Takeaways from spending a day with some of the smartest energy people on the planet:

🛢️ The risk of a US product export ban is real if the national average gasoline price hits ~$5/gallon

🛢️the most important questions to come up at dinner were "how does this end?" and "why would Iran give up the Strait at this point?"

🛢️base expectation broadly is the Strait will NOT reopen soon as neither party is feeling enough pressure and both sides believe they are winning - military reopening not politically palatable and lacks European buy-in (you broke it, you fix it)

🛢️I believe the Kuwaitis, Saudis, and Emiratis will NOT ship through the Strait under an Iranian toll system. Incremental workarounds underway with more to come but will take years...Strait oil exports will never reach past levels

🛢️many expect US tank bottoms in July and US SPR to approach minimum operating levels in July/August (!) - the US has front-loaded emergency responses not having expected the closure to last as long as it has and now has limited recourse after July - Presidential jawboning has made the imbalance worse as demand has not yet been impacted. Regional product shortages are being masked (bring your own jet fuel)

🛢️skepticism around available data - China believed to be drawing from SPR even though satellite data does not show and Strait voyages OUT believed to be potentially higher than reported

🛢️how long will it take for production to recover? Weeks/month for majority (~80%) for KSA, UAE, Kuwait, the last 20% is the hardest, and big question mark for Iraq (~2.9MM Bbl/d shut-in) given geology and bureaucracy

🛢️biggest reason why the expected shortage has been delayed? Chinese drop in imports of ~4.0MM Bbl/d leveraging their SPR. Much skepticism around reported demand "destruction" of 5MM Bbl/d

🛢️Net/net: bullish near-term oil price with significant frustration on price action. "New normal" ahead with energy security priority 1, 2, and 3 = increased influence of Western Hemisphere (ie. Canada if we seize it). Many oil stocks discounting <$65WTI with an expected floor price of $75-$80 in 2027+

🚨 WARNING: MONDAY COULD BE THE WORST MOMENT OF 2026!!

Make sure to take a look at this before June 8, that’s tomorrow.

The $SPCX IPO is coming on June 12.

And markets open this Monday, June 8.

This is the first real trading week before one of the biggest IPO events in market history.

SpaceX is expected to go public at around $1.75 TRILLION to $2 TRILLION valuation.

That one number explains everything.

Because money does NOT appear from nowhere.

If funds want to buy $SPCX, they need cash.

And where does that cash come from?

They sell what they already own.

Stocks will dump.

Crypto will dump.

High beta tech will dump even harder.

This is NOT just an IPO.

This is a liquidity drain.

Everyone sees the Elon hype.

Almost nobody sees the forced selling.

There are only a few ways this goes from here, and they are NOT equal.

- LIGHT SHOCK: funds sell small positions, stocks get hit first, crypto follows, then markets try to stabilize.

- HEAVIER SCENARIO: funds raise cash before June 12, high beta tech dumps, Bitcoin loses support, and retail gets trapped.

- WORST CASE: everyone rushes into $SPCX at the same time, liquidity disappears from crowded trades, stocks dump HARD, crypto gets hit first, and people get liquidated.

That last one is the REAL danger.

Because none of this is happening in a vacuum.

Stocks are already crowded.

Crypto is already weak.

Liquidity is already getting worse.

And now one of the most hyped IPOs in history is about to absorb even more money.

Now connect the dots.

If everyone wants $SPCX, they need dollars.

To get dollars, they sell assets.

And when everyone sells at the same time, markets do NOT dip slowly.

They dump.

This is NOT a theory.

The $SPCX IPO is June 12.

Markets open Monday, June 8.

And this is when positioning starts.

Markets are NOT pricing the liquidity drain now.

But they will.

I usually do the opposite of what the masses are doing.

Reminder: I’ve called all the market tops and bottoms for the last 15 years, including the Bitcoin bottom at $16,000 and the top at $126,000.

The next call will be even more important.

When I exit the markets completely, I’ll post it here publicly like I always do.

Turn notifications on. If you’re not following yet, you’ll understand why that was a mistake later.

A thought

In the 1950s to the 1970s, information channels were so scarce that even the most studious investor, reading the same New York Times as everyone else on the morning commute, inevitably absorbed the same narrative, producing classic groupthink.

Today, I fear we might be recreating that exact dynamic at digital speed: millions of users generate daily AI briefings with near-identical prompts fed into overlapping models, receiving essentially the same market summaries, signals, and conclusions.

The result? A new era of synchronized thinking, just like 50–70 years ago, when alpha generation was far higher precisely because consensus created exploitable edges.

Independent thinkers who step outside the AI echo chamber will soon regain that same advantage.

Active stock-picking is poised for a comeback.

----

The era of Google searches, circa 2005 to 2024, was always ad hoc, so they never produced groupthink on the level we saw in the 1950s, and may see again.

(AI image of what I'm arguing)

🚨The US private credit CRISIS is spreading to the largest funds in the industry:

Blackstone's $79 billion Private Credit Fund capped redemptions at 5% in Q2 2026 after investors requested to withdraw 10% of assets, marking the first time Blackstone has ever gated this fund, according to Bloomberg.

This follows last quarter when Blackstone allowed the full 7.9% of requested redemptions by having senior executives contribute hundreds of millions of their own cash to fund the withdrawals.

Meanwhile, Cliffwater also capped redemptions at 5% after investors requested 17% back, and Partners Group reported 9.8% redemption requests, confirming this is now a market-wide crisis across the entire $2 trillion private credit industry.

