How $IREN can reach $1T:

AI hype leads to 50x multiple. $IREN would need EBITDA of $20B.

1.5GW Colo: $4B revenue.

1.5GW CSP at $20m/mw: $30B revenue

$34B x 50x = 1.7T

$IREN > $5k/share

Even giving up 30% CSP economics for NVDA Lepton, 1T is conservative.

STAY HARD!

$NUAI RSUs seem to be the hottest topic in the market these days… but not all RSU packages are created equal.🔥

This might be even more bullish than José speaking at Data Center World Power.

José Rodriguez did not join NUAI just for a salary and some easy time-based stock compensation.

His 450,000 performance shares are divided into three separate tranches, and each tranche requires NUAI to achieve a major operational milestone:

1. Reach commercial operations at a campus producing at least 200 MW.

2. Sign a binding lease or pre-lease with a Tier 1 hyperscaler for a second NUAI data center site with at least 500 MW of scalable critical IT capacity.

3. Secure binding financing sufficient to develop that second site, with at least 500 MW of contractually committed critical IT capacity across NUAI’s campuses.

Think about what that means.

José came directly from senior data center roles at Microsoft and ByteDance/TikTok, and he has personally agreed to compensation targets that go far beyond simply completing Phase 1.

His incentives are tied to commercial operations, another Tier 1 hyperscaler agreement, a second major data center site and the financing required to build it.

This does not look like a management team planning one small project. It looks like a team being assembled to build a much larger hyperscale platform.

NUAI is still valued at roughly $500 million, yet it has recruited an executive of José’s caliber, placed him on one of the industry’s biggest stages and tied his equity directly to gigawatt-scale execution.

The market is pricing NUAI like a small speculative developer. José’s compensation package suggests management is planning something much bigger.

RAISE Day 1 Summary $IREN:

‣ Horizon 1 handover confirmed 19th July

‣ Commisioning H2

‣ MSFT very happy with IREN so far, very hands off. Great partners.

‣ IREN on call with NVDA basically everyday

‣ Deals signed today are even better than 2 months ago.

‣ Pre payments sweetspot now between 25-40 roughly. Some even offering 100%

‣ IREN GB300 NVIDIA EXEMPLAR Cloud certified. Likely announced next week. Only THREE have this right now.

‣ IREN selected with small number for VERA rubin for testing VERY SOON. Unofficially late EOY mass production. Likely early 2027

‣ H5-H6, Sweetwater 1 Vera Rubin

‣ Mirantis deal closing this month is the aim

‣ Semi conductor shortage micron $MU seeing into 2031

h/t: @FinGigawatt

https://t.co/Rx84G8EYzc

This $NUAI press release tells me one thing:

This company is getting smarter every step of the way.

No ego. No founder pride. No pretending one person can do everything.

They are putting the right people in the right seats for the next phase.

Charlie Nelson as Chairman & CEO.

Ted Warner expanding into President, CFO and Board member.

José Rodriguez coming in as COO with real hyperscale experience from Microsoft, TikTok and AWS.

Will Gray moving into the Permian role where his local relationships and stakeholder work can create the most value.

That is exactly what serious companies do.

They don’t protect egos.

They protect execution.

They protect shareholders.

They build the team the opportunity requires.

$NUAI is not just talking like a scaled digital infrastructure platform anymore.

They are starting to act like one.

In anticipation of @bitcoinbutcher1's Space tonight covering $NUAI, I wanted to put out a quick brief for anyone new to the name. Hopefully this gets the brain juices flowing and brings some good questions!

$NUAI call tonight at 7p central. See you there!

A quick refresher on $NUAI (New Era Energy & Digital) for anyone hearing about it for the first time.

$NUAI is formerly New Era Helium, a Permian Basin oil/gas/helium company that has pivoted into AI data center infrastructure. The asset that matters is Texas Critical Data Centers (TCDC) a 438-acre AI and high-performance computing campus in Ector County, just outside Odessa, master-planned in phases with capacity scaling to 1+ gigawatt over time. The legacy gas business is background now, does not matter. TCDC is the whole story.

The GP/LP model is one of the most important parts. $NUAI doesn't fund these mega-campuses off its own balance sheet. It acts as the General Partner (sponsor/developer) while institutional investors come in as Limited Partners providing most of the capital financed primarily at the project level and designed to scale while limiting dilution. In practice, $NUAI contributes site control and local relationships, co-invests equity alongside the institutional partner, and keeps a long-term stake rather than just selling the land. They're targeting roughly 80/20 debt-to-equity per project and earning fee streams plus equity participation. Capital-light at the top, scalable underneath. We can't be sure of deal specifics yet, but indications from recent Northland Capital analyst reports point to $NUAI capturing 45%+ of deal economics.

