투자자는 AI 기술보다 AI CapEx를 먼저 봐야 한다.

왜냐하면 시장을 움직이는 것은 기술이 아니라 자본이기 때문이다.

많은 사람들이 AI 투자가 과열되었다고 우려한다.

하지만 지금의 AI 투자는 과거 닷컴버블과 결정적인 차이가 있다.

닷컴 시대에는 미래의 트래픽을 기대하며 투자했다.

반면 지금의 AI 투자는 이미 확보된 수요를 바탕으로 집행되는 경우가 많다.

대표적인 것이 하이퍼스케일러들의 RPO(Remaining Performance Obligations)다.

RPO는 이미 계약은 체결되었지만 아직 매출로 인식되지 않은 미래의 계약 잔고다.

RPO가 증가한다는 것은 앞으로 서비스를 제공해야 할 의무가 늘어난다는 의미이며, 이를 이행하기 위해 데이터센터와 GPU 투자는 선택이 아니라 필수다.

즉 현재의 AI CapEx는 '희망'이 아니라 '계약 이행'에 가깝다.

이것이 이번 AI 사이클이 생각보다 오래 지속될 수 있다고 보는 이유다.

SK Hynix: ADR 자금을 원화로 환전할 경우 생기는 일

주거래 은행이 외환 익스포져를 피하기 위해 한은에 매각하는 경우를 가정

한은은 주거래은행으로부터 매입한 달러를 그대로 두면 지준금이 그대로 늘어나 통화관리에 문제가 생길 수 있음

한은이 통안증권 발행으로 지준금을 흡수하는 상황 가정

https://t.co/BC6c13CQmW

중간보고 받았다고 하니 세제 개편안 큰 틀이 대충 나왔네요.

고가주택 잡겠다는 정부 의지가 저렇게 강한데도

여전히 부동산에 투자하겠다는 사람들이 많다는 게..

역사적으로 봐도 정부랑 정면으로 맞서서 성공한 투자 사례는 정말 찾기 어려움.

Shocking stat of the day:

The Memory ETF, $DRAM, has surpassed $25 billion in assets under management (AUM) for the first time, officially overtaking the 26-year-old South Korea ETF, $EWY, despite launching on April 2nd.

This comes as $DRAM has attracted a record +$22 billion in inflows since its debut.

Over the same period, $EWY has posted -$2 billion in outflows.

To put this into perspective, before $DRAM launched, $EWY had attracted +$6 billion in inflows in 2026.

Prior to $DRAM, investors largely used $EWY as the international proxy for memory stocks.

Today, these two ETFs still carry a 46% overlap in underlying holdings.

The memory trade has never been more popular.

The US economy is now dependent on AI spending:

AI investment now accounts for more than 25% of US GDP growth, the largest contribution on record.

This includes spending on software, IT equipment, R&D, and data centers.

In other words, for every $4 of US economic growth today, over $1 is coming from AI investment.

This comes as AI spending is up to a record ~8% of US GDP.

By comparison, spending on IT equipment, software, and R&D peaked at ~6.5% of GDP during the 2000 Dot-Com bubble.

US economic growth is now all about AI.

The AI race between the US and China is intensifying:

Currently, 20 of the world’s 50 most used AI models come from China, according to Apollo, up 400% since 2025.

Over the same period, the number of US models in the group has fallen to 28 from 33.

Meanwhile, monthly token usage of Chinese models among the top 20 AI models surged +113% MoM, to 98 trillion tokens in June.

By comparison, US model token usage rose +43% MoM, to 53 trillion tokens last month.

As a result, token usage for Chinese models is now 85% higher than for US models, up from 24% in May.

China is challenging the US' lead in AI race.

A stunning piece of engineering!!

1X unveils the new humanoid hand for NEO

- 25 degrees of freedom: 22 fully actuated in the fingers and palm, plus 3 at the wrist.

- The DoF are distributed anatomically rather than evenly, deliberately biased toward a thumb that genuinely opposes the fingers.