Redemption requests are expected to increase further in Q3 as investors who were restricted in Q2 redouble efforts to reclaim their capital, with market leaders warning of a potential rise in defaults as AI continues to disrupt software-dependent borrowers.

When even Blackstone starts gating investors, the private credit industry has a serious problem.

These FT charts capture the core variables in the US "fundamentals" tug-of-war: a large, growing debt burden versus the outlook for higher productivity and growth—essentially, debt obligations vs. the capacity to meet them.

This dynamic is complemented by risk-adjusted valuations (including US debt relative to the rest of the world), technical issues (such as issuance versus available investible funds), and socio-political factors.

Altogether, it forms an equation that is becoming increasingly less sustainable, though it remains unclear just how close it is to a truly unsettling tipping point.

#economy #markets #debt #growth @FT

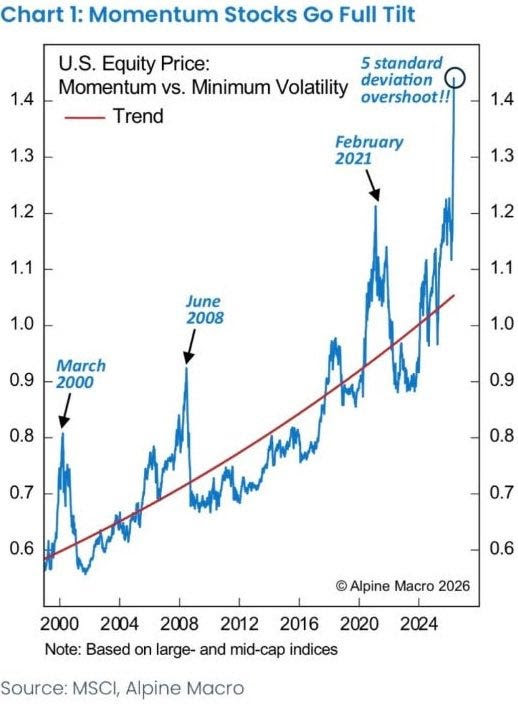

🔴THIS HAS NEVER HAPPENED BEFORE:

US technology and communication services sectors now reflect a RECORD 50% of the S&P 500's market cap.

Since 2018, this percentage has more than DOUBLED.

By comparison, at the 2000 Dot-Com Bubble peak, the tech share was ~44%.

Meanwhile, 12 companies accounted for 12.2 percentage points of the S&P 500's +16.3% total return in April and May.

The level of market concentration is absolutely huge. For how long can this last?

No cabe duda que entre los peores enemigos del “movimiento” de la 4T están los hijos de López Obrador. Con sus decisiones, su estilo de vida y la imagen que proyectan, contradicen la lucha contra los privilegios y traicionan los principios de austeridad que la Cuarta Transformación dice representar.

Michael Burry is short Nvidia, 1 million shares. His case: three customers now owe it 64% of receivables, and the biggest is paying slower while buying less. The same three are building their own chips to need it less. He calls it a finger on the trigger.

Three customers. 64% of the money Nvidia is owed.

The investor who shorted the 2008 housing crash just bought puts on 1 million Nvidia shares, and that one number is the reason.

It is not the size that matters. It is the slope. Those three were 33% of Nvidia's receivables in 2020. They were 56% last quarter. They are 64% now. The dependence has nearly doubled in six years, and 8 of those points landed in a single quarter.

Here is the part the headlines skip. The money Nvidia is owed is now more concentrated than the money it earns. For the first time in 13 quarters, its single biggest customer claimed a larger share of receivables while taking a smaller share of sales. Burry's read: that buyer is paying slower than it is buying, or orders got pulled forward. His phrase for it, a finger on the trigger.

His thesis: today's AI spend is a benchmarking race, not durable demand. Empty planes flown for the leaderboard. Nvidia has fallen 43% to 67% in past cycles, and he thinks the next one is worse.

And the same three giants are building their own chips, Google's TPU, Amazon's Trainium, Microsoft's Maia, to need Nvidia less every year.

Now the bull case, and it is real. Nvidia discloses all of this by law, still collects its cash on time, and is rated 39 buys to 1 sell. The cloud giants have lined up $660 to $700 billion of AI spending this year alone.

So this is concentration, not a crime. One of those three delaying, renegotiating, or shifting to its own silicon would hit the most important cash flow in the market harder than anything else. A real fragility. Not proof the demand is fake.

The test is the next filing, in August. If the three slip back under 60% and the cash keeps flowing, Burry is early. If their share climbs or payments slow, the finger tightens.

The number is real, and Nvidia disclosed it. Whether it is a warning or just arithmetic is what the next two quarters decide.

De confirmarse lo de Durazo, sería letal para AMLO y Sheinbaum. Sería el García Luna de Morena. Les recomparto el texto de @stevelfisher en @latimes. https://t.co/guU0qtOZF6

Les quitaron la visa a los gobernadores morenistas Alfonso Durazo de Sonora y Américo Villarreal de Tamaulipas, revela el diario @latimes. Durazo además es presidente del Consejo Nacional de Morena.

El reportaje señala que han entrado a Estados Unidos bajo una condición llamada Utilidad Pública Significativa, que suele usarse para quienes están cooperando con las autoridades en casos criminales.

https://t.co/3JLfx04tPM

Private credit stress doesn’t transfer to an independent balance sheet at arrival, but to a balance sheet controlled by the same entity that originated the exposure.

Apollo owns Athene. KKR owns Global Atlantic. Blackstone controls FGL Holdings. Ares has insurance relationships.