We are on an unsustainable fiscal path:

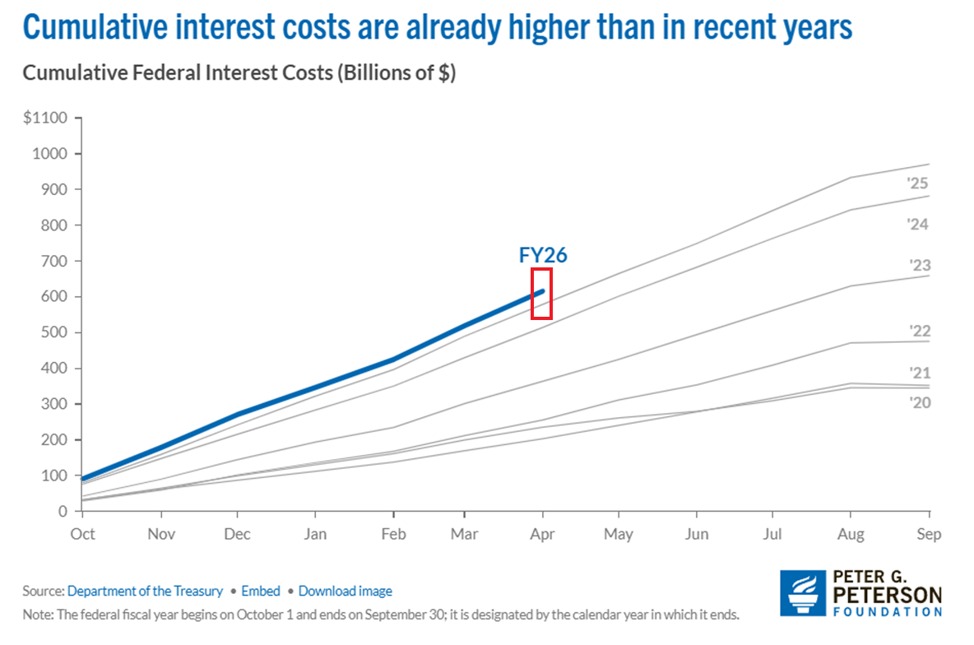

Interest costs on US public debt rose +$37 billion YoY in the first 7 months of FY2026, or +6.4%, to a record $616 billion.

Interest has more than TRIPLED for this time of the year since 2021.

As a result, interest payments are now the fastest-growing portion of the entire federal budget and the 2nd-largest spending category, surpassing Defense and Medicare, only behind Social Security.

The Congressional Budget Office projects annual net interest payments to more than DOUBLE from $1.0 trillion in 2026 to $2.1 trillion by 2036.

Over the next 10 years, interest costs are expected to total a massive $16.2 trillion.

As a proportion of GDP, interest is projected to reach 3.2% this year, surpassing the previous record set in 1991, and surging further to 4.6% of GDP by 2036.

The cost of US government debt has never been this high.

