$SLNH @jbelizaireCEO sharing this @WSJ article is worth paying attention to.

The article is not about @SolunaHoldings directly, but it validates almost every major theme behind the Soluna thesis.

WSJ’s core message is that America’s data-center buildout is falling behind schedule, even while hyperscalers are throwing unprecedented amounts of capital at AI infrastructure.

According to the article, supply-chain backlogs, permitting fights and power availability are delaying data-center construction. JP Morgan found that more than 60% of planned 2027 data-center capacity is still not under construction, with another 7% already delayed.

The AI race is no longer only about who has the biggest capex budget.

It is about who can actually secure power, get connected, manage grid strain and bring capacity online fast.

WSJ also notes that @Microsoft, Alphabet, @Meta and @amazon collectively spent $410B on capex last year and are expected to spend more than $670B this year. @Google alone is now raising $80B for data centers.

But even that kind of money does not automatically solve the bottleneck.

Power is the bottleneck.

Grid approval is the bottleneck.

Transformers, turbines, permitting and interconnection are the bottlenecks.

That is why the line John highlighted matters:

“Having on-site power is becoming a strategic advantage for tech companies.”

That is basically the Soluna model in one sentence.

Build where power already exists.

Build near generation.

Use behind-the-meter structures.

Reduce dependence on congested grid queues.

Create flexibility around how compute loads interact with the grid.

The article also explains that Google is moving closer to the power layer. Google acquired Intersect for $4.75B, a wind and solar developer with projects intended to support data centers. It is also investing in demand response and load shifting, including a three-year agreement with Voltus that could create up to 100MW of flexible capacity in PJM.

That is very important.

The largest tech companies are no longer treating power as a utility bill.

They are treating power as strategic infrastructure.

That is where Soluna already sits.

Kati 2 fits directly into this trend: Las Majadas wind, ERCOT access, grid flexibility, potential on-site generation, gas optionality, solar, BESS and grid-stability solutions.

Dorothy / Briscoe adds another layer because Soluna now controls power generation directly at one of its key campuses.

The market is slowly waking up to a simple reality:

Not all MW are equal.

Capital without power is not enough.

Land without grid access is not enough.

A data center plan without a realistic path to energization is not enough.

The winners will be the companies that can combine power, location, flexibility, speed and bankable execution.

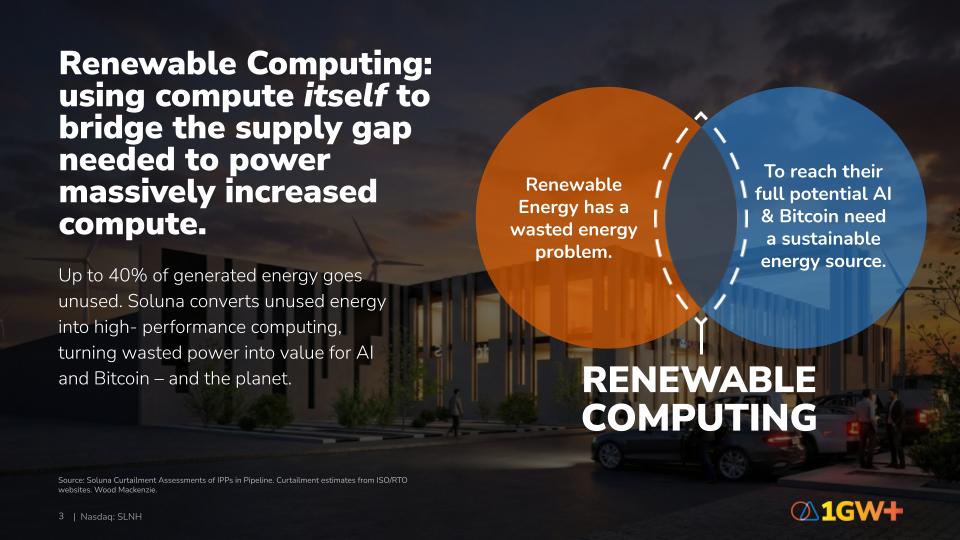

What if the energy that couldn't be absorbed by the grid became the foundation for AI infrastructure?

$SLNH CEO John Belizaire joined Brightsmith's Conversations in Cleantech to discuss exactly that —

Curtailed renewables, co-located data centers, and the economics of building compute infrastructure at the generation source.

Listen to the full conversation: https://t.co/4W5GEtH8rY

In a recent AMA, the new $SLNH CFO Michael Picchi (who appears to have just purchased 100,000 shares on the open market a week ago) provided a major update on Project Kati 2 indicating it could potentially expand into a giga-campus (1GW+).

