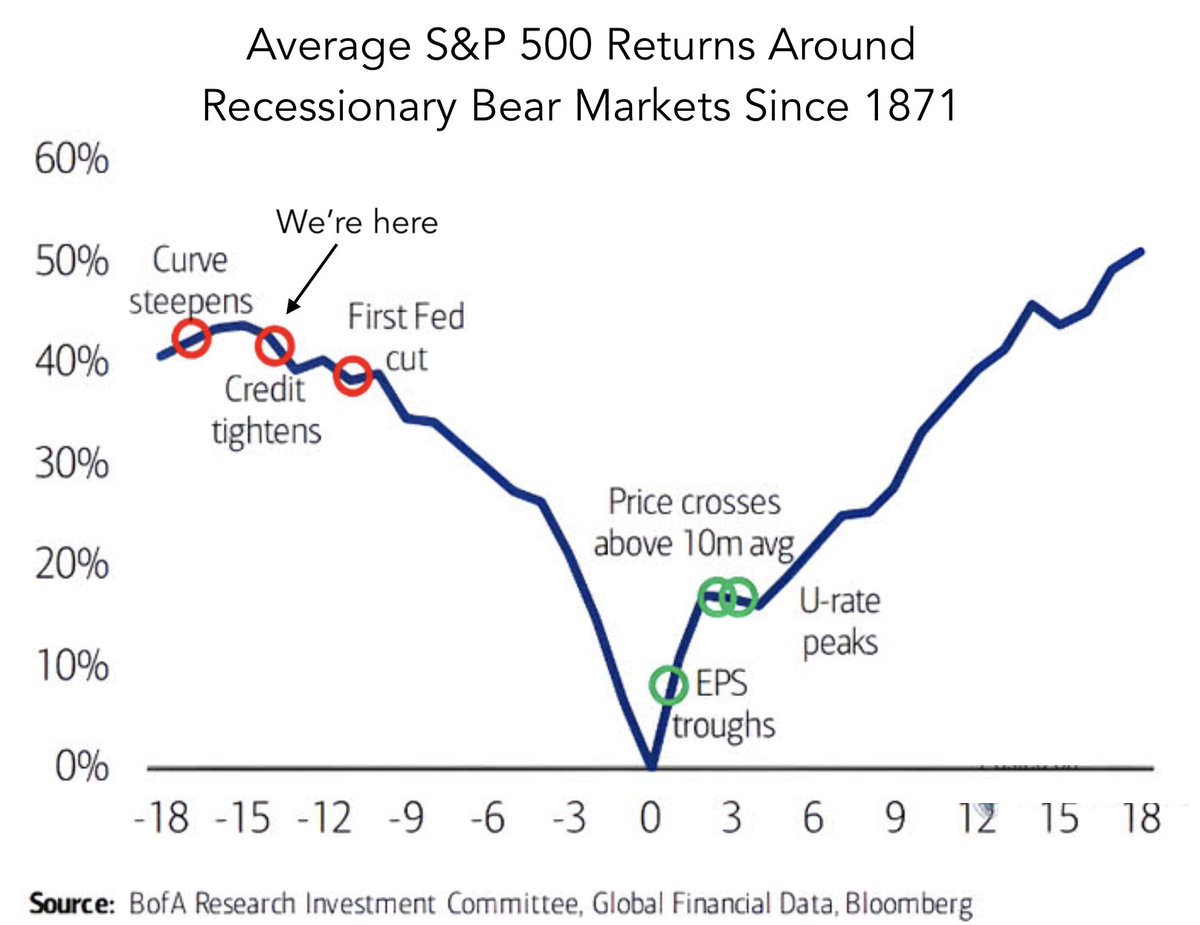

Lets be very clear about the potential risk to #stocks on a steepening yield curve such as we are experiencing now. This chart is worth studying closely...

The chart highlights 4 episodes where the yield curve underwent steepening over the last 35 years and what happened to #equities in the subsequent period.

In the lower panels, the performance of the #SP500 Index is highlighted with the cumulative returns over rolling 6 month windows in the navy (positive) and orange (negative) bars.

