Bristlemoon just published a 16k+ word report on $FICO, the credit score monopolist that has increased its mortgage scores prices by 800% over the last three years. We explore how entrenched FICO is in the US credit ecosystem and whether the company still has pricing power...

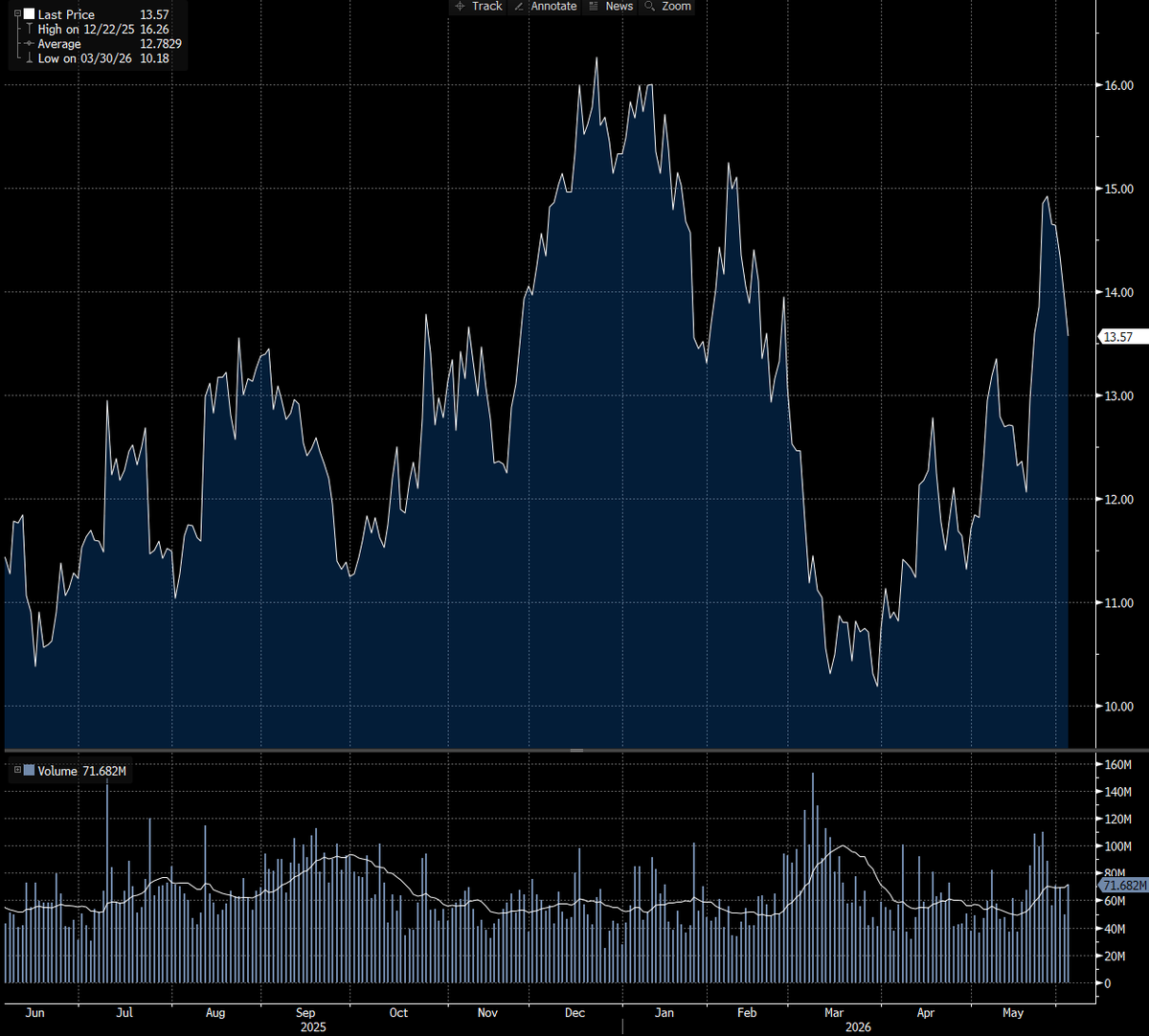

Published a piece on Infineon $IFX $IFNNY the big chungus of power semis and microcontrollers. We discuss the power conversion challenges posed by MW-scale AI racks, the transition to 800V DC architecture, and the AI DC opportunity for IFX. We also touch on the challenges that the automotive division has faced, the AI power opportunity within the laggard Green Industrial Power division, and whether there’s evidence of an emerging MCU shortage.

