SaaS is screwed.

We made a better @DocSend in one night.

@cjayls got back from hols, so I thought why not give him a stupid task to keep him up until 3am. We had a few people asking for pitch decks recently and wanted to include an interactive revenue forecast model with some elements gated to more serious viewers, and @DocSend couldn't do this.

We were pretty convinced in the simplicity of coding the backend, and given @cjayls is also incapable of human sleeping hours, we were pretty confident we'd get something decent out same night.

The result was pretty sick and took way less time than expected.

I think I’d expand and suggest doing anything “crypto” is a bad move. In the same way that doing anything because of SQL is a bad way to start.

The start needs to be identifying a problem that can’t be solved with SQL and then applying decentralised blockchains and smart contracts to solve it

@safetyth1rd Soc2 isn’t even that expensive … it’s the time that people are unwilling to give it because often it means they have to do stuff they’re not actually willing to do

💯 this a million times - unless you know everyone in your target job has done this programme it’s a waste of time. The difference between my wife graduating at Imperial and me graduating at Surrey was insane.

If you can’t optimise for nerd, you need to optimise for girls, booze and sports. That can be done very cheap in mainland europe.

THE SWARM IS HERE.

Applications for Swarm Village are now OPEN!

Built for builders preparing for:

→ Forward Deployed Engineering (FDE)

→ GTM Engineering

→ AI Systems roles

→ The next wave of startups

The next generation of builders won’t just use AI.

They’ll orchestrate agents.

Deploy systems.

Coordinate intelligence.

Ship faster.

At Swarm Village you’ll learn:

⚡ Multi-agent orchestration

⚡ AI systems & execution

⚡ Human × AI coordination

⚡ Deployment & real-world workflows

Apply now ↓

This will be a very very interesting product if you can do it UNFUNDED

otherwise capital inefficient and the Greeks hedging will spank you. It will be particularly annoying around expiries so you’d need to layer a load of options.

One advantage of Ethereum means you can layer a large amount of complexity without huge ops costs

Just chillin' in Amsterdam and reading our brand new Field Report on Institutional Crypto Lending.

And I can already hear some of you saying, "What the heck is a Field Report?"

Well, this is how Google's Gemini defines it:

"A field report is a document that details on-site observations, data collection, or activities outside of a traditional lab. It bridges the gap between theory and practical application by summarizing real-world events, conditions, or behaviors so decision-makers can draw conclusions."

So instead of solely looking at raw data, having our analysts interpret it, and letting them present their conclusions, we wanted to try something new.

That's why we spoke with 10 practitioners across the crypto lending landscape and asked them for their views on the current state of institutional crypto lending.

The result is a 15+ page deep dive that distills their key insights and explains:

- Why institutions still account for only ~6-10% of onchain lending activity

- How firms like BitGo, Sygnum, and Anchorage are now unlocking institutional access to onchain markets

- Where today’s infrastructure still falls short for institutional participants

- Why fixed-rate infrastructure and RWA collateral may define the next phase of growth

We hope that institutional players entering the space will find it useful and that it delivers on its goal of informing those firms' approach to this growing vertical.

P.S. For those joining us at our Amsterdam Summit at ABN AMRO’s HQ in the evening, we’ll have a limited number of printed copies of the report available.

See you later! 🫡

I’ve never hired “coders” I’ve hired primarily on problem solving ability. I’ve always thought that code is a byproduct of a tenacity to solve problems quickly and do a good job at it. I will generally go in pretty hard on someone’s CV claims and see how well they underhand the fundamentals. It’s pretty easy to tell when someone is using AI helpers.

We had one guy that had a strong CV but we told him we would introduce him to the team in the next round as “Claude” after nerves got the better of him and he fumbled around with AI helpers at the start.

@RektReznor@LoganJastremski@SCBuergel@FTX_Official That’s not an application - that’s like saying SQL is decentralised. Also bitcoin is only even decentralised because the person who created it is likely dead. Otherwise it would be the same as Linux and all other OS software.