So who exactly are these partners? In April they signed an LOI to form a JV with Stream Data Centers. Stream is a Tier-1 platform within the Apollo ecosystem. Stream runs development and operations while a third party institutional investor provides equity and arranges the debt, a serious counterparty for a company this size. Important to note. Stream was selected by the hyperscaler $NUAI is currently partnered with. PDI was originally partnered with $NUAI before the hyperscaler requested Stream to take over. Most, if not all, of the partners below were selected by the hyperscaler.

Ramboll: Engineering

Apollo: Not an explicitly noted partner but they own Stream so yeah they are doing something...

Stream: DC operations

RK Mission Critical: Modular offsite fabrication

Thunderhead Energy: BTM gas turbines

Macquarie: Additional Institutional Funding Partner

The balance sheet is firming up alongside it. $120M equity raised, a $290M Macquarie credit facility, and $80M+ cash at the end of April, with management saying Phase 1 can be funded without material near-term dilution. The CFO indicated this also helps build into Phase 2 of TCDC.

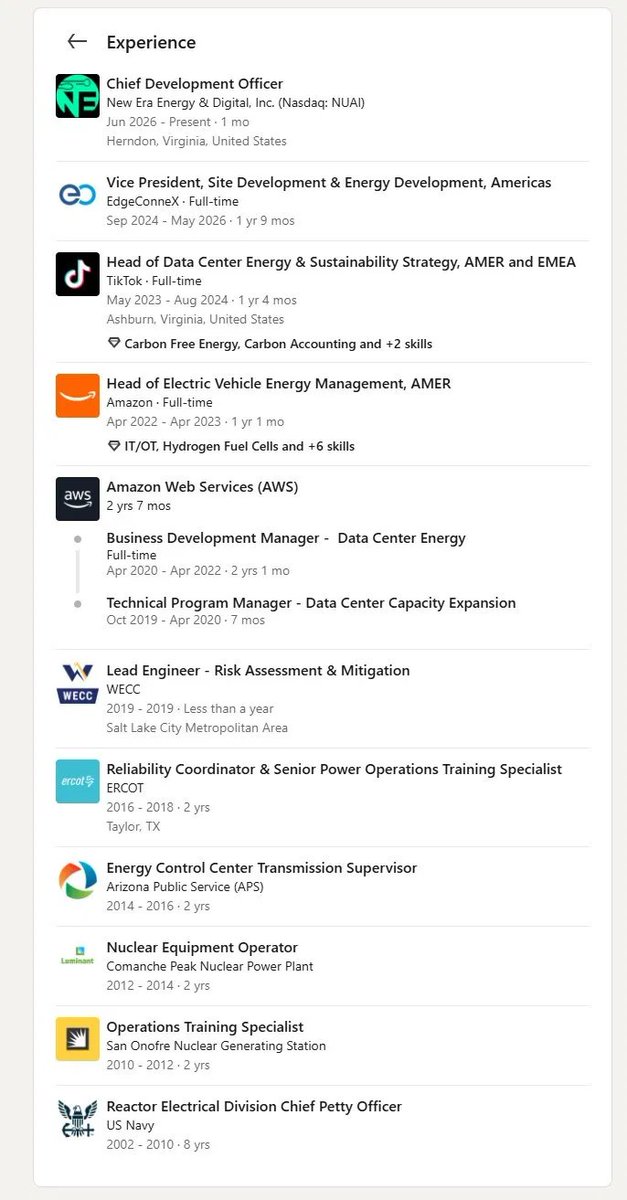

Staffing has been beefed up to match all of the above. Charlie Nelson (President & COO, Jan), Ted Warner (CFO, March, 20 yrs across energy, power, and digital infra capital markets, he helped set the playbook at $APLD). And Evan Pierce, Chief Development Officer, one of the most recent additions, joined with an extensive background spanning nuclear, AWS, ERCOT, and TikTok.

Now the other side, worth saying plainly, because this is still a execution dependent, pre-revenue story:

- New Mexico litigation. Mostly addressed, not fully closed. $NUAI reached a pending $1M settlement (court approval still needed) that would dismiss the five claims against the company with no admission of liability. But three claims against CEO Will Gray personally remain and are still being contested. The corporate overhang is largely lifted, the individual one isn't.

- Guidance has slipped. Management originally pointed to a signed hyperscaler lease by Q1 or early Q2 2026. We're now in late June and it's still unsigned it remains the "key near-term priority." They were too bullish on timing, and the deal that anchors the entire thesis hasn't been inked yet.

