The first thing I ever talked about months ago?

#Optics.

How many times did I repeat it?

Enough that if you ignored it… that’s on you.

Its not just that any name works! Fundamentals, valuations and technicals must all embrace each other 🤗. Because if you treated stock picking like picking a life partner 😂— not a one-night stand — you’d be sitting on some very serious money by now.

Now here’s where it gets interesting:

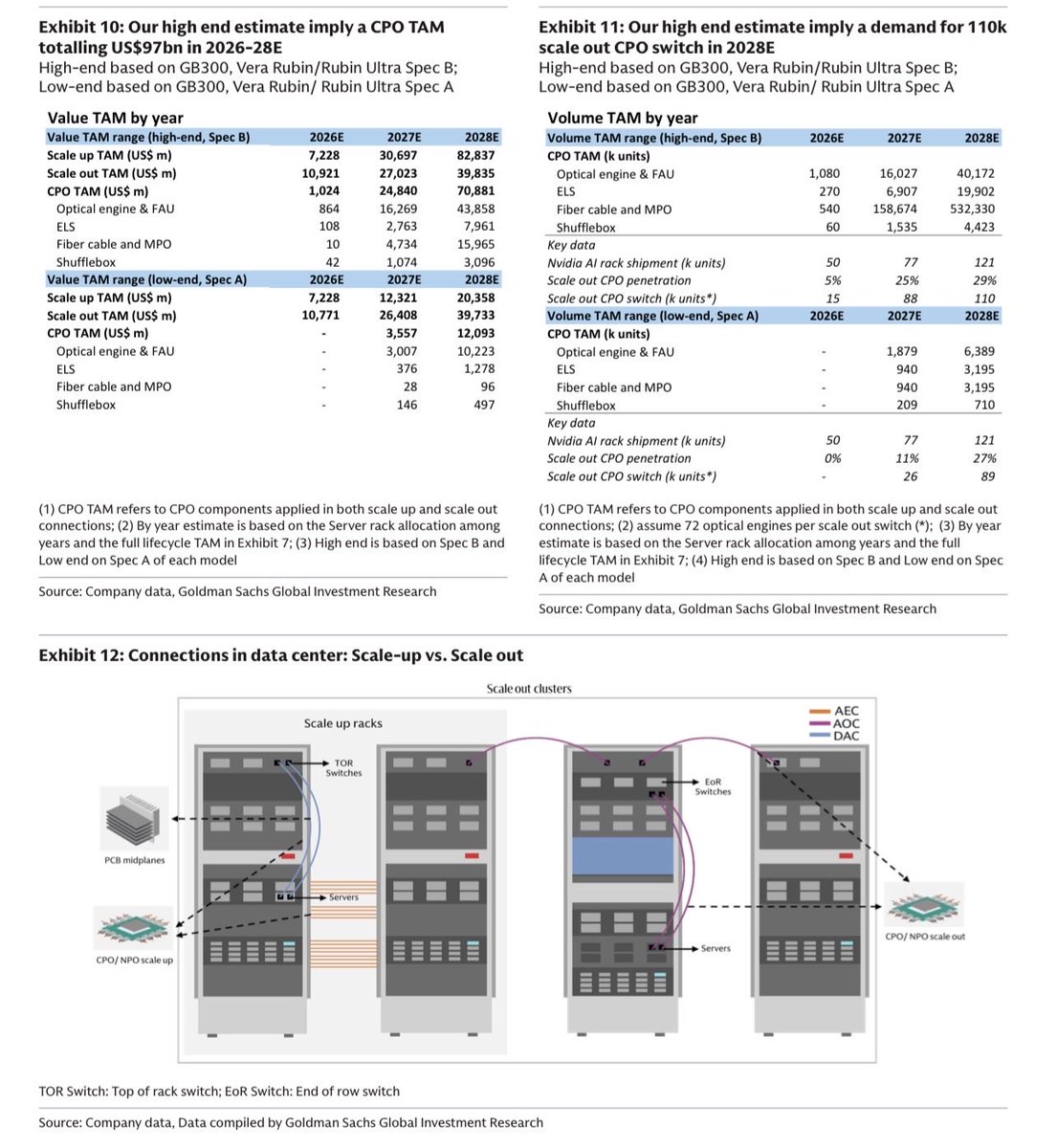

Goldman Sachs just dropped projections on optical networking… and they’re not normal.

