One thing about the World Cup, especially if you have some friends all around the world like I do.

Show some respect. It’s not your job to comment on everything and you are unlikely to add value.

I saw games without Argentina, with of our historic rivals and didn’t go around celebrating their losses or lamenting their wins or questioning refereeing.

Some people are pathetic. So little.

Excited to FINALLY release toughest+most rewarding paper I've worked on...

….we attack a 150 year old Walras question that's gone unanswered, not for lack of trying (Hicks, Samuelson, Arrow; our chances?😱)...

Q: Is the market equilibrium stable or unstable?¯\_(ツ)_/¯

🧵

La magnífica humanidad que Dios ha creado se encuentra hoy ante una elección decisiva: levantar una nueva torre de Babel o edificar la ciudad donde Dios y la humanidad habiten juntos. En Jesucristo, esta magnífica humanidad encuentra el camino, la verdad y la vida, abriendo a cada uno de nosotros la vía para crecer hacia la plenitud. #MagnificaHumanitas

https://t.co/Ple93kfbB8

📢 The 21st Economics Graduate Students Conference (EGSC) at Washington University in St. Louis is now accepting submissions!

-Conference date: October 10th, 2026

-Submission deadline: July 19th, 2026

Submit and learn more at: https://t.co/InJIb7N9my

Email: [email protected]

Online Summer School:

If you or your student(s) want to join, please register soon! (It's free, but hard and rewarding work esp. for current and future PhD students) https://t.co/oryNoRLItO

Agradecemos y respaldamos a @MRE_Bolivia en su respuesta a las expresiones desafortunadas realizadas por el Embajador @AmbRichPorter en @UKinBolivia con motivo de la participación del Vicecanciller boliviano en el acto de conmemoración del día de Veteranos y Caídos en el Conflicto del Atlántico Sur y su posterior comunicado.

La Cuestión Malvinas no es sólo argentina, es fundamentalmente una causa regional.

Gracias Bolivia por el histórico y valioso apoyo a la Argentina en esta Cuestión.

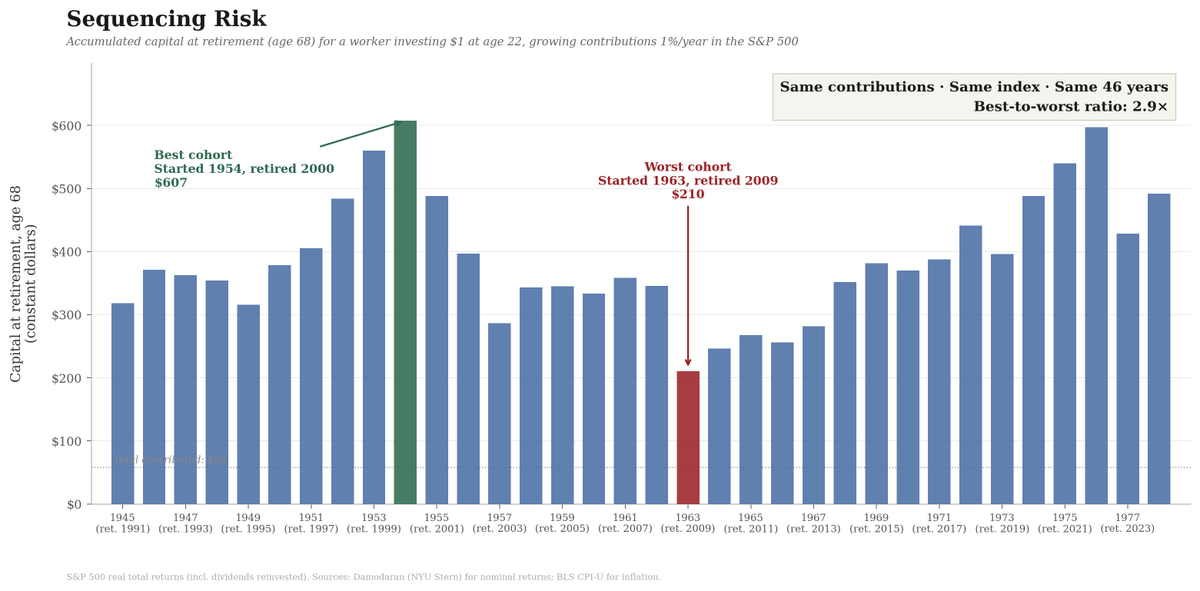

I am always amazed that most people saving for retirement (or designing optimal Social Security systems) rarely take sequencing risk seriously. Simply put, sequencing risk is the risk associated with the order in which returns arrive over one’s lifetime.