- CEO track record. Will Gray draws real skepticism from part of the shareholder base tied to past business turbulence in his prior landman career, the personal New Mexico claims, and lease deadlines that have already moved. Fair to ask how much of the bull case rests on management delivering on a timeline they've pushed before.

I am sure there will be additional concerns but these are the three I have seen the most of and seem to be the most issue for those looking into $NUAI.

Continuing On:

The actual thesis for all of the above. Behind-the-meter (BTM) power. Every AI data center needs power, and the grid interconnection queue can take years. $NUAI's site sits right next to existing generation from Vistra and Calpine in West Texas. Generation equipment is being procured through partners Thunderhead Energy and Turbine-X.

$NUAI management's line: "the easiest place to build power is where it already exists." The plan runs in phases:

Phase 1: 200 MW via adjacent generation

Phase 2: +450 MW behind-the-meter (gas-fired turbines and reciprocating engines fed by diverse gas across three pipelines)

Phase 3: scales up to 1.4 GW

One liner for all this. Powered land in the Permian + a capital-light GP/LP model + behind-the-meter gas to skip the grid queue = a path to deliver hyperscale AI power fast. Execution is still ahead of them, but that's the setup for $NUAI. There is an additional New Mexico site with 2GW of Natural gas power and 5GW of nuclear power that we know of also. I did not get into this here as TCDC is the current priority and will serve as the anchor and proof of concept but is important to keep in mind.

Bring your questions tonight. I'll be listening and looking forward to any unique insight. The panel has some great speakers lined up too! 😃In full transparency I'm heavily invested in $NUAI, so I'm clearly biased. Everything above is meant for informative purposes, not advice, dig in and form your own view!

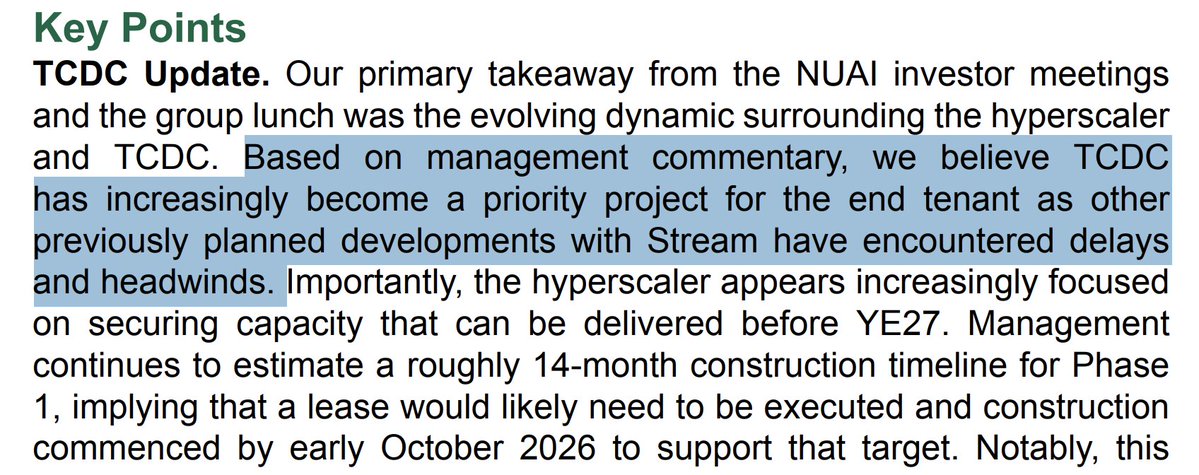

I'll be brief. Based on the highlighted sentence from the recent Northland company update, I believe the probability of $NUAI closing a hyperscaler deal by October 2026 is basically 100%. In fact, I believe October is the line in the sand, and the signing date will likely be late July or early August. Therefore, it would make sense for all data center investors (e.g., investors in $IREN, $WULF, $CIFR, $APLD, $HUT, etc.) to have some exposure to NUAI by August, even if only a lotto position.

New Era Energy & Digital ($NUAI): A bull case for an AI-infrastructure story the market is still underestimating

NUAI is a re-rating in progress. A former Permian Basin E&P that has pivoted into large-scale AI/HPC data-center development, the company is systematically retiring the legal and capital-structure overhangs that have kept institutional capital on the sidelines — while the equity still trades closer to the baggage than to the platform underneath it. The setup is the familiar small-cap asymmetry: a genuinely scarce underlying asset priced at a discount to its de-risked value because the market has not yet marked the clean-up to par.