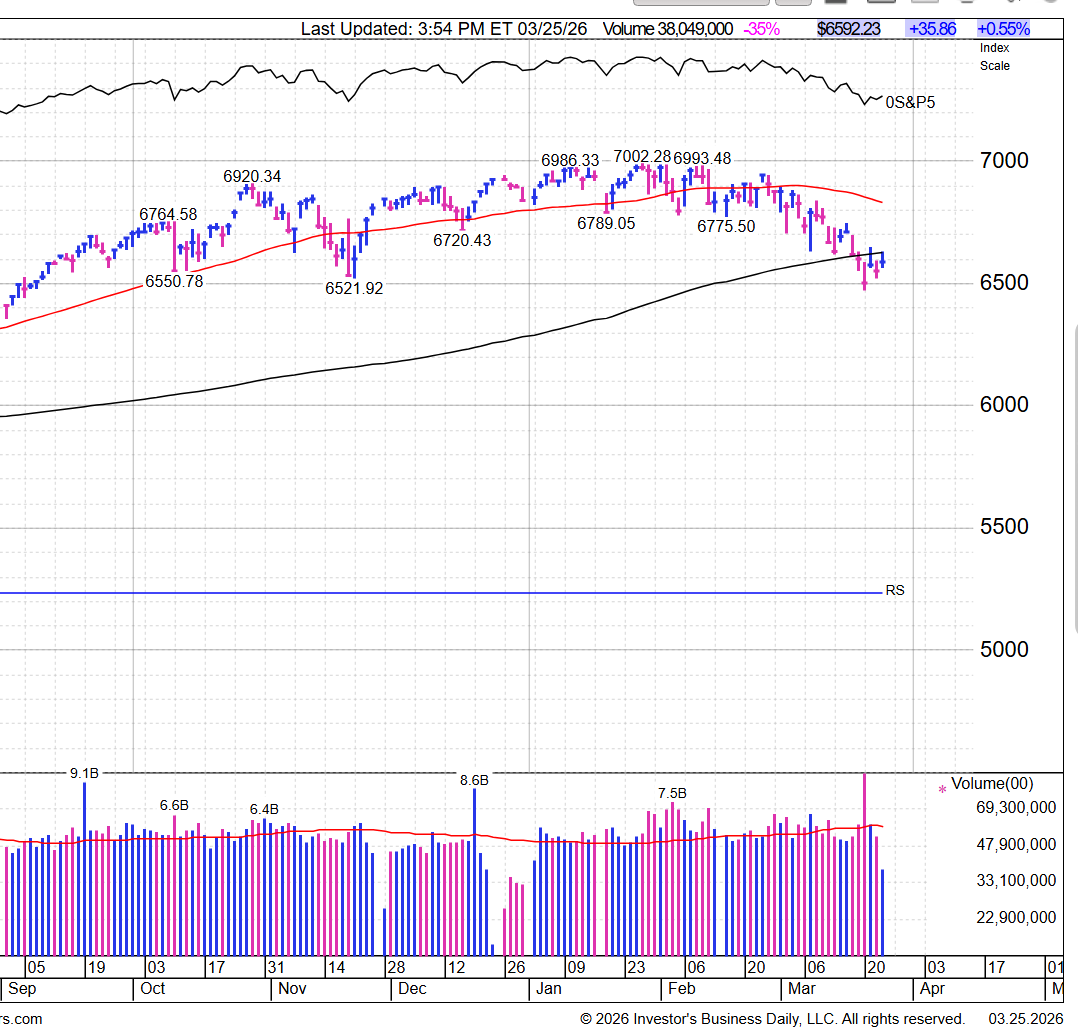

The market's character is still one of a bear market or cyclical correction; strong open, fade into close and major average living below the 200-day line. Before a reliable bottom can be established, we need to see better price and volume action, including better action from breakout names forming bases.

We are clearly NOT out of the woods yet. The market backdrop is one where sentiment has improved with rising pessimism, but not a full capitulation. The VIX has reached bear warning levels, but remains below true washout extremes. A volatility washout is not required for a bottom, but would add conviction.

Bullish Scenario

--The war ends

--Oil prices recede

--Stagflation concerns ease

--Central banks continuing their easing trajectory

Under this scenario, we would expect:

-A broadening market advance

-Emergence of new leadership from sound bases

-A Follow-Through Day (FTD) on the NYSE and/or NASDAQ confirming institutional buying with little in the way of immediate distribution

-Significant drop in volatility

Bearish Scenario

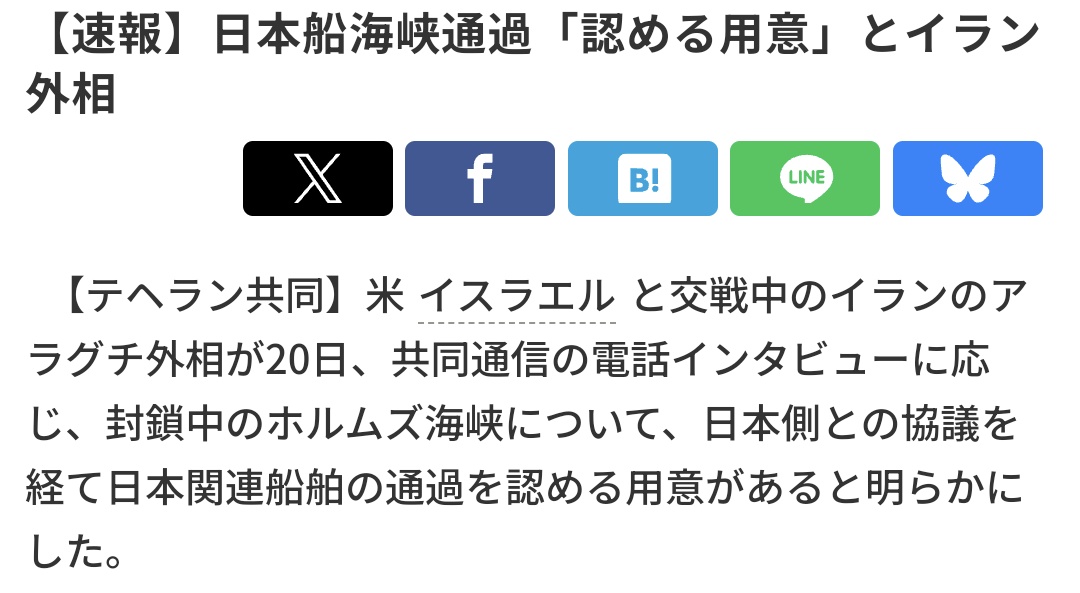

--The war persists or escalates

--The Strait of Hormuz remains disrupted

--Oil prices make new highs

--Stagflation becomes evident in hard economic data

This would likely result in:

-Limited general market rally attempts with most breakout stocks failing

-Lack of follow-through from breakout names

-Further deterioration in breadth and leadership

-Dearth of setups in buyable position

-Continued elevated volatility and distribution

In that case, sentiment would likely need to reach higher levels of pessimism before a durable market bottom could form. In its absence, and end to the factors that are pressuring the market could cause the market to bottom in less dramatic fashion.