Personal update: I've joined Anthropic. I think the next few years at the frontier of LLMs will be especially formative. I am very excited to join the team here and get back to R&D. I remain deeply passionate about education and plan to resume my work on it in time.

The Obituary, As Usual, Is Premature. (Read the Plumbing, not the Panic!)

As @Cheytax_1 flagged, X timeline suddenly thick with Macro Reads, most engineered for Doom Bait, distorting proper signal. Every twelve years Indonesia is declared finished. 1998. 2013. Now 2026. The reading is reliably wrong, this is not a default event. Hardly. It is a Market Premia Repricing, made uglier by improper Govt Navigation.

But should capable hands of Jakarta wake up, easily Passable. For the time now that it is not, we read, we positioned. Below :

The Premises :

Jakarta would remain Logical and Current, all tools at their potent disposal (Yes Even Cutting Expenses is a tool)

Exchange Rates, and Real Rate Differential. Is means of shock absorbing. Even measured depreciation is preferrable to exhausting import cover ratio. Coming out of the shock, cycle begin anew. Business as usual, Indo was operating under this macro anchor. In SMI era.

Picture 1 - The Gravitational Field

Picture 2 - The Pragmatic Opportunity

3 year forward 10Y USD swap rate at 4.2% sits a hair below the 4.4% post 2013Taper peak meaning the market priced higher for longer not as a cycle but as new resting heart rate of dollar liquidity. For Indonesia this matters in every rupiah of sovereign refinancing, every dollar of corporate rollover, every BI reserve calculation now lives under a permanent ~150bp uplift in the global riskfree rate versus the 2010s. The "free money" world that incubated Indonesia's foreign-investor SBN share is gone, 14% presence now to the peak of 39,% back then. the forwards say it is not coming back any soon.

EM/US fair value gap at +1.3%, but Indonesia having wider premia asked is with reason. IndoGB is generously priced versus fair value, because fair value itself has deteriorated: fiscal trajectory, capital account outflow, reserve drawdown, and BI that held 4.75% since October not out of conviction while defending through FX. The carry is real. Our "fair value" anchor moves.

The dissonance and finance plumbing :

Onshore INDOGB Comrades, Favor belly of the curve, not long end. The fiscal supply is structural; The 5-7Y sector gives most of the carry.

Timing.

optionality on BI's reaction function. If BI hikes 25bp next week, another 25-50bp post fuel hikes. front end shall reprice and IndoGB curve bear flattens, Position for the curve shape.

Three rules for this cycle.

One: do not confuse repricing with default.

Two: do not confuse fiscal drift with collapse.

Three: do not confuse a noisy timeline with a thesis. Jakarta has tools, history, and capable hands waiting to be used. Onshore, we earn the carry, shorten the duration, and wait for the curve to do the work. Pragmatism is alpha when everyone else is selling doom poetry.