📈 Total Addressable Market:

From $15B → $154B (that’s a 9x expansion)

💡 And the real kicker?

CPO (Co-Packaged Optics) alone = $91B

Let that sink in for a second.

This is infrastructure-level transformation.

The Federal Reserve is designed to fight “demand-driven inflation”—not supply shocks. A war-driven spike in energy prices does not reflect overheating consumer demand, and higher interest rates cannot increase oil production or reopen disrupted supply routes. #cpi

🚨 Don’t Misread Today’s KOSPI Drop

The KOSPI isn’t predicting tomorrow’s US market—it’s catching up to Friday’s selloff.

🇺🇸 Friday: US tech and memory stocks fell sharply.

Weekend: Markets were closed.

🇰🇷 Monday: South Korea opens and prices in the same move, with Samsung and SK Hynix leading the decline.

The US market is ahead in this cycle, not behind it.

Today’s #KOSPI weakness is less a new warning sign and more an echo of Friday’s US selloff

Goldman Sachs just dropped a 34-page report for Institutional clients validating everything we’ve been saying about the #Copper Wall thesis. We are already up triple digits long ago. Here’s what matters:

> 💡 THE ONE NUMBER

$154 BILLION

That’s the optical networking TAM Goldman projects by 2028.

Up from $15bn today. A 9x expansion in under 3 years.

> 📐 THE THREE STATS TO SCREENSHOT

▸ 16x / 45x — dollar content increase per rack (Scale Out / Scale Up) from today’s GB300 to Rubin Ultra

▸ 13x — larger TAM for optics as they expand from Scale Out into Scale Up

▸ 10x — more pluggable optical module value per rack, even after CPO takes 29% share

The biggest investor fear — CPO killing pluggables — is answered. Both grow. The market expands faster than CPO can cannibalize it.

> 🗺️ THE ROADMAP (SIMPLE VERSION)

GB300 (Now) → $315k/rack

Vera Rubin 2027 → $504k/rack (+60%)

Rubin Ultra 2028 → $1.17BN/unit (+3,600%)

That last number isn’t a typo. One Rubin Ultra computing unit = 8 racks × 72 GPUs. The networking content alone crosses $1 billion per unit.

> 👁️ THE SLEEPER CALL: OCS

#Optical Circuit Switch — most investors aren’t talking about this yet.

•No optical-electrical-optical conversion needed

•Speed agnostic: same switch handles 800G, 1.6T, 3.2T

> 📌 BOTTOM LINE

Goldman Sachs just told their institutional clients what we’ve held since the thesis was called fringe:

Optical networking is the next mega trend in AI infrastructure. Dollar content per rack is going up 29x. The TAM is going to $154bn. All configurations grow.

📡 AI INFRASTRUCTURE — 5 BULL PILLARS

Goldman Sachs published a major framework this week on the scale of the AI build-out. Here are the five structural reasons I'm bullish on AI infrastructure as an investment theme.

