A clear investing philosophy cuts through the noise. If you’re serious about investing, you need one.

• PART 0: Different Camps of Value Investing

• PART 1: A Silly Example: Grocery Shopping

• PART 2: Act like a Business Owner

• PART 3: Evolving Definitions of “Cheap” and Accounting Trickery

— 3a: Enterprise Value

— 3b: Free Cash Flow

— 3c: Buffett’s Strict Owner’s Earnings

• PART 4: MISC Learnings

• PART 5: Management

https://t.co/7TW3pmVhQc

Simply too cheap for a company with that level of cash flow, don’t care how much they’ve shrunk. $50m/qtr in FCF for a software company like this at a $388m mkt cap is a STEAL

Been too busy to post about $BMBL but it was looking so juicy in the $2.50’s … 👀

I acquired a position a week or two ago and seems to be rocketing on acquisition buzz

$216m buyback authorization

$360m total mkt cap

~$200m in FCF/yr

Already paid their final TRA payment ($156m) for the year in Q1 (no significant payment expected in ‘27 nor ‘28 either)

Debt situation is high relative to mkt cap but with that much earning power relative to valuation I don’t care. They just need to survive and buyback stock.

I was in $ALIT at $0.66 cents a month ago and it quickly hit $1. I’m not one to turn down a 50% one week gain so I sold it. Now it’s back to where I initially bought and I’m reopening a position.

Nobody owes you anything

You’re not owed praise

recognition

sex

money

thank you’s

The world doesn’t owe you shit

Humble yourself in every way

Understand it is actually the opposite.

YOU owe the world.

You owe the world your toil.

You owe it to those who raised you

You owe it to your friends

You owe it to God

You owe it to yourself

It is your moral duty to give back to the world that gave you life

Go for a walk, smell the flowers, tune out the voices. Take joy in what you have. Pray to God. Take your eyes off the goal at times. Life is a gift. Fickle. And meant to be maximally enjoyed.

And then… go work your ass off for all of those who you owe it to.

My wife mentioned a nice private school over dinner this week

She said the campus was beautiful

I asked what's the tuition

She said we should look at it as an investment in him not a cost

I made a note

She said don't make a note

I said I always make notes

She said this isn't a deal

I said everything is a deal

She closed her eyes

She said we'd discuss it Saturday

I agreed

Saturday 7:02am

She came downstairs in her Saturday robe

Coffee in hand

I had my cargo shorts on

The dining room had been cleared

The projector was on

The analyst was at the head of the table

Quarter zip on, three iced coffees, a legal pad, and two laptops

He had been there since 6:44am

I texted him at 11:14pm Friday

The text said dining room 6:45am bring the model

He sent a thumbs up

My wife stopped in the doorway

She said what is this

I said you said you wanted to discuss it

She said this is not a discussion

I did not respond

She sat down anyway

The analyst stood

He said good morning ma'am

She did not respond

He sat back down

A printed deck in front of each seat

A fourth copy in case

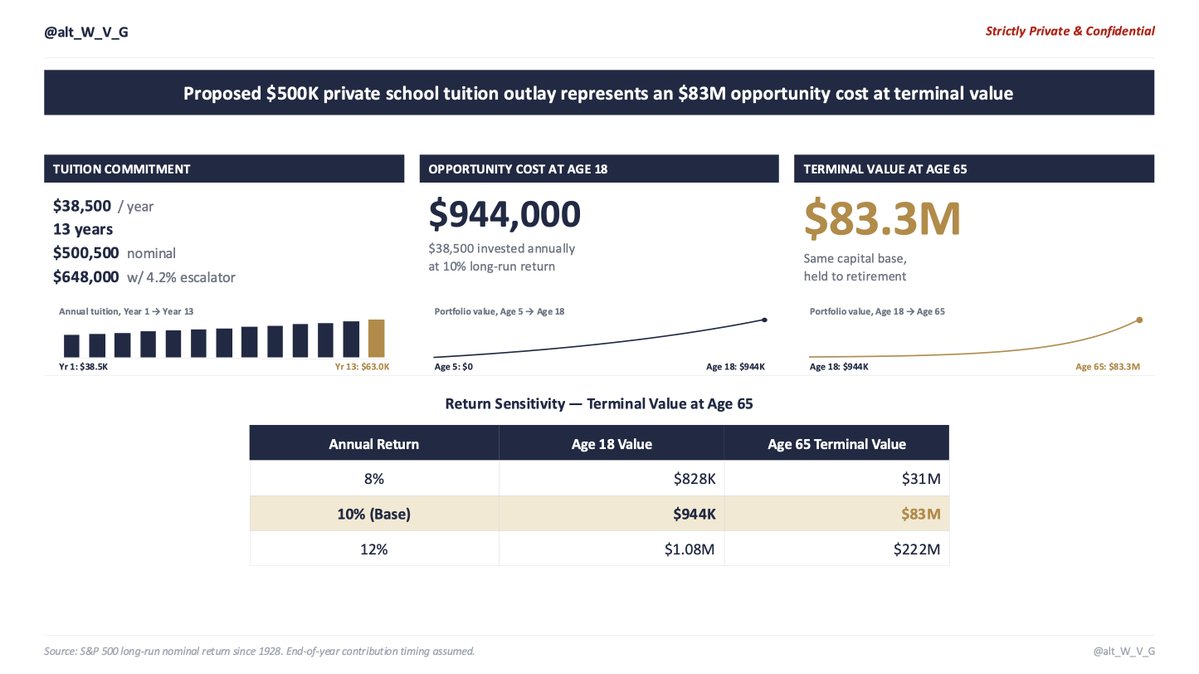

Slide 1 Tuition Schedule

$38,500 per year

Thirteen years

$500,500 nominal

Before escalators

The school has raised tuition 4.2% per year for a decade

With escalators $648,000

My wife said okay

I said I'm not done

Slide 2 Opportunity Cost

Even before escalators

$38,500 invested annually

10% nominal return

S&P long-run average since 1928

By his eighteenth birthday $944,000

My wife said we can afford it

I said I know that's not the slide

Slide 3 Terminal Value at Age 65

$83 million

She was quiet

The analyst slid the sensitivity tables across the table

8% return $31 million

10% return $83 million

12% return $222 million

She did not look

She said this isn't about money

I said it's always about money

She said no it isn't

I said then what is it about

She did not answer

She said you can't put a dollar value on his teachers his classmates his environment

