“Why no $TEL upgrade airdrop like last time?”

IMO - the two biggest reasons:

Airdropping while legacy TEL still circulates creates up to 200B in simultaneous claims causing a potential supply dilution. The current plan opt-in guarantees 1:1 supply via lock-and-mint across both v2 and v3. New supply can only be created if legacy $TEL is converted. This gets handled by a simple interface that we will be putting guides out for and will be hosted on the association website.

Airdropping to raw addresses dumps tokens into bridge contracts, making trackers misattribute pooled supply to single “holders.” We are still dealing with the aftermath of that decision from the last time, where aggregates like dexguru or CoinGecko see the polygon bridge and flag it as a massive holder, making metrics like “supply held by top wallets” disproportionally flag tel as a scam

Check out more faqs here:

https://t.co/sZ0fZCsUOH

🚨 Why This Could Be the Biggest Bullish Catalyst for $TEL

For years, $TEL has carried a hidden disadvantage that most investors never realized.

Unlike almost every other ERC-20 token, TEL uses 2 decimals instead of the industry-standard 18 decimals.

That single design choice created a surprising amount of friction.

Every exchange, wallet, DeFi protocol, custodian, and bridge that wanted to support TEL often needed custom engineering. In an industry where thousands of tokens compete for attention, many platforms simply prioritized assets that worked with their existing infrastructure.

The result? TEL has spent years facing technical barriers that most projects never had.

This proposed upgrade changes that.

By moving to the standard 18-decimal format, TEL becomes significantly easier to integrate across the Ethereum ecosystem. It won't automatically guarantee listings, but it removes one of the biggest technical reasons exchanges and platforms had to treat TEL differently.

That's a major shift.

At the same time, the upgrade activates $TEL as the native gas token of Telcoin Network. Every transaction on the network will require TEL, creating recurring on-chain utility tied directly to network activity.

Combined with cleaner cross-chain liquidity, improved DeFi compatibility, and a modern bridging architecture, this proposal doesn't simply modernize the token—it prepares TEL to operate on the same technical standards as the broader EVM ecosystem.

Existing holders keep exactly the same number of tokens through a 1:1 upgrade, with no dilution and no increase in supply.

For nearly eight years, TEL has been playing with a technical handicap.

This proposal removes that handicap.

If Telcoin Network delivers on its vision, many may look back at this upgrade as the moment TEL finally became technically ready for global adoption.

Bullish on the future of $TEL. 🚀

https://t.co/luMm4i0vz6

TEL just launched the first regulated on-chain bank account in the US. real routing number, ACH deposits, full Nebraska bank charter.

full story:

https://t.co/vaAPW7Md2a

How yield would work in theory:

This dual structure future-proofs Telcoin under the CLARITY Act while giving everyday users (remittance senders, DeFi participants, or simple holders) a single, regulated product that bridges traditional banking yield with blockchain utility.

The bipartisan Tillis-Alsobrooks change in the CLARITY Act has a very clear distinction: passive, bank-like yield (interest-style rewards simply for holding stablecoins) is reserved exclusively for chartered banks, while activity-based rewards (tied to actual usage like payments, trading, lending, or liquidity provision) remain allowed for everyone.

Telcoin’s Nebraska Digital Asset Bank charter puts it in the rare position to operate on both sides of this divide at once - something most pure crypto stablecoin issuers or traditional banks can’t match.

1. Fiat Bank Side (Passive / Bank-Like Yield – Reserved for Chartered Banks)

Telcoin Digital Asset Bank is a fully regulated U.S. bank, so it can legally offer bank-style yield on eUSD holdings.

Reserves are held in cash + short-term U.S. Treasuries (standard bank practice). The bank earns real-world yield on those Treasuries and can pass a portion back to eUSD holders as compliant interest or deposit-like returns - exactly what the compromise protects for chartered banks.

1. Users deposit fiat USD

2. bank mints eUSD 1:1

3. holders earn yield simply for holding (subject to banking rules, disclosures, and Nebraska oversight).

No offshore issuer or separate custodian needed.

This is the “bank-like” yield that non-bank crypto firms are now barred from offering. Telcoin gets it by design.

