Do households adjust their portfolios when central bank rates move?

What triggers adjustments?

We tackle these questions in this paper!

We study nearly identical safe liquid assets where moving funds is free and instantaneous

Yet most households barely respond to spreads!🧵

New CEPR Discussion Paper - DP20612

What Makes Depositors Tick? Bank Data Insights into Households’ Liquid Asset Allocation

@fercirelli @arnavardar

https://t.co/SF4uIBzce8

#CEPR_AP#EconTwitter

¡Felicitaciones a los 16 alumnos de la Maestría en Economía de @utditella que continuarán sus estudios en los más prestigiosos programas doctorales de EEUU y Europa! Celebramos con mucho orgullo este gran logro. 👏🎉

Mirá nuestro placement histórico: https://t.co/9UE4wlnzhx

@fcastellorojo@floripasa Felicidades Fede!

Di Tella economics es un lugar maravilloso y muy meritocratico. Muchas historias como la tuya: llegas siendo nadie y con solo sacar buenas notas te vas a vivir afuera con una beca. A disfrutar!!!

@dandolfa Interesting David!

We extended your research on CBDC and bank lending to also include Stablecoins here in case of interest!

https://t.co/PMsiY4ZDwM

@lucasllach Excepcional industria de pagos en Argentina Lucas, felicitaciones. Cada año mejor. El crecimiento fue también ayudado por la alta inflación y la falta de emitir billetes de mayor denominación del gobierno anterior.

Top CEPR Discussion Paper of 2025 - DP20612

What Makes Depositors Tick? Bank Data Insights into Households’ Liquid Asset Allocation

@fercirelli @arnavardar

https://t.co/YcGtnYjxeB

#CEPR_AP#EconTwitter#2025inReview

The Economics Department at Universidad Torcuato Di Tella is seeking applicants for multiple full-time faculty positions at any rank: Assistant, Associate or Full Professor in any field of Economics.

More details below.

https://t.co/2LFtAdJ1wl

Wondering how to read Argentina’s recent legislative results—and what they tell us about U.S. foreign economic policy in LA and beyond? Get answers tomorrow (10/28) from this stellar webinar. @VickyMurilloNYC@fercirelli@jafrieden + @Sgc28Sara

Register: https://t.co/Pi7aTXba5E

Aún más: es momento de independizar el banco central de una vez por todas.

Cual es el argumento por el cual el socio del ministro de economía dirige el central?

Argentina necesita imitar al resto del mundo y crear institución independiente con amplio apoyo del congreso

US support is certainly helpful to prevent speculative currency moves. However, durable progress will require Argentina to move to a more flexible exchange rate regime, accumulate reserves, and build support for its reforms at home.

@FairyCalvo Not sure if this fully answers your question, but if you ask who leaves the most money on the table? → it’s also the wealthy (right figure: forgone interest / consumption).

Even though they earn higher yields and adjust when spreads move, they still forgo the largest amounts

Do households adjust their portfolios when central bank rates move?

What triggers adjustments?

We tackle these questions in this paper!

We study nearly identical safe liquid assets where moving funds is free and instantaneous

Yet most households barely respond to spreads!🧵

New CEPR Discussion Paper - DP20612

What Makes Depositors Tick? Bank Data Insights into Households’ Liquid Asset Allocation

