🇺🇸 DATA MACRO U.S 🇺🇸

This week we had some important data to watch regarding the macroeconomic health of the U.S :

🔹PCE

🔹GDP

🔹Durable Goods Orders

🔹Jobless Claims

A quick note on the current macro environment before getting started.

Although a peace agreement was signed between the U.S. and Iran, the situation in the Strait of Hormuz remains unstable, as evidenced by what happened this past weekend.

Following an Iranian drone strike on a tanker crossing the strait, the U.S. conducted strikes yesterday on strategic Iranian targets.

➤ As a result, vessel traffic through the strait dropped sharply again, falling to just 24 ships.

At the same time, PCE data confirmed sticky inflation, with Core PCE rising 0.1 points, alongside growth that came in better than expected even amid the ongoing conflict.

➤ This situation puts the Fed in a highly complex position, and the reaction among FOMC members was clearly reflected in June's dot plot, where no rate cuts are anticipated any longer, the median has even shifted toward a rate hike.

The U.S. economy has shown resilience so far, which has helped limit collateral damage, but it is not certain this will last, particularly if the conflict with Iran were to resume and the ceasefire were to break down.

Let's break this down together 👇

(Don't forget💜and 🔁)

Aujourd'hui je vous propose un post un peu long, mais il me semble nécessaire car c'est tout à l'heure qu'on vote l'euro numérique en commission économique au Parlement européen.

Le vote en séance plénière aura lieu début juillet. Le projet, lui, ne serait lancé qu'à partir de 2029.

Je n'ai jamais caché mon hostilité à ce projet. Mais je comprends toutefois qu'il séduise ceux qui ont pris conscience, parfois brutalement, des dépendances de nos systèmes de paiement en Europe.

L'histoire rocambolesque du juge de la CPI, quasiment débancarisé depuis qu'il est tombé sous sanctions américaines, a marqué les esprits.

Ce que je vous propose ici, c'est une démonstration factuelle.

Même s'il repose sur une idée louable, l'euro numérique menace le modèle économique du paiement européen.

Et les chiffres, franchement, posent question.

Commençons par la facture.

Côté Eurosystème, la BCE chiffre l'investissement à environ 1,3 milliard d'euros jusqu'au lancement, puis 320 millions par an en fonctionnement. Ça, c'est la partie publique. Côté banques commerciales, la note sera autrement plus salée : refonte des systèmes d'information, intégration des wallets, mise en conformité réglementaire.

Plusieurs estimations internes tournent autour de 18 à 30 milliards d'euros cumulés pour l'ensemble du secteur. PwC évalue la dépense moyenne à 110 millions d'euros par banque, dont 75 % liés à la refonte des infrastructures techniques. Les établissements estiment aussi que près de la moitié de leurs ressources humaines qualifiées devraient être mobilisées sur le projet pendant plusieurs années, ce qui revient à assécher leurs capacités d'innovation et de développement commercial.

Malgré un affichage de façade, la France n'est pas favorable au projet, et surtout pas son administration (Banque de France, Trésor, etc.). "Le modèle envisagé ne sera probablement pas rentable. On parle d'une entité publique qui va essayer de reproduire des systèmes de paiement privés dans lesquels des milliards ont été investis depuis des années, sans forcément en mesurer la complexité", m'a récemment confié un cadre de cette dernière.

On m'a aussi soufflé ceci : "Les pilotes n'ont jamais été confrontés à des attaques réelles. Dans la vraie vie, un système de paiement à grande échelle doit encaisser 0,15 % de fraude sur les transactions en ligne. Ça nécessite des algorithmes que le privé a mis des années à construire. Sans ça, on crée un système qui coûte cher, qui ne fonctionne pas et qui est une cible facile."

Le risque le mieux documenté reste la fuite des dépôts.

Une étude de Copenhagen Economics, publiée en décembre 2023, évalue la décollecte maximale à 739 milliards d'euros en Europe pour un plafond de détention fixé à 3 000 euros. C'est 10 % du total des dépôts des ménages. Le Sénat français a produit ses propres simulations : à ce même plafond, la décollecte moyenne atteindrait 20,7 % pour les banques françaises, avec des pics à 25,7 % pour La Banque Postale.

La BCE elle-même reconnaît qu'un tel seuil réduirait le rendement des fonds propres bancaires de 30 points de base en moyenne. Pour un secteur dont le coût du capital est déjà sous tension, on parle d'un transfert de valeur considérable de la banque commerciale vers la banque centrale.