- In-house tendon-driven, quasi-direct-drive running low gear ratios of ~5:1 to 15:1 vs the typical 100:1–200:1.

- Motors live in the forearm and pull tendons through the wrist. This keeps the hand light and its inertia low while producing high forces.

Sensing

- All 25 DoF are natively force-controlled and fully backdrivable. Every joint doubles as a force sensor.

- Very important, closed-loop proprioception: it always knows its own pose and effort without looking.

- Tactile skin across the fingertips and surfaces measuring contact and shear. This helps with adaptive gripping in real time.

Safety and durability

- IP68 waterproof and food-safe, so it can wash its own hands.

- Compliant by construction: the low gear ratios, tendon drive, and low distal inertia let external impacts safely backdrive the fingers. It yields when hit by a hammer or caught in a drawer.

- Full finger assemblies validated to millions of cycles.

Manufacturing

- Deep vertical integration: in-house motors, custom electronics, and tendon systems.

- Hundreds built already, with capacity to produce 10,000 hands this year.

"An API to the Physical World"

This is just ridiculous..

2027 P/E multiples per BofA:

$AMZN, 21.4x

$MSFT, 18.7x

$META, 16.3x

$NVDA, 15.7x

S&P 500 is currently at 21x forward earnings.

These are the highest quality companies in the index with way above average growth projections, yet $AMZN trades at index multiple while $META, $MSFT and $NVDA are discounted relative to the index.

This is outright ridiculous and won’t be sustained. They’ll eventually be re-rated.

All are no-brainers here.

주도주 매수를 고려해야 할 4가지 이유

$SNDK, $MU, SK hynix, Samsung, Kioxia

1. 레버리지 펀드 청산 압력 완화

헤지펀드 등 레버리지 펀드들의 주식 차입비용이 정점을 통과하면서 포지션 청산 압력이 낮아졌습니다.

S&P 500 레버리지 포지션 구축 비용과 SOFR 금리의 스프레드(AXW3 Index)가 5~6월 내내 급등하다가 6월 말 정점을 찍고 하락 중입니다. (과거 2024년 연말, 2025년 9월 말에도 이와 유사한 조정 패턴이 관측된 바 있습니다.)

2. 주도주의 기술적 부담(리스크) 경감

2024년 이후 반복되어 온 [① 이격 확대 → ② 언와인딩 → ③ 펀더멘탈 우려 제기 → ④ 강한 실적으로 우려 불식]의 패턴이 재현되고 있습니다.

6월 당시 200일선 대비 200% 상회하며 엄청난 기술적 부담을 보였던 '마이크론'의 이격도가 현재 100% 수준으로 절반가량 떨어졌으며, 다른 주도주들도 이격 부담을 상당 부분 덜어냈습니다. $MU

3. 언와인딩 강도의 경험적 고점 도달

주도주와 소외주의 상대수익률을 측정하는 MSZZMOMO Index가 고점 대비 22% 하락했습니다. 이는 2023년 하반기 AI 장세 확립 이후 경험했던 언와인딩 강도의 한계치 수준입니다.

과거 언와인딩 국면에서 최고 선도주의 낙폭은 고점 대비 30~40% 수준이었습니다(2024년 7월 엔비디아 27%, 2025년 2월 팔란티어 40%). 현재 주도주인 마이크론(-23%)과 샌디스크(-31%)의 낙폭 역시 이미 해당 과거 고점 수준에 근접했습니다.

4. 꺾이지 않는 견고한 주도주 실적 전망

압도적인 실적을 가진 주도주가 단번에 하락 추세로 전환된 사례는 역사적으로 드뭅니다.

통상 전고점 근접 후 최소한 '쌍봉'을 만들며, 실제 하락 추세 전환은 실적이 완전히 무너질 때 일어납니다. 하지만 현재 주도주들의 실적 전망은 너무나도 공고하여 이번 사이클이 끝났다고 보기 어렵습니다.