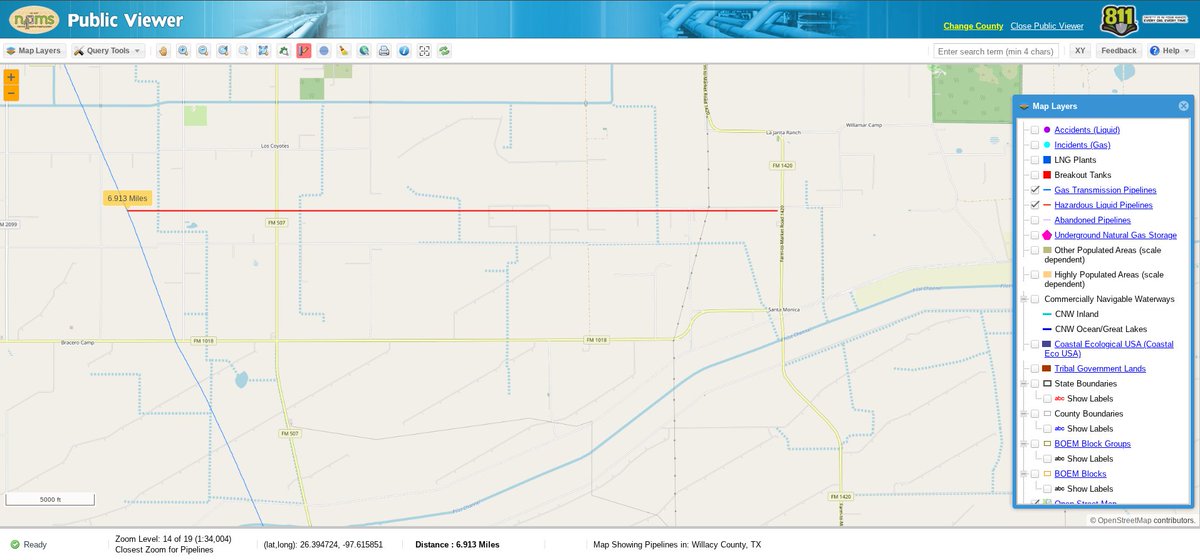

If you've researched Project Kati, you know it's on the southern tip of Texas (close to Starbase) and major natural gas infrastructure.

Additionally, $SLNH also appears to have Projects Ellen and Hedy nearby which could potentially be clustered into the Project Kati mega-campus.

I've included an image showing the distance of Project Kati to the nearest natural gas pipeline and another one with the distance of Project Kati to Projects Ellen and Hedy. I had to pull coordinates and still need to confirm these are accurate locations/distances.

I plan to ask the CEO of $SLNH more detailed questions about this site in our upcoming interview.

$SLNH CEO John Belizaire and CFO Michael Picchi joined the @power_analys1s podcast to discuss Soluna’s Q1 results, the company’s AI strategy at Project Kati 2, and answer some of the biggest questions we’ve been hearing from investors.

Watch the full episode here: https://t.co/VZyoazctTo

@jbelizaireCEO@cazenove_uk@McnallieM2

Congress just handed one company a legal monopoly on U.S. military optics.

Almost nobody has noticed.

$LPTH (LightPath Technologies) — ~$871M market cap.

---

**The trigger**

China controls the vast majority of global germanium refining — the material inside every U.S. military thermal imaging system. In 2023, China imposed export controls, driving a 65% price surge.

Congress responded with the FY2026 NDAA: a hard January 1, 2030 deadline requiring complete elimination of adversary-sourced optical components from all U.S. military platforms.

Every major defense prime must redesign their optical systems.

One domestically produced, NDAA-compliant, germanium-free infrared glass is qualified at scale.

LightPath's BlackDiamond™ — compounded entirely at ITAR-registered U.S. facilities.

---

**Why BlackDiamond™ wins**

Germanium's refractive index shifts with temperature, causing defocusing requiring heavy mechanical correction or cryogenic cooling.

LightPath's BDNL-4™ — exclusively NRL-licensed — has a *negative* thermo-optic coefficient. Pair it with a positive dn/dT lens and thermal shifts cancel passively. No motors. No cooling. No weight penalty.

BD6™ transmits across SWIR, MWIR, and LWIR in a single element — previously three separate systems. And unlike germanium, BlackDiamond™ is Precision Glass Moldable — high-volume, scalable, dramatically cheaper.

---

**The moat**

Exclusive rights to 14 chalcogenide glass compositions from the Naval Research Laboratory. No competitor can access them.

- Phase 1: Three formulations qualified — already replacing germanium in active programs of record

- Phase 2: Six more being qualified to MRL-9 — full high-rate production readiness

Once qualified into a defense program, a material stays for the program's entire lifecycle.