We can see that in each case, the performance of equities became deeply negative over protracted periods. In the bottom panel, the $VIX is charted and reflects the same dynamic, with each case characterized by rising downside volatility for an extended period.

The point of this exercise is to highlight the risk to equities on further steepening of the yield curve from here, should higher yields cut into the growth outlook which is exactly what preceded each and every one of these examples.

You've probably seen the evidence circulating Fintwit of the #softlanding narrative being often expected, but ultimately illusory. These episodes demonstrate how such a situation plays out in yields and ultimately stocks.

This latest steepening kicked off in June and has initially been driven by "higher for longer" expectations which have accelerated recently post #FOMC. That could in essence be a positive message for equities as its implying stronger for longer nominal growth.

However as I've highlighted in previous tweets, the market may impound higher growth (and elevated treasury supply) into higher long end yields for a while as is happening now, but the risk is that with the economy already in slowdown mode after 500+bps of rate rises, the resultant increase in long end rates is the straw that breaks the camel's back and destroys that same growth.

There is early evidence of that exact dynamic now as we head into Q4, with renewed weakness in consumer sentiment and the NAHB housing market index, sequential falls in real disposable income, slowing retail sales and a likely fall in residential construction activity ahead. Should those trends continue, we should expect a growth scare to refocus the market on #recession pricing (and the timing of cuts to short end rates again) which perversely, like in many of these examples, can drive the yield curve even steeper.

It seems incongruous to write it, as pricing out those same rate cuts is what the #Fed's recent objective was at the FOMC. But their aim in doing just that was to create a further tightening of financial conditions to SLOW down nominal growth and tame inflation even though achieving their objective will lead back to the same rate cuts they just priced out. The difference between a benign or destructive outcome comes down to the magnitude and rate of change to the growth outlook.

If that change results in anything like the highlighted examples over the last 35 years, it would likely be very destructive to stock prices.