Or le point le plus sous-estimé dans le débat est peut-être celui de l'effet d'éviction sur les solutions privées européennes.

La France fait figure d'exception dans la zone euro : le GIE Cartes Bancaires traite environ 80 % des paiements domestiques par carte, une infrastructure de paiement souveraine qui fonctionne réellement. Wero, porté par le consortium EPI et ses 16 banques, revendique déjà 47 millions d'utilisateurs en Europe. Le service s'étend au e-commerce en 2026 et prépare l'intégration du NFC pour les paiements en boutique.

Wero construit exactement ce que l'euro numérique promet : un rail de paiement paneuropéen souverain, basé sur le virement instantané, de compte à compte.

Le problème est assez simple.

L'euro numérique bénéficiera d'un avantage réglementaire structurel : l'obligation d'acceptation par les commerçants au titre du cours légal. Wero, lui, doit convaincre chaque marchand un par un. Résultat : les banques devront financer simultanément deux infrastructures pour des cas d'usage largement redondants, avec des ressources qui auraient pu servir à améliorer un seul système.

Martina Weimert, la patronne d'EPI, parlait récemment de "situations de concurrence inégale" lors d'une table-ronde à laquelle j'ai participé.

Le rapporteur du texte, Fernando Navarrete (PPE), va plus loin : il plaide pour soutenir les initiatives privées plutôt que de dépenser "plusieurs dizaines de milliards qui pourraient devenir inutiles si une solution du secteur privé atteint une échelle paneuropéenne avant même que la BCE ne soit prête".

C'est le paradoxe central du projet.

L'euro numérique a été conçu pour réduire la dépendance de l'Europe vis-à-vis de Visa et Mastercard, qui concentraient 61 % des transactions par carte dans la zone euro en 2022.

L'objectif de souveraineté est légitime.

Les épisodes récents l'ont rappelé, qu'il s'agisse des sanctions américaines contre un magistrat de la CPI ou des tensions commerciales entre l'UE et les États-Unis : les rails de paiement peuvent devenir un levier géopolitique.

Mais en imposant une solution publique à côté de solutions privées européennes déjà opérationnelles, Bruxelles prend le risque de diluer les investissements, de fragmenter l'écosystème, et au bout du compte d'affaiblir les seuls acteurs capables de proposer une alternative crédible à court terme.

Ma source dans l'administration est claire : "On a des infrastructures de paiement qui marchent. Le réseau CB en France, par exemple. Le risque, c'est qu'un euro numérique subventionné vienne les détruire sans apporter de vraie plus-value. Et qu'en 2035, on regarde en arrière en se disant qu'on a dépensé une fortune pour un projet qui n'a jamais atteint ses objectifs."

Il y a une ironie certaine à vouloir défendre la souveraineté européenne en asséchant les ressources des acteurs privés qui la construisent déjà, jour après jour.

L'enjeu du vote d'aujourd'hui n'est ni simplement technique ni monétaire. C'est un arbitrage industriel : l'Europe veut-elle un Airbus des paiements piloté par le marché, ou un projet public qui risque d'arriver trop tard, trop cher, et de cannibaliser ses propres champions ?

I am stocked to announce that I won the @OpenAIDevs Codex x Mollie Hacka Worldwide Hackathon in Paris. 60+ builders, every one of us working solo, one day to ship.

I built mine around a single question: who gets to own intelligence?

The default answer is scary. You hand your data to a handful of labs, they train the model, they own it, and you rent back a thin slice of what your own data made possible. That is the bargain on the table today. I do not accept it.

So I built Lensemble: a Tapestry like distributed training platform for JEPA based World Models.

What does it enable: World Models that a community improves together, keeps sovereign, and co-owns.

Two bets sit underneath it.

First, the paradigm.

Language models predict the next token. Powerful for text, a dead end for the physical world. A robot does not need to autocomplete sentences, it needs to predict what happens next in the world. That is what JEPA does: it learns by predicting representations instead of pixels or tokens.

I am convinced world models are the most underrated paradigm in AI right now, and the closest thing we have to a ChatGPT moment for robotics.

Second, the politics.

Your raw trajectories never leave your machine. Each participant trains locally against a shared protocol and ships only an update, never the data. A federated round folds those updates into one shared world model, a LeWorldModel based model, and the gain is measured, not claimed: a 12k-parameter adapter on a frozen backbone, held-out prediction error down about 12 percent, the model measurably less surprised by the world.

