TeraProbe 6627, Japan's largest semiconductor testing house, which is a small-cap company (worth about USD250mm mcap) and trading at 2.2x EV/EBITDA, has seen its share price break out of its uptrend channel since early 2023, and appears to have room to run because of strong earnings growth.

Profits have risen 651.7% y/y in FY12/21, and 74.7% y/y in FY12/22. Dividend was hiked by over 3x LY, and will be set at 30% of profits this year. So far, sales are outpacing guidance, meaning that profits are also likely to outperform, barring a sudden spike in expenses.

TeraProbe is a subsidiary of Taiwan's Powertech Technology Inc., the world's leading provider of turnkey services for chip probing, packaging, and testing. Powertech owns 47.84% of TeraProbe. The company cites its strong connection to the Taiwan market as one of its strengths.

As shown in the image below, wafer testing is the final step in the backend process of semiconductor production, and involves the identification of defective products. It plays a crucial role in satisfying product specifications, and contributes to raising the non-defective product rate by feeding back the test results to the wafer manufacturing process.

As Japan's largest test house, TeraProbe has a wealth of cutting edge testers and probers. A quick glance at its balance sheet shows that a large portion of its assets are weighted toward these testing equipment. Its testers are mainly used for logic (CPU, SoC), image sensors (CIS, CCD), analog/mixed signals, and memory (DRAM, Flash). Its testing process involves 5 steps: (1) selection of test equipment (2) design and development of jigs and tools (3) test program development (4) test pattern development, and (5) on-site development support.

Reading through its disclosures, I found out that 1.056 billion yen in profits (out of a total of 3.134 billion yen in profits LY) were booked as extraordinary profit from dividends received from its Taiwan subsidiary TeraPower Technology, a Taiwan-based wafer testing JV between Powertech Technology and TeraProbe. It appears that this subsidiary is posting strong profits thanks to its AI-assisted highly automated testing technology. It's already churning out 1/3 of TeraProbe's profits, and I suspect this subsidiary might soon be more valuable than TeraProbe itself. Time will tell.

Links

1. Investors Page in English: https://t.co/B1HMmWQSmI

2. Powertech Technology: https://t.co/2QUBgnEhpe

3. TeraPower Technology: https://t.co/M41NiHkXEL

Very bullish I-tech presentation in ABGSC providing some extra colour. '23 looks very promising, after 3 disappointing years the thesis is now starting to play-out.

"We can 5-fold our revenues with the same number of employees, around 10 + consultants".

https://t.co/9yUJUUqA81

Nice read - the world is getting more aware of soil microbes and their importance in nourishing us and help fight climate change.

Verde already does that!