IFX stock has tread water for much of the past 4 years since the post-COVID automotive upcycle ended, before doubling in the space of 2 months as an AI play. Solving the power delivery constraint requires a complete overhaul of the traditional LVAC à 54/48V layout to an 800V HVDC architecture, which rely heavily on the wide bandgap semis, power MOSFETs and VRMs that form the core of IFX's power portfolio.

Mgmt has guided to AI power revs of €1.5B in FY26 and €2.5B in FY27, representing 9% and mid-teens% of total revs. Considering STMicro $STMPA just u/g its DC guide earlier this week from $500M/$1B to $1B/up to $2B for 2026/27, there is likely upside to IFX’s AI numbers as well.

Mgmt also had a 2030 SAM target of €8-12B, but as of last quarter, has replaced this with a $100-250/kW content range with an average of $175 today. This change was purportedly because some forecasts for 2030 GW deployed are now much higher than what’s implied in that €8-12B SAM i.e. there’s upside to that range. But curiously, mapping the €8-12B back to $100-250/kW content already necessitates as much as $3-4T of capex in 2030 – something that arguably only Jensen believes in today.

IFX claims to have 30-40% of the AI DC power semis market (in line with its overall DC share) which we think is ballpark true based on peers’ disclosures of DC revs and would make IFX the leader in AI power semis. We believe the company is well positioned to extend its share esp in the high value VRM stage with its vertical power delivery module, which mgmt flags is at the high end of the $/kW content range.

However, we would be wary against overextrapolating the content opportunity from the 800V transition, as some elements of the existing power delivery chain will be cannibalised/eliminated. As such, the AI power opportunity seems more like a volume play to us (GW deployed) with modest net $/kW content uplift across the power stages – though IFX can always outgrow the market through share gains.

Two other opportunities that we think are interesting and don’t get much airtime today:

1) IFX has €500M of non-AI DC revenue, and its conventional server business is 10% of group revenue (~€1.5B). Given the anticipation around CPU demand from agentic AI, it wouldn’t surprise us if IFX’s non-AI DC revenue doubled or tripled over the same 5Y timeframe.

2) Solid state transformers, which contain a tremendous amount of WBG semis content vs 0 for conventional transformers, could open an incremental $1-2B high margin market for IFX by 2030.

Unlike some of the more speculative AI pumps, we’d say the rerating of the power semis sector more broadly is not without merit. The 800V transition has legs and is a quasi 0-to-1 opportunity i.e. even if Rubin and RU-class sales are flat vs Blackwell, the 800V transition must still happen and is a big content uplift opportunity for power semis suppliers. Ultimately, we like IFX as a business, but the violence of the recent rerating has likely pulled forward substantial future returns and leaves us lukewarm on IFX as an investment.

Bristlemoon just published a report on Infineon Technologies (IFX GY), the power semis company that's set to benefit from the shift to 800VDC rack power architecture for data centers. We look at the physics behind this conversion, why it's consequential, and how IFX benefits.

@anvil_capital@MikeFritzell Jedi level thinking. Know the details, but know that it probably doesn't matter re vals as long as fundamentals are accelerating and there are enough people willing to buy that accel.

@orrdavid@the_fat_pitch@MikeFritzell I'm in the same boat. Have been long $NVDA and $ASML. Haven't done badly but they're boring vs. the memory bottleneck and everyone wants torque.

$ULCC another example (although they're also getting route recapture from Spirit bankruptcy which is leading to an RASM uplift). According to the mkt, the conflict has been a net positive for Frontier Airlines.