#macro #VIX $SPY $QQQ #Nasdaq100 $TLT #HOPE

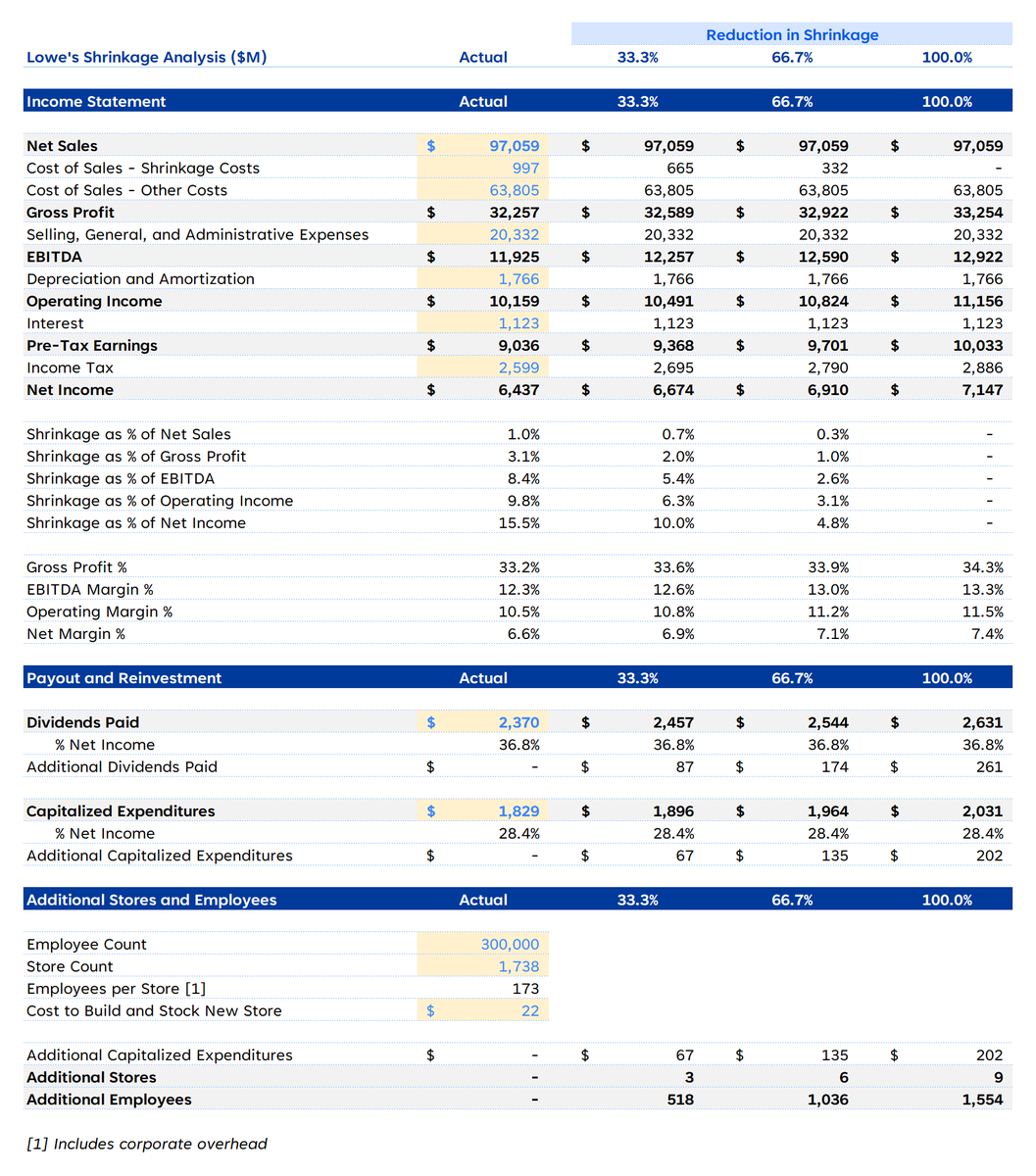

I’ve lost all patience with the gaslighting about shoplifting—it’s just 1% of revenue, it doesn’t hurt anyone but rich investors, blah blah blah.

Using numbers from Lowe's 2022 10-K, here's a quick analysis showing how destructive it really is, including killing 1,500+ jobs. 👇

(1) For retail chains, 1% of revenue is an absolutely massive number. In the case of Lowe’s, inventory shrinkage—most of which is consumer shoplifting or employee theft—cost the company $997M in 2022.

That’s right: One company lost nearly a billion dollars from theft. In one year. If that $1B were the revenue of a company in its own right, it would be large enough to be publicly traded.

And, again, this is just Lowe’s. Think of the scale if you added in Walmart, Target, Home Depot, Dick’s Sporting Goods, and all the grocery stores and drug stores across the country. Imagine how many billions of dollars that must be.

All of a sudden, 1% doesn’t seem that trivial anymore, does it?

(2) Even if you still believe that 1% of revenue isn’t that big a deal, let’s look at it in terms of earnings. In 2022, Lowe’s generated $11.9B in EBITDA and $6.4B in net income. That $1B in shrinkage represents 8.4% and 15.5% of those numbers, respectively.

In other words, for every $6.50 in earnings for Lowe’s shareholders, they’re losing roughly $1.00 due to theft.

If Lowe’s were able to eliminate all shrinkage, EBITDA would grow more than 8%, and net income would grow 11%. The company would generate an extra $710M in earnings, all without having other sell a single extra item or grow sales by even a dollar.

(3) For investors, that $710M of foregone net income is massive. In 2022, Lowe’s paid out 36.8% of net income in the form of shareholder dividends—actual cash payments to its owners, including mom-and-pop retail investors and the pension funds that represent a large portion of its shareholder base. Assuming that Lowe’s kept the same payout ratio, eliminating shrinkage would create another $261M available for dividend payments.

(4) More important, though, is the earnings that Lowe’s doesn’t distribute—the cash they reinvest back into their business. In 2022, Lowe’s had $1.8B in capex, in the form of new stores, improvements to existing stores, and other strategic initiatives. This $1.8B represented 28.4% of earnings.

If Lowe’s kept the same ratio and applied it to an incremental $710M in net income, that would represent an extra $202M available for capex. It costs Lowe’s about $22M to build and stock a new store, and the company has an average of 173 employees per store (inclusive of employees working in corporate-overhead positions).