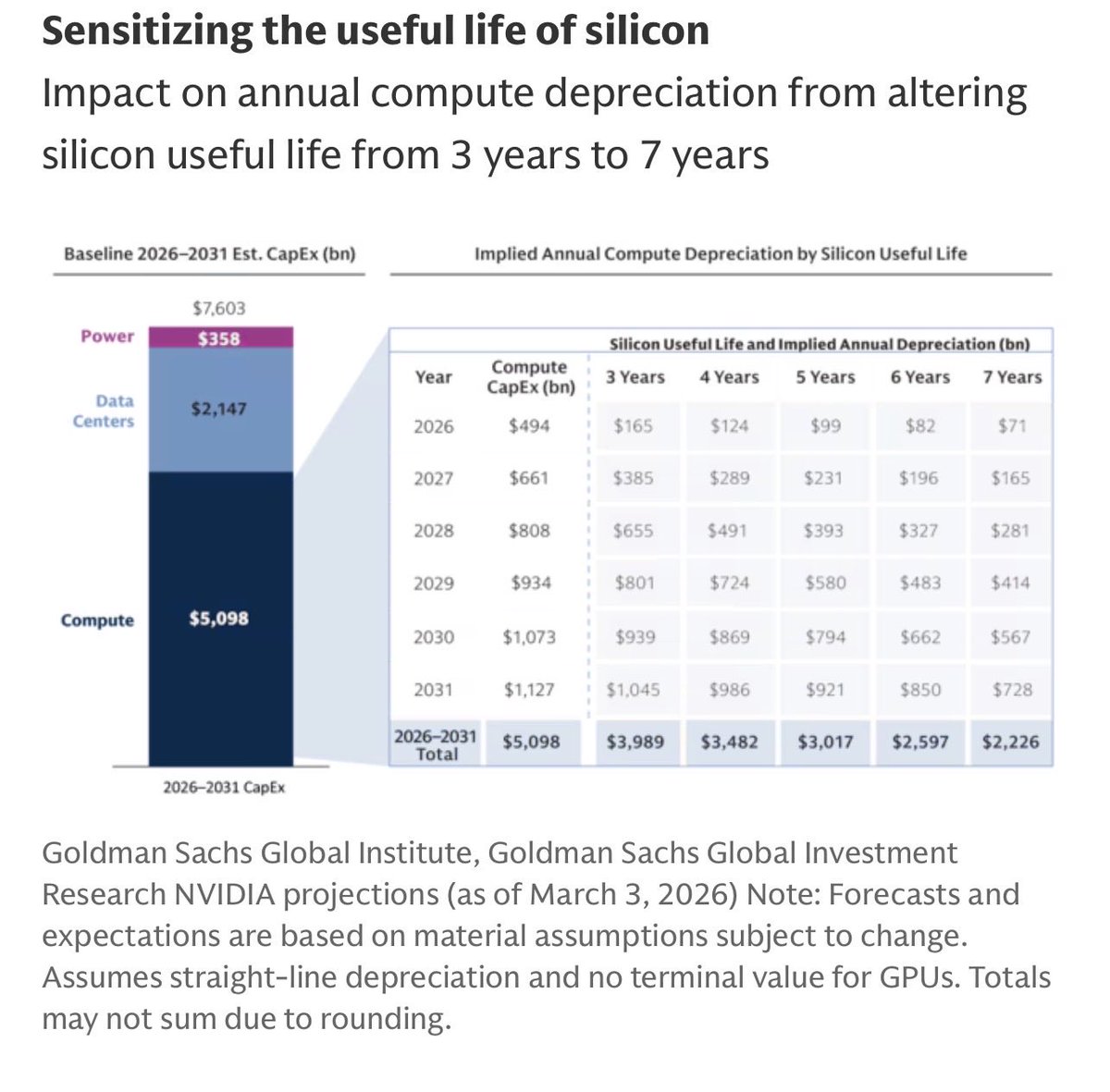

1. The floor is $7.6 trillion — and it's already committed

This isn't speculative demand. $765 billion in AI infrastructure spend is locked in for 2026 alone, rising to $1.6T annually by 2031. Hyperscalers have signed power offtake agreements, placed equipment orders, and committed capital budgets years in advance.

You're not betting on whether #AI works. You're betting on whether the physical machine that runs it gets built.

It does.

2. Cheaper compute = more compute, not less spend

The most important structural insight in the GS report — and the one most investors get wrong.

When chips get cheaper, buyers don't spend less. They buy more compute and run bigger models. GS calls this elastic demand.

It means every efficiency gain — every DeepSeek-style breakthrough — is fuel for more infrastructure spend, not a reason to pull back. The debate about cheaper AI chips deflating the sector? It reshapes who earns the margin. It doesn't shrink the total spend.

3. Nvidia's upgrade cycle is a structural force — not a trend

Nvidia releases an entirely new GPU architecture every single year. Each generation delivers step-function leaps in performance — not incremental improvements.

This forces a 3–4 year replacement cycle across every data center on the planet. It's the single biggest lever on cumulative AI capex, and it's structurally short. The accounting may say 5–6 years of useful life. The economics say otherwise.

The replacement machine never stops.