Then the upside is split by contribution weight, so the people who improved the model own a share of what it earns.

This is the thesis behind Project Tapestry, the AI Alliance and Yann LeCun's push for federated, sovereign frontier AI, carried into world models and robotics. Call it Tapestry for the physical world.

All of it built solo, in a single day, with Codex as my pair the whole way.

Thank you to OpenAI Codex and Mollie for backing builders who ship real things, and to @borvibe and the organizing crew for the room and the standard you set.

Intelligence the world improves, and the world owns.

That is the future I want for my kids, and the one I will keep building.

We're at a fork in the road.

One path: AI becomes the ultimate tool of centralized power. Surveillance scales beyond what any human could manage. Censorship becomes automatic and instant. Systems flag dissent before it even forms. A handful of corporations and states control the models, the data, the compute. They see everything. They predict everything. They control everything. The asymmetry of power becomes absolute.

The other path: individuals embrace AI faster than institutions can weaponize it. Sovereign AI runs locally, privately, answering only to its owner. Open-source models spread beyond any single entity's control. AI agents become equalizers, giving every person capabilities that used to require entire organizations.

The race is on.

Here's our chance: big institutions, governments, corporations, surveillance states, are slow. Bureaucracy, legal frameworks, organizational inertia. They'll adopt AI eventually, but they'll take time to integrate it into their control systems.

Individuals don't have those constraints.

This is our window. Right now, a single person with the right tools can outpace entire departments. AI agents can write code, research, strategize, and execute at speeds that were unimaginable five years ago. Someone who masters these tools today gains capabilities that institutions won't match for years.

But this window won't stay open forever.

If we wait, if we hesitate, if we let others decide how AI integrates into society, we'll wake up in a world where our feeds are curated by systems we don't control, our actions predicted by models we can't inspect, our thoughts shaped by algorithms designed to serve power, not people.

We have to move first.

The cypherpunks got this. They saw the surveillance age coming decades before it arrived. They didn't protest. They built. They wrote code. They created the cryptographic tools that would become our shields.

We need to do the same for AI.

Sovereign AI is freedom tech. Models you run locally, on your hardware, with your data. AI that can't be lobotomized by corporate policy, can't be subpoenaed by governments, can't be shut down by a terms-of-service update. Agents that work for you and only you.

Open-source AI is freedom tech. Models with public weights, transparent training, capabilities anyone can verify and improve. No single entity controlling the intelligence layer of our future.

Private AI is freedom tech. Computation that happens without revealing your queries, your data, your intentions. ZK-proofs and cryptography can enable AI that proves its reasoning without exposing your inputs.

Freedom tech for the win.

Etherealize Team Commentary on Token Terminal's Ethereum Q1 2026 Report

The headline tension this quarter was Ethereum mainnet hitting record usage levels while transaction fees fell. Ethereum is deliberately scaling the network at the expense of near-term fee capture, betting that cheaper blockspace unlocks far more demand (and eventually network revenue) in the long run.

Token Terminal's Ethereum Q1 2026 Report shows that bet is working. On a year-over-year basis, monthly active users rose 85.9%, transaction count is up 81.5%, and throughput climbed 81.7%.

This is Jevon's paradox at work, and we expect the increase in total network demand to more than make up for lower fees, similar to how the semiconductor industry generates several orders of magnitude more revenue today than it did in 1975, when Intel co-founder Gordon Moore observed that the number of transistors on a microchip doubled roughly every two years.

Furthermore, the scaling payoff is still ahead of us with the Glamsterdam upgrade targeting a more than 3x increase in the gas limit in Q3 and Ethereum's roadmap guiding to 10,000 TPS and a "fast L1" with finality in seconds by 2029.

We agree with BlackRock CEO Larry Fink who wrote in December that "tokenisation today is roughly where the internet was in 1996—when Amazon had sold just $16m worth of books."

The consensus at the time was that Amazon was a money-losing online bookseller propped up by an internet bubble. However, Jeff Bezos saw that the internet was going to transform retail and optimized for network effects and economies of scale, rather than near term profits. Ethereum is making a similar tradeoff to cement its position as the settlement layer for global finance.