I said I can the analyst already did slide 6

He flipped to slide 6

She did not look

She said the school is the best in the city

I said best is a feeling

She said it produces the best students

I said the students were already the best before they got there

She said our son deserves it

I said our son deserves $83 million

My son walked in

He is five

Dinosaur pajamas

He looked at the projector

He looked at the open deck on the table

He looked at slide 3

He said are we modeling pre-tax or after-tax

The analyst opened a new tab

My wife looked at the ceiling

He said what's the discount rate

The analyst set down his pen

She closed her eyes

He said is this the same return assumption from the 529 conversation

The analyst stopped typing

He looked at me

I did not say anything

She stood up

Sat back down

He said dad can I help

I said yes

He pulled up a chair

The analyst handed him a printout

He started reading

My wife watched him read

She watched him for a long time

She said his name

He looked up

She said do you like school

He said the work is too easy and the kids don't ask questions

She did not respond

She looked at the ceiling

She walked out of the room

The analyst started packing up

He said should I follow up Monday sir

I said no follow up needed

He'll be fine

Sent from my iPhone

Unfortunately X is shutting down communities so this small group will be gone soon!

Feel free to follow me if you still want to occasionally hear about investing from yours truly

Yes the proxy gave an initial liquidation distribution estimate

It’s $.061 to $3.48

So a lot of upside but also a lot of potential downside. The big swing almost completely comes from their equipment / IP sale. Thats too speculative for me personally.

I’m not gonna bet on the IP stack being worth a lot.

Kind of the opposite of margin of safety actually

$ORGN up 36% on liquidation estimates as high as $3.48 a share.

Low end of estimate is a lot lower though. Theres still potential here but this is good enough for me, I’ll probably bail out without a more solid margin of safety

@shravanrayhaan If it drops back to low $1’s again I’ll consider the same speculative position again. But close to $2 felt like the right time to sell at current liquidation estimates

I (literally) sat on my keyboard one day while browsing stocks and this thing popped up. After its 1st real earnings, it’s my favorite position.

$VSNT with a huge quarter. Pretty much as expected. Biggest part is the revenue looks fairly solid, and cash flows even sturdier.

$500m+ in FCF/owner earnings this quarter. For a $6B market cap, this thing trades at a cheaper multiple on a quarterly basis than some media companies annually. If they keep up the pace and go for $2B in FCF/owner earnings this year, there’s no way they trade at a 3x multiple forever. This thing will rerate hard.

Maybe the safest feeling position in my portfolio right now. Bought back $100m of stock this quarter too. Announced another Accelerated Share Repurchase for $100m that they expect to complete 2nd quarter.

Just paid out $50m in dividends to shareholders this quarter. Thats a 3.5% dividend yield on top of a still super cheap stock.

Theres a lot going for this stock, and the only thing not to like is the $2B they paid Comcast in fees to split off. Thats long term debt on the balance sheet for now, but it’s the only debt they have.

I got in low $30’s. I think this thing hits $100 eventually.

❕The 14th largest U.S. homebuilder $DFH wants to gobble up the 21st largest $BZH to make themselves the 8th largest

The offer is for $25.75/share (Beazer was trading at $18ish)

Beazer says their book value is $41.83/share. Which might not actually be far off. Their balance sheet actually looks great. The business seems mismanaged.

Book value isn’t hard cash of course, it’s land, inventory, lot deposits, debt, dreams and vibes

It’s not an intangible goodwill piñata either though. These are hard assets

It’s actually right up Mr. Zalupski’s alley. Take a land heavy builder, shove it through the land light playbook, cut SG&A, and keep the growth coming.

Of course this doesn’t come with risks.

Dream finders is levered.

Beazer is levered.

Putting two levered homebuilders together is not necessarily “margin of safety”.

But it is a very $DFH specific arbitrage.

Buy cheap land-heavy assets, use land banking to avoid tying up the entire balance sheet, turn inventory faster, and fuel growth through acquisition.

If they continue to pull it off, their growth will be fiery and they’ll look like geniuses. But if the housing market turns, they might be underwater

There’s a new guy in town though, Kevin Warsh, and while it remains to be seen what he’ll do with rates, this might turn into huge upside if rates come down after all this oil stuff calms down.

WOAH

Beazer Homes stock jumps up +30% this morning after Dream Finders Homes—America's 14th largest homebuilder—publicly announces it has bid $704 million to acquire Beazer Homes—America's 21st largest homebuilder

$BZH looks significantly undervalued from a balance sheet perspective. Cash flows says the business has been woefully mismanaged. This feels like the exact kind of acquisition $DFH is known so well for pulling off.

I agree $BZH has been mismanaged AND $DFH is trying to steal this asset

More power to them. Probably should have got long this baby $NVR long ago

Watching this one with interest