The asset is Texas Critical Data Centers (TCDC), a ~492-acre campus in Ector County, Texas, with ~650 MW of capacity secured and a design that scales toward 1.4 GW. The thesis in one line: management is clearing overhangs faster than the stock has repriced, while assembling the financing, operating, and commercial partnerships needed to convert powered land into contracted, project-financed cash flow. The sections below lay out the de-risking, the platform being built against it, the capital-markets catalysts, the Street's early valuation work — and, in fairness, what has to go right for the gap to close.

The defense: clearing the overhangs

Sharon AI is gone — and paid in cash. The single largest structural overhang was NUAI's partnership obligation to Sharon AI in the TCDC joint venture. That chapter is now closed. NUAI consolidated full ownership of TCDC, and on April 24, 2026 it repaid the remaining $50 million senior secured convertible note to Sharon AI entirely in cash, plus accrued interest — eliminating the conversion-driven dilution that had been hanging over the share count. Total consideration on the buyout came in around $74 million, and crucially, Sharon AI retains no ownership, governance, or control rights in the campus. A messy, two-headed JV became a clean, wholly owned flagship.

The ATW structure has been de-risked. Earlier in the year the company scrapped a planned convertible preferred issuance — exactly the kind of variable-priced instrument that tends to grind small-cap charts lower — in favor of an amended waiver with ATW AI Infrastructure II that reset warrant exercise prices to a fixed $2.00. That converted a potentially toxic, open-ended dilution mechanism into a known, fixed-strike overhang that is now being worked down as warrants are exercised. It is not fully retired — there remain unexercised warrants on the books — but the shape of the dilution is dramatically friendlier than it was, and the worst-case path is off the table.

The New Mexico lawsuit is being settled. On May 28, 2026, the company announced a pending agreement that would dismiss every State of New Mexico claim against New Era — five claims in total — for a $1 million payment to the bankruptcy trustee, subject to court approval. The stock moved double digits in after-hours trading on the news, a sign of just how much the litigation cloud had been weighing on sentiment. This removes the corporate legal overhang that had made many institutions reluctant to underwrite the story.

The offense: building a platform that can execute

Removing overhangs only matters if there's something worth de-risking. Since March, the moves on the offensive side have arguably been more important than the defensive ones:

A real CFO for a capital-intensive business. In March, NUAI brought on Ted Warner as Chief Financial Officer. This is not a generalist hire — Warner ran Northland Capital Markets' Energy, Power and Digital Infrastructure practice, which since 2023 has structured more than $7 billion of financing for large-scale data-center development. For a company whose entire value-creation path runs through project finance and capital partnerships, hiring a banker who has actually closed this exact type of deal is a tell.

Macquarie validated the asset. Also closed in early April: a multi-tranche senior secured term loan credit facility of up to $290 million with Macquarie Group, earmarked for the TCDC flagship. A blue-chip infrastructure lender does not extend a facility of that size against a project it hasn't diligenced. Combined with a $115 million registered equity offering, management reported $80 million-plus in cash as of April 30 — runway to actually execute rather than survive.

The bench is now stacked with hyperscaler-native talent. What had been a thin team is being built out quickly. On June 1, NUAI named Evan Pierce as Chief Development Officer and Michael Johnson as General Counsel and Chief Compliance Officer — and the pedigrees matter as much as the titles. Pierce spent two decades on the customer-and-infrastructure side of this exact business: most recently leading data-center site and energy development for the Americas at EdgeConneX, and before that in energy, utility-engagement and capacity roles at Amazon/AWS and ByteDance, with a hand in planning more than 5 GW of data-center and power infrastructure. NUAI effectively just hired someone who has sat in the hyperscaler's seat and knows exactly how these tenants evaluate sites and procure power.

Johnson, the new GC, arrives from CoreWeave and, before that, Switch — two of the most relevant names in the industry — bringing three decades of data-center leasing, powered-land acquisition, construction and financing experience. Pairing a heavyweight GC with a dedicated compliance mandate also signals a deliberate institutionalization of governance, which is precisely what an investor base wary of the litigation overhang wants to see. You don't recruit people like this to sit idle; you recruit them to paper a lease and build.

A Tier-1 operator and institutional capital are circling — and a hyperscaler appears to be steering. On April 1, NUAI signed a non-binding LOI to form a development-and-financing joint venture for TCDC with Stream Data Centers, a top-tier U.S. data-center operator, alongside an institutional capital partner. New Era contributes site control and local execution, Stream serves as developer and operator, and the institutional partner provides equity and arranges the bulk of project-level debt. Two details elevate this above a routine LOI. First, Northland's research describes the pairing as effectively brokered by the prospective hyperscaler tenant itself — the customer pointing NUAI toward the partners it wanted building and financing the site, which is a meaningful tell on intent. Second, Stream was acquired by Apollo Global Management in late 2025 at a valuation of roughly $40 billion, and the institutional partner is believed (per Northland) to be Apollo — putting some of the most credible capital in infrastructure behind the structure. It is still an LOI, not a signed definitive, but the roster is what turns a development concept into a financeable platform.

