Another Hindenburg Omen was triggered yesterday, bringing the total to 5 in the past month.

Since 1970, a cluster of 5 H.O's has happened 19 other times.

It also brings the total number of H.O signals to 232.

🇺🇸 S&P 500

The S&P 500 has never peaked in June. Every other month has done so at least once since 1950. If history holds, the market's high may still be ahead, giving bulls reason to smile

👉 https://t.co/yIk7SZYp6p

h/t @RyanDetrick $spx #spx

What just happened?

The S&P 500 just erased nearly -$2 TRILLION of market cap just hours after 3rd strongest US jobs report in 18 months.

Meanwhile, Bitcoin is officially down over -50% from its record high in October 2025.

What's happening? Let us explain.

(a thread)

NDR's pattern matching tool shows that the NASDAQ has closely tracked the dotcom analog and is closer to 1998 than 2000. It still suggests near-term volatility ahead.

JENSEN HUANG WAS ASKED WHO IS USING AI BETTER THAN ANYONE ELSE IN THE WORLD

His answer wasn't OpenAI. It wasn't Google. It wasn't even Nvidia itself.

Here's what he said on CNBC:

"Nobody uses AI better than Meta."

He explained that Meta went from a classical recommender system running on CPUs to a generative AI agentic system making recommendations across the entire platform.

"Everything from the way social media works and the way they recommend ads and help advertisers create content has fundamentally been changed. And their earnings show it."

"That's the reason why they're investing so hard. They see a much larger future potential for it."

Mark Zuckerberg $META is spending $70B+ on AI this year.

Deutsche Bank on the huge stock market run-up:

"Since WWII, the only other time the S&P 500 has risen this rapidly (except after a recession) was months before a huge market crash."

BREAKING: South Korea’s KOSPI hit new all-time high and crossed 8,750 for the first time in HISTORY.

The index is now up +106% in 2026, adding ₩3,150,000,000,000,000 ($2.3 TRILLION) in market value.

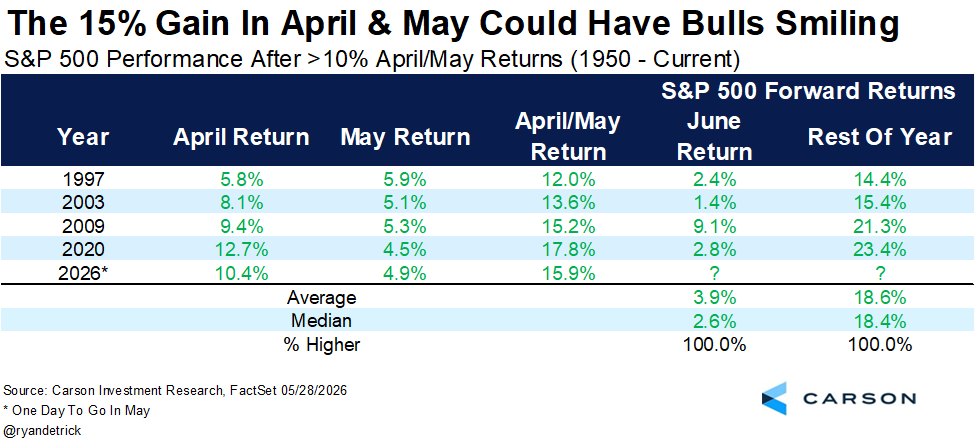

Want to make a bear mad?

Tell them that after April & May gain more than 10% (like 2026 will), the rest of the year has gained double digits each time and been up an average of nearly 19% the rest of the year.

The index rebalancings at the bell yesterday were criminal. The exchanges and the largest companies and fund managers have to get together and figure out how to do these things correctly. A 3:50 pm. re-balance with no buybacks allowed can crunch billions for NO REASON.

⚠️Just 2 companies have overtaken the South Korean stock market:

Samsung Electronics and SK Hynix together now account for ~60% of the MSCI Korea index.

Samsung alone makes up ~35% and SK Hynix ~25%.

US-domiciled diversified funds are subject to diversification requirements under the Investment Company Act of 1940, which limit concentration risk for regulated investment vehicles over time.

As index weights rise, funds may need to periodically rebalance portfolios to manage concentration exposure, creating structural pressure in highly concentrated markets.

Since October 2025, estimated selling pressure from these diversification requirements has reached a record ~$69 billion, according to Goldman Sachs estimates.

In other words, the stronger Samsung and SK Hynix perform, the more rebalancing pressure builds among the funds that hold them.

This is incredible.

Just the other day I was told that it isn't a bullish signal when equal-weight indexes make new highs.

The good news is this is what makes a market. I think it is a good sign.

