The current FX conundrum perfectly summed up by @EpsilonTheory

The war is bullish USD until it isn't.

"A paradox is emerging in which the war simultaneously strengthens the dollar's short-term position through traditional crisis demand while eroding the institutional foundations that support its long-term dominance. Treasuries are not functioning as a safe haven, fiscal deficits are expanding under wartime and stimulus pressures, and the media language that once argued forcefully that there is no alternative to US largecap growth is fading. The convergence of rising inflation expectations, weakening growth signals, and retreating confidence in dollar-denominated assets points to a market caught between competing time horizons—seeking dollar safety now while quietly pricing that the post-war world may look structurally different."

Equity bears are at the brink of insanity given resilience in the indices, but odds of a breakdown are increasing now.

Equities top slowly as passive flows and rotational dynamics can hold up indices for a long time. There are many structural forces rigged to push them higher, and thus it takes a lot to make them go down. Over the course of an equity bull market, buy-the-dip behavior continually gets reinforced, and the majority of capital will be controlled by adherents to this mantra. In theory, the longer prices remain coiled, the larger the move once they exit the range.

This nuke in gold suggests there are liquidity issues brewing under the surface. It feels like a preview of what is going to happen to crowded trades. My theory is the Middle East is selling gold to shore up capital, as they have lost their revenue, and have many expenses around defence. They will also need to rebuild lost energy infra, and eventually, new pipelines to reroute around Hormuz.

The buyback window is starting to close, and the sugar rush of higher-than-usual tax refunds is starting to fade. Retail has been a key marginal buyer of equities in these past weeks, and the fading of the tax refund tailwind is critical.

The market is gradually coming to terms with the fact that this conflict may last for a long time. On a conventional level, the US and Israel have completely dominated Iran, but Iran has an asymmetric edge when it comes to controlling world oil prices through Hormuz. Trump can still end it, but the issue is that the US cannot simply leave, a ceasefire with Iran must be struck in order to guarantee that Hormuz is reopened. In order to strike a ceasefire, Iran wants to see a guarantee that the US and Israel won't attack them again (at a bare minimum), and it will be difficult for the US to get Israel to agree to that. Trump is used to being able to quickly maneuver according to his whims, as he did with tariffs, but the complex interlocking physical realities of war are different.

Oil shocks often contribute to the end of bull markets, since they constrain consumer spending, hit manufacturing, and lower the ability of central banks to offer support. Indeed, the Fed came out slightly hawkish yesterday, and Powell also hinted that he may stay in his Governor seat post his role as Chair ending, which would constrain Trump's plans to unleash liquidity.

We have a stronger dollar and long duration bond yields are going up over the world, which tightens liquidity. The Middle East is tight on money now and they were the marginal bidder in many assets. In particular, they were a key funder for AI capex through their investments in the frontier labs. They've been 40-50% of recent big rounds. Remember other deep pockets like Softbank are close to being tapped out. Any dollar that goes into these rounds will have to come out of something else, like liquid stocks (look at my pinned post for this broader thesis). And if we have any signs of risk to AI capex expectations, this will be a major shift that the market needs to contemplate.

I've said this before, but puts are a difficult way to express bearish equity views because timing is so uncertain. Equities can hold on for a long time, because they are structurally rigged to go higher. Easier expressions are simply being in cash, or gradually shorting cash stocks over time, which helps avoid getting chopped. This is a very difficult market, stay safe out there.

I continue to believe drones are the single best investment sector over the next 5y outside of AI/robotics.

The current Middle East conflict is teaching us that drones are here to stay as cheap, modern kamikaze against infra & high value targets.

Many drone stocks are overvalued based on TAM & team due to people piling in on war onset. However I would expect a sector wide correction to occur during any reported resolution or de-escalation. THAT is the dip to buy. 🍌

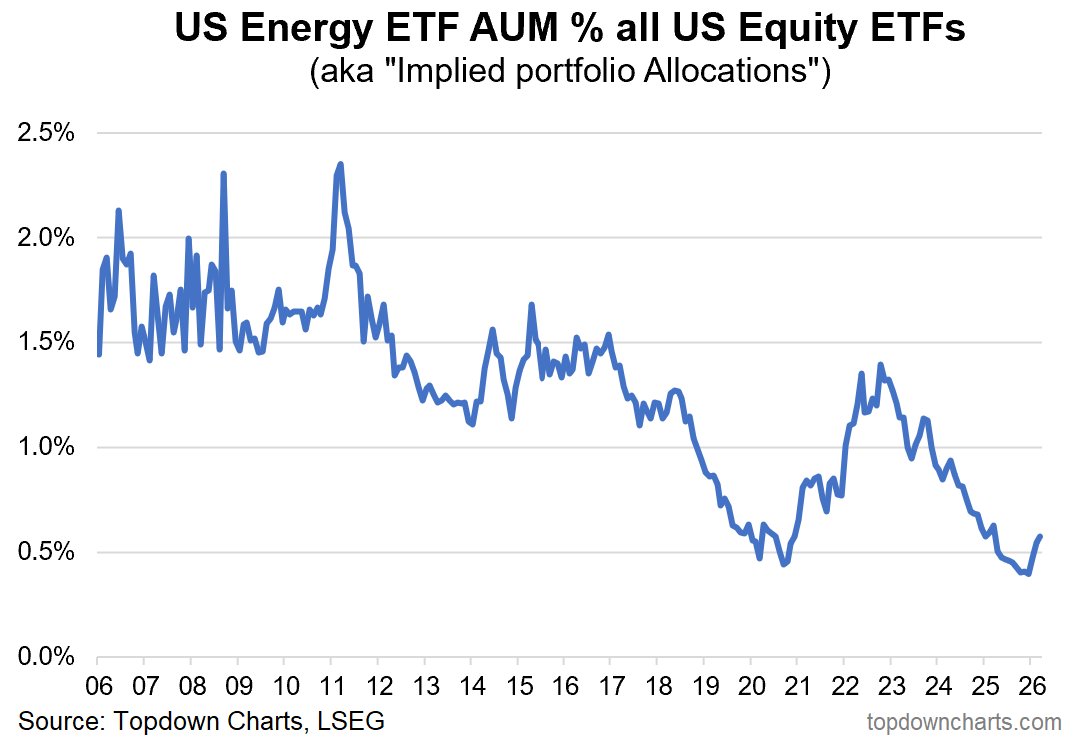

The energy sector remains extremely cheap.

- Implied portfolio allocation is still at historic lows

- To reach the previous high, energy stocks would need to outperform 4:1

In other words, investors are still massively underweight energy.

Historically, the biggest commodity bull markets started exactly like this:

low allocations, low expectations, and a sector most investors ignored.

Which means we are still very early.

$IBRX For those who don’t see ImmunityBio as a multi Trillion $ company, see pics below- you can’t unsee!

All Cancer, All Lymphopenia….All Infectious Disease (COVID to Sepsis)- Inevitable! ALC!

Revenue from only ≈400 NMBIC Patients out of 1.5M!

US gold reserves have never been this small relative to government debt:

Gold reserves now reflect just 3% of US federal debt, one of the lowest readings on record.

This comes despite the US holding 8,133.5 metric tons of gold, the largest stockpile in the world, and prices surging to record highs.

By comparison, the ratio was ~18% in 1980, or 6x higher.

At the same level of reserves, gold prices would have to rise +400%, to $26,000/oz, to match the 1980s peak.

Meanwhile, in the 1940s, gold reserves backed over 50% of federal debt.

To match the 1940s ratio, gold would need to surge +1,340% to ~$75,000/oz.

Gold reserves are highlighting just how astronomical US debt has become.