@RektReznor@LoganJastremski@SCBuergel@FTX_Official What are you smoking… the traditional financial system has outstanding notional approaching a quadrillion meanwhile defi has barely 100bn

So how did that turn out? It turned out great.

If you want to spank cash on some outrageous extravagance England or France is the place to do it.

The A zone is expensive for middle earners purely because of FX rate but they fundamentally have very little there other than countryside and scenery.

If you are absolutely filthy rich, England is the place to be.

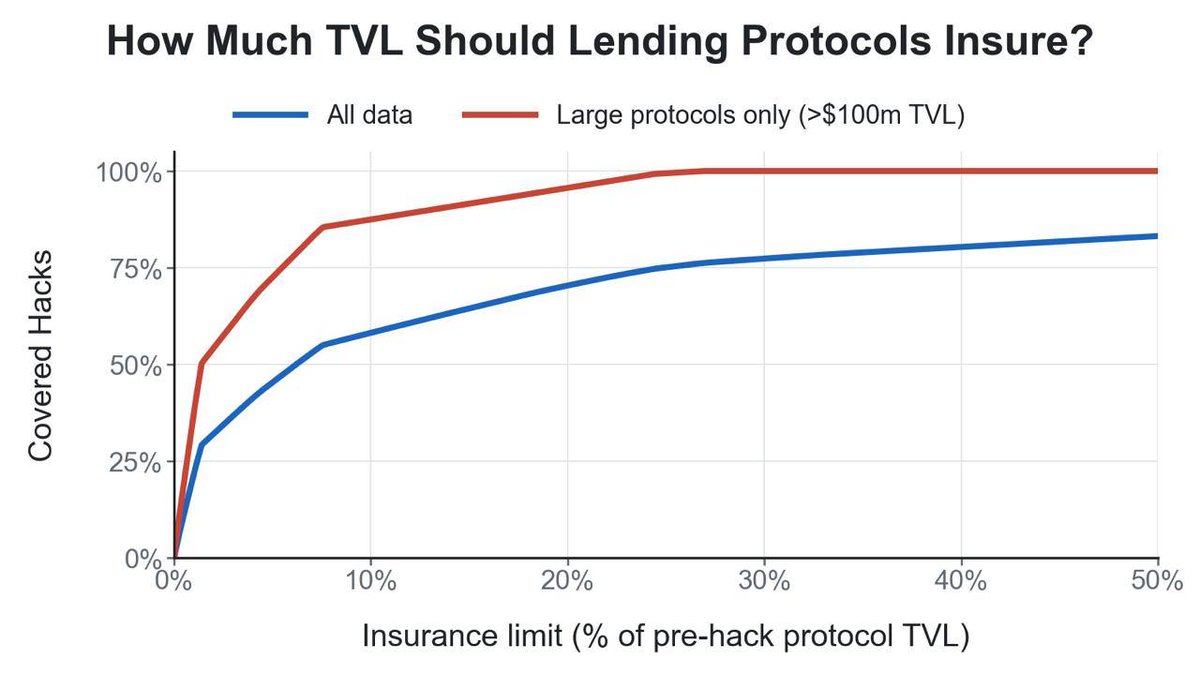

@SentoraHQ 100% sharing what we briefly talked about wrt coverage that has implications for @Flrelightfi in that just having $5m of coverage mitigates something around 50% of the actual losses in lending as an absolute number. This shows how skewed the data is.

https://t.co/kfdZNJeQWt

How do you get DeFi insurance for under 20bps?

It all relates to how much insurance protocols should actually pay for per TVL.

From shopping around, I can confidently say that the price in the market being offered is between 1.5-4% on lending and borrowing crime insurance.

"but.. but.. you said the expected value is 3bps"

yes but the insurers are:

1) skittish about cover, and

2) they have to take into account Expected Shortfall, and given no-one is buying cover they have pretty high concentrations on what they write.

How the hell do you get to <20bps when you're paying 2% ?