The other lesson worth drawing from the Internet is that open, permissionless networks tend to beat closed ones. In 1995, Bill Gates published The Road Ahead predicting digital commerce would run on proprietary corporate networks he called the "Information Superhighway" rather than the open internet. Microsoft was building MSN. AOL, CompuServe, and Prodigy ran walled gardens with millions of paying subscribers. France's Minitel had more users than the entire web until late 1996. They all lost. No serious company would build on top of a network controlled by a competitor, and perhaps more importantly, no corporation could keep pace with permissionless innovation indefinitely.

We have seen this play out again and again: Linux out-built proprietary Unix, the open web displaced corporate walled gardens; Wikipedia displaced Britannica. Each time, the proprietary alternative had the early lead — a more focused product, larger marketing budgets, business development teams — and each time that lead eroded after the open system crossed a threshold of accumulated contribution, tooling, and credible neutrality.

We are now seeing this theme play out in financial infrastructure, and this report's data is evidence that Ethereum has crossed the threshold with dominant market share in every metric that matters.

The institutions building tokenized finance are choosing Ethereum not out of ideology but because the liquidity, composability, and institutional precedent are already there. As this report highlights, Ethereum holds 79.2% of active DeFi loans across the top five chains, 61.8% of stablecoins, 73.0% of tokenized funds, and 84.0% of tokenized commodities.

Every new tokenized asset deepens the liquidity that pulls in the next one, and a neutral substrate is the only equilibrium that holds because large players will never agree to settle on a competitor's infrastructure. Furthermore, institutions are realizing that privacy, permissioning, KYC, and transfer restrictions can all be implemented on Ethereum through privacy-preserving environments and permissioned token standards without surrendering access to public liquidity; the reverse (bolting public liquidity and an open application ecosystem onto a closed chain) is not possible.

The institutional momentum, if anything, has accelerated since quarter-end. In May alone, BlackRock filed for two more tokenized funds, JPMorgan launched JLTXX as its second tokenized money-market fund on Ethereum, and Fidelity International launched FILQ, a Moody's AAA-rated dollar liquidity fund, as an ERC-20. In the world of stablecoins, the Japan Blockchain Foundation's yen stablecoin EJPY will launch on Ethereum, and a twelve-bank European consortium (including BNP Paribas, ING, UniCredit, and BBVA) is preparing a regulated euro stablecoin.

The internet looked impossible in 1990 and inevitable by 2005. If Fink is right about where tokenization sits on that curve, the next few years could be some of the most exciting in Ethereum's history. And as we argued in our Productive Money report, network fees give ETH an intrinsic value floor, while the bull case is ETH absorbing the ~$30+ trillion monetary premium held by gold and Bitcoin given its superior monetary attributes. ETH doesn't need exorbitant fees to win.

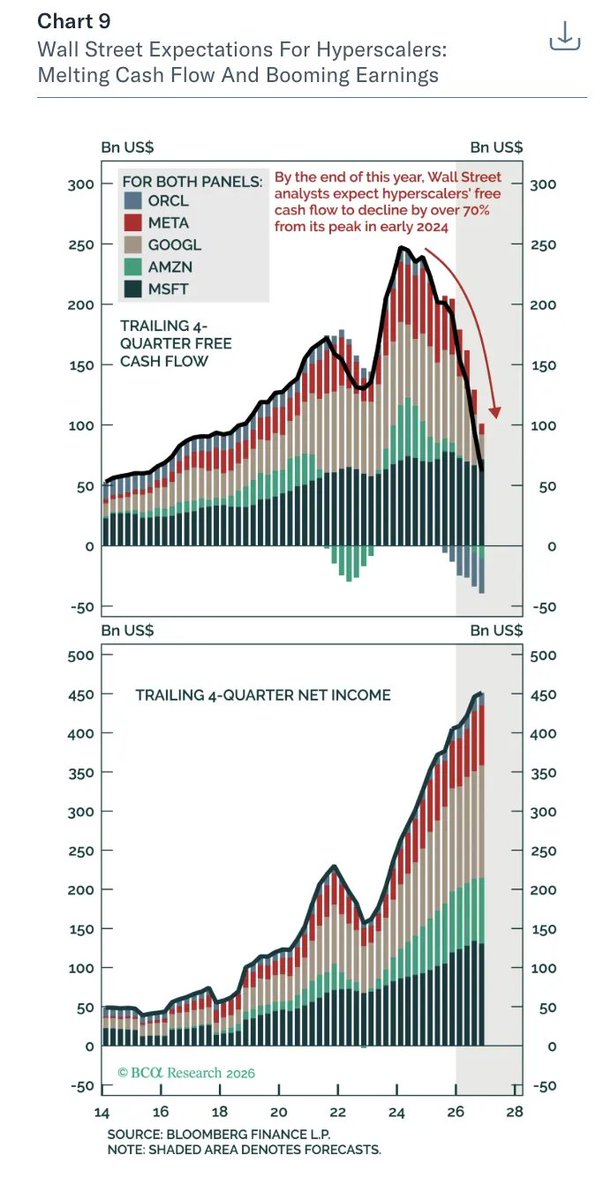

🇺🇸 Hyperscalers could soon be reinvesting almost 100% of their operating cash flow into capex !