Sequencing risk hits you twice: while you are working and accumulating wealth, and again while you are retired and drawing it down. Today, I will focus on the first part. The retirement phase warrants its own discussion, and I will address it in a subsequent post.

Let me walk you through an exercise I ran yesterday using actual historical U.S. stock market data from the past 80 years to illustrate how important sequencing risk is.

I took the annual total returns of the S&P 500 (including reinvested dividends) from 1945 to 2024. The source is the dataset maintained by Aswath Damodaran at NYU Stern, a standard reference for long-run U.S. equity returns. I then deflated each year’s nominal return by the CPI-U inflation rate published by the Bureau of Labor Statistics to obtain real total returns, i.e., returns in constant purchasing power.

Over this 80-year period, the S&P 500 delivered a geometric mean real total return of about 7.5% per year. That is an impressive number. But this average return masks a lot.

Imagine a worker who starts investing at age 22 and retires at age 68. That gives them 46 years of contributions. In their first year, they contribute $1. Each subsequent year, they increase their contribution by 1% (roughly keeping pace with real wage growth). Every dollar is invested in the S&P 500. They never touch the money until retirement. No panic selling, no market timing, no strategy switching (and no management fees!). Textbook investing and waiting.

I ran this exercise for every possible cohort for which the data allow. The first cohort starts investing in 1945 and retires in 1991. The second starts in 1946 and retires in 1992. And so on, all the way to the last cohort, which starts in 1978 and retires in 2024. This yields 34 cohorts, each investing for 46 years, making the same contributions and investing in the same index. The only difference among them is which 46-year slice of historical returns they happen to live through.

The most fortunate cohort, the one that started investing in 1954 and retired in 2000, had $607 on the day of retirement (remember, all in real terms), with a real annual return of 8.82%. The unluckiest cohort, the one that started in 1963 and retired in 2009, accumulated $210, with a real annual return of 4.83%. Same contributions. Same index. Same strategy. Same investment horizon. Yet the luckiest retiree ended up with 2.9 times more wealth than the unluckiest.

Why? The 1954 cohort had a spectacular final decade. The late 1990s delivered some of the best equity returns in American history, and those returns compounded on a large portfolio built over decades. They retired at the peak, at the end of 1999, before the dot-com crash. The 1963 cohort was not so fortunate. They spent their last working years running straight into the 2008 financial crisis. The S&P 500 lost over 36% in real terms in 2008 alone. That loss hit their portfolio when it was at its largest, right before retirement, with no time left to recover.

Clearly, sequencing risk is not about the average return. Both the 1954 and 1963 cohorts experienced roughly similar average returns over their 46-year periods. The difference is when the good and bad years occurred. For the 1954 cohort, the bad years came early (when the portfolio was small) and the good years came late (when the portfolio was large). For the 1963 cohort, the opposite was true.

In fact, sequencing risk is even worse because poor returns in the stock market are correlated with weak labor markets: you have a much higher probability of losing your job (or seeing your wage income fall) precisely when the market is doing poorly, preventing you from saving when prices are low and equities are most attractive. However, let me set that point aside today to simplify the exposition.

The standard response of the financial planning industry to sequencing risk is the so-called glide path. The idea is simple: when you are young, you hold mostly equities. As you age, you gradually shift toward bonds. By the time you are near retirement, most of your portfolio is in bonds. A common implementation is a linear rule: start with 90% in stocks at age 22 and reduce the equity share steadily until you reach 20% in stocks at age 68. This is roughly what target-date retirement funds do.

