Recent advancements in one-shot AI protein / antibody development by Chai, Nabla, AI Proteins, Generate, and a few others are accelerating the *main* theme in biotech:

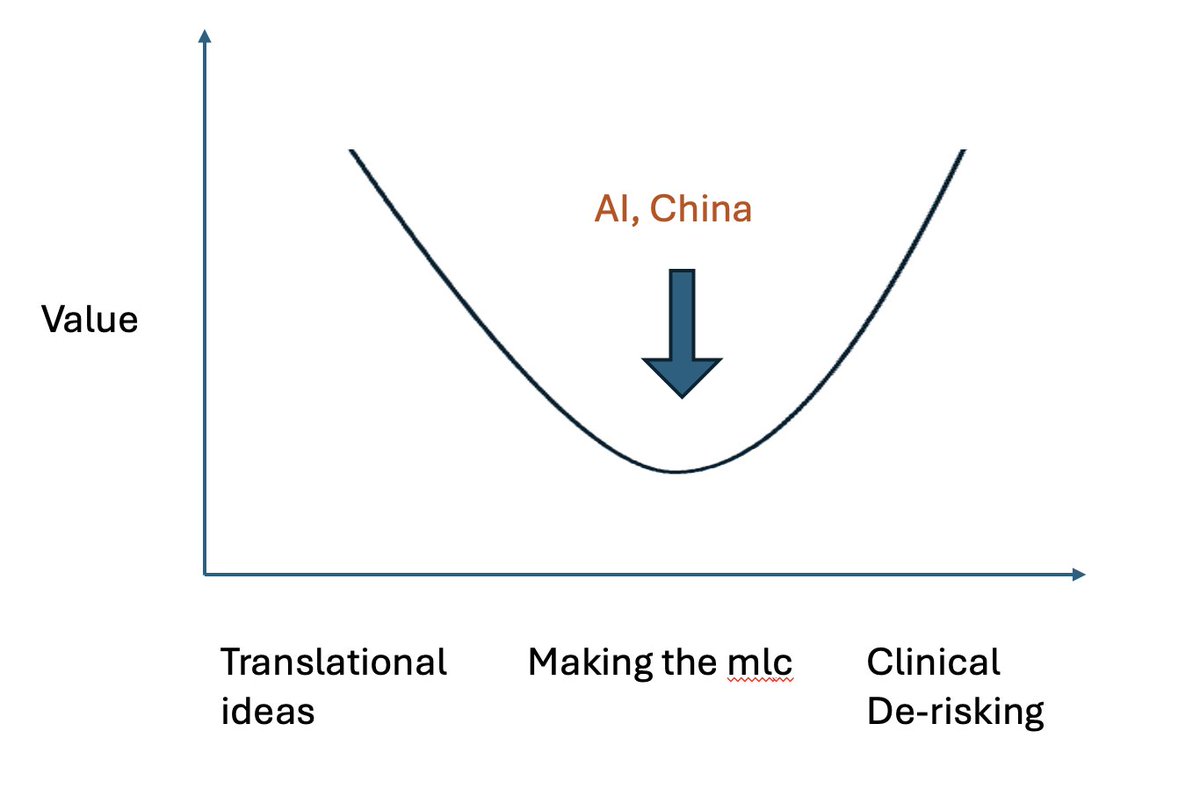

Value of building the molecule is going down. The value of novel targets, novel translational ideas, AND also the value of clinical execution is going UP

Here's where the value graph is moving towards:

The twin forces of AI and China are quickly driving down price of mlc dev across many modalities:

For AI - mainly Ab right now, emerging for genetic medicines, small mlc, ADCs, cell therapy;

For China - Abs, cell and gene therapy, small mlc, and soon genetic medicines

Having a "best in class" mlc is no longer enough - many tech platforms will soon offer you a mlc priced on metered compute (getting cheaper) and China CROs / biotechs will continue to eat the world with (over)capacity (continued involution).

To make a valuable drug, you must differentiate on either:

a) Novel translational ideas.

Novel targets, novel mechanisms, but not just that - connecting targets with diseases; novel application of certain targets in new disease settings, new intuition on which patient pops have widest therapeutic index for a drug, etc

OR

b) Clinical execution.

Determining the appropriate endpoints in a trial. Recruiting the right patients. Appropriate relationships with the right PIs / clinical sites. Ability to finance registrational studies in US markets ($10s to 100s of Ms)

Either be a translational target discovery engine / tech platform that unlocks new modalities (which unlocks new translational hypotheses) OR get a team of grizzled clin dev / CMO vets and go raise $X00M+ to validate a clinical hypothesis

Living in the middle (ie being "full stack") is dangerous work (at least for a startup)

**A grand unified theory on what will happen in biotech in the next 10-20 years**

the two major forces reshaping industrial biotech in the next decade are:

1. China

2. AI

- and they're critically linked

how?

China's low R&D cost basis democratizes execution by providing infrastructure to more drug developers (similar to how AWS helped cloud apps explode in 2010s)

AI makes scientific information much more freely available; agents & lab automation increase R&D productivity as well as throughput, further deflating development costs

What happens when many more translational ideas can be tried much more cheaply?