Loved this chart from @JC_ParetsX that shows new highs for S&P 500, Nasdaq-100, and Dow equal-weight

Day 100 of 2026 and the S&P 500 is up a very impressive 9.9% YTD.

22 other times it was up >9% YTD on this day and the rest of the year was higher 86.4% of the time (19 out of 22) and up another 8.1% on average.

This does little to change our overall bullish thesis.

⚠️THIS IS ABSOLUTELY INSANE:

Long global semiconductor stocks is now the MOST CROWDED trade among global fund managers, cited by ~73% of respondents in the BofA Global Fund Manager Survey.

This is also the 3rd-highest reading on record since data began in 2014.

Furthermore, fund managers are the most overweight in technology since February 2024, and near the highest overweight since 2020.

By comparison, the previous most crowded trades at similar conviction levels were Long Magnificent 7 in June 2024 at ~70% and Long US tech in October 2020 at ~80%.

When a trade gets this crowded, and an unwind occurs, the selloff can be swift and painful.

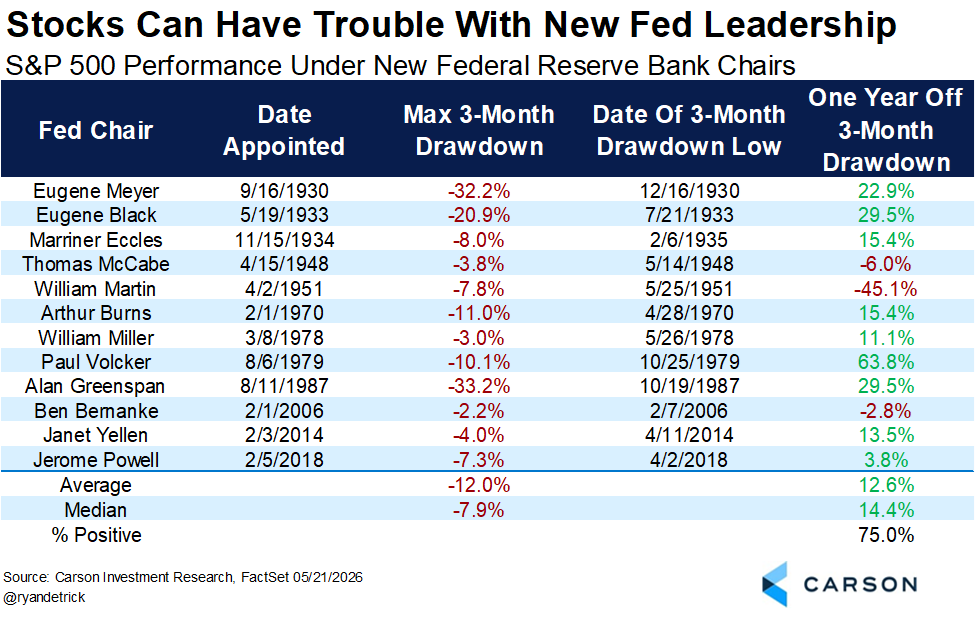

Kevin Warsh was sworn in at the East Room of the White House on Friday.

The only other Fed Chair to ever be sworn in at the White House? Alan Greenspan in the East Room under Ronald Reagan on August 11, 1987.

The Crash of '87 was just a couple months later. 😱😨😱😨

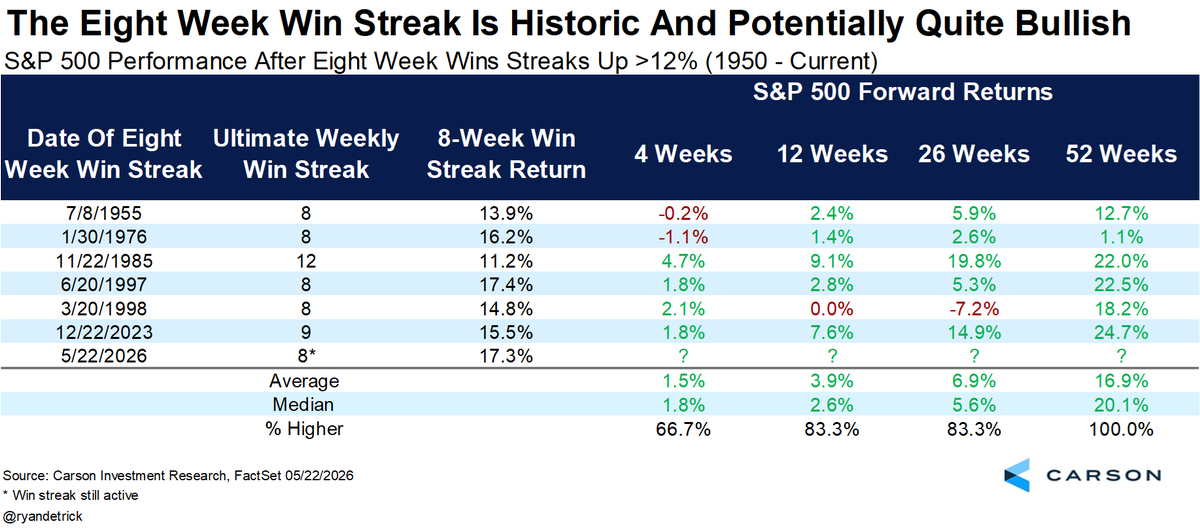

We just barely missed the best 8-week rally in history.