(26. 7. 9 신한)

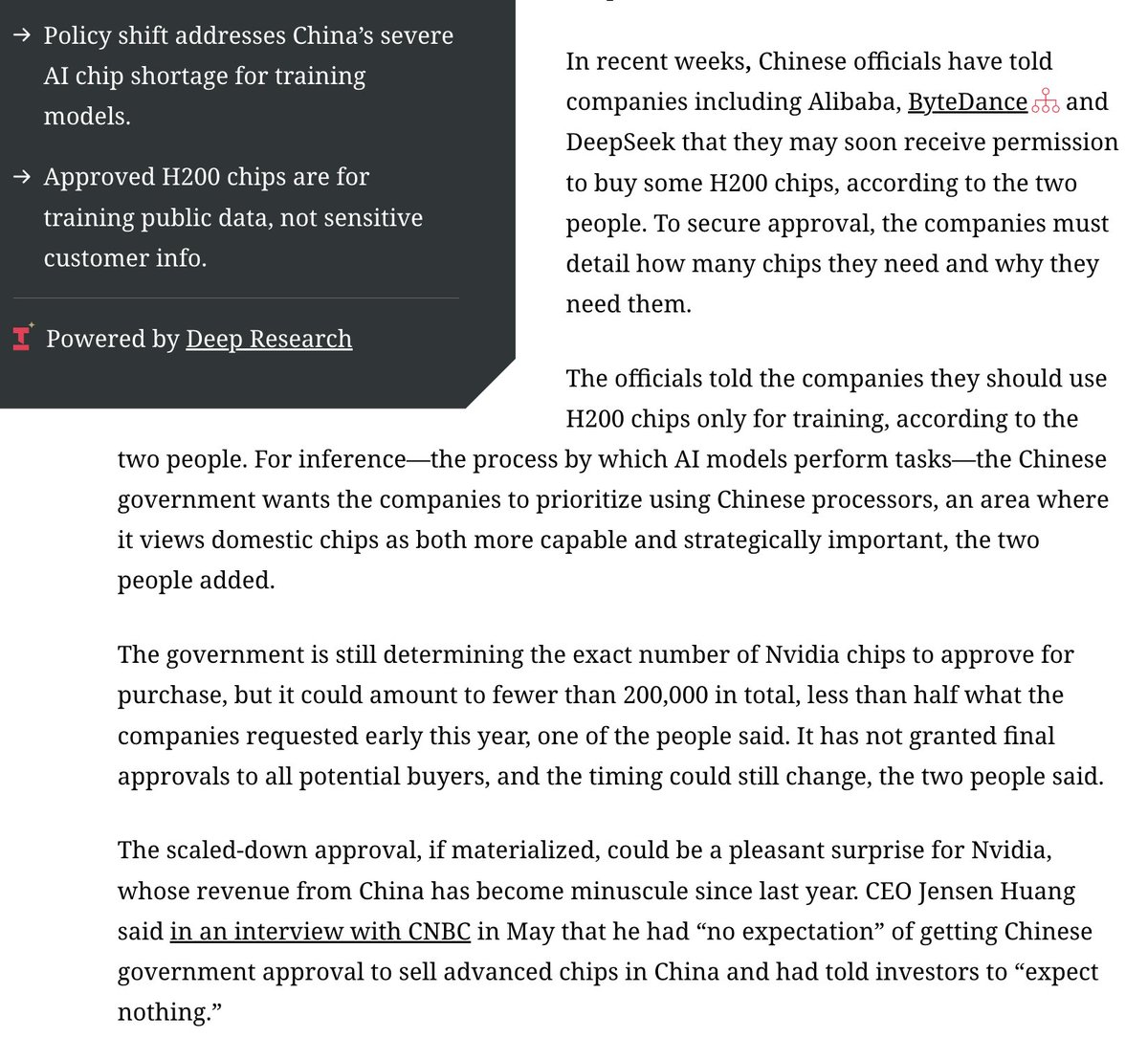

CHINA CONSIDERS RESTRICTING OVERSEAS ACCESS TO CUTTING-EDGE AI MODELS

China’s Ministry of Commerce has led meetings over the past month with major AI companies, including Alibaba, ByteDance, and https://t.co/YDe0KRldDB, to discuss measures that would restrict overseas access to cutting-edge AI models, including models that have not yet been released.