2. Crypto Stablecoin Side (Activity-Based / “Buy-and-Use” Yield – Allowed for All)

eUSD lives natively on Ethereum and Polygon in self-custodial wallets, so it’s fully programmable and usable in DeFi, remittances, payments, and the Telcoin network.

Telcoin can layer on actionable, usage-based rewards that the compromise explicitly permits: liquidity provision, on-network transactions, remittances, spending, or participation in Telcoin’s DeFi-connected ecosystem.

Examples:

- rewards for providing liquidity in Telcoin pools, earning fees from real-world payments/remittances, or yield from on-chain activity (similar to yield farming but fully compliant and tied to genuine use, not passive holding).

Because it’s issued by the bank itself, these crypto-native rewards can sit on top of (or alongside) the bank-like yield without violating the new rules.

Net result for Telcoin users: You get the best of both worlds in one regulated asset - bank-grade passive yield on your eUSD balance (from Treasury-backed reserves) plus crypto-native activity yield when you actually use it on-chain.

No other major stablecoin issuer currently combines a full U.S. bank charter with direct on-chain issuance and DeFi connectivity like this.

That’s exactly why @Telcoin’s official account (one known for no-fluff and only posting when it's of importance) noted the support and importance of #CLARITY in its current form.

telcoin:native

From humble beginnings to revolutionizing global finance; let's talk about Paul Neuner @TelcoinPaul founder and CEO of @telcoin and the powerful life lessons from his journey. 🌟

#LearnKaroCryptoKaro $TEL #Telcoin

👨🏻🎓 A Notre Dame graduate, class of '97, Paul kicked off his career in D.C. and internationally, gaining a truly global perspective early on. He built deep expertise in telecom, founding Mobius Wireless Solutions in 2006 to combat fraud and secure mobile networks across Japan, the Middle East, and beyond.

For over a decade, he contributed to the GSMA Fraud and Security Group, sharpening his skills in a high-stakes industry before successfully exiting and boldly pivoting to blockchain in 2017 by launching Telcoin.

📱 Telcoin emerged from a clear vision: billions have mobile phones but lack easy access to banking. Paul aimed to bridge that gap with low-cost DeFi, remittances, and financial inclusion in a mobile-first world.

💸 Today, Telcoin is pioneering Nebraska's first digital asset bank, partnering with regulators to blend traditional finance with crypto, turning obstacles into opportunities for underserved communities worldwide. Along the way, he also founded ventures like Pangea K.K. in Tokyo and Sedona for advanced fraud tech, showing relentless adaptability.

💎 Life lessons from Paul's path:

1️⃣ Embrace the unknown: Ditching a proven telecom career for blockchain took real courage. Innovation happens when you ride the wave of change instead of waiting for it to hit you.

2️⃣ Build globally, think inclusively: Years in diverse markets ~ China, Japan, and more taught him that real impact comes from understanding local needs and cultures.

3️⃣ Persistence through iteration: Like his admired inventor Thomas Edison, Paul turned setbacks into breakthroughs, from telecom security to crypto banking; proving consistent effort wins.

4️⃣ Compliance builds trust: In crypto's fast-moving space, working hand-in-hand with regulators, even relocating HQ to Nebraska transforms challenges into lasting advantages.

Paul's story proves your journey isn't just about the end goal, it's the bold pivots, global hustle, and mission to improve lives that matter most.

Thanks for sharing your perspective, and I appreciate the honesty. I don't hold the same opinion, but I am glad you still follow me :)

I have conviction that even though the price is bad for $TEL that the team is doing the right thing by the community and that it will work out.

I understand that comes across like blind optimism to some, but I have spent over 400 hours researching, speaking to the team, meeting some team members in person, comparing the charts, modelling out historical macro data and other things.

I can empathise that right now it feels crap, but I don't give up on things I have researched, acted on and am being patient with.

I have left many other crypto communities over my 8 years and I believe 99% of crypto is a scam, but $TEL is different.

$TEL listing on Kraken is big.

Price probably won’t move much yet and that’s fine.

What matters is access + credibility

When the real launches roll out this year, millions can now buy instantly.

This is exactly what I wanted to happen before Bank and network launch $TEL the 🌍

Ethereum is the #1 choice for global financial institutions.

Over the last few months, adoption has accelerated. Here are 35 stories of how institutions are building on Ethereum.