@fercirelli @arnavardar

https://t.co/SF4uIBzce8

#CEPR_AP#EconTwitter

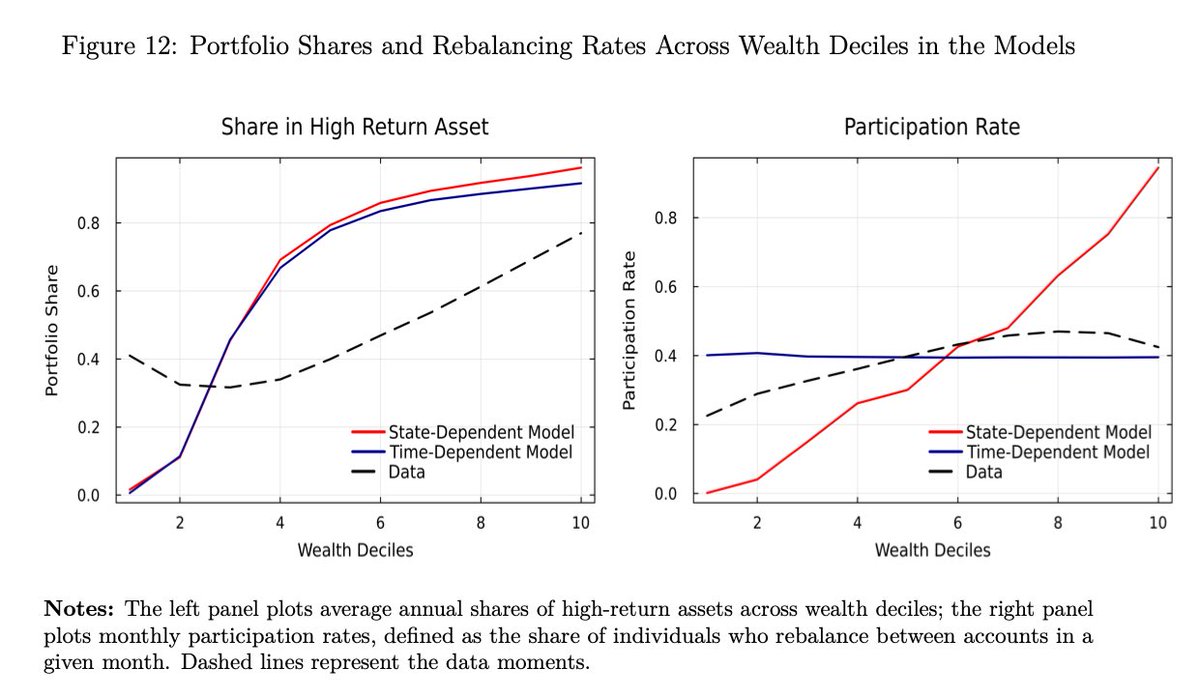

How do models perform against the data?

A two-asset incomplete-markets model with state- or time-dependent frictions:

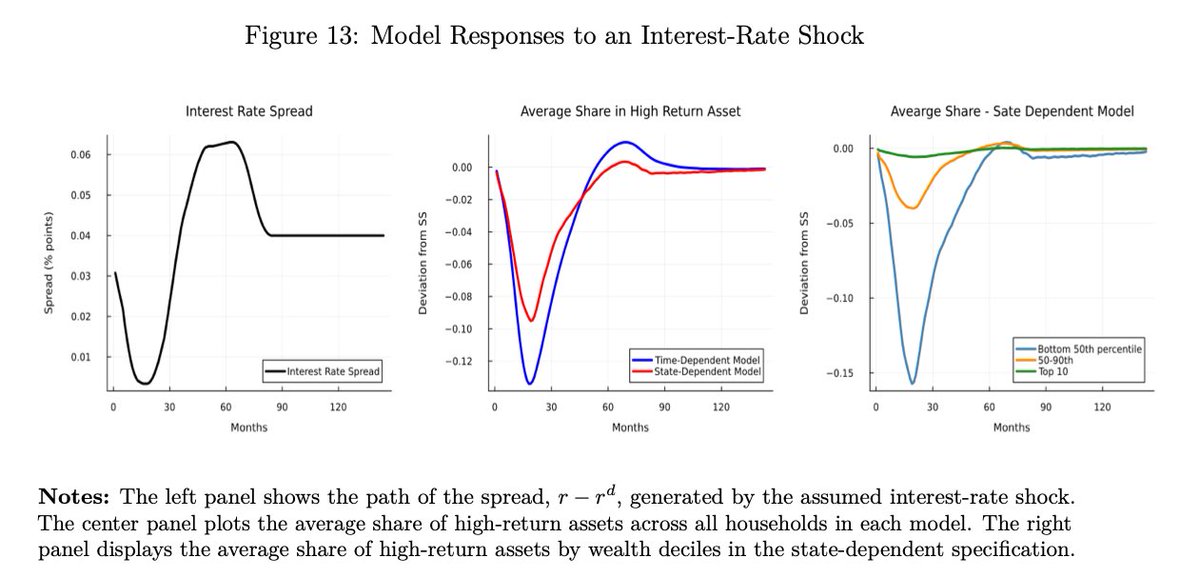

✔️ Captures cross-sectional portfolio shares across wealth levels ❌ Strongly overstates average portfolio responses to interest rates

Relevant for macro!

But if only a few adjust, who drives aggregate deposit shifts?

Wealthy households.

Deposits are highly concentrated, and the wealthy chase yields.

Decomposition: it’s yield-chasing reallocations by the wealthy that move deposits—not anything else.