1/ We'd also love to connect with organizations that can supply public goods like solar, water and carbon systems that can be installed via local entrepreneurs in the global south.

I'm looking to speak with the people who have done the most thinking at the intersection of crypto x circular economies.

Who should I be speaking with? @commonsstack@owocki@HumanityCash

Pls reply in comments!

@Eli_B_Cook מתכנתים לא יפגעו, להיפך, אני מהמר שהדרישה תגדל.

אין שום סיכוי (טכני, מתמטי) שai בטכנולוגיה הקיימת יכול להחליף אנשים. מה שכן הוא יכול ליצור המון אוטומציה שזה בעצם אומר המון תוכנות קטנות. כל תוכנה צריכה אנשים שיתחזקו אותה.

@TBariach@ryonnixon maybe that's because nvidia has a propriety product with low amount of competitors and it generates revenue for its share holders.

while ethereum has many competitors, no significantly better tech (that actually matters) and it barely generates profits

Last week, @ESultanik from @trailofbits reported to me an exploit in @revnets found by @AnthropicAI. All Revnet V5 funds were at risk.

Sunday i attempted a whitehat rescue of the funds. I successfully pulled $140k of funds belonging to the @Artizen ART revnet and @markee_xyz MARKEE revnet. In the process, I lost ~25 mainnet ETH from the NANA @juiceboxETH, REV @revnets, and BAN @bannynet revnets... due to my negligence in executing the script. MEV got the best of my urgency in the heat of the moment, despite thinking I did all I could to be ready to go. All other non-revnet Juicebox projects are unaffected.

For the past three months, I have been working on an "AI hardened" version of Juicebox – a fork of V5 that has gone through the ringer of any and all AI, harness, any novel auditing concept I could get my hands on. This weekend's exploit took advantage of a nuance in the revnet loans code that I had caught and fixed at the beginning of this process, but I had not realized it put funds at risk until reported by TOB and Anthropic.

I'm grateful we managed to keep customers' funds safe, and regretful we'll have to start our own businesses over. I'm frustrated at myself for having left the exploit in the original code, and for failing to recover all of it despite the opportunity. I'm encouraged knowing I've already been working on the solution and won't be starting this AI risk assessment from 0... the downtime will be relatively short.

But most of all I'm relieved that this AI security moment has come now, when funds at risk were relatively modest. I do not envy those with centi-million dollar protocols in production going into 2026. Despite doing all we could to get the Juicebox and Revnet V4/5 protocols audited over the past three years before deploy, the obsessive manual reviews and tests from ourselves and from top pros still missed what the latest AI crawlers have caught.

The other side of this diligence storm is sunny. This turbulence is a blessed precondition for open finance, one that will level up the quality of open source, enable anyone to run audits, and allow those of us who take responsibility over the integrity of these public tools to sleep better at night. We must get to the other side.

As usual, I will continue running my businesses using my own tools that I do everything to derisk, and I will continue telling others that they probably shouldn't follow my lead – the tradeoffs are real and borne by users of the open source. But I've found there are folks like me who stubbornly prefer assuming this risk if the reward is the freedom, agency, and strong guarantees the tools offer in their ideal form, unlike the corporate landscape of law-fare, capture, and executive discretion.

Reaching the ideal form is inevitable if we keep going at it. It is the holy grail. Open source, open accounting, and the open internet can and will outcompete everything, but damn the journey ain't easy.

On a practical note: V5 NANA, REV, and BAN holders will receive their V6 tokens as soon as the protocol is deployed, and we will restart revenue aggregation from there. MARKEE and ART holder will also receive their V6 tokens, and have their whitehat rescued funds added to their revnets to back the value of the tokens.

These next few weeks before we launch V6, we need all hands on deck pointing AIs at it and fishing for exploit opportunities, efficiency nudges, documentation clarification, and everything in between. JBX and REV rewards to those who report issues.

All you have to do is pull up Claude Code, Codex, or your favorite LLM and run:

"Clone github Bananapus/version-6 recursively, read AUDIT_INSTRUCTIONS.md, then walk me through my options for auditing this codebase. Ask me how deep I want to go, which subsystem interests me, and whether I have any specialization to add — then start."

I’m joining @Crypt0Mondays tomorrow to talk about why we're doing the opposite: building an "Etsy for private credit tokenization" where you can deploy a pool in minutes without a lawyer.