1/ @krakenfx launched xStocks on Ethereum, issuing tokenized versions of popular U.S. stocks and ETFs as ERC-20 tokens.

Kraken’s eligible clients can now deposit and withdraw fully collateralized equities, directly on Ethereum.

2/ @OndoFinance launched Ondo Global Markets on Ethereum with 100+ tokenized U.S. stocks & ETFs.

24/7 access to programmable equities, backed by real securities, is now available alongside DeFi integrations for lending, trading, and more.

3/ @ChinaAMC_HK launched its Select USD Money Market Fund on Ethereum, one of the first tokenized funds from a major Chinese asset manager.

One of Asia’s largest firms (over $449B AUM) now provides access to high-quality, short-term USD instruments with 24/7 settlement.

4/ @Fidelity introduced the FDIT tokenized money market fund on Ethereum.

The Fidelity Digital Interest Token (FDIT) brings the bank’s investors the speed of onchain settlement alongside the stability of traditional instruments.

5/ @Google announced the Agent Payments Protocol (AP2), enabling AI agents to autonomously execute payments using stablecoins on Ethereum.

Built in collaboration with The Ethereum Foundation, Coinbase, MetaMask, and others, AP2 allows AI to transact securely, bridging the gap between automated intelligence and finance.

6/ @UBS, @PostFinance, @sygnumofficial, and the Swiss Bankers Association successfully piloted Deposit Tokens on Ethereum.

By demonstrating legally binding cross-bank settlement on Ethereum’s public infrastructure, the proof-of-concept paves the way for programmable, instant, cross-institution settlement.

7/ Santander’s @openbank_es launched ETH trading services in Germany, allowing customers to buy, sell, and custody ETH directly through their bank accounts.

This integration is a strong signal of institutional confidence in ETH under MiCa regulation.

8/ @AmericanExpress launched Amex Passport, blockchain-based travel stamps minted as NFTs on Ethereum L2 @base.

Cardholders can now create an onchain record of experiences and memories from international trips, blending loyalty rewards with digital ownership.

9/ The first tokenized S&P 500 Index Fund licensed by @SPDJIndices, SPXA, was launched by @centrifuge on Base.

10/ SWIFT and 30+ banks are designing a blockchain ledger to support tokenized assets and real-time, 24/7 cross-border payments alongside existing financial systems, starting with a prototype with Consensys.

@swiftcommunity connecting 11,500+ institutions globally will create a bridge between traditional finance and onchain value.

11/ @SocieteGenerale FORGE, an integrated subsidiary of the 161-year-old commercial bank, deployed EURCV & USDCV lending and trading on Ethereum DeFi protocols Morpho and Uniswap.

One of the largest custodians in Europe now provides institutional-grade collateral and liquidity for DeFi markets.

12/ @Stripe expanded its crypto support on Ethereum to include stablecoin-based subscriptions and recurring billing.

Hundreds of thousands of companies that use Stripe can now accept USDC for subscriptions with automatic renewals, building on Ethereum for lower-cost payments with near-instant settlement.

13/ @Securitize and @FGNexusio tokenized the FGNX stock on Ethereum, representing the first NASDAQ-listed preferred equity issued fully onchain.

Ethereum is the platform to build programmable assets that bring public markets to the digital age.

14/ @AntGroup, the fintech behind @Alipay, launched @JovayNetwork, a L2 for institutional tokenization.

The company behind one of the world's largest retail platforms is now building global institutional settlement for tokenized assets on Ethereum.

15/ @jpyc_official launched the world's first yen-pegged regulated stablecoin on Ethereum.

Complaint, programmable yen transactions are now available worldwide, backed 1:1 by yen reserves under Japan’s Payment Services Act.

16/ @BNYglobal and Securitize announced a tokenized AAA-rated CLO fund on Ethereum.

Institutional credit moving onchain brings liquidity and transparency to traditional asset classes.

17/ Google partnered with @Polymarket, integrating onchain prediction market data to Google search results.

The largest search provider now leverages the Ethereum ecosystem as a primary source of truth.

18/ @StartaleGroup released the Startale App, a SuperApp for @soneium's growing Ethereum L2.

Mainstream users in the Soneium L2 ecosystem can now access simple onchain interactions and rewards with a unified platform for wallets, assets, and apps.