4. The copper wall — bandwidth that physics cannot solve

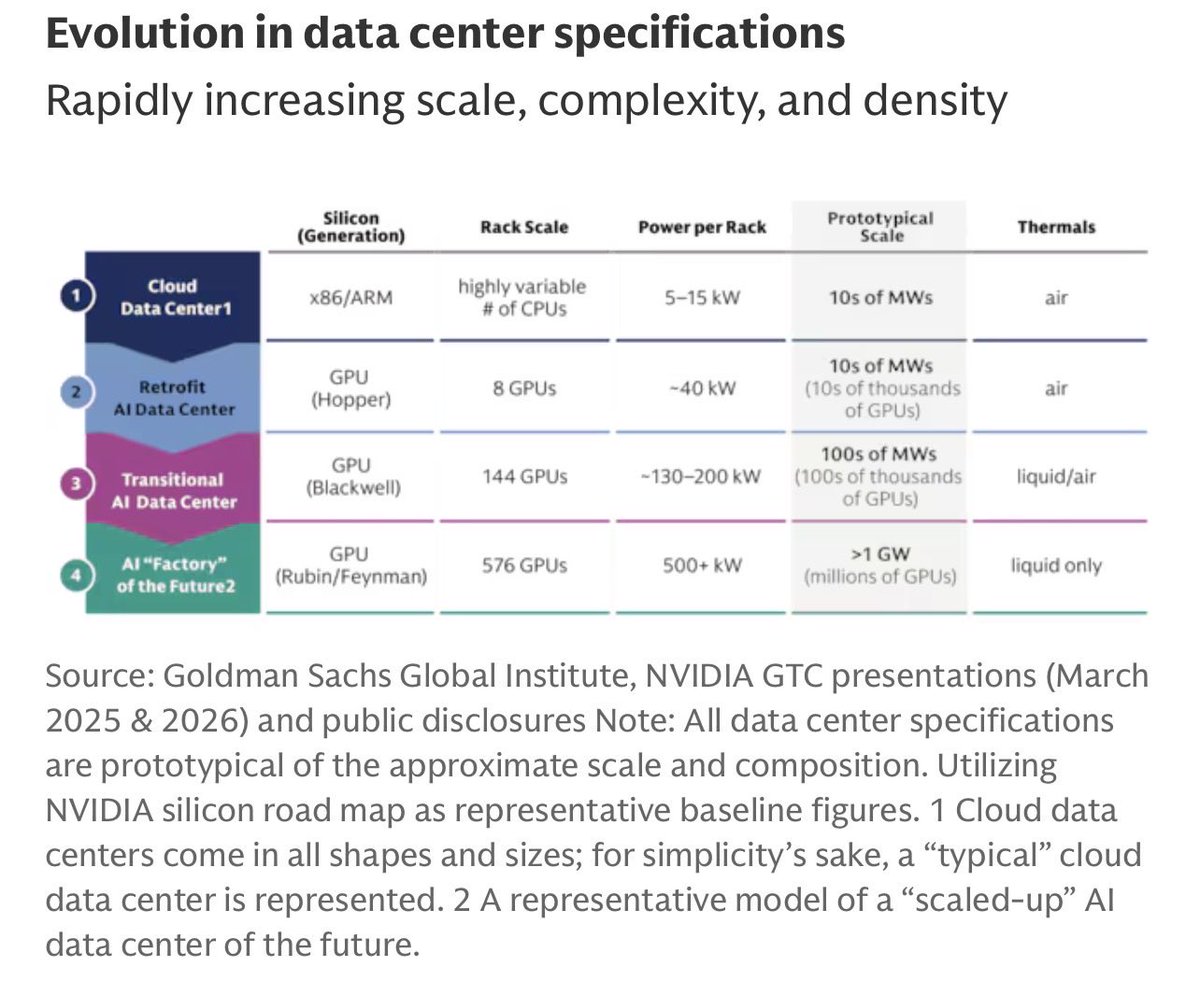

Today's AI racks pack 72 GPUs drawing 3,000 watts per package. At that density, copper cables physically cannot carry the bandwidth required between chips, racks, and data centers.