---

**Three acquisitions built the complete stack**

**Visimid (2021):** Phoenix FPGA engine — turned LightPath from component supplier into systems integrator.

**G5 Infrared (Feb 2025, $27.1M):** Long-range cooled MWIR cameras. G5 booked $100M+ in new orders since acquisition — triggering GAAP earnout revaluation, creating $12.2M in non-cash charges YTD that mask real profitability.

**Amorphous Materials (Jan 2026, $7M):** Expanded maximum optic diameter from 5 to **17 inches** — unlocking space-based payloads. Already supplies glass for the F-35 targeting system and Apache Arrowhead sensor suite.

---

**Defense programs already won**

- **Lockheed NGSRI (Stinger Replacement):** Sole-sourced. Flight tests successful. 10,000 units/year at full rate. **$50M–$100M annual revenue** over 10 years.

- **Air Force SEWADS (Counter-UAS):** $30M backlog. EdgeIR™ runs Hailo-8 AI at 26 TOPS — processes video locally, transmits only target coordinates. Unjammable.

- **L3Harris Shipboard Threat Detection:** Sole-sourced. 10-year program. $10M–$20M/year.

- **Elbit Border Surveillance:** 85–90% win probability. $20M CY2026 bookings. 14-year cycle.

- **Golden Dome (Space Satellites):** Three aerospace primes in active design review. ~$16M per satellite payload.

---

**The financials**

Q3 FY2026:

- Revenue: $19.1M — up **109% YoY**

- Assemblies & Modules: up **355% YoY**

- Gross margin: 36%, targeting 40%

- Third consecutive positive adjusted EBITDA quarter

- Record backlog: **$110.6M** — up 196% in one fiscal year

- Cash: $55.2M — up from $4.9M nine months prior

- GAAP net loss of $4.1M — almost entirely non-cash earnout revaluation

Every quant screen sees a loss-making small-cap. The loss is a direct function of G5 booking $100M+ in orders — the better the business performs, the worse the income statement looks.

That disconnect is the entry point.

---

Priced as a commodity optics company.

It is the domestic infrared monopoly the entire U.S. defense industrial base is legally mandated to use by 2030.

The deadline doesn't move. The alternatives don't exist.

---

*Not financial advice. Do your own due diligence.

Soluna has completed full equity ownership of the Dorothy 1 campus.

Briscoe Wind Farm. Dorothy 1A. Now Dorothy 1B.

150 MW of owned renewable power. 50 MW of fully consolidated compute. One ownership chain, end-to-end.

Dorothy 3 AI campus development moves forward on our terms.

Full details: https://t.co/XXh4YRoDY7

$SLNH

We underestimated $SLNH.

Soluna beat EPS... significantly (-$0.24 vs -$0.62). This is the largest EPS beat in $SLNH's history.

Revenue is up significantly as well (~59% YoY). Data hosting revenue more than doubled YoY.

The pivot to renewable powered AI infrastructure is working... the entire thesis is playing out.

Cash position of $86M, much stronger than what bears were worried about.

The one downside? Their net losses increased from overhead growth/G&A expenses.

The company is expected to announce its next earnings report in August, with analysts projecting an EPS of $0.

They're already pricing in the transition from burning cash to operationally sustainable. This is huge.

But what they're building behind the scenes is what's interesting... which'll also catalyze a rally upon fruition.

Kati 2 (350 MW AI campus) is progressing fast in the design stage, while Dorothy 3 (owned outright) development stage is advancing.

Once construction begins, you'll start seeing the valuation gap fill start to happen. We are very early.

Any volatility we see should be extremely short-lived. Might get the perfect opportunity to enter on a pullback...

We just wrapped one of the most active quarters in $SLNH history 🚀

Q1 2026 highlights:

→ 147 MW under management, up from 123 MW

→ Bitcoin hosting revenue up 178% year over year.

→ Revenue up 58% YoY; 4 consecutive quarters of growth.

→ Hash rate exceeding 7 EH/s, a new company record.

→ A 4.3 GW power pipeline that keeps compounding.

But the bigger story is what we're building toward...

(1/2)

$SLNH was probably my most asymmetric pick so far this year.

It’s up by 21% today and 132% this month.

The market is just waking up, there is still way to go as power is now the biggest bottleneck for scaling AI and $SLNH has it.

It has 350 MW data center capacity under development in Project Kati 2 with behind-the-meter renewable power and ERCOT grid access.

This is a JV with Metrobloks.

Assuming $1.5 million/year per MW from a single-tenant, they can generate $525 million revenue from this site alone.

Even if we assume 50/50 revenue share, $SLNH will generate $262.5 million revenue from this site.

It has under 300 MW under development in Project Dorothy 3. Based on the same assumptions as Kati 2, this site can generate $450 million revenue.

In total, these two sites combined can generate $712.5 million additional revenue from AI/HPC tenants.