19/ @jpmorgan migrated its tokenized deposit product, JPM Coin (JPMD), from its internal permissioned blockchain to Base.

Moving from a private chain to an Ethereum L2 will meet demand from JPMorgan’s institutional clients for payments, collateral, and margin settlement on public infrastructure.

20/ @Mastercard announced it will build on Ethereum L2 @0xPolygon to expand its Crypto Credential program to self-custody wallets.

Working with @mercuryo_io, the expansion will allow Mastercard users to send crypto using verified, human-readable aliases.

21/ @Amundi_ENG, Europe’s largest asset manager ($2.75T AUM), launched a tokenized share class of its euro money market fund on Ethereum mainnet.

Bringing traditional cash management onchain unlocks 24/7 settlement and composability for euro-denominated capital.

22/ Sony Bank announced plans to launch a USD-pegged stablecoin on @soneium, its Ethereum L2, in early 2026.

From gaming to finance, Sony is building its ecosystem’s home base on Ethereum.

23/ @WisdomTreeEU introduced the world’s first physically-backed ETP for @LidoFinance Staked Ether.

The fund will provide European investors with regulated exposure to the spot price of stETH and its ETH staking rewards.

24/ The @CFTC announced a pilot program that will allow ETH, BTC, and USDC to be used as collateral in US derivatives markets, alongside new guidance on using tokenized assets as collateral.

This marks a significant shift in how ETH and other digital assets can be integrated into regulated US markets.

25/ @BlackRock filed for a staked ETH ETF.

Following the success of their spot ETH ETF, this filing seeks to unlock the value of Ethereum's native staking reward rate for traditional investors.

26/ The @ADI_Foundation, backed by IHC, announced the mainnet launch of institutional L2 @ADIChain_, part of the @zksync Elastic Network.

Supported by the UAE's largest conglomerate, ADIChain will host the country's regulated stablecoins and aims to bring 1 billion people onchain across the Middle East, Asia and Africa.

27/ JP Morgan launched MONY, their first tokenized money market fund, on Ethereum mainnet.

The firm seeded the fund with $100M of its own capital, signaling their commitment to public chain tokenization.

28/ @coinbase announced Coinbase Tokenize, built on Base, as their new end-to-end institutional platform for tokenizing RWAs.

Combining issuance, custody, compliance, trading, and infrastructure, the new product will streamline the process of bringing assets like tokenized stocks, equities, funds, and real estate onchain in the Ethereum ecosystem.

29/ @RobinhoodApp added 500 tokenized assets on @arbitrum, bringing their platform to nearly 2000 assets tokenized.

With over $14M in total tokenized value, Robinhood continues deepening their integration with Ethereum’s L2 ecosystem.

30/ @BlackRock, @Mastercard, and @FTI_Global partnered with the ADI Foundation in the UAE, builders of the ADIChain L2.

The group will explore tokenized asset structures, digital asset regulatory frameworks, stablecoin settlement, and cross-border payment infrastructure.

31/ @SoFi became the first national US retail bank to issue a stablecoin (SoFiUSD) on a public, permissionless blockchain.

Launched on Ethereum, SoFiUSD will first be used for faster, cheaper internal settlements for the fintech giant and its partners.

32/ @telcoin launched eUSD on Ethereum and Polygon, a regulated U.S. dollar stablecoin issued by Nebraska state-chartered digital asset depository institution Telcoin Digital Asset Bank.

The launch marks another milestone in U.S.-regulated banks issuing stablecoins directly on public blockchains, bringing traditional regulated banking to the Ethereum ecosystem.

33/ @Grayscale distributed the first ETH staking rewards to ETHE ETF shareholders.

In a first for US regulated products, investors received Ethereum’s native yield directly, proving that staked ETH ETFs can deliver the economic utility of the network.

34/ @MorganStanley filed for a Staked Ether ETF, doubling down on its crypto strategy.

One of the world’s largest wealth managers is moving beyond spot exposure to capture Ethereum’s native staking yield for clients, signaling a shift to productive participation.

35/ The ADI Foundation partnered with M-Pesa to bring 60M+ users onchain.

Africa’s largest mobile money platform is integrating blockchain rails to power instant cross-border payments and stablecoin transactions, merging massive fintech scale with Ethereum’s global settlement layer.