The power story is validated. What differentiates TCDC is not the dirt — it's the power. NUAI's "behind-the-meter" (BTM) thesis received concrete substantiation through a 450 MW behind-the-meter generation plan at TCDC developed with named partners Thunderhead Energy and TURBINE-X Energy. In a market where the binding constraint on AI buildout is increasingly electrons, not acres, a credible path to nearly half a gigawatt of on-site generation is the asset.

The hyperscaler is in advanced negotiations — over secured capacity, not a concept. The event that would re-rate the whole equity is a hyperscale lease. Management has described advanced commercial discussions with a top-tier, credit-worthy hyperscaler — realistically one of the big four cloud builders (Alphabet, Amazon, Meta, Microsoft) — for a campus with roughly 650 MW already secured and a path beyond 1 GW. The acquisition of an additional 54-acre corridor adjacent to Vistra and Calpine power plants was itself a milestone within those lease discussions. Timing is framed conservatively around fall 2026, and conservatism here is a feature given how the market punishes overpromising. The backdrop is favorable: recent hyperscale leases in the sector have printed in roughly the $140–190 per kW per month range (at least one recent deal involving Google reportedly reached ~$188), while the big four are guiding to historic 2026 capex — Alphabet to about $175–185 billion and Amazon to around $200 billion — as demand outruns deliverable power. In that environment, a power-secured, near-shovel-ready site is exactly what is scarce.

The invisible bid: a capital-markets function, finally resourced

Not every driver of a stock is a press release. For most of its life, NUAI was too small and too underfunded to run the kind of investor-relations program that institutional money expects — sustained institutional outreach, non-deal roadshows, analyst targeting, the steady cadence of being in front of the right funds. Those functions weren't broken; they were simply never staffed. That is changing, and the upgrade is visible in the hires themselves.

The company's investor relations now runs through OG Advisory Group, where the engagement is led by Lincoln Tan — who previously ran investor relations and marketing at IREN through precisely the kind of transition NUAI is now attempting (a power-and-mining story re-rating into an AI data-center story), and who came to IR from Macquarie Capital. Pair that with CFO Ted Warner, whose career was built structuring data-center financings on Wall Street, and the company has, arguably for the first time, a team explicitly equipped to court institutional capital rather than simply collect retail attention.

The practical implication is the kind of "invisible" activity that rarely makes headlines but steadily changes a stock's character: institutional meetings, conference presence (B. Riley in May, Datacloud in June), and the normal rhythm of roadshows and analyst engagement that turns a thinly followed micro-cap into a name long-only funds can actually own. As the shareholder base broadens and deepens, two things tend to follow — a higher-quality register and lower volatility — as price discovery shifts away from fast retail money toward investors underwriting a multi-year build.

This compounds with the de-risking. Every overhang removed — the lawsuit, the dilutive structures — is one less reason for a fundamental investor to pass and one less piece of "hair" on the story. The explicit catalysts get the headlines; this quieter professionalization of the capital-markets function is part of what lets them stick.

What the Street is starting to see

Sell-side coverage is one of the clearest signs the professionalization is working. In April, Northland Capital Markets initiated coverage with an Outperform rating and an $11 price target — against a share price barely above $5 at the time, implying roughly 2x upside. The logic is a staged, project-finance valuation: Northland credits only ~283 MW of TCDC capacity (Phase 1 plus half of Phase 2), assumes NUAI retains ~45% of the JV, applies a ~19x EV/EBITDA multiple in line with listed data-center peers, and discounts back on a ~125 million fully-diluted share count. Notably, that target deliberately excludes the back half of secured capacity, all of Phase 3, and NUAI's entire ~7 GW wholly-owned New Mexico pipeline (a ~3,500-acre Lea County site with a small-modular-reactor angle via a Last Energy partnership) — meaning the bull case carries option value the published target doesn't pay for.

NUAI now has its first real institutional research footprint, and a company running a proper IR program with a clean-up story to tell typically attracts more coverage over time. Additional analysts picking up the name through year-end — plausibly several — would broaden the buy-side audience and is exactly the kind of slow, compounding tailwind the "invisible bid" is built on.