Optical transceivers — fiber-based interconnect — are the only solution. And the supply chain for these components is already tight. GS explicitly flags optics in what it calls the "buy out the store" dynamic: intense, lumpy demand hits a supply chain that takes years to expand.

This is the copper wall. It's a physics constraint, not a market cycle.

5. Bottlenecks protect pricing — for years

Power grid queues. Transformer lead times. Specialized labor shortages. Permitting delays.

These constraints don't reduce the total amount of infrastructure being built — GS is clear on this. They stretch timelines. And for the suppliers of constrained components, stretched timelines mean sustained pricing power well beyond what historical cycles would predict.

The companies that make the scarce things — power generation, specialty components, optical modules — are not victims of the bottleneck. They're the beneficiaries of it.

💡 The one-line thesis:

The $7.6T is the floor, not the ceiling. The physical infrastructure of AI is not optional, not deferrable, and not subject to the demand debate in the near term.

The machine is being built.

🛢️ The Day the Oil Cartel Cracked: UAE’s Exit Is Bigger Than You Think

The oil market didn’t just move today — it structurally shifted.

🔎 What Just Happened (The Facts)

The United Arab Emirates has officially announced it will leave the Organization of the Petroleum Exporting Countries and OPEC+ effective May 1, 2026, ending more than five decades of membership.

This comes at a highly sensitive moment:

* A global energy shock driven by the Iran war

* Disruptions to critical supply routes like the Strait of Hormuz

* Rising internal tensions within OPEC, particularly with Saudi Arabia

👉 In short: this is not timing coincidence — it’s strategic.

🧠 Why This Matters (Beyond Headlines)

1) A Direct Hit to OPEC’s Power Structure

The UAE isn’t just another member — it’s one of the few producers with meaningful spare capacity, a key lever OPEC uses to influence prices.

Without it:

* OPEC’s ability to control supply weakens structurally

* The cartel risks losing its role as the global oil “central bank”

2) From Coordination → Competition

The UAE explicitly framed this as a “strategic” shift tied to its future capacity and national interest.

Translation for markets:

* No more quota constraints

* Freedom to increase production independently

* Potential shift toward market share competition

👉 This is how price wars begin — quietly.

3) Geopolitics Is Driving Energy Policy

This move is deeply political:

* Frustration over regional security support amid Iranian tensions

* Growing divergence with traditional allies

* Realignment toward sovereign decision-making over cartel discipline

👉 Energy is no longer just economics — it’s strategy.

📉 Market Implications (What Investors Should Watch)

🛢️ Oil Prices

* Short-term: Volatility spikes (supply uncertainty + war dynamics)

* Medium-term: Downward pressure if UAE ramps output

* Long-term: Weaker price floors due to fragmented coordination

📊 Equities & Inflation

* Lower oil = disinflation tailwind

* Eases pressure on central banks like the Federal Reserve

* Potentially bullish for equities (especially rate-sensitive sectors)

🌍 Global Power Shift

This is the real story:

The world is moving from cartels → capacity competition

* National interest > collective discipline

* Supply becomes less predictable

* Volatility becomes structural, not cyclical

⚠️ The Signal Most Are Missing

This isn’t just about oil.

It’s about:

* The decline of coordinated global control mechanisms

* The rise of independent economic blocs

* And a future where pricing power is earned, not negotiated

🎯 Bottom Line (Investor Lens)

* OPEC just lost cohesion

* The UAE just gained flexibility

* Markets just inherited more uncertainty

👉 And in markets, uncertainty is where alpha is created — or destroyed

#OilMarkets #OPEC #UAE #EnergyCrisis #MacroStrategy #Geopolitics #Investing #Commodities

SK Hynix just delivered a statement quarter.

Record-breaking 1Q26 performance:

₩52.58T in revenue.

₩37.61T in operating profit.

Not just growth — dominance.

Powered by next-gen HBM and eSSD solutions, SK Hynix isn’t riding the AI wave… it’s engineering its foundation.

From silicon to systems, they’re positioning themselves as a true Full-Stack AI Memory Creator — quietly becoming one of the most critical enablers of the global AI ecosystem.

In this cycle, memory isn’t a component.

It’s the bottleneck.

And SK Hynix is holding the key.