Founder & Principal Analyst, Beat Billions Research | Institutional-Grade Equity Research & Intelligence for Asset Managers, Family Offices, and Web Platforms

Mark, with all due respect — the UAE doesn’t need a permission slip from Washington to conduct its foreign policy. The UAE has 3 islands illegally occupied by Iran, a shared maritime border, and billions in bilateral trade exposure. Managing that reality isn’t “coddling” — it’s called statecraft, something that requires nuance beyond a cable news monologue.

The UAE stood firmly against Iranian proxies, hosted the US Fifth Fleet’s logistics, signed the Abraham Accords, and has been one of the most consistent partners in regional stability. If pragmatic diplomacy reads as weakness to you, perhaps the question is whether your framework is equipped to understand a region you’re watching from 7,000 miles away.

Frustration is understandable. Oversimplification, however, is not analysis.

$PFE faces a few challenges.

The patent cliff threatens to wipe $17 billion in annual revenue.

Investor trust in the management seems shaky.

There’s blood in the streets.

But the strength of the Launched and Acquired portfolio seems under appreciated.

Read my full analysis here: https://t.co/2KQORfPnTS

$AAPL price hikes are here.

As I noted in a post last week, historically, price hikes have worked really well for Apple. But these prices hikes are on another level.

We'll see more about Apple's pricing power (or lack thereof) in the coming quarters.

In Q1, $BKNG confirmed that payments revenue boosted total revenue growth.

But I think the more important thing to watch is not just the direct revenue Booking gets from payments, but the indirect revenue potential.

The payment platform can become a bigger enabler of Booking’s connected-trip strategy over time. If Booking can handle more of the transaction layer itself, it has a better chance of creating a smoother, more integrated travel experience across accommodations, flights, rental cars, attractions, and other trip components.

That matters because connected trip is more of a behavior-change story than a product story, IMO.

Travelers do not automatically consolidate their entire trip with one platform. Booking has to give them a reason to do so. Payments can help by reducing friction at checkout, improving consistency across suppliers, supporting cross-sell opportunities, and giving Booking more control over the customer experience after the initial booking.

Although payments revenue is the visible benefit in the short run, the bigger prize could be the incremental travel demand that becomes easier to capture when payments make the broader trip easier to stitch together.

If the payment platform keeps scaling, I do not want to view it only as a standalone monetization lever. I want to understand whether it is quietly improving Booking’s ability to grow connected-trip adoption, increase attach rates, and capture more wallet share per traveler over time.

For $BKNG, that second-order effect could matter more than the payment revenue line itself.

Last week, $AAPL CEO Tim Cook told the WSJ that price hikes are inevitable. The official narrative is to pass on cost inflation to consumers.

But the more interesting question is whether Apple uses this cost cycle as cover for a more durable iPhone pricing reset.

That would not be without precedent.

In 2017, Apple introduced the iPhone X at $999, which was a major psychological jump at the time. The market initially debated whether consumers would accept that price point, but in hindsight, Apple effectively moved the premium smartphone ceiling higher.

The result was not just a one-time expensive model. It helped reshape the iPhone mix and lifted the long-term ASP framework for the business.

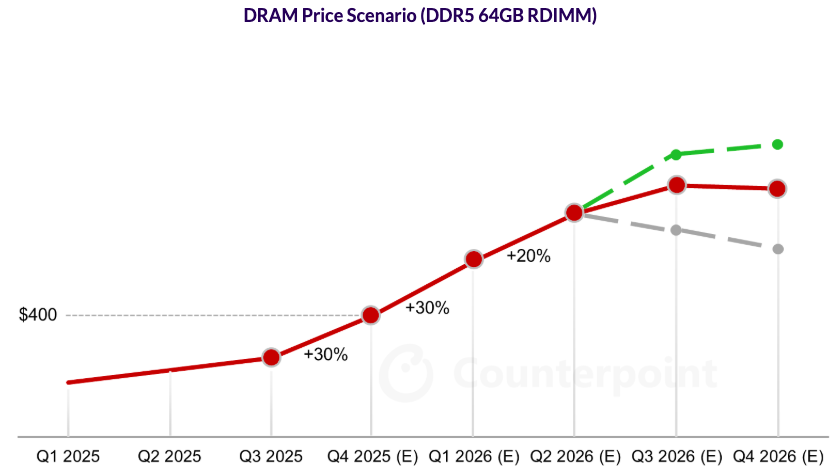

I think the current memory cycle could create a similar opportunity.

If mobile DRAM and NAND prices continue rising, Apple has a very clean external reason to push pricing higher. Consumers may not love it, but “input costs are up” is an easier message to sell than “we are expanding margins.”

Apple does not need every customer to upgrade immediately. It needs enough high-end buyers to accept a higher price architecture, especially around Pro models, storage tiers, and AI-capable devices.

Storage is particularly important here.

Apple has historically monetized storage upgrades extremely well. If underlying storage costs rise, Apple can raise device prices or push users toward higher-priced configurations while still preserving the perception that the increase is tied to real cost inflation.

The market may initially frame this as a gross margin headwind.

My take is that it could become an ASP tailwind over time.

I believe Apple will treat this as a strategic reset of the iPhone pricing ladder.

This is how Dubai operates. 🇦🇪

A resident reported a tree branch blocking the street. 24 hours later, the municipality cleared it.

Efficient, responsive, and zero excuses. That’s what sets this city apart. 👏

$ACHR has been a part of my portfolio for ~2 years.