The catalysts ahead

The next few weeks and months offer a dense sequence of potential catalysts:

Datacloud Global Congress, June 2–4, Cannes. President & COO Charlie Nelson is scheduled to speak at the industry's marquee gathering — the kind of room where hyperscalers, Tier-1 operators, and institutional capital allocators are all present (in fact, the hyperscalers, Stream, and Apollo are all present). For a company in active lease and JV negotiations, the value of being on that stage, at that moment, is hard to overstate.

A Stream JV definitive agreement converting the LOI into something binding.

A hyperscaler lease, the single highest-impact event in the story.

Expanding analyst coverage. With one Outperform initiation on the board, additional firms picking up the name — potentially several by year-end — would deepen the institutional audience.

A still-growing team. The June 1 additions of a chief development officer and general counsel are likely an opening move, not the finish; further senior hires would keep signaling that management is staffing for execution and often front-run bigger announcements.

The picture

Step back and the pattern is consistent: every quarter, if not every month, a structural negative has come off the board and a structural positive has gone on. Sharon AI — cleared. The toxic-preferred path — scrapped. The state lawsuit — settling. In their place: a Macquarie facility, a Tier-1 operating partner, a validated power plan, a CFO and now a development chief and general counsel drawn straight from the hyperscaler and data-center world, and an $80 million-plus cash cushion. The market tends to discount a stock for its overhangs right up until the moment they're gone — and then re-rate it for the platform underneath. With the first sell-side target sitting at roughly double the recent price and explicitly excluding most of the pipeline, the gap between where NUAI trades and what a leased, financed platform could be worth is the heart of the opportunity. NUAI is converting overhangs into catalysts on a remarkably steady cadence.

$NUAI announced the appointments of Evan Pierce as Chief Development Officer and Michael Johnson as General Counsel and Chief Compliance Officer.

Together, they bring leadership experience from EdgeConneX, AWS, CoreWeave and Switch, further strengthening New Era's capabilities as it advances its digital infrastructure and power development platform.

Read More: https://t.co/qTC8W7oC0T

$NUAI just brought on Evan Pierce as Chief Development Officer.

Below is a brief summary of his experience:

Nuclear operator (Comanche Peak, San Onofre)

ERCOT reliability coordinator

AWS - data center capacity expansion and business development

TikTok - Head of Data Center Energy & Sustainability, AMER and EMEA

EdgeConneX - VP of Site Development & Energy Development, Americas

People with this resume don't join micro cap companies for a salary. They join because they see something others don't. I would not be surprised if he brings in a wealth of new connections and opportunities for $NUAI much like Ted Warner did on his arrival.

Maybe what he is seeing at $NUAI is hard to ignore?

The company has a New Mexico site with up to 5GW of nuclear capacity and 2GW of natural gas on deck.

You don't recruit a CDO who spent his career scaling hyperscale energy at AWS, TikTok, and EdgeConneX unless you're planning to actually build something.

I found this particularly interesting. He began his nuclear career as an Equipment Operator at Comanche Peak Nuclear Power Plant operated by Luminant, a Vistra company. Vistra sits right across the road from TCDC. I would not take this as a signal but would in some fashion highlight he has intimate knowledge of the industry and knows what needs to be done at the $NUAI level to get this deal across the finish line and expand the $NUAI footprint to future sites.

The talent being attracted doesn't lie. I saw this post via LinkedIn this morning. Looks like the thesis continues to play out for $NUAI.

$NUAI: The Last Asymmetric Bet in the Data Center Trade

Look across the small-cap data center cohort right now. NUAI is the only remaining sub-$500M name with a real, exclusive, late-stage hyperscaler negotiation in motion. And after parsing the Q1 2026 call, conviction goes up, not down.

The Lease Math Now Works Backwards From 2027

Charlie Nelson laid out the schedule cleanly:

"Our schedule is largely driven by power availability. The power that we have available in phases 1 and 2 is in second half of 2027. Everything that we're doing is kind of back-solving from those dates... We still feel good about second half of 2027 in-service date for the first phases of this."

Working backwards from ~August 2027 with Stream's compressed 12-14 month build cycle, the lease has to be signed by July or August 2026 to preserve schedule. The construction calendar is a hard forcing function — every party at the table knows it, including the hyperscaler.

The Documents Are Closer Than Anyone Realizes

When asked about sequencing, Charlie was specific:

"The JV docs are well underway, multiple turns already with the lawyers, and the lease as well, as well as the PPA. All of these are progressing concurrently... And this is how it goes with most of these types of industrial developments — concurrent execution, especially when they're all kind of lining up around the same time, just makes sense. And you just kind of have a signing day, if you will. A very fun day, by the way, for any industrial development."

