$AMZN:

$743 billion revenue, $91 billion net income, valued at $2.6 Trillion, Plus Amazon Leo

$SPCX:

$18 billion revenue, -$10 billion net income, value at $2.2 trillion

And people think this is normal

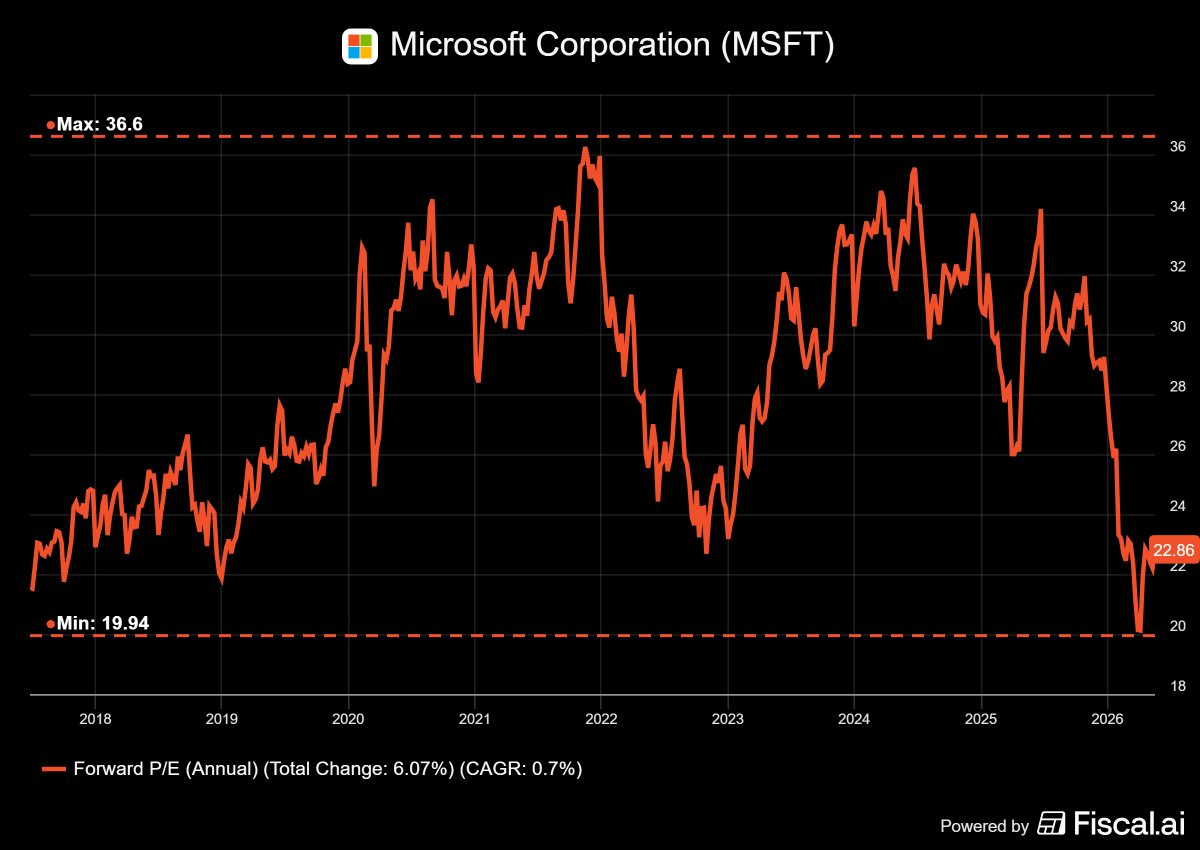

Microsoft is trading near its lowest forward P/E in years!

Meanwhile, revenues, margins, and positioning have never been stronger.

Disconnects like this don’t last!

$MSFT

This is what will happen to the stock market. Listen to me, because I am the #1 trader in Singapore.

We are in a narrow rally.

1. $SPY can hit new highs but market breadth is poor: meaning few stocks are participating in this rally.

2. Small group of high-valuation leaders like $MU, $SNDK carries almost all the gains.

3. This happened in late 1990's (dot-com era) and 2022 banking criss.

What will happen when the leaders pull back massively?

1. It's called a, "catch down." The big leaders will pull back huge.

2. Rotation will go into laggards called, "catch up." Money flows out of crowded and expensive winners to the stocks that have NOT gone up yet.

3. These laggards fall less and they will outperform.

We've seen this happen:

1. During the dot com era

2. 2022 banking criss

3. Same thing will happen now

So what should you do?

1. No need to sell your best winners, just trim.

2. Rotate that money into laggards and balance.

What are the laggards?

1. Software like $INTU, $NOW, $MDB, $CRM, etc.

2. International stocks like $BABA, $GRAB, and $MELI, $XPEV, etc.

3. Financials like $HOOD, $SOFI, $JPM

4. Healthcare like $UNH, $PFE, $MRK, $BSX

5. Consumer discretionary like $NKE, $TSLA, $HD, and $TGT

6. Real estate like $SPG, $O

7. Consumer staples like $CLX, $PG, $KO, and $PEP

8. Others like $UPS

$HIMS earnings big miss, I'm selling all my shares.

...is what the paper hands would say.

The important points most will miss:

→ $NVO turnaround came late in Q1, shipping only began in April, so the benefit is more of a Q2/Q3 catalyst.

→ Eucalyptus closes mid-2026, only partial FY26 revenue can be booked depending on timing. Full contribution hits in FY27.

→ A $700M Q2 would be about 29% YoY growth, that is where the re-acceleration starts to become visible.

Now let's look at the revenue headline:

United States: $530M

→ down -8% y/y

→ down -4% q/q

Rest of World: $78M

→ up +969% y/y

→ up +23% q/q

Total revenue: $608M

→ up 4% y/y

→ down 1.5% q/q

So yes, the US business clearly took a hit during the GLP-1 reset. But international revenue is already starting to show why Eucalyptus matters.

Now here is what the company actually said:

Management did not talk like a company whose growth story is broken...

Andrew Dudum called 2026 a "defining year" and said "HIMS is not just growing, it is pulling away from the field on the path to becoming the world’s largest consumer health platform". That is a big statement.

The key points from management:

→ Domestic business is accelerating as they exit Q1

→ They are expanding into new categories and new countries

→ They are investing in diagnostics and technology infrastructure

→ The platform is becoming more personal, data driven and AI led

$HIMS has already fulfilled 125K+ Wegovy product orders within 6 weeks of launch. Again none of this demand has been factored into ER.

So yes I will be buying this dip because this has never been short term. It's a 2030 hold at the very least.