The biggest challenge I see for the company is scaling manufacturing.

I don't think more partnership announcements will move the stock higher. Investors need to see progress on the manufacturing front.

Read my latest analysis of Archer's manufacturing progress for free: https://t.co/3LxUxLnKf4

The AI debate around $META is still getting dragged on.

On one side, Meta is already showing measurable payoff signals in the core ad business.

Revenue was up 33% YoY in Q1.

Ad impressions increased 19% YoY.

Average price per ad rose 12% YoY.

That combination matters because it points to both volume and pricing strength. Meta is not just serving more ads but is also getting better economics per ad. In an AI context, that is important because improved ranking, targeting, recommendation quality, creative tools, and conversion efficiency can all show up through stronger ad delivery and pricing.

The market tends to focus heavily on the cost side of AI, and understandably so.

R&D growth was 46% YoY in Q1.

Capex reached $19.8B in Q1 2026.

Total commitments through 2030 stood at $240 billion.

That is a major burden, and it raises the bar for future returns. Meta needs these investments to translate into durable revenue growth, better engagement, higher monetization, and eventually operating leverage.

The company is absorbing a massive investment cycle while the core business is still accelerating. That is very different from a company spending aggressively because growth has stalled.

I am leaning towards concluding that the current improvement in ad monetization is an early signal that Meta’s AI infrastructure is already reinforcing the economic engine that funds the entire strategy.

If revenue growth, impressions, and ad pricing continue moving in the right direction, investors may become more willing to underwrite the capex burden. For now, though, Meta remains one of the worst-performing big tech stocks. This may not change for some time.

$GME CEO Ryan Cohen wants to pursue a hostile bid for $EBAY

I noticed one detail in GameStop’s proposed $125/share bid for $EBAY that stands out more than the headline premium. The EPS bridge.

According to the proposal, diluted GAAP EPS is expected to move from $4.26 to $7.79 in year one.

That is an implied increase of ~83%.

What makes this interesting is that the EPS uplift appears to be driven heavily by cost reduction assumptions rather than revenue acceleration. The proposal points to $2.0 billion of annualized cost reductions within twelve months of close, including $1.2 billion from Sales & Marketing, $0.3 billion from Product Development, and $0.5 billion from G&A.

That is a big claim because the pro forma operating margin target moves to roughly 38–40%, versus a FY2025 baseline of 20.5%.

My read is that this bid is not just being framed as a takeover premium story. It is being framed as a margin-reset story.

The market will probably focus first on the 46% unaffected premium and the ~$55.5 billion aggregate equity value. But the more important debate may be whether the proposed cost takeout is achievable without damaging eBay’s marketplace competitiveness.

Cutting Sales & Marketing from $2.4 billion to $1.2 billion is especially aggressive. For a marketplace business, marketing efficiency matters, but so does buyer/seller liquidity. If those cuts reduce traffic quality, seller acquisition, or category depth, the EPS accretion could look better on paper than in practice.

The other interesting piece is GameStop’s stated strategic angle beyond cost reductions to use roughly 1,600 U.S. stores as a national network for authentication, intake, fulfillment, and live commerce.

That is the part that makes this more than a standard financial-engineering pitch.

If GameStop can credibly connect its physical footprint to eBay’s marketplace infrastructure, the argument becomes that the store base is not just a legacy retail asset, but a potential trust, logistics, and recommerce layer.

Still, the burden of proof is high.

The bid math depends on a major step-change in profitability, and the proposal’s year-one EPS target appears to assume a very large portion of the synergy case materializes quickly.

I believe the chances of a successful hostile takeover of EBAY by GameStop is quite low, but I sure am keeping an eye on how things play out.

The UAE exited OPEC last month.

For the likes of Adnoc Drilling, this was a welcome move given that their capacity expansion investments were literally sitting idle due to OPEC's production constraints.

Not good news for some consumer discretionary companies, though.

For OPEC, the UAE's exit was definitely a major blow. The UAE is the biggest oil producer to have left the cartel since joining.

@awpthorp@AlsieLC But the GPS DOES work from Al Quoz to JVC. GPS does not work around the airport area only if I’m not mistaken. Also, if you came across a taxi driver who doesn’t know how to go from Al Quoz to JVC, unless he’s a newbie, my bet is he was not being genuine.

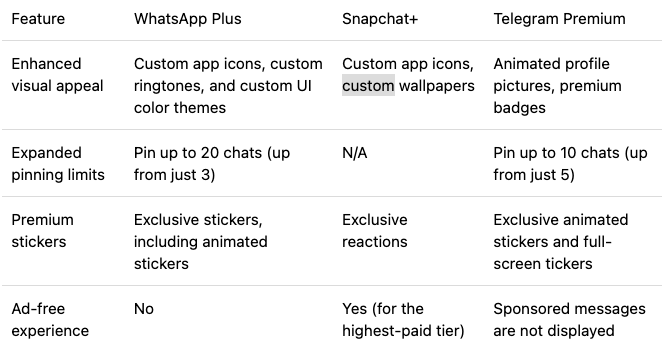

Those who are not keen followers of $META might have missed a major move by the company 2 weeks ago to monetize WhatsApp.

Meta rolled out a paid subscription tier named WhatsApp Plus in Europe, Mexico, and Pakistan.

Meta is most certainly taking a leaf out of Telegram's playbook (even Snapchat rolled out a paid tier a few years ago).

Been a Meta shareholder for a while and it's good to see the company deploying a tried and tested strategy to finally monetize the 3 billion+ WA monthly users.