The logic is sound in principle. You reduce your exposure to equities precisely when a crash would hurt you most. If 2008 happens when you are 65 and 80% of your portfolio is in bonds, the equity crash barely affects you.

I applied this glide path strategy to the same 34 cohorts, using historical real returns on the S&P 500 for the equity portion and real returns on 10-year U.S. Treasury bonds (from Damodaran) for the bond portion. Each year, the portfolio is rebalanced to the glide path weights.

The glide path does what it is intended to do: it reduces dispersion. The gap between the best and worst cohorts narrows from 2.9x under pure equities ($607 vs. $210) to 1.6x under the glide path ($292 vs. $178), but so does the upside. The best equity cohort (1954–2000) earned a geometric mean real return of 8.82% per year. The best glide path cohort (1975–2021) earned 6.59%. That is a 2.2 percentage point gap. Over 46 years of compounding, a 2.2 percentage-point annual yield yields an enormous difference in terminal wealth: the best glide-path outcome ($292) is less than half the best equity outcome ($607).

In other words, the cost of this insurance is substantial. In fact, the median cohort ends up meaningfully poorer under the glide path than under 100% equities. You are not trimming a bit of upside. You are forgoing a substantial share of your expected wealth at retirement.

This should not be surprising. Over the long run, equities have outperformed bonds by a wide margin. The equity risk premium is one of the most robust facts in finance. Every year you shift a dollar from stocks to bonds, you accept a lower expected return. Do this for 25 years of your career (roughly the back half, when the glide path has you increasingly in bonds), and the cumulative cost from foregone compounding is very large.

But the part that makes me most uncomfortable with the standard glide path advice is that bonds are not safe. People hear “bonds” and think “safe.” They are not. Bonds carry two risks that are easy to forget when inflation is low and interest rates are stable.

The first is inflation risk. A conventional bond pays you a fixed nominal coupon (yes, there are TIPS and similar instruments, but they have their own problems, so let me skip them for today). If inflation rises above the market’s expectations when the bond was issued, the real value of those payments declines. The cohorts that retired through the 1970s learned this the hard way. In the data, the real return on 10-year Treasuries was negative in multiple years during the 1970s.

The second is interest rate risk. When interest rates rise, the market value of existing bonds declines. The longer the maturity of your bond, the larger the hit. In 2022, the Bloomberg U.S. Aggregate Bond Index declined by approximately 19% in real terms. If you were 65 and had just shifted most of your portfolio into bonds following the standard glide path advice, you would have lost nearly a fifth of your “safe” allocation in a single year.

And here is the real sting of 2022: equities fell, too. The S&P 500 lost about 24.5% in real terms that year. The glide path assumes bonds will be there to cushion you when stocks fall. In 2022, both fell together. The cushion was not there. This is not some once-in-a-century event. Stocks and bonds have moved in the same direction before: the 1940s, the 1970s, and in 2022. The negative correlation between stocks and bonds that many investors take for granted is a feature of the disinflationary period from roughly 1982 to 2020. It is not a law of nature.

Let me be clear: I am not saying the glide path is wrong. For many people, it is the right choice. If a 30% equity crash near retirement would force you to sell assets at the worst possible time to cover living expenses, the insurance is worth paying for.

However, you should know what you are paying. The glide path (or variations of it that I am skipping in the interest of space) is not free. It entails substantial costs in expected returns. Worse, the insurance itself can fail. Bonds can lose money in real terms for extended periods. Bonds can fall at the same time as equities. The glide path reduces sequencing risk. It does not eliminate it. It also introduces risks of its own.

The deeper lesson from this exercise is that a substantial part of your retirement outcome depends on when you are born. You can do everything right (save diligently from your first paycheck, invest consistently, stay the course through every crash, never panic sell) and still end up with vastly different results than someone who did the same thing a decade earlier or later. The 1963 cohort did nothing wrong. They just had the misfortune of turning 68 in 2009.

No allocation strategy eliminates this. Even under the glide path, the best cohort ends up with substantially more than the worst. Sequencing risk is, to a significant extent, a matter of luck.

Next time: what happens when sequencing risk hits you in retirement, when you are drawing down instead of building up. The math there is, if anything, even more unforgiving.