$NPK.TO

@CristianoVelos9

https://t.co/ADGGBJ8oYr

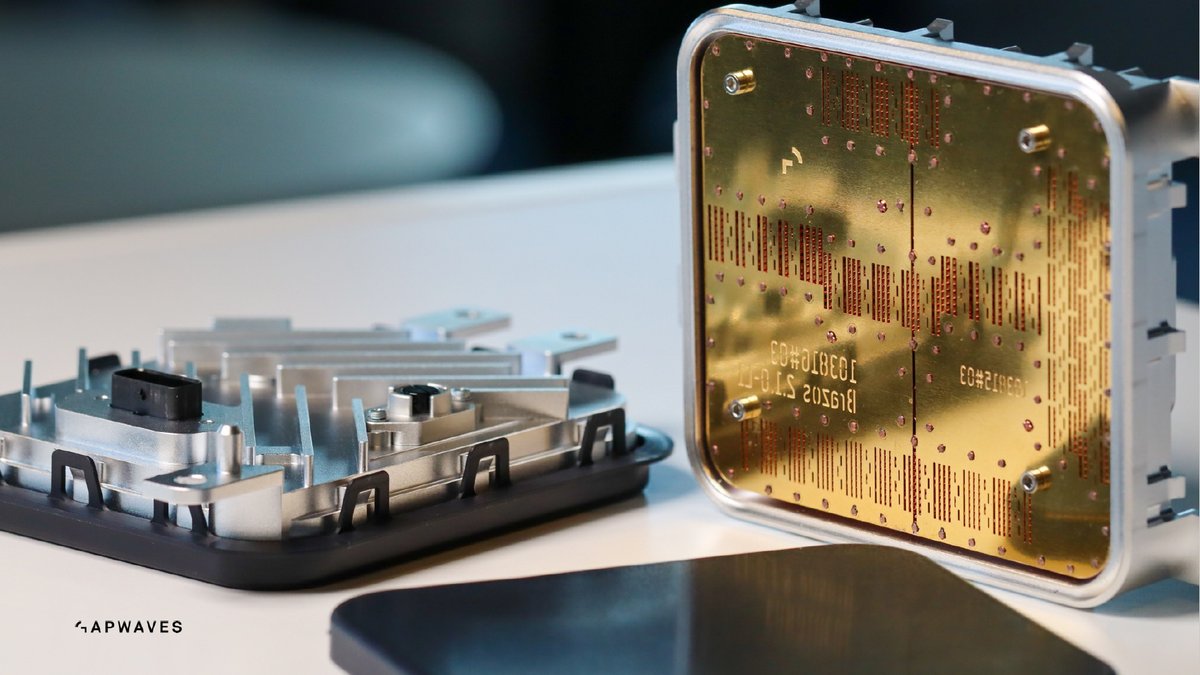

Gapwaves' report came in weaker than Redeye expected, with sales decreasing 16%. Lower sales and higher OPEX are the main reasons for EBITDA deviation. Thus our initial view is that this is a bump in the road:

$GAPW

https://t.co/LHVpk2DHWI

I read all 154 pages of Microsoft Research's "Sparks of AGI".

Most people don't realise the shocking reality AI is going to bring.

Here's what I found:

1/12 Today's short thread will cover ROIC or return on invested capital and one of the ways I like to calculate the ratio.

We will look at the formula, and inputs and briefly discuss why. Keep in mind there are a gozillion ways to determine ROIC, this is my fav.

🧵⬇️

@GuyFeldm I agree to a large extent with you. Potash prices determine margins a lot in the short/medium term, still a big runway for more adoption of a superior product. I hope they find a way the carbon sequestration via Carbon Credits.

@david_katunaric I don't own it and don't have a pitch, but I am very interested in the stock of the Polish stock exchange, trades at a p/e around 10, I think it has long-term tailwinds due to Polish economic development.

@VC05530508@WillThrower3 the past is not a good indicator for the future on the stock market. But yeah these kinds of early-stage/growth companies are certainly high-risk.

Amazed to have found such an in-depth report on $ANO.AX for free (by @WillThrower3 on value investors club). The report is a few years old, but I think it is a really interesting company. They are producing less harmful ingredients for sunscreens.

https://t.co/EDXN2h0fZG

@VC05530508@WillThrower3 I am not saying I am bullish or bearish (don't know the company well enough for that at this point), just that what they are actually doing (as a company for their customers) is interesting in my opinion. But still I would like to mention:

My latest on $INTZ on Seeking Alpha here: https://t.co/nwZqL9pGeb.

For those interested in collaborating on this company and others, feel free to join our Breakout Investors WhatsApp group here: https://t.co/Z59FkSf2Ct

Interesting acquisition by $MHUB.V. Strengthening their offering along the supply chain, and increasing the customer base.

Dilution ~10%.

https://t.co/Qv0JaLh4to

Nordic Semiconductor

@jeffmeyers72

"Nordic Semiconductor is poised to accelerate revenue growth and margin expansion due to the launch of its new line of cellular Internet-of-Things products."

https://t.co/86bli5jLyo

(1/2)

I think these are the most interesting (and not well-known) disruptive innovation companies listed on public markets:

-Verde Agritech ( $NPK.TO)

-Graphene Manufacturing Group ( $GMG.V)

-XTPL ( $XTPL)

-Mustgrow Biologics ( $MGROW.V)

-Minehub ( $MHUB.V)

-Intrusion ( $INTZ)