⚡️Canada is a rich-country warning flare.

The country did not suddenly break.

It spent years converting future capacity into present comfort through housing, leverage, population growth, and state-managed consumption.

Now the bill is showing up.

Canada has enormous natural advantages: land, energy, minerals, water, agriculture, institutional stability, proximity to the U.S., educated labor, and strategic geography.

A country with that asset base should be one of the great productive powers of the 21st century. Instead, much of the national growth model became a loop of importing people, inflating housing, expanding household debt, taxing/redistributing around the pressure, and calling the aggregate number progress.

That model creates GDP, but it does not necessarily create prosperity.

The core sickness is per-capita stagnation hidden by headline scale. A country can grow on paper while the median person feels poorer, more crowded, more indebted, less housed, and less hopeful. That is Canada’s fracture. The macro story and the lived story diverged for too long.

Housing became the false god. It absorbed savings, distorted politics, rewarded incumbents, punished young families, and redirected capital away from productive enterprise. When a country’s main wealth engine is bidding up shelter, it eventually starts consuming its own future. Young people lose formation. Families delay. Businesses struggle. Talent leaves. Politics curdles.

The recession print is the surface crack. The deeper fracture is that Canada’s old growth engine has stopped producing legitimacy.

Tariffs and weak jobs matter, but they are accelerants. The deeper problem is strategic drift. Canada did not build enough future-facing industrial strength relative to its potential. Energy could have been a sovereign superpower. Minerals could have been a strategic weapon. AI power infrastructure could be a national moonshot. Instead, the country over-indexed toward housing, bureaucracy, compliance, redistribution, and moral-managerial politics.

The U.S. has plenty of dysfunction, but it still creates monsters: Nvidia, OpenAI, SpaceX, Palantir, Anduril, hyperscalers, shale, venture capital networks, deep markets. Canada produces capable people and then often loses them into stronger systems. That is the brutal asymmetry.

The policy path ahead probably becomes rate cuts, fiscal support, more housing intervention, immigration recalibration, and attempts to cushion households. Some of that may stabilize the surface. It will not fix the core unless Canada shifts from asset inflation toward productive power.

The real question is whether Canada chooses productivity or keeps protecting the old model.

Productivity means energy development, industrial strategy, permitting reform, housing supply, capital formation, defense/AI/minerals infrastructure, and a political culture that rewards building. The current model means more debt, more transfers, more housing distortion, more young-person despair, and more dependence on U.S. demand.

Final compression:

Canada is not poor.

Canada is misallocated.

The recession is the signal that the housing-population-debt model has reached exhaustion.

A country with immense real assets forgot to build enough real power.

Food for thought.

Will the CLARITY Act wake investors up to the real carry trade?