Register here: https://t.co/oGh8hgVrbZ

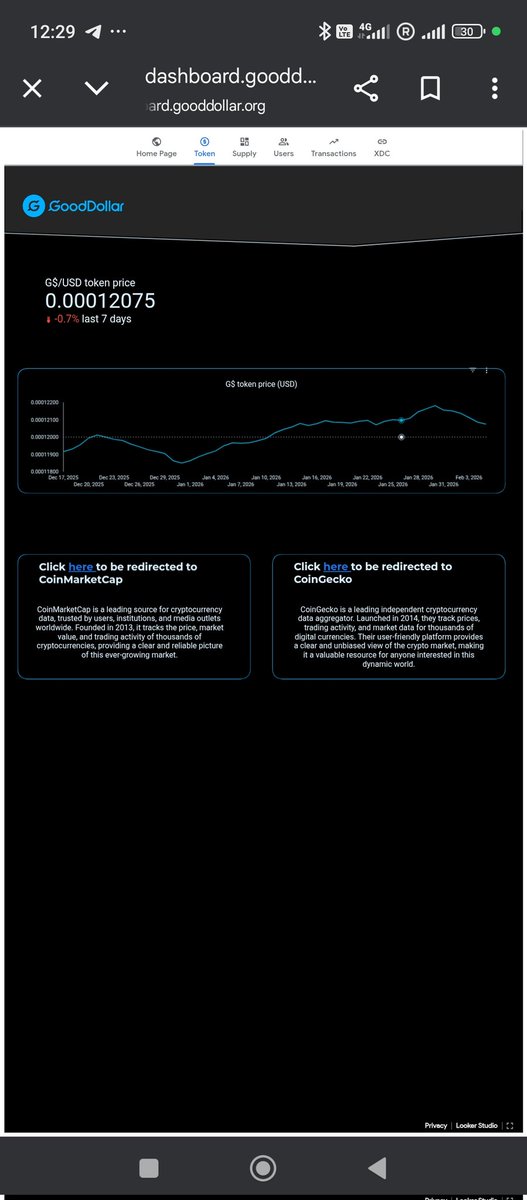

GoodDollar keeps growing 💙🌏

A new GoodDollar Reserve is now live on @XDCNetwork

✅ Native minting of G$ on XDC

✅ More collateral backing the protocol

✅ Expanding the infrastructure behind digital UBI

What this means for the future of UBI👇🧵

🔗 https://t.co/n8njPXhYoL

I just opened a stream to the GoodBuilders Season 3 distribution pool on Flow State.

Join me in supporting these public goods builders at https://t.co/wzMlBTSdxg

GoodBuilders Season 3 is here!🌱

$50k+ in G$ rewards. Streaming funds with real-time feedback. Mentorship & community. 💸🤝

We sat down w/ Rael & @HadarRot of @gooddollarorg to explore S3 and what builders need to know to get involved! 🎙️

🎧Listen: https://t.co/QgPlP9Y5xB

We discuss:

💬 The power of dynamic funding based on real-time community feedback

💰 Why crypto is such a valuable tool for scalable Universal Basic Income (UBI)

✨ How to get involved as a builder, mentor, or community member

💡 Some standout projects in the ecosystem, and use cases they are excited to see in Season 3

@sfrantzman The problem has nothing to do with what "everyday people" want. It's the Arab culture of not taking accountability, victimhood and silencing any dissenting voices. So there's actually no voice to these everyday people you claim to exist. Let's hear them and we'll have peace!

Unlike other cryptos where liquidity is gone during downturns causing a run, the G$ reserve model ensures every g$ is always liquid. That's why we can create money to fund the commons while being "stable enough"™️ to drive real economic activity and not speculation.

Imagine an incredibly resilient rail network, which allows for cross-border movement of cargo carriages. Imagine too that it is resistant to any forms of disruption. Finally, imagine that it is not controlled by any single party

Now ask yourself whether these features - resilience, disruption-resistance, and decentralization - tell you anything about the carriages themselves? Are the carriages somehow given ‘value’ through the fact that they run upon such an infrastructure?

A core claim of the Bitcoin community is precisely that. They often argue that the resilient, distributed and ‘censorship-resistant’ nature of the Bitcoin infrastructure - the ‘rails’ as it were - somehow imparts ‘value’ onto the tokens that are moved around upon it. It is akin to arguing that the movability, or unstoppability, of a carriage is the thing that ends up loading a ‘cargo’ onto it

This argument is, at best, highly dubious

If you start with a valuable cargo, it is true that having a resilient and censorship-resistant network to move it around upon is very useful. But the logic does not work the other way around - i.e. merely having a resilient, censorship-resistant network does not somehow create valuable cargo

GoodBuilders Season 3 applications are LIVE✨

🌊 $50,000+ in G$ streaming funding on @flowstatecoop@Celo

🧠Mentorship + real community & users

👉 Apply now: https://t.co/x5KAe6dnTt

@nirhasson@nw41807640322 מז"א, ברור. כל אחד אחראי לבחירות שלו.

האם אנחנו בוכים לחמאס? או מסתכלים לתוכנ�� כיצד הגענו למצב של 7 באוקטובר?.

זה ההבדל בין היהודים לערבים, היכולת לקחת אחריות ולא להיות קורבן חסר יכולת.

A bitcoin maximalist completely baffled with the accelerating money printing under Milei.

Maybe it is about time you realize you don't understand how money works.

I explained it here

https://t.co/oA88zqhLNv

Javier Milei One Year Assessment

Everyone excited about an Argentina economic miracle is basing it on all sorts of government statistics except the most important statistics: money supply measures and public debt growth.