Value starts accruing in the best ideas to try ie the value shifts earlier in the value chain

if the cost of everything from preclinical R&D to clinical trials are dropping significantly due to combo of AI and China, the disparity between clinical stage vs early pipeline assets shrinks dramatically from the current order of magnitude difference

The premium on true creativity, novel scientific insight, fundamentally new biology will 100x

In a few years the top-of-industry drug hunters / translational biologists will command a hefty premium (maybe not $100m a year like current top AI scientists but ... maybe??)

Even more provocatively, foundational models in translational biology that surface / accelerate novel biological hypotheses will suddenly capture outsized value

When will a translational foundational model be worth more than a top 10 pharma co?

sounds crazy... but like everything else --> slowly, then all at once

There is a fundamental flaw with the argument: “U.S. is 70% of global profits in tx and therefore can dictate which therapies are allowed in the U.S., including excluding China assets".

The weight bearing assumption is that China’s biotech industry will not be able to sustain itself without US market.

This does not conform with reality.

Prior to 2022, Chinese biotech industry had minimal capital inflows from outlicensing / newco’s to US / Western pharma AND a very austere tx pricing environment domestically. Yet significant companies grew to dominate the domestic market, and many Chinese biotechs managed to move up the innovation curve.

Do you think that Chinese biotechs sprang up overnight in Dec 2022 when this out licensing wave started? Akeso, Keymed, Hengrui, Hansoh, Innovent, and so many others have been around for years - pretty much all of them starting off by making drugs for the domestic China market. US out licensing deals were few and far in between, and yet many of them became $ B+ or $10’s Bn companies in the process.

Furthermore, in recent months the Chinese payor market is now getting better at rewarding true innovation. 2025 NRDL reform introduced a higher pricing tier for true innovation (not me-betters). Domestic economics for first-in-class assets are getting meaningfully stronger, regardless of the exit to Western pharma path.

From a unit economics perspective, "removing the exit to the West will kill Chinese biotech progress" argument just isn’t supported by facts on the ground.

Another serious drawback to the banning argument is that presumes Chinese drugs are only me betters or me toos that are knock offs of western efforts (and will continue to be). Otherwise, the interpretation is that US patients would be ok not having access to the latest and greatest drugs.

This, too, does not conform with reality.

Chinese biotechs are now making net new innovative drugs across ADCs, in vivo CARs, genetic medicines and many more modalities, going after novel targets, payloads, and incorporating delivery tech that we have not seen here in the west; and if they work clinically - US patients will want access to as they will improve the clinical treatment paradigm.

I have spoken to the Chinese biotech CEOs and seen these programs. Some will work and some won’t (that’s just drug discovery), but they are coming, and there is no use in arguing about it.

Do you think it will be acceptable that US patients will not have access to best in class / first in class drugs?

so to summarize: in the US, we have an industry that is *losing* pricing power (no matter if R or Ds are in power, tx pricing pressure is on the docket), trying to keep drugs being made from a country with *increasing* pricing power (based on government support) out, at a time when those drugs are increasingly innovative.

Who do you think the actual loser from this is going to be?

US patients.

all this to say: the back and forth arguing is a moot point, the innovation is coming **whether we like it or not**.

I’d suggest we in the US get busy competing, investing in innovative science, deregulating trials, and doing less belly aching.

Patients, American and otherwise, are waiting.

Then Chinese biotechs will not develop for the US market

And if their assets are good, US patients will miss out

The fundamental flaw of the US profit argument is that Chinese biotechs will keep developing valuable, clinically impactful drugs for their own population no matter what

It’s just a matter of whether US patients will have access

@SylvainGariel Even in China they are not mentioned with leaders of local biotech industry yet - but chalk this up to biotech entrepreneurs in China being mostly ex traditional drug discovery folks and relatively conservative / not fully being computational pilled yet

moolenaar's proposal would likely have the opposite of the intended effect. if u ban US pharma from acquiring chinese IP, what is likely to happen is EU/Japanese pharma will get that IP, and u hand them a structural advantage. if u somehow convince them to also ban china deals, then u force chinese biotech to forward integrate and compete directly sooner. hengrui and at least 10 other biotechs already have the resources to do so. then let's say u ban those companies from the US market, then u just have a replay of the EV story, chinese pharma will just take over the rest of the world.

the proposal also tries to scare people by drawing the analogy to chips and rare earths. there is no such analogy. licensing deals are for IP, and almost always include the right to manufacture wherever you want. so there is no supply chain risk. in fact, in drug world, the vast majority of the value of drug IP accrues to whoever develops and commercializes a drug, not who invented it. so right now western pharma is the winner from this relationship.

so if the Q is well how do we not lose to china longterm? the answer is we must compete. america is great, we should lean into our natural advantages. continue to lead in breakthru science, maintain fda's position as the preeminent regulator, apply our cutting edge technology, and entice the world's best with the most pro-innovation commercial market. these leads are larger than many realize. we should mitigate our weaknesses, most importantly the bureaucracy that comes from being around longer than others that slows us down.