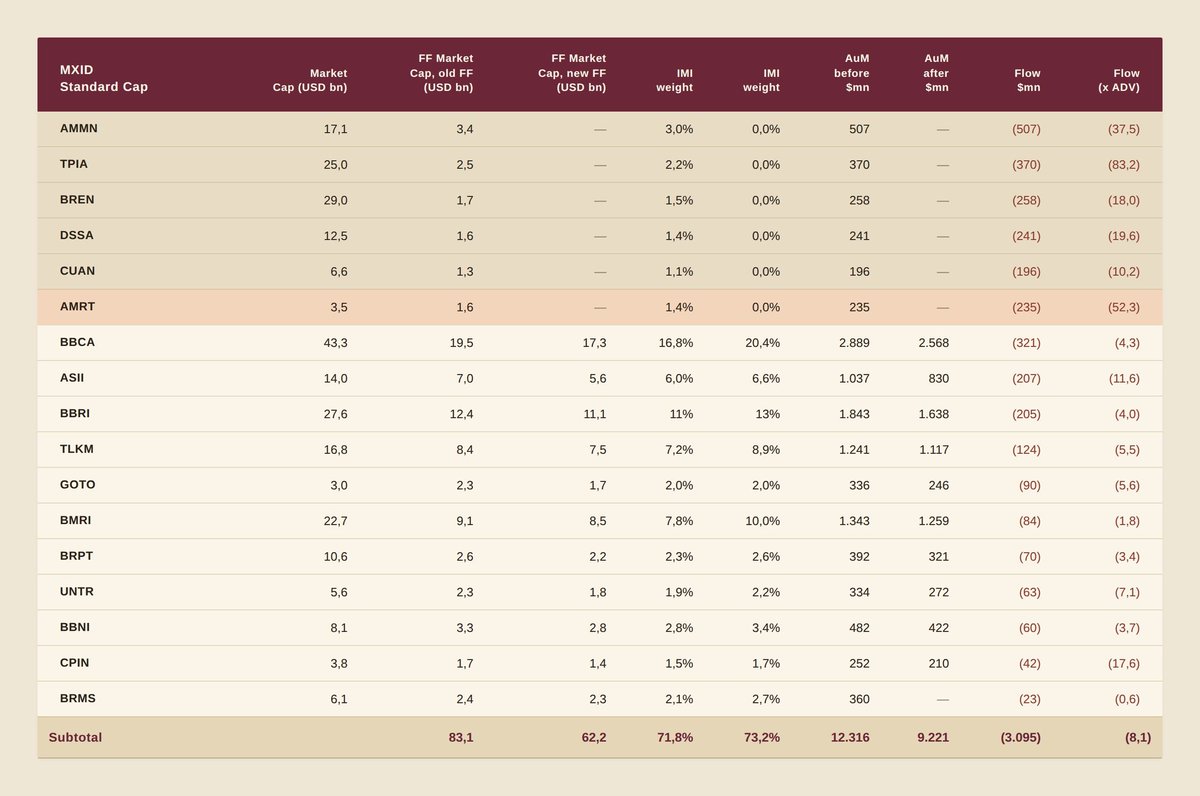

Event Horizon : Larger Downweight, Concentrated on The Scallywags. Shiver me Timber IDR Impact 😵💫

Verdict: Material negative impact. US$3.45bn aggregate passive outflow,

Est. outflow $3.45bn

Standard Cap $3.1bn

Small Cap $353mn

Est. Indonesia weight in MSCI EM IMI to decline from 0.86% to 0.63%

Concentrated in six Standard Cap deletions, with TPIA carrying outsized liquidity stress at 83x ADV.

Total estimated passive outflow lands at US$3,448mn Standard Cap drives US3,095mn (90%), Small Cap contributes US353mn. AuM tracking Indonesian equities via MSCI Indonesia IMI compresses from US13.6bn to US10.2bn, a 25% decline in passive footprint. no longer marginal rebalance; it is the largest single-event Indonesia outflow since I remember, at Rupiah vantage point no less.

Barito complex takes a combined almost US$ 1Bn hit, testing their mettle in midst of real business capex cycle. This is one open corpfin class to observe.

BBCA & BBRI, Reprieve. outflow under $500Mn each. MSCI surprisingly fair on these. Local Money (ReksaDana) has been playing underweight ahead, this posit for their imminent cover window so natural domestic Bid should clear absorbs.

AMRT, Net Inflow. Dang Everyone Were Ready to Catch the Knife, But Pa Joko count his luck parlay.

AMMN, the endearing bless in disguise. Rare occasion of revulsion entry at "near fair price level", operating leverage right before industry structural uplift.

Bottom line: this is a high impact, low ambiguity passive event. More FX Impactful than I thought before. Patience Capital Remain Deployable on Mechanical Flush Event but Position sizing and execution windows should be wiser. 4-5 Days Execution

invoke your inner templeton, jangan lupa sarapan pondasi!

Circles on Circles - Invoke 97-00

Kalo Fintwit mau draw Parallel sekarang ke 97? Coba Mundurin sedikit, ke 95 nya dulu, Mexican Tequila! Moral Hazard impor dari situ, Meksiko tumbang - brady bond backstop. Mata Uang EM di Peg. Capital ngalir pindah ke Asia. 95 Everything is fine

Vibe-trading digital oil is like vibe-hedging in treasuries during Hormuz risk-off. Both share one house of cards that works on paper.

Difference: oil at least has Dated Brent. Treasuries? Vibes all the way down.

EUCRBRDT Index GP <GO>

In line with the ceasefire in Lebanon, the passage for all commercial vessels through Strait of Hormuz is declared completely open for the remaining period of ceasefire, on the coordinated route as already announced by Ports and Maritime Organisation of the Islamic Rep. of Iran.

Introducing Claude Opus 4.7, our most capable Opus model yet.

It handles long-running tasks with more rigor, follows instructions more precisely, and verifies its own outputs before reporting back.

You can hand off your hardest work with less supervision.