The discussions reportedly include not only closed-source models but also open-weight models. However, the scope of application is still under debate, and the rules may ultimately apply only to future frontier models.

Officials have also discussed designating the leakage or theft of proprietary AI technologies as a national security crime, with stronger penalties, as well as restricting the types of foreign capital that can invest in Chinese AI startups.

The backdrop is the U.S. move to strengthen export controls on AI models, along with national security concerns over cutting-edge models that could possess advanced cyberattack capabilities.

Chinese authorities are reportedly concerned that advanced U.S. cybersecurity AI models could be used to exploit vulnerabilities in Chinese software.

Since the beginning of this year, China has continued to tighten measures to prevent AI technology from being transferred overseas. Authorities have investigated whether Chinese AI startups that relocated abroad violated export control laws, while also strengthening oversight of overseas transactions involving Chinese investors, technology, data, and national security concerns.

Future regulations could take the form of a tiered framework based on technological capability. Basic open-source AI models may be managed through a filing system, high-performance models may be subject to security reviews, and the most sensitive frontier models may be banned from public release or restricted to use within China.

New Anthropic research: A global workspace in language models.

Of everything happening in your brain right now, only a tiny fraction is consciously accessible—thoughts you can describe, hold in mind, and reason with.

We found a strikingly similar divide inside Claude.

The US stock market has never been more dominant:

US stock market capitalization is up to a record ~$81 trillion, now accounting for ~48% of global market cap.

This exceeds the world's 2nd largest stock market, China, at $17 trillion, by 375%.

The US stock market is now twice as large as that of China, Japan, Hong Kong, and Taiwan combined.

It is also larger than the next 18 stock markets combined.

The Magnificent 7 stocks alone are now larger than China's market value.

The current scale of the US stock market is unprecedented.

![DrNHJ's tweet photo. 주도주 매수를 고려해야 할 4가지 이유

$SNDK, $MU, SK hynix, Samsung, Kioxia

1. 레버리지 펀드 청산 압력 완화

헤지펀드 등 레버리지 펀드들의 주식 차입비용이 정점을 통과하면서 포지션 청산 압력이 낮아졌습니다.

S&P 500 레버리지 포지션 구축 비용과 SOFR 금리의 스프레드(AXW3 Index)가 5~6월 내내 급등하다가 6월 말 정점을 찍고 하락 중입니다. (과거 2024년 연말, 2025년 9월 말에도 이와 유사한 조정 패턴이 관측된 바 있습니다.)

2. 주도주의 기술적 부담(리스크) 경감

2024년 이후 반복되어 온 [① 이격 확대 → ② 언와인딩 → ③ 펀더멘탈 우려 제기 → ④ 강한 실적으로 우려 불식]의 패턴이 재현되고 있습니다.

6월 당시 200일선 대비 200% 상회하며 엄청난 기술적 부담을 보였던 '마이크론'의 이격도가 현재 100% 수준으로 절반가량 떨어졌으며, 다른 주도주들도 이격 부담을 상당 부분 덜어냈습니다. $MU

3. 언와인딩 강도의 경험적 고점 도달

주도주와 소외주의 상대수익률을 측정하는 MSZZMOMO Index가 고점 대비 22% 하락했습니다. 이는 2023년 하반기 AI 장세 확립 이후 경험했던 언와인딩 강도의 한계치 수준입니다.

과거 언와인딩 국면에서 최고 선도주의 낙폭은 고점 대비 30~40% 수준이었습니다(2024년 7월 엔비디아 27%, 2025년 2월 팔란티어 40%). 현재 주도주인 마이크론(-23%)과 샌디스크(-31%)의 낙폭 역시 이미 해당 과거 고점 수준에 근접했습니다.

4. 꺾이지 않는 견고한 주도주 실적 전망

압도적인 실적을 가진 주도주가 단번에 하락 추세로 전환된 사례는 역사적으로 드뭅니다.