Under its new supposedly free-market Rothbardian president, Argentina's money supply in 2024 has increased at these astonishing rates:

M0: 209%

M1: 133%

M2: 93%

M3: 123%

To put these numbers in perspective, note that they dwarf the rates during the preceding years, during which Argentina thoroughly earned its reputation as one of the most dysfunctional fiat monetary basket cases in the world.

In the four years of 2020-2023, Argentina’s money supply measures grew at a compound annual growth rate of:

M0: 50%

M1: 77%

M2: 90%

M3: 86%

In Milei’s first six months in office, public debt grew from $370 billion to $442 billion, a staggering increase of 19.4%. Borrowing $72 billion in 6 months can make any economic statistics look good, but the problem of course is in the long-term consequences. It is possible to make short-term growth, poverty, unemployment, or inflation numbers look good by printing and borrowing money, thus transferring the cost of a short-term glow up to the future, where they are paid with exorbitant interest. Those of us who thought things could not possibly get worse might need to reconsider.

Remember that in his election campaign, Milei specifically campaigned on a platform of abolishing the central bank, even saying that that was non-negotiable. Yet as soon as he went into office, all such talk was ignored, and replaced with elaborate stories about how shutting down the central bank would be very politically unpopular. In this, Milei has fully adopted the same statist rhetoric that is always used to justify inflation by governments: the short-term pain of stopping inflation would be so bad, that it's better to continue down the path of inflation and ignore the long-term consequences. The reality is that the Argentine central bank is bankrupt, and the sooner this reality is acknowledged, the quicker it can be overcome. Trying to save the central bank can only be done by piling up debt obligations that will make the future problems even worse. In this, Milei is no different from all his predecessors who sought short-term relief at the expense of the future.

Milei has also refused to default on the public debt, which would have been the Rothbardian solution to finally free his countrymen from eternal debt slavery to pay for the consumption binges of their previous presidents. A default on foreign debt, and a shuttering of the central bank would have caused a few months of painful adjustment, after which the Argentine economy would recover on a solid footing, without even the possibility of a government being able to create inflation or saddle the population with debt. Foreign currency and bitcoin would likely dominate such an economy, and the state would necessarily be limited by the fact that it cannot print money.

By not shutting down the central bank and letting it ramp up its money printing, Milei is sowing the seeds for currency crises in Argentina’s future. By not defaulting and hiring the same bankers who brought calamity to the country in the previous administrations, it seems Milei is eager to get another IMF bailout, which will saddle Argentinians with generational debt slavery and more fiscal crises in the future. Unsurprisingly, he is raising taxes significantly, illustrating that his understanding of Austrian economics is no deeper than the regurgitation of cliches on TV. To increase taxes in order to facilitate more government borrowing is a crime against the people of Argentina to benefit the international banking cartels and the IMF criminals. It is a tyrannical recipe advanced by the Keynesians at the IMF, and has no relation whatsoever to what any real economist worth his salt would advocate.

A lot has been made about Milei reducing the budget deficit, but this is not that important. Argentina’s problem was not that it had a big budget deficit, as its budget deficit has usually been pretty low, under 4% of GDP, the same range as European countries with no major inflation and fiscal problems. The problems have always been in money supply increase and in public debt, both of which have accelerated under Milei in an unprecedented way.

The cherry on top is that Milei has shipped off the little remaining gold Argentina has to London, in search of some yield. Pawning off a politically neutral monetary asset free of counterparty risk in search of a few quick bucks does not inspire confidence. In his book The Ascent of Money, historian Niall Ferguson details how Argentina’s economic problems began when president General Juan Domingo Peron visited the central bank in 1946 and was astonished at how much gold was sitting there. Argentina had more than 1,000 tons of gold at that time, and Peron and his successors would not resist the temptation to finance their spending by running down the gold reserves that should have been backing the people’s money. The past 8 decades of calamity were the predictable consequence. After billions of percentage points in inflation and countless defaults, Argentina’s gold reserves today are no more than 61 tons. By shipping off the last monetary reserve of the future in exchange for a quick buck to allow him to keep paying off debt so he can get another IMF loan, Milei has completed Peron’s inflationary legacy to its logical end. Argentina now has no money of its own, only an ever-growing pile of liabilities from foreign banks replete with political and economic risks. Rothbard must be turning in his grave every time this Peronist invokes him to justify his actions.

This data is astonishing and flies in the face of the hype. But unless someone can show me why this data is wrong, then, for all of his libertarian and free market rhetoric, Milei is a vintage Latin American populist inflationist, buying short-term popularity with long-term inflation and debt, essentially no different from every Argentine leader since Peron. All that his free market rhetoric seems to have achieved is to trick poor Argentines into trusting their broken central bank again instead of trying to find a working alternative like Bitcoin. His anti-socialist rhetoric is nice to listen to, and his hysterical antics, relentless emotional crying, and triumphant theatrics may be amusing to some, but fate usually serves its cruelest dishes to those who celebrate before victory.

@saifedean Lol. Maybe it is time you realize you austrians dont understand money. Most "Money printing" is not done by the govt/central bank but by the private sector borrowing from banks. Inflation decreased yet m0 is 3x! Follow @ProfSteveKeen to get educated