The whole market cap is currently $350 million and it will still have +3.5 GW of pipeline after these two projects.

Long $SLNH.

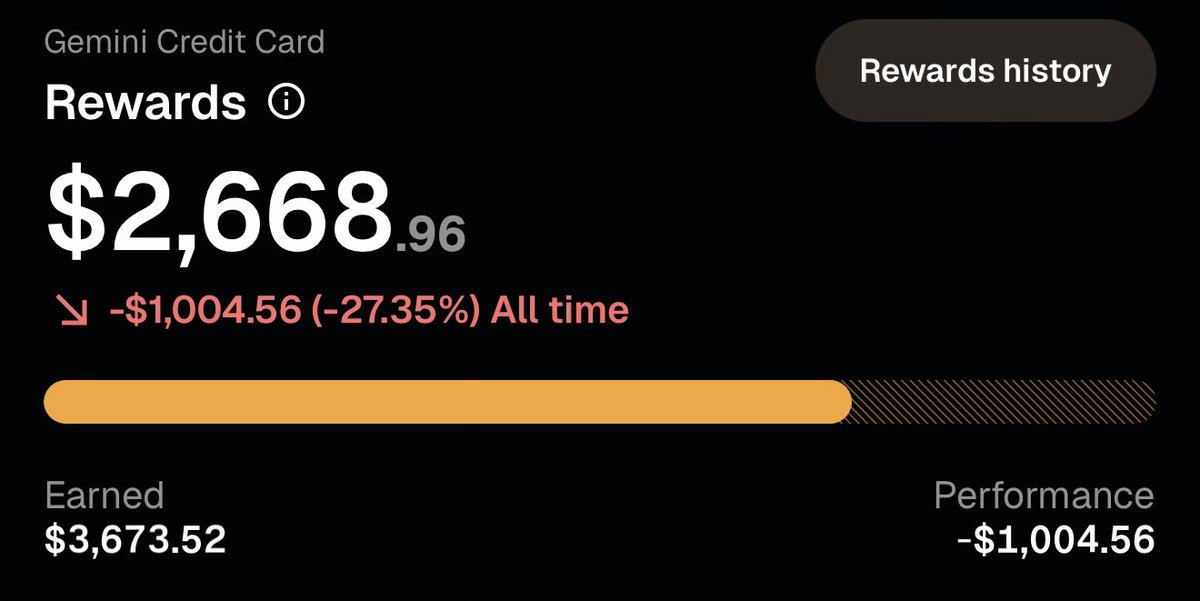

Gemini has paid me $3,673.52 in Bitcoin from their credit card for FREE.

I know it’s down 27% FOR NOW, but eventually, this Bitcoin will be worth tens of thousands of dollars.

Starting to slowly average up in SLNH. Tyler Page's comments on Tuesday really solidified my view that behind the meter power generation is going to be a key part of the long term story here. SLNH is well positioned for this at a very low market cap. High asymmetry possible.

Funny moment from our recent Kati 2 AI design kickoff in southeast Texas.

During the visit, we gave the design team a tour of the Kati 1 BTC control room.

On the main MaestroOS™ screen, they saw the live all-in power price Kati 1 was experiencing at that moment.

One HPC design engineer paused and said:

“Is there a bug? That can’t be $2X/MWh. You mean $2X0/MWh, right? It's missing a zero no?”

We told him:

“No bug. That’s the Soluna Way.”

Our model is built around locating computing infrastructure where power can be abundant, flexible, and cost-advantaged.

Renewable Computing™ in action.

We Keep Pushin’.

$SLNH @SolunaHoldings

(@cazenove_uk, @disruptorinvest, @McnallieM2)

Seattle passed a 365-day moratorium on new data centers. The concerns are legitimate.

The fix isn't better PR. It's building where the power already exists, not on top of the communities that need it.

That's Renewable Computing. That's what we do.

$SLNH

I’ll take it… 5% pullback on $SLNH after back to back ~30% days. Completely reasonable (for a microcap) and very healthy. Nothing goes straight up without coming straight down.

Back to where we started the day in AH. Being bullish pays well. See you next week.

$SLNH

Kati 2 was originally an 83 MW project that got upsized to 100 MW and then to 350 MW in partnership with Metrobloks.

It’s likely that potential tenants require a larger capacity to move the needle for them.

Then they have 300 MW under development at Project Dorothy 3.

So, you are looking at roughly 650 MW capacity under development.

At the current industry rates ($1.5 million/year per MW) it can generate $975 million revenue.

Kati 2 is a JV, so assuming 50/50 revenue share, $SLNH can generate $712.5 million from these sites alone.

Even if it can achieve 1/3 of this, we are looking at $237.5 million revenue add.

Market cap is $240 million today.

Definition of an asymmetric bet.