통상 전고점 근접 후 최소한 '쌍봉'을 만들며, 실제 하락 추세 전환은 실적이 완전히 무너질 때 일어납니다. 하지만 현재 주도주들의 실적 전망은 너무나도 공고하여 이번 사이클이 끝났다고 보기 어렵습니다.

(26. 7. 9 신한)](https://pbs.twimg.com/media/HMxZT0sbAAAnrYg.png)

![DrNHJ's tweet photo. 주도주 매수를 고려해야 할 4가지 이유

$SNDK, $MU, SK hynix, Samsung, Kioxia

1. 레버리지 펀드 청산 압력 완화

헤지펀드 등 레버리지 펀드들의 주식 차입비용이 정점을 통과하면서 포지션 청산 압력이 낮아졌습니다.

S&P 500 레버리지 포지션 구축 비용과 SOFR 금리의 스프레드(AXW3 Index)가 5~6월 내내 급등하다가 6월 말 정점을 찍고 하락 중입니다. (과거 2024년 연말, 2025년 9월 말에도 이와 유사한 조정 패턴이 관측된 바 있습니다.)

2. 주도주의 기술적 부담(리스크) 경감

2024년 이후 반복되어 온 [① 이격 확대 → ② 언와인딩 → ③ 펀더멘탈 우려 제기 → ④ 강한 실적으로 우려 불식]의 패턴이 재현되고 있습니다.

6월 당시 200일선 대비 200% 상회하며 엄청난 기술적 부담을 보였던 '마이크론'의 이격도가 현재 100% 수준으로 절반가량 떨어졌으며, 다른 주도주들도 이격 부담을 상당 부분 덜어냈습니다. $MU

3. 언와인딩 강도의 경험적 고점 도달

주도주와 소외주의 상대수익률을 측정하는 MSZZMOMO Index가 고점 대비 22% 하락했습니다. 이는 2023년 하반기 AI 장세 확립 이후 경험했던 언와인딩 강도의 한계치 수준입니다.

과거 언와인딩 국면에서 최고 선도주의 낙폭은 고점 대비 30~40% 수준이었습니다(2024년 7월 엔비디아 27%, 2025년 2월 팔란티어 40%). 현재 주도주인 마이크론(-23%)과 샌디스크(-31%)의 낙폭 역시 이미 해당 과거 고점 수준에 근접했습니다.

4. 꺾이지 않는 견고한 주도주 실적 전망

압도적인 실적을 가진 주도주가 단번에 하락 추세로 전환된 사례는 역사적으로 드뭅니다.

통상 전고점 근접 후 최소한 '쌍봉'을 만들며, 실제 하락 추세 전환은 실적이 완전히 무너질 때 일어납니다. 하지만 현재 주도주들의 실적 전망은 너무나도 공고하여 이번 사이클이 끝났다고 보기 어렵습니다.

(26. 7. 9 신한)](https://pbs.twimg.com/media/HMxZRqnbkAAvdlj.png)

![DrNHJ's tweet photo. 주도주 매수를 고려해야 할 4가지 이유

$SNDK, $MU, SK hynix, Samsung, Kioxia

1. 레버리지 펀드 청산 압력 완화

헤지펀드 등 레버리지 펀드들의 주식 차입비용이 정점을 통과하면서 포지션 청산 압력이 낮아졌습니다.

S&P 500 레버리지 포지션 구축 비용과 SOFR 금리의 스프레드(AXW3 Index)가 5~6월 내내 급등하다가 6월 말 정점을 찍고 하락 중입니다. (과거 2024년 연말, 2025년 9월 말에도 이와 유사한 조정 패턴이 관측된 바 있습니다.)

2. 주도주의 기술적 부담(리스크) 경감

2024년 이후 반복되어 온 [① 이격 확대 → ② 언와인딩 → ③ 펀더멘탈 우려 제기 → ④ 강한 실적으로 우려 불식]의 패턴이 재현되고 있습니다.