"Multiple turns" means the documents are mature. What's left should be legal documentation — a slower, more deterministic process than commercial negotiation. The phrase "signing day" is not casual. It's deal-maker code for a coordinated execution event where multiple interdependent documents close together.

The Hyperscaler Engineered This Deal

This is the part nobody is talking about enough. The hyperscaler wasn't recruited. They initially came to NUAI wanting to buy the land. Ted Warner walked through the sequence:

"We were also getting offers to buy this from actual hyperscalers... One of those we did, we signed an exclusivity agreement because we kept turning them down on selling, and we wanted to work with them on how can we partner with you to own something here. Essentially, it was, 'You've got to work with a really reputable developer.' We went and tried to find one, that exact same party sort of led us to a different party. Now here we are with that party, Stream."

The hyperscaler directed NUAI to Stream. They didn't just suggest a developer — they pre-approved their own counterparty. Stream walked in with existing commercial agreements and pre-approved designs with this specific hyperscaler. Charlie confirmed it:

"Having pre-approved designs with this particular hyperscaler, which is why we were guided into the relationship with them, frankly — to the fact that they house long lead time equipment that goes towards these projects, and it's a rinse and repeat design."

A hyperscaler that takes the time to direct partner selection, share technical specs, sign exclusivity, and cooperate through a developer restart is not a hyperscaler that walks away at the finish line. That's a counterparty that has been quietly engineering the conditions for this deal to close on terms they already endorsed.

And It's the Same Hyperscaler

Ted's clarification on the Sharon AI confusion was the most underrated moment of the call:

"The same party, that hyperscaler is still the person that we hope will be our tenant, that our designs are specifically for... [Stream has] been incredible to work with, just every day checking boxes. It's been awesome to watch them work."

No one walked. The hyperscaler that wanted this site in 2025 still wants the site in 2026. The designs are still tailored to their specs. The exclusivity is still in place.

The Balance Sheet Is Built For This

Ted's segment removed the financing overhang that haunted this name for months. $80M+ cash on hand. $290M Macquarie credit facility. The Sharon AI note is gone. Liens lifted. They illustrated the math:

"Our cash needs for phase one would be roughly $180 million before the credit that we'd get for the land contribution... That theoretical $180 million investment is more than covered for phase 1."

NUAI's expected equity check for Phase 1 is fully funded. No more "how do they pay for this" question hanging over the stock.

The Setup

The market just sold the stock 11% on a quarter that confirmed every workstream is on track

The lawsuit resolution should come soon

PPA likely ready first

JV DA close behind — Stream is the most motivated party in the deal

Hyperscaler lease execution window: late June through Early August 2026

One signing day, three documents, complete rerate

This is the playbook setup for an asymmetric trade. The downside is bounded by the cleaner balance sheet, the Stream-driven execution model, and the standing hyperscaler engagement. The upside is a name with a sub-$500M market cap signing a lease comparable to deals that already moved peers multiples higher.

"As a shareholder, I sit here with you, and I wish I could announce who the prospective tenant is, and I can't wait to announce it one day. We've been working very, very hard to get there." — Will Gray, closing remarks

NUAI is the last shoe left to drop.

https://t.co/kYQhkjttsK

I’ve brought up this question to people who know even more about the company than I do, and it seems like Will is someone who knows deeply about nat-gas and energy generation. He has deep connections with the local government and other partners in the ecosystem which allowed $NUAI to secure long lead time items that usually take 3y+ to obtain.

Now, with that being said it’s obvious that he isn’t the best speaker on podcasts or earnings calls. If you’ve listened to them it’s usually Charlie Nelson doing the talking and Will is more of the figurative head of the company. The people that Will is surrounded by are exceptional people, like Ted Warner, Charlie Nelson, and PJ Lee on the board of directors.

What I can say is that I am extremely confident they will secure this hyperscaler deal in the next coming months. The stock is currently trading at $3.90 at the time I’m writing this because of the lawsuit and the CEO’s negative image. The way you can capitalize off of this investment is being able to see through the negative optics and noise that is going around and looking into the thought process behind the heavy hitters like Macquarie and Apollo that are able to look deeper than anyone can.

Another thing to remember is that you aren’t trusting Will to be able to build the datacenter himself. NUAI’s role in this TCDC project is putting up the land for phase 1 and bringing the partners together on the project and then for phase 2, BTM power too. Stream is going to be handling the execution of the project, who was selected by the hyperscaler after working with them previously. TCDC’s campus is the only plot of land that this specific hyperscaler can use for their ESA for 200MW with Calpine and Vistra who are right next door. That is a binding agreement already. Follow the clues and it will pay off.