$AAL & various other US airlines are good examples of rates of change mattering more in this mkt regime vs valuation in a vacuum. Airline stocks dumped in March (no surprise why), but then most staged a significant rally off the back of ceasefire/peace talks (bad situation getting better). The fact that $AAL rallied above where it traded pre-Iran is kind of wild.

One of the greatest energy disruptions of our generation yet the mkt shrugged it off and is willing to look through to 2027 & price the stock back to pre-war levels bc the 2nd deriv is positive and news was getting better. The bull case is RASM is strong and fuel recapture will sequentially improve as we move through '26, and mkt is already looking through to '27 where we might see alleviation of jet fuel costs but airlines probably won't pass back all ticket price increases (i.e., margins could expand as ticket prices remain elevated yet CASM normalizes).

Mkt is making a call around SoH closure being temporary/isolated to '26 and mkt overall feels quite complacent as to whether Iran situation drags on and the fallout from that re inventory draws, energy prices spiking back up. So maybe some of these airlines are asymmetric on the downside to the extent that the mkt has gotten too excited re a peace deal and the path to get paid as a long requires imminent SoH reopening + minimal impact on fuel costs in '27.

If you'd told me back in early March that the SoH would be shut and remain shut until June, yet $AAL would be the same price, I would have laughed. Yet here we are.

$AAL & various other US airlines are good examples of rates of change mattering more in this mkt regime vs valuation in a vacuum. Airline stocks dumped in March (no surprise why), but then most staged a significant rally off the back of ceasefire/peace talks (bad situation getting better). The fact that $AAL rallied above where it traded pre-Iran is kind of wild.

One of the greatest energy disruptions of our generation yet the mkt shrugged it off and is willing to look through to 2027 & price the stock back to pre-war levels bc the 2nd deriv is positive and news was getting better. The bull case is RASM is strong and fuel recapture will sequentially improve as we move through '26, and mkt is already looking through to '27 where we might see alleviation of jet fuel costs but airlines probably won't pass back all ticket price increases (i.e., margins could expand as ticket prices remain elevated yet CASM normalizes).

Mkt is making a call around SoH closure being temporary/isolated to '26 and mkt overall feels quite complacent as to whether Iran situation drags on and the fallout from that re inventory draws, energy prices spiking back up. So maybe some of these airlines are asymmetric on the downside to the extent that the mkt has gotten too excited re a peace deal and the path to get paid as a long requires imminent SoH reopening + minimal impact on fuel costs in '27.

If you'd told me back in early March that the SoH would be shut and remain shut until June, yet $AAL would be the same price, I would have laughed. Yet here we are.

Population of Australia in 1990: 17 million.

Now: 28 million

I looked at the incremental 11 million people and thought "wow, that's a lot" (c.65% cumulative increase), but it also pencils out to a measly 1.4% annual growth rate.

@patrickc@pmarca The problem is that the mechanisms for absorbing the shock are finite (at least in the ST), and give people (investors, perhaps even govt) the false sense that Hormuz was overblown. But unless SoH reopens imminently, the math re shortages is difficult to refute.

c. 10% of advertiser budgets are for testing (presumably spread across many platforms like $PINS, $SNAP, $RDDT, TT, and new features on $META / $GOOGL) according to @eric_seufert in the latest @stratechery interview.

To me that says a meaningful amount of budget could be reallocated to $APP once self service moves to GA next month. Much like $NFLX introducing its ad tier at $65 CPMs and advertisers being willing to pay that (i.e., ROAS-insensitive, at least initially) just to test the new platform, I suspect there will be a ton of experimental spend flowing to $APP in a way which could see a wall of ad $ hit their platform. Could be some pretty crazy numbers around the Consumer ramp for $APP ...

Full quote from Eric below:

"Well, I think it��s a little bit more than some incidental amount of money. A lot of advertisers use 10% as a rough benchmark for testing budget, now that’s 10% with no ROAS accountability, so now imagine clawing a lot of that back because I’m pre-testing, I’m pre-testing with the model that’s been distilled on their model, it’s a lot."

@Larryjamieson_ Pretty soul sucking. But if there are ways to make money I guess people will find them.

Substack (and X) should find ways to penalise AI driven content (not in their ST monetary interest to do so, but affects the LT health of the platform).