It’s not just US domestic deposit flight…it’s all deposit flight to US-denominated, non-domiciled stablecoins.

V1 Eurodollar was an accidental phenomenon, followed by LIBOR, swap lines, and eventual financial integration.

With V2 Eurodollar, led by USDT, it will likely follow a similar path to integration, but this new iteration is a hostile viral cordyceps that will dig deeper into the nervous system of global currency markets.

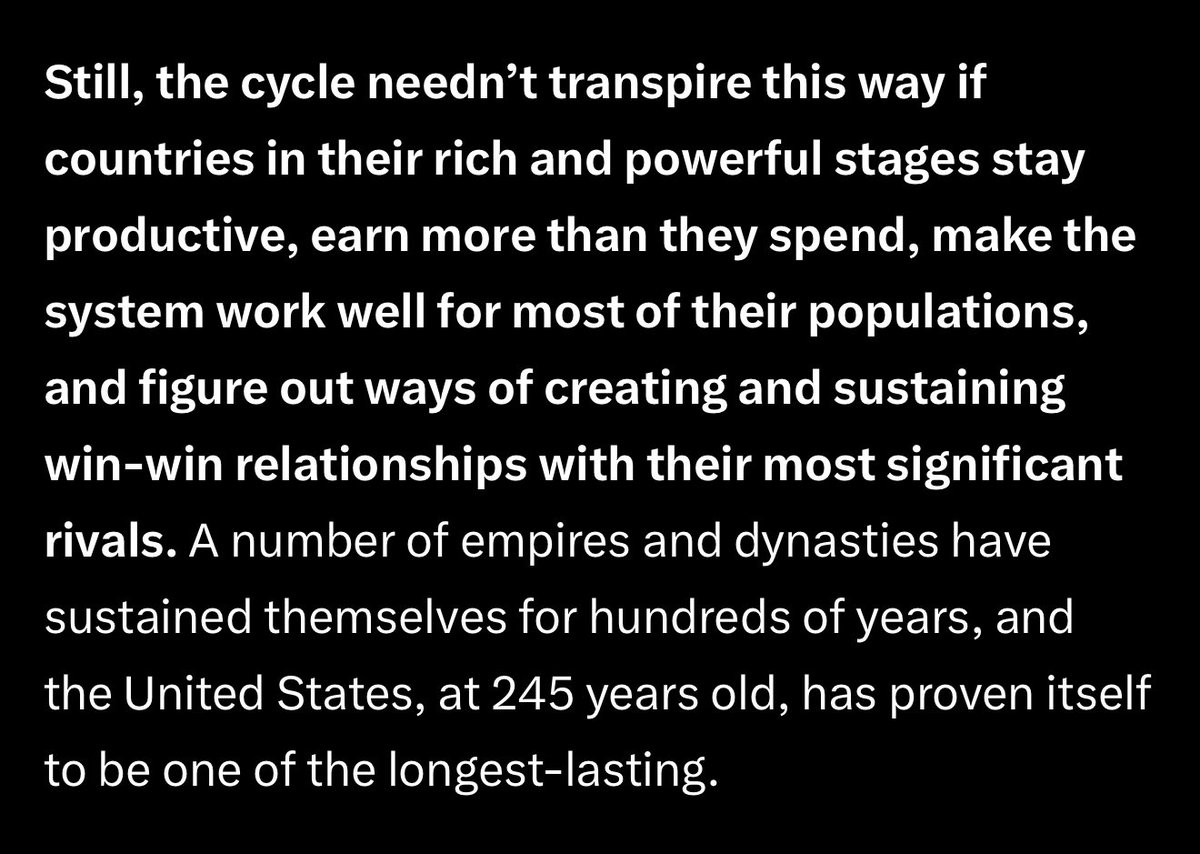

Everyone is walking away with a doom scenario from Dalio’s post, but the most important part is the last sentence of the last paragraph: the staying power of the US.

As Dalio points out throughout, at the end everything ultimately comes down to the propensity to execute efficiently on the threat of violence.

The United States is a well-oiled violence machine with real-world reps at scale that is unmatched.

To ease anxiety, have a good bug-out bag that includes gold coins so you can pay the captain of the ship you board to leave your country if things go to shit, plus a few more gold coins to get you settled. Stack Bitcoin for ultimate wealth portability, procure a firearm to protect said gold coins and family. Once you have that, keep calm and carry on.

@ZeroHedge_@GrantCardone BRICS being successful at cutting out the dollar is one of many probabilities.

It has a EV of about 15% +/- 10

Everyone wants to cut out the US but tbh, there is value in the status quo that many don’t price in.

With precious metals now acting like crypto, perhaps the ease of storage, tight spreads, and portability of Bitcoin will capture more of the SoV mindshare.

Bitcoin can’t beat thousands of years of decentralized on/off ramps like jewelry and pawn shops, but it can still win if the price moves up one more power level.

Hasbro is being sued by its own shareholders for printing so many damn Magic cards, 'destroying the long-term value of the brand' https://t.co/k4du7M5NEe

Fun fact: There was a decent shot Walmart (and nearly every major retailer) would’ve accepted Bitcoin payments pre-2020 because of the QR based payment cabal, MCX, the retailers created to rival Mastercard and Visa.

I know because I was in the trenches with them.

Everyone talks about “loyalty” programs in crypto, without knowing anything about how that business or how the balance sheet requirements works. It’s not even universal, with many regional consumer regulatory frameworks impacting them.

I got a deep look in that industry, helping some of the largest programs in the world.

Loyalty points are more permissive in their structure, but have other rules.

Loyalty programs do not want to adopt stablecoins to fully back points and carry that backing in their balance sheets. That compromises the value of their programs.

There are other uses for stablecoin-like features, and tokenization, but stablecoins as is, is not the solution.

I hear different “loyalty program” pitches regularly, but people just don’t understand the core business, and what makes it attractive to operate at scale.

@tempo Think about big companies with loyalty points.

Loyalty points are liabilities.

Every point you issue sits on your balance sheet as a debt.

Airlines manage billions in outstanding miles. CFOs hate it. The whole model depends on "breakage" - hoping customers forget to redeem.