Start with defn of protocol crime insurance for hacks:

- exclude bridge-related events

- Solana and EVM

- Protocol exploits or oracle manipulation involving a theft, a few others things too but it's PROTOCOL stuff

Lets also give an explicit counter-example...

START EXAMPLE SIDE QUEST >>>

As a concrete example, most people in crypto talk about the "Aave hack". @aave didn't get hacked by any stretch of the imagination, you would definitely know if they did.

@aave had a credit event. A collateral lost its peg because of an error in technical configuration. That error was propagated from a criminal cyber attack / hack on a bridge, who had also made an error in a recommendation to their client on their DVN setup.

This is not a protocol hack of @aave and no crime insurance policy covering Aave would pay out for this.

This is a credit default risk and protected by a Credit Default Swap.

Where it gets confusing is that Aave's DAO appoints risk managers that are supposed to price the margins for collateral. However, you spin it though, the risk manager missed a credit event and the protocol remained resilient.

What should ideally have happened is @aave have umbrella, collateral have Crime & E&O coverage and Bridge has Crime & E&O coverage. Insurers then get triggered by both collateral and bridge and then sue each other to decide who pays what %.

There could be some argument that the risk manager might have some liability but it's going to be hard ground to justify because they have a framework, it's very public, they published their homework and we all deposited in a non-custodial fashion.

<< END EXAMPLE SIDE QUEST

Getting back to the quant stuff.

When you look at all the data of the 600 lending/borrowing protocols and 100+ hacks, especially on the larger protocols (of which there are nearly 20 hacks now) you notice something kind of interesting.

The data suggests that the majority of protocols get pinged for a low proportion of their overall TVL. In fact the largest protocol hack was @eulerfinance and even that zero-day took about 63%

There is a myth that is misunderstood, by even some brokers I discussed this with this morning, that hacks are total loss scenario. It might be for random off-the-book hedge funds but in the public and open-source Ethereum / Solana landscape we see all and it says the losses are varied but on average a small ratio.

In fact you would cover 73% of all losses if you had just 5% of the TVL insured.

Now hold up.

If quotes in the market are around 1.5-4% and we can insure a large chunk with just 5% of cover then the passthrough to lenders is 1.5-4% / 20 per unit of TVL

However, Increased Limits Factors kick in

(honestly I don't even know if that's the correct acronym expansion, I just know it as "ILF")

Insurers will generally insure blocks and create a "tower" which means that those at the bottom of the tower have higher risk. If the bottom of the tower is priced at 1% then the next guy might be happy to do next-loss cover at 90bps which implies an ILF of 90/100 = 90%

On average ILF can vary but I think it's conservative to estimate around 95-99%. One of my broker buddies has also said there is a commercially minimum rate around 60bps so no matter how high the tower, you'll pay at least 60bps to get someone out of bed on each tower chunk.

When you look at how this scales, on $1b of coverage you would buy actually just $50m of cover which would cover 73% of all losses.

You would pay between 120.4bps and 325bps on that $50m

You would pass through ONLY 5-19bps though to lenders.

From a protocol perspective this is a total no brainer and insane that people don't do it more.

The caveat? And why I care.

"Unpermissioned DeFi is broadly uninsurable", a well known DeFi broker.

Plug @KeyringNetwork...

Lucky for you fuckers we charge no money on this and Keyring can onboard users with ZKPs in 3-30 seconds without selfies or passports. And most importantly, there is no backend review process, so you remain fully decentralised without triggering "points of control" for regulators.

If you want to get insured, it's likely you'll want to look at putting a door lock on the think you insure to get a non ridiculous quote. Or get a quote at all.

@zkGaylord@binji_x When skiing I take cheddar, baked beans and an old El Paso fajita kit. Beans on toast is a fantastic recovery snack and old El Paso is a great group meal for the boys for just €5

My French mates go fucking skitz tho when I slap out the @CathedralCity cheddar slab

@novogratz The American banking system is both the shittest and the best in the developed world.

It’s the shittest place for basic retail functions whilst retaining the strongest and most sophisticated investment banking operation.