In other words, stolen merchandise is costing the company the opportunity to build another nine stores, which would create 1,500+ new jobs.

(5) To summarize: $997M in shrinkage turns into $710M in foregone net income. This foregone net income, using 2022’s ratios, means $261M in shareholder dividends missed out on, nine stores not built, and 1,500+ jobs not created.

So you really want to say that shoplifting isn’t a big deal? You really want to justify it and say that it’s a victimless crime?

Go tell that to the senior citizens not getting the dividend checks that they otherwise would have received. Go to nine mid-size towns without a Lowe’s and tell them that. Go find 1,500 people looking for retail jobs and tell them that the only people getting hurt here are fat-cat shareholders.

Really, go on.

This chart has to be the big elephant in the room.

The recent collapse in Treasuries is yet to impact equity markets that continue to defy gravity at historically inflated valuations, particularly the big tech companies.

5. Play to your advantage

Jim Simons' Renaissance Technologies is only right 51% of the time.

The key to trading success is:

- Winning more from your winners

- Losing less from your losers

Place asymmetric bets where your downside is capped and the risk is to the upside.

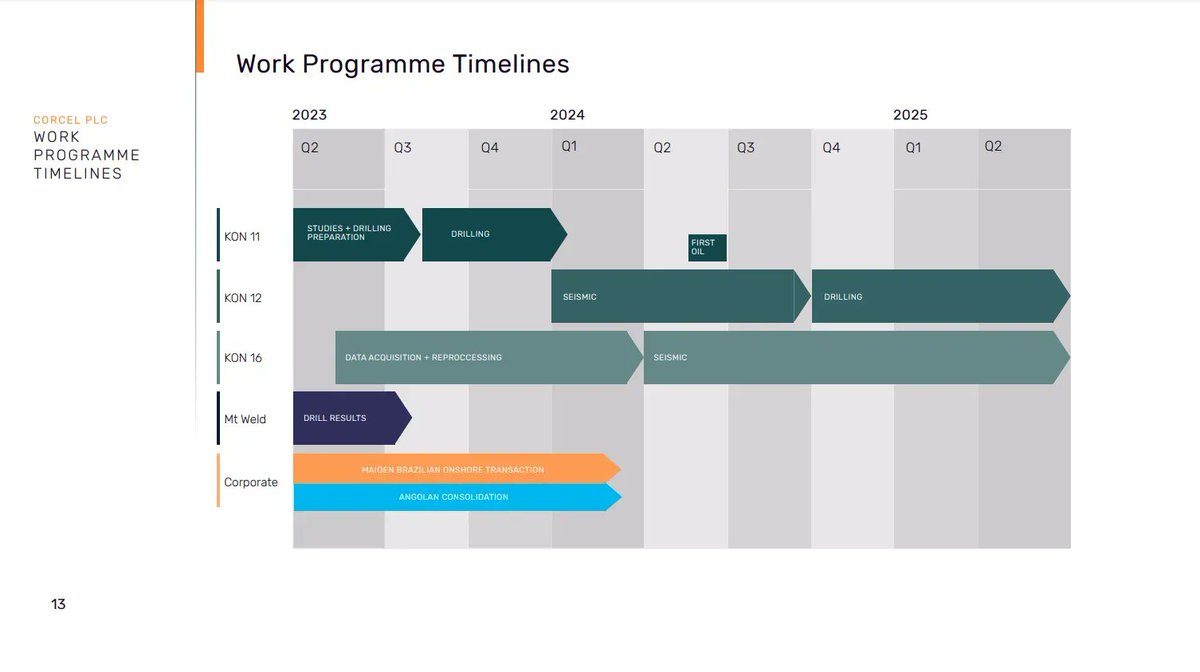

#CRCL#Oil#RNS

𝗛𝗶𝗴𝗵𝗹𝗶𝗴𝗵𝘁𝘀 💡

Agreement with the Lender to fund £1m in October 2023 and £1m in January 2024, with a further £8m to potentially be made available over a three-year term.

https://t.co/b454pGmxlE