—

Ethereum is the trusted, global settlement layer for real-world adoption, used by institutions, governments, and enterprises worldwide.

Learn more about building on the institutional liquidity layer: https://t.co/jUshBvAXKa

Why DCA works, and why you should be accumulating your favorite projects right now:

$TEL DCA results from Jan 18, 2021 to Jan 19, 2026:

💰 Total Invested: $61,000 (61 months × $1,000)

📊 Estimated TEL Holdings: ~20M tokens

💵 Current Value: ~$73,400

Current Price: $0.00367

📈 Profit: ~$12,400

Return: +20.3%

Monthly Purchases:

Jan 2021 | $0.00075 | ~1,333,333 TEL

Feb 2021 | $0.0031 | ~322,581 TEL

Mar 2021 | $0.015 | ~66,667 TEL

Apr 2021 | $0.015 | ~66,667 TEL

May 2021 | $0.040 | ~25,000 TEL

Jun 2021 | $0.028 | ~35,714 TEL

Jul 2021 | $0.018 | ~55,556 TEL

Aug 2021 | $0.021 | ~47,619 TEL

Sep 2021 | $0.016 | ~62,500 TEL

Oct 2021 | $0.019 | ~52,632 TEL

Nov 2021 | $0.016 | ~62,500 TEL

Dec 2021 | $0.012 | ~83,333 TEL

2022 (12 months) | avg $0.0030 | ~4,000,000 TEL

2023 (12 months) | avg $0.0015 | ~8,000,000 TEL

2024 (12 months) | avg $0.0032 | ~3,750,000 TEL

2025 (12 months) | avg $0.0055 | ~2,181,818 TEL

Jan 2026 | $0.0037 | ~270,270 TEL

Key insights:

• Started DCA on Jan 18, 2021

• Bought through the peak ($0.0647 ATH in May 2021)

• Accumulated heavily during 2022-2023 bear market

• DCA strategy paid off - profitable despite TEL being down 94% from ATH

The lesson: Dollar-cost averaging works. Buying consistently through the lows (2022-2023) made up for the high-price purchases during the 2021 bull run.

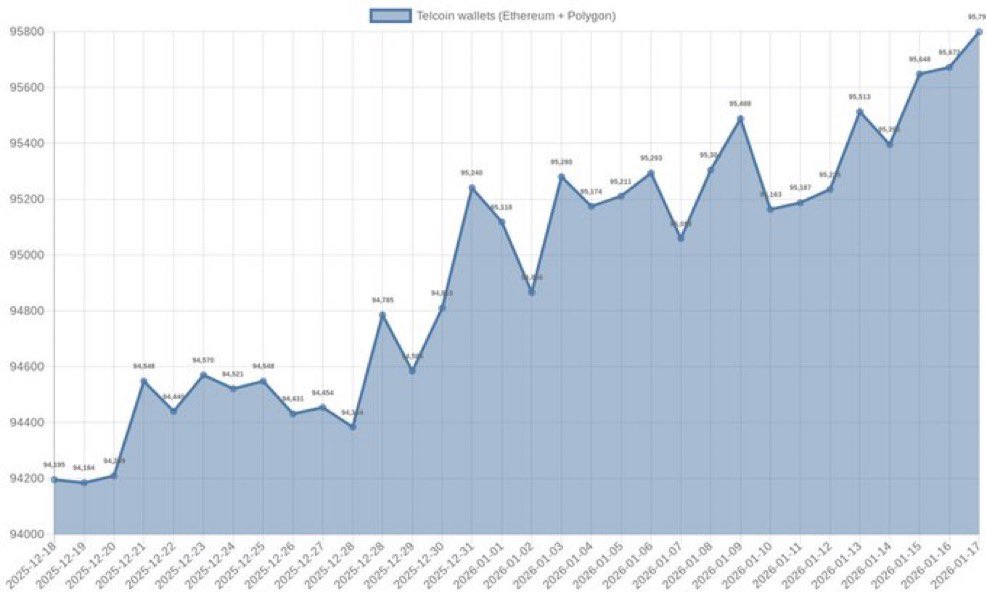

Why the retail holder count and supply constraints will shape $TEL’s trajectory

(TLDR: ~95B $TEL is circulating. ~70.8B is in retail wallets across chains. Exchanges hold a fraction. Wallet holders keep climbing. When the network is live and staking + burn begins, the liquid float tightens and creates real structural pressure.)