6월 당시 200일선 대비 200% 상회하며 엄청난 기술적 부담을 보였던 '마이크론'의 이격도가 현재 100% 수준으로 절반가량 떨어졌으며, 다른 주도주들도 이격 부담을 상당 부분 덜어냈습니다. $MU

3. 언와인딩 강도의 경험적 고점 도달

주도주와 소외주의 상대수익률을 측정하는 MSZZMOMO Index가 고점 대비 22% 하락했습니다. 이는 2023년 하반기 AI 장세 확립 이후 경험했던 언와인딩 강도의 한계치 수준입니다.

과거 언와인딩 국면에서 최고 선도주의 낙폭은 고점 대비 30~40% 수준이었습니다(2024년 7월 엔비디아 27%, 2025년 2월 팔란티어 40%). 현재 주도주인 마이크론(-23%)과 샌디스크(-31%)의 낙폭 역시 이미 해당 과거 고점 수준에 근접했습니다.

4. 꺾이지 않는 견고한 주도주 실적 전망

압도적인 실적을 가진 주도주가 단번에 하락 추세로 전환된 사례는 역사적으로 드뭅니다.

통상 전고점 근접 후 최소한 '쌍봉'을 만들며, 실제 하락 추세 전환은 실적이 완전히 무너질 때 일어납니다. 하지만 현재 주도주들의 실적 전망은 너무나도 공고하여 이번 사이클이 끝났다고 보기 어렵습니다.

(26. 7. 9 신한)](https://pbs.twimg.com/media/HMxZPLyaUAAar3a.png)

![DrNHJ's tweet photo. 주도주 매수를 고려해야 할 4가지 이유

$SNDK, $MU, SK hynix, Samsung, Kioxia

1. 레버리지 펀드 청산 압력 완화

헤지펀드 등 레버리지 펀드들의 주식 차입비용이 정점을 통과하면서 포지션 청산 압력이 낮아졌습니다.

S&P 500 레버리지 포지션 구축 비용과 SOFR 금리의 스프레드(AXW3 Index)가 5~6월 내내 급등하다가 6월 말 정점을 찍고 하락 중입니다. (과거 2024년 연말, 2025년 9월 말에도 이와 유사한 조정 패턴이 관측된 바 있습니다.)

2. 주도주의 기술적 부담(리스크) 경감

2024년 이후 반복되어 온 [① 이격 확대 → ② 언와인딩 → ③ 펀더멘탈 우려 제기 → ④ 강한 실적으로 우려 불식]의 패턴이 재현되고 있습니다.

6월 당시 200일선 대비 200% 상회하며 엄청난 기술적 부담을 보였던 '마이크론'의 이격도가 현재 100% 수준으로 절반가량 떨어졌으며, 다른 주도주들도 이격 부담을 상당 부분 덜어냈습니다. $MU

3. 언와인딩 강도의 경험적 고점 도달

주도주와 소외주의 상대수익률을 측정하는 MSZZMOMO Index가 고점 대비 22% 하락했습니다. 이는 2023년 하반기 AI 장세 확립 이후 경험했던 언와인딩 강도의 한계치 수준입니다.

과거 언와인딩 국면에서 최고 선도주의 낙폭은 고점 대비 30~40% 수준이었습니다(2024년 7월 엔비디아 27%, 2025년 2월 팔란티어 40%). 현재 주도주인 마이크론(-23%)과 샌디스크(-31%)의 낙폭 역시 이미 해당 과거 고점 수준에 근접했습니다.

4. 꺾이지 않는 견고한 주도주 실적 전망

압도적인 실적을 가진 주도주가 단번에 하락 추세로 전환된 사례는 역사적으로 드뭅니다.

통상 전고점 근접 후 최소한 '쌍봉'을 만들며, 실제 하락 추세 전환은 실적이 완전히 무너질 때 일어납니다. 하지만 현재 주도주들의 실적 전망은 너무나도 공고하여 이번 사이클이 끝났다고 보기 어렵습니다.

(26. 7. 9 신한)](https://pbs.twimg.com/media/HMxZVsAboAABCr-.png)