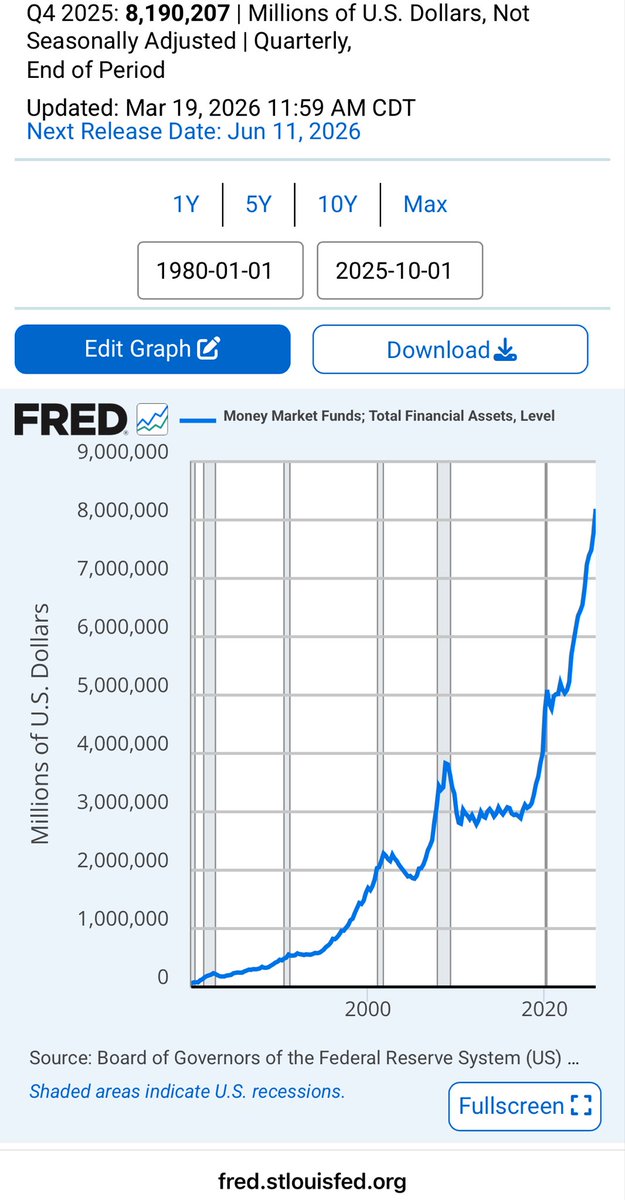

More than 7.75 trillion dollars now sits in US money market funds, while roughly 3 trillion in reserve balances is parked at the Federal Reserve earning about 3.65%. That is over $10 trillion still chained to the logic of the old monetary order, accepting what looks like “safe” yield even as the purchasing power of the underlying currency is steadily eroded.

Since the gold window closed in 1971, broad money has exploded growing at close to 8% p/a; the fiat unit of account is designed to grow, yet savers are asked to pretend that a nominal rate a few points above zero is “risk‑free.” Sensible is not the same thing as efficient. Nor is “risk‑free” the same thing as preserving real wealth.

The thesis of the incumbent system is simple. Safety lives in bank deposits, Treasury bills, central bank reserves and government‑only money funds. Investors, chastened by crises, park cash in money markets for liquidity and low volatility. Banks, scarred by regulation, leave reserves at the Fed for a predictable overnight rate and a quiet life with supervisors.

The classical carry trade built on this foundation was straightforward: borrow cheaply at the policy rate and reach a little for yield in duration or credit, clipping a modest spread. Now add the risk free rate in the digital world.

The antithesis is already visible in the digital world. Instruments linked to Bitcoin‑centred balance sheets and digitally native structures are building a different yield curve. Strategy’s STRC, a perpetual preferred backed by a Bitcoin‑levered corporate, has recently offered an annualised 11.5%, paid monthly, with distributions structured as return of capital rather than ordinary income.

It is not a Treasury bill, and there is balance‑sheet risk. But it shows that the market can engineer “cash‑like” exposure with double‑digit, tax‑efficient payouts, anchored in hard digital collateral rather than in the spread between overnight funding and a five‑year note. Bitcoin itself sits at the philosophical core: its supply is capped at 21 million coins, while fiat continues to expand.

The synthesis is a new definition of “risk‑free” and a new destination for the global carry trade. Public debate still obsesses over the dialectic of stablecoins versus bank deposits. The Digital Asset Market Clarity Act of 2025 would create a federal framework for digital asset markets and formalise regulatory boundaries.

More important is what such a law would symbolise: a tacit admission that a parallel monetary system is being built on top of the US dollar and Treasury market, but with yields discovered in competitive digital markets rather than by the constricted economics of legacy banks. Fully collateralised, dollar‑denominated, Treasury‑backed structures on public rails can in principle offer both the credit quality of the US sovereign and higher, more transparent yields than the old deposit‑money market complex.

This does not make every high‑yield token or Bitcoin‑linked security safe. It does mean that “risk‑free” in the old world has become a marketing phrase for nominal returns that often fail to protect purchasing power. Banks leaving reserves at 3.65 % are leaving money on the table. Investors accepting mid‑single‑digit money‑market yields in a structurally inflationary fiat regime are doing much the same.

The real question is whether the CLARITY Act will be remembered as the moment investors finally woke up to a generational shift: the point at which they realised that the true baseline for low‑volatility, dollar‑denominated returns had begun to migrate out of the old banking system and into a new, digital, USD Treasury‑backed monetary architecture.

Yes Bretton Woods 2.0 is upon us, the only question now is when will investors wake up to the opportunities in front of them.

Canada's CPI is ON TARGET at 2.36%/yr. Canada’s money supply (M3) is growing at 4.77%/yr.

That’s a bit below Hanke's Golden Growth Rate of ~6-8%/yr, a rate consistent with Canada's 1-3%/yr inflation target.

THE INFLATION STORY = A MONEY SUPPLY STORY.