————————

There are ~95.08B $TEL circulating out of 100B total supply. Only ~5B is held in escrow or association reserves that aren’t tradable today.

According to on-chain holder data, ~99,300 wallets hold 70.81B $TEL, or about 76.5% of the circulating supply.

That means the bulk of what’s available is already in retail hands right now. A significant share (8.5b) of what’s left outside those wallets resides on exchanges or locked in SAFE/banking accounts. That’s a relatively small portion of the overall float.

There’s also approximately 3-5b held by exchanges.

That means theres approximately only 14-12B left for purchase.

Look at the wallet count chart. The number of holders is steadily rising. Sustained growth in holders is a signal of broadening distribution across unique wallets. More participants, wider base. It’s not explosive mania, but it’s durable accumulation. That trend itself doesn’t make price go vertical, but it narrows what’s actually available to trade.

With the network going live, staking becomes a thing. Tokens will move out of exchange or traveling wallets into staking, validation duties, and network operations. Those tokens become effectively out of liquid supply for long periods.

When staking demand grows, liquidity shrinks. That’s simple supply mechanics. Same supply with no sell pressure from unlocks, fewer tokens tradable. Higher competition among buyers for what’s left.

You don’t need leverage for this to matter. You need tightening float and increasing demand from real usage and participation.

The most interesting part is this: retail holders hold the majority now, exchanges hold relatively little, and a lot of the non-retail supply is budgeted out for the next 10 years, mostly for rewards for stakers and LP. As network participation ramps and more $TEL gets committed to staking and validation, the liquid float will shrink further.

That’s how structural pressure builds into price behavior over time as adoption and network usage climb.

(Chart credit: @telcoinnews )

@telcoin Digital Asset Bank already operates under clear state law. The CLARITY Act and the GENIUS Act don’t make TDAB legal - it's already legal and operating - it makes TDAB easier to recognize, interact with, and scale outside Nebraska.

Nebraska’s digital asset bank statutes establish legality, supervision, and permissible activities at the state level. this also was the first government structure to build this out in its entirety. TDAB exists because that law already exists (they helped write it). What the federal bills do is reduce the friction that normally appears once a state-chartered digital asset bank tries to plug into the national system (fed rails).

The CLARITY Act primarily addresses classification and jurisdiction. By drawing clearer lines between digital commodities, securities, and payment assets, it reduces the chance that a federally supervised counterparty treats a state-chartered digital asset bank as a regulatory unknown. That matters even when the underlying activity is already lawful at the state level. Less classification ambiguity means fewer internal vetoes at large banks, payment processors, and enterprises.

The GENIUS Act focuses on payment stablecoins and reserve-backed issuance. TDAB does not need GENIUS to issue or custody digital assets under Nebraska law. What GENIUS does is standardize expectations around reserves, redemption, disclosures, and oversight at the federal layer. That alignment makes a state-chartered bank’s stablecoin activity easier to integrate into national payment and settlement workflows without custom legal analysis every time.

In other words, state law answers “can this bank exist and operate?”

The CLARITY and GENIUS Acts help answer “can everyone else safely interact with it?”

At the state level, TDAB already benefits from statutory clarity: predictable exams, defined asset treatment, and a known supervisory regime. Federal clarity doesn’t replace that. It removes the incentive for counterparties to second-guess it.

This is why the absence of a federal charter isn’t a weakness here. State-chartered banks have always relied on a combination of state authority and federal overlay. These bills simply make that overlay more explicit for digital assets instead of leaving it to enforcement risk and interpretation.

The net effect is leverage, not permission. Nebraska law establishes the bank. The CLARITY Act reduces classification friction. The GENIUS Act reduces payment and stablecoin friction. Together, they turn a state-level digital asset bank from a local certainty into a nationally legible one.

No regulatory roulette. No retroactive punitive measures. Just fewer excuses for counterparties to say no.

$TEL

if @telcoin is able to get the bank up and fully operational by Q1 2026 and the latest $XRP ETFs going live this week doesn’t positively effect the XRP price over the next few months, I believe we will start to see an inflow of $XRP holders into $TEL.

I hold both tokens by the way 🫡