A guide for students of economics: Ten statements that demonstrate that someone does not understand modern economics or what an equilibrium is, and that you can safely ignore everything else they say.

1. “Equilibrium means the economy is stable or at rest.”

Many assume that an equilibrium is a peaceful state with no forces at play. Instead, an equilibrium is just an arrangement of actions and expectations over time that are mutually consistent. It can be locally unstable, explosive, or fragile. Nothing in the definition of equilibrium implies stability.

2. “Equilibrium implies optimality or social efficiency.”

Equilibrium is often conflated with efficiency, but equilibrium merely reflects decentralized consistency, not welfare maximization. Market power, externalities, incomplete markets, nominal rigidities, and frictions routinely produce inefficient equilibria. I often teach a first-year macro graduate course, and not a single one of the equilibria I define is efficient.

3. “Equilibrium is a unique outcome.”

Many often expect models to have one equilibrium. In reality, multiple equilibria arise naturally in dynamic, strategic, and incomplete-market environments. Models of coordination failures, self-fulfilling expectations, bubbles, overlapping generations, and liquidity traps all hinge on the existence of equilibrium multiplicity.

4. “Equilibrium requires perfect foresight or perfect information.”

Equilibrium does not assume agents know the future. In fact, equilibria are often stochastic. The definition of equilibrium only requires that beliefs are consistent with the (perceived) stochastic laws of motion implied by the model. Bayesian learning, noisy signals, ambiguity, and subjective uncertainty all fit well within an equilibrium framework, provided beliefs converge to an internally consistent (but possibly incorrect) distribution.

Bonus point: equilibria are compatible with agents having diverging beliefs that never converge to a single Dirac distribution.

5. “Real economies are rarely in equilibrium, so the concept is unrealistic.”

Equilibrium is not meant to describe the daily state of the world. It is a conceptual device used to understand the outcome of our models under the assumptions we make. Also, see point 1 above.

6. “Equilibrium requires agents to be fully rational in a psychological sense.”

Equilibrium only assumes internal consistency: agents optimize given preferences and constraints. It does not assume realism about human cognition. We can and do define equilibria in models with behavioral biases, bounded rationality, inattention, or rule-of-thumb behavior. We only need to ensure that the resulting actions and beliefs are mutually compatible.

7. “Equilibrium eliminates dynamics or learning.”

Equilibrium is sometimes misinterpreted as a static state in which nothing evolves. In fact, many equilibria are sequences of probability distributions over states driven by shocks, policy rules, and endogenous responses. Learning dynamics (Bayesian updating, adaptive rules, experience-based expectations) can occur within equilibrium if the evolution of beliefs is self-consistent.

8. “Equilibrium renders expectations unimportant.”

A common misconception is that equilibrium mechanically determines outcomes. In reality, expectations are often central: they determine investment, consumption, asset prices, and policy responses. Many equilibria differ only in their expectations. This is why communication, credibility, and forward guidance matter even in fully rational models.

9. “Equilibrium excludes policy intervention.”

Some interpret equilibrium as a laissez-faire concept. In fact, equilibrium analysis is the foundation of modern policy evaluation. Fiscal, monetary, and regulatory interventions work through equilibrium responses (prices, wages, interest rates, quantities) and must satisfy equilibrium conditions to be credible. Equilibrium is a tool for policy design, not a barrier to it.

10. “Equilibriums…”

Aequilibrium is a Latin neuter noun of the second declension, which forms a nominative plural in “a”. It is composed of aequus (equal; the same root as equality or equity) and libra (balance or scales or the name of several currencies over history).

A final thought: “equilibrium” is a term of art. Its meaning in economics differs from its use in the natural sciences or in everyday language. Terms of art are ubiquitous across academic disciplines, and the first act of intellectual diligence when one starts studying a discipline is to learn what they mean.

Reforma laboral en Argentina. Importantisimo.

Un concepto importante: si intentas proteger al trabajador se reduce el incentivo a la contratación y la eficiencia del mercado labora.

Acá uno de los mejores papers sobre este tema escrito por un gran economista argentino.