![litigious_dulce's tweet photo. $NUAI: The Last Asymmetric Bet in the Data Center Trade

Look across the small-cap data center cohort right now. NUAI is the only remaining sub-$500M name with a real, exclusive, late-stage hyperscaler negotiation in motion. And after parsing the Q1 2026 call, conviction goes up, not down.

The Lease Math Now Works Backwards From 2027

Charlie Nelson laid out the schedule cleanly:

"Our schedule is largely driven by power availability. The power that we have available in phases 1 and 2 is in second half of 2027. Everything that we're doing is kind of back-solving from those dates... We still feel good about second half of 2027 in-service date for the first phases of this."

Working backwards from ~August 2027 with Stream's compressed 12-14 month build cycle, the lease has to be signed by July or August 2026 to preserve schedule. The construction calendar is a hard forcing function — every party at the table knows it, including the hyperscaler.

The Documents Are Closer Than Anyone Realizes

When asked about sequencing, Charlie was specific:

"The JV docs are well underway, multiple turns already with the lawyers, and the lease as well, as well as the PPA. All of these are progressing concurrently... And this is how it goes with most of these types of industrial developments — concurrent execution, especially when they're all kind of lining up around the same time, just makes sense. And you just kind of have a signing day, if you will. A very fun day, by the way, for any industrial development."

"Multiple turns" means the documents are mature. What's left should be legal documentation — a slower, more deterministic process than commercial negotiation. The phrase "signing day" is not casual. It's deal-maker code for a coordinated execution event where multiple interdependent documents close together.

The Hyperscaler Engineered This Deal

This is the part nobody is talking about enough. The hyperscaler wasn't recruited. They initially came to NUAI wanting to buy the land. Ted Warner walked through the sequence:

"We were also getting offers to buy this from actual hyperscalers... One of those we did, we signed an exclusivity agreement because we kept turning them down on selling, and we wanted to work with them on how can we partner with you to own something here. Essentially, it was, 'You've got to work with a really reputable developer.' We went and tried to find one, that exact same party sort of led us to a different party. Now here we are with that party, Stream."

The hyperscaler directed NUAI to Stream. They didn't just suggest a developer — they pre-approved their own counterparty. Stream walked in with existing commercial agreements and pre-approved designs with this specific hyperscaler. Charlie confirmed it:

"Having pre-approved designs with this particular hyperscaler, which is why we were guided into the relationship with them, frankly — to the fact that they house long lead time equipment that goes towards these projects, and it's a rinse and repeat design."

A hyperscaler that takes the time to direct partner selection, share technical specs, sign exclusivity, and cooperate through a developer restart is not a hyperscaler that walks away at the finish line. That's a counterparty that has been quietly engineering the conditions for this deal to close on terms they already endorsed.

And It's the Same Hyperscaler

Ted's clarification on the Sharon AI confusion was the most underrated moment of the call:

"The same party, that hyperscaler is still the person that we hope will be our tenant, that our designs are specifically for... [Stream has] been incredible to work with, just every day checking boxes. It's been awesome to watch them work."

No one walked. The hyperscaler that wanted this site in 2025 still wants the site in 2026. The designs are still tailored to their specs. The exclusivity is still in place.

The Balance Sheet Is Built For This

Ted's segment removed the financing overhang that haunted this name for months. $80M+ cash on hand. $290M Macquarie credit facility. The Sharon AI note is gone. Liens lifted. They illustrated the math:

"Our cash needs for phase one would be roughly $180 million before the credit that we'd get for the land contribution... That theoretical $180 million investment is more than covered for phase 1."

NUAI's expected equity check for Phase 1 is fully funded. No more "how do they pay for this" question hanging over the stock.

The Setup

The market just sold the stock 11% on a quarter that confirmed every workstream is on track

The lawsuit resolution should come soon

PPA likely ready first

JV DA close behind — Stream is the most motivated party in the deal

Hyperscaler lease execution window: late June through Early August 2026

One signing day, three documents, complete rerate

This is the playbook setup for an asymmetric trade. The downside is bounded by the cleaner balance sheet, the Stream-driven execution model, and the standing hyperscaler engagement. The upside is a name with a sub-$500M market cap signing a lease comparable to deals that already moved peers multiples higher.

"As a shareholder, I sit here with you, and I wish I could announce who the prospective tenant is, and I can't wait to announce it one day. We've been working very, very hard to get there." — Will Gray, closing remarks

NUAI is the last shoe left to drop.

https://t.co/kYQhkjttsK](https://pbs.twimg.com/media/HIroOK1X0AA6Mm6.jpg)