This one is up 17.3% and there was a 17.4% one in 1997. Stocks gained another 22% a year later back then by the way.

In fact, never lower a year later after an 8-week win streak that gained at least 12%.

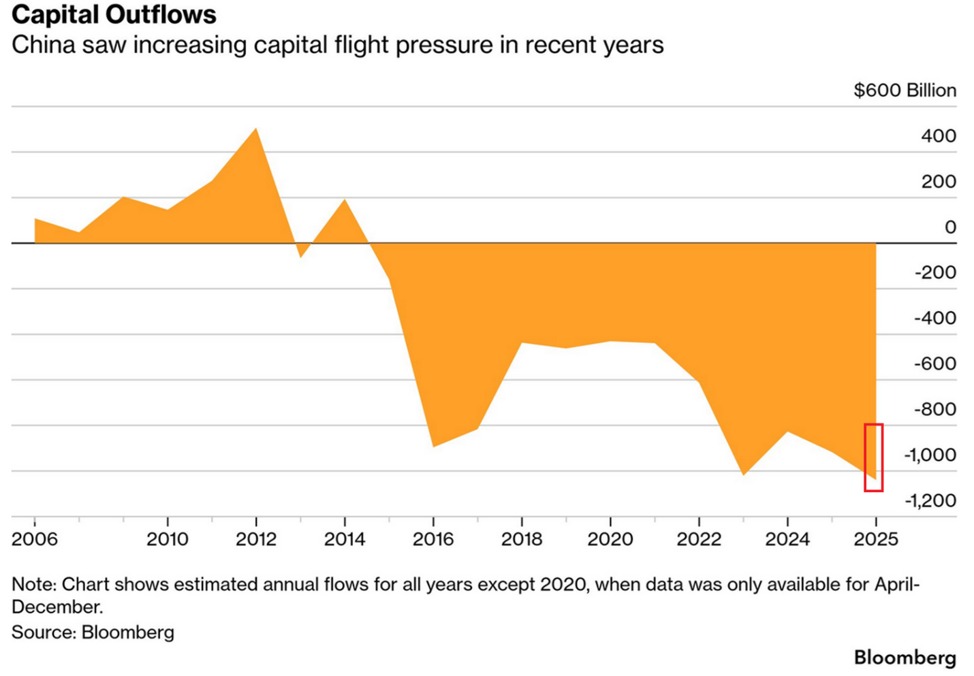

China is seeing massive capital outflows:

An estimated $1 trillion in capital flowed out of China in 2025, the largest annual outflow since records began in 2006.

Capital outflows have more than DOUBLED since 2021.

This comes as Chinese investors have moved funds into overseas equities through offshore brokers, particularly into the US and Hong Kong markets.

In response, China imposed restrictions on cross-border stock trading on May 22nd, ordering all illegal accounts to be liquidated within 2 years.

Furthermore, the country fined three offshore online brokers, Hong Kong-based Futu, Singapore-based Tiger Brokers and Longbridge Securities, a combined $330 million for offering Chinese investors access to foreign stock markets without regulatory approval.

China is tightening capital controls as outflows intensify.

AI is increasingly driving market profitability:

The S&P 500's net profit margin excluding financials is up to a record ~15%.

At the same time, the S&P 500's net margin excluding the Magnificent 7 and tech is down to ~8%, near the lowest since the 2020 pandemic.

This marks a ~7 percentage point gap between tech and non-tech sectors, the widest on record.

This comes as margins for companies outside of tech have been trending down since 2022.

Meanwhile, Magnificent 7 and tech firms have seen a rapid increase in margins over the last several quarters.

AI is all that matters right now.

Short interest on US stocks is at multi-year highs:

Short interest in the median S&P 500 stock is up to 3.0% of market cap, the highest since 2012.

This is DOUBLE the levels seen during the 2020 pandemic.

By comparison, at the peak of the 2008 Financial Crisis, short interest in the median S&P 500 stock stood at 3.8%.

Furthermore, short interest among the most heavily shorted 10% of S&P 500 stocks is up to 8.0% of market cap, the highest since 2018.

Both metrics are now even higher than during the bear market following the 2000 Dot-Com Bubble burst.

Are markets setting up for a short-squeeze?