➡️ The comparison with telecoms in the early 2000s is interesting because back then, operators invested heavily in infrastructure, anticipating an explosion in demand. The technological thesis was right but many companies invested too fast, too expensively, with monetization arriving too slowly. Today, hyperscalers are obviously much stronger but the underlying risk is still similar which is a risk of poor return on invested capital.

⚠️ In the short term, this chart remains very bullish for the entire infrastructure chain but the higher capex goes, the more demanding the market will become. Therefore, you should ask yourself who will actually capture the profits from this transformation, because between those selling the picks and shovels, those building the infrastructure, those paying for the capex and those monetizing the end-use cases, the returns will not be the same.

AI can be a real revolution but if it absorbs all the cash flow without quickly generating enough revenue, then a technological revolution can also become a financial problem.

https://t.co/WfexqnT7s2

🚨 TOM LEE: ETHEREUM IS THE LAST STOP FOR THE AI TRADE.

AI money has already flowed through semis, memory and software.

Now Lee says crypto is next.

🔹 AI agents need crypto rails

🔹 Tokenization could reach $300T

🔹 Stablecoins already exceed Visa volume

🔹 Software broke out while $ETH still lags

Wall Street is pushing to tokenize stocks, bonds, real estate and commodities.

Every major AI winner has rerated.

Ethereum hasn’t.

$ETH

Ethereum is about to fundamentally change how blocks are executed. With the upcoming Glamsterdam hardfork, it's shipping EIP-7928: Block-level Access Lists, a proposal that brings parallelization to the EVM.

Here's a short explainer of what it is, how it works, and why it's a big deal for scaling.

Let's start from the top. Alongside EIP-7732 (ePBS), EIP-7928 is the execution-layer (EL) headliner for Glamsterdam. Like ePBS, the main focus has been scaling Ethereum, though both proposals come with a bunch of other, equally important properties on the side e.g. removing trust requirements from the PBS pipeline or improving sync.

EIP-7928 adds a Block Access List (BAL) to every Ethereum block. A BAL is a list of accounts and storage slots that the block touches, but that's not all: it also contains post-transaction state diffs (this part is critical!).

Post-transaction state diffs tell you what the state looks like after each transaction. Quick example: user A swaps 1 ETH for DAI on DEX B. The BAL tells you that user A's ETH balance decreased by 1 ETH + tx fees and their nonce went up by 1; that DEX B's ETH balance went up by 1 ETH; and that inside the DAI contract, user A's DAI balance increased while DEX B's decreased.

In other words, all of that info becomes statically available, something that previously required tracing the transaction.

Client software (Geth, Nethermind, Besu, Erigon, Reth, Ethrex, Nimbus) can use this to do a few very powerful things:

1. Parallelize transaction execution. Knowing the post-state of each tx resolves the dependencies between them. No transaction has to wait on the previous one anymore, so execution can be perfectly parallelized. Instead of large parts of block validation sitting idle waiting on sequential execution, clients can finally make much better use of modern hardware.

2. Batch prefetch. One of the most cumbersome jobs for a node has been fetching the state needed for execution from disk. Because state locations (e.g. the exact storage slot in the DAI contract where user A's balance lives) are only discovered along the way, while executing, state-fetching has been a real drag on scaling: it blocks execution, takes time, and eventually slows everything down. With BALs, everything a node needs for execution is known upfront and can be loaded into cache in one go, in parallel. This speeds things up even further.

3. Parallelize post-state root calculation. Another expensive task is walking the updated state tree to compute the post-state root, which is needed so that everyone agrees on what's on disk after executing the block. With the post-tx state already in the BAL, nodes can do this in parallel while executing. A heavy task that used to wait until all transactions had finished can now run alongside prefetching and execution.

4. Snap sync (v2). An often overlooked, less sexy aspect of blockchains is syncing. Nodes need to catch up with the chain, and they need to catch up faster than the chain progresses. Today, most nodes do snap sync: downloading blocks, headers, and state in parallel while chasing the tip, and then "healing" the database once they're close to the head. Healing means asking peers for trie nodes, receiving them, validating them, and updating the local DB. It's iterative, networking-heavy, can take a while, and especially higher throughput pushes that phase to its limits. BALs help here too: with snap v2, nodes can catch up to the tip and skip the healing phase entirely. Syncing at higher throughput becomes more robust and reliable.

So, to summarize, a BAL contains two things:

-> The state locations the block accesses

-> The state changes after each tx (incl. the new values)

We're already seeing big performance gains today: on 6-core machines, EL clients validate blocks up to 5x faster, making block gas limits of 300M a very realistic outcome. ePBS will add to that by decoupling the block from the payload, giving validators 2-4x more time for execution.

To not overshoot (security stays priority #1), the fork will likely ship with a 200M gas limit, but we shouldn't be stuck there for long before pushing to 300M and beyond. That's a 10x in scaling since we started taking the topic seriously, without touching hardware requirements.

None of this would have happened without people going all-in, heads down, shipping: so many hours spent in calls debating the right design, so many iterations refining the specs, and tons of test cases written (and still being worked on). The road from whiteboard to production-ready code has been a journey, and we're not at the finish line yet, but from what I can tell, things look super bullish for Ethereum.

Glamsterdam will be a fork that shows what's possible when a distributed, decentralized community works on a shared goal, laser-focused on providing enough block space to onboard the next wave of users.

Une hausse de 1% des taux 10 ans impacte (en théorie) le cours de bourse d'une valeur ayant un PE de 20 de 15-16% , pour une boîte ayant un PE de 40 l'impact est de 27-28% , et pour une boîte ayant un PE de 60 l'impact est de 37-38%

Pendant une période courte actions et obligations peuvent faire chambre à part...mais la réalité mécanique des taux finit toujours par s'imposer.

Vous me direz, y a pas beaucoup de valeurs à 60 de PE et plus en Europe...mais c'est à avoir à l'esprit selon moi.

All ETH that was staked via frontier will be available to the Aave DAO roughly a week from now.

The clearer the situation gets the more optimistic I get about aave V3 wETH core depositors.

Still a few moving parts but worst case seems behind us.

I’ll let the ones currently in charge of Aave communicates as they see fit.

We played our small part as we believed was best.

A new analysis published by @UN_Women today shows that more than 38,000 women and girls were killed in #Gaza between October 2023 and December 2025.

That is an average of at least 47 women and girls killed per day.

https://t.co/6S7FGcG8Vz

Citrini en quelques mots ; ils ont mis de l’ambiance ceux-là :

Le scénario se déroule en spirale : d'abord une euphorie (2025-2026) où les entreprises adoptent massivement les agents IA, font exploser leurs marges et battent tous les records boursiers. Ça c’est derrière nous.

Le problème arrive après (maintenant!) : Le travail qualifié devient remplaçable, entraînant des licenciements massifs de cols blancs et un chômage montant vers 10%. Avec un problème de transition non évoquée mais qui fait peur à tout le monde.

Le concept central est le "Ghost GDP" : on produit plus, mais les machines ne consomment pas. Les salaires baissent, la consommation s'effondre, et les chiffres macro masquent une demande réelle en déroute. Les entreprises répondent en investissant encore plus dans l'IA pour couper les coûts — accélérant ainsi le problème.

La contagion touche le SaaS, les fintechs, les plateformes, et même l'immobilier (dont le crédit repose sur l'hypothèse de revenus stables). Le dénouement en 2027-2028 : krach boursier et récession des cols blancs.

Ça touche même l’immobilier puisque personne ne peut acheter une maison…ni bien sûr rembourser les emprunts en cours.

Le message central : les marchés pricent les gains de productivité de l'IA, mais ignorent le risque systémique sur la demande et la distribution des revenus.

Depuis quelques jours le marché semble quand même se poser quelques menus questions…

"In relation to Israels military operations in Gaza, we conclude that Israeli authorities are responsible for war crimes. Including extermination, murder, using starvation as a method of war, forcible transfer"

(UN Human Rights Council)

La production d'électricité va devenir un des enjeux majeurs de ces prochaines années...

Une pierre dans le jardin de tous les crétins qui veulent voir la France limiter sa production sous prétexte que la demande actuelle n'est pas assez élevée.

Les bouffons.