With SpaceX getting priced at $135 today, Bloomberg estimates Musk's net worth is now $970.5B

Tomorrow, any pop above the IPO price (or a Tesla rally) could make him the first Trillionaire!

Spacex is one of those, remember who said what. Anyone defending the valuation or talking about it bullishly who is an institutional/professional investor is either an idiot or a shill it's that simple (looking at Gavin Baker as an example...)

I think there are two AI problems building, and the data/stories around them have been growing the last few weeks.

1. AI costs are outstripping utility at a lot of enterprise at least for now until it's figured out.

2. Datacenter buildout is facing limitations of speed and so these bottlenecks arent as bad.

But we're in the front side of an exuberant rally (nobody can tell me MRVL today was logical). And in markets price creates narrative. However given positioning price can flip and the key point is that now we have narratives if people want to shift their focus that would raise doubts and create fuel for a correction. Nobody is debating whether earnings are strong, the issue is earnings are now being priced out years, that becomes more about sentiment as nobody can accurately forecast 3-5 years out, especially with historically disruptive technology.

I think there are two AI problems building, and the data/stories around them have been growing the last few weeks.

1. AI costs are outstripping utility at a lot of enterprise at least for now until it's figured out.

2. Datacenter buildout is facing limitations of speed and so these bottlenecks arent as bad.

But we're in the front side of an exuberant rally (nobody can tell me MRVL today was logical). And in markets price creates narrative. However given positioning price can flip and the key point is that now we have narratives if people want to shift their focus that would raise doubts and create fuel for a correction. Nobody is debating whether earnings are strong, the issue is earnings are now being priced out years, that becomes more about sentiment as nobody can accurately forecast 3-5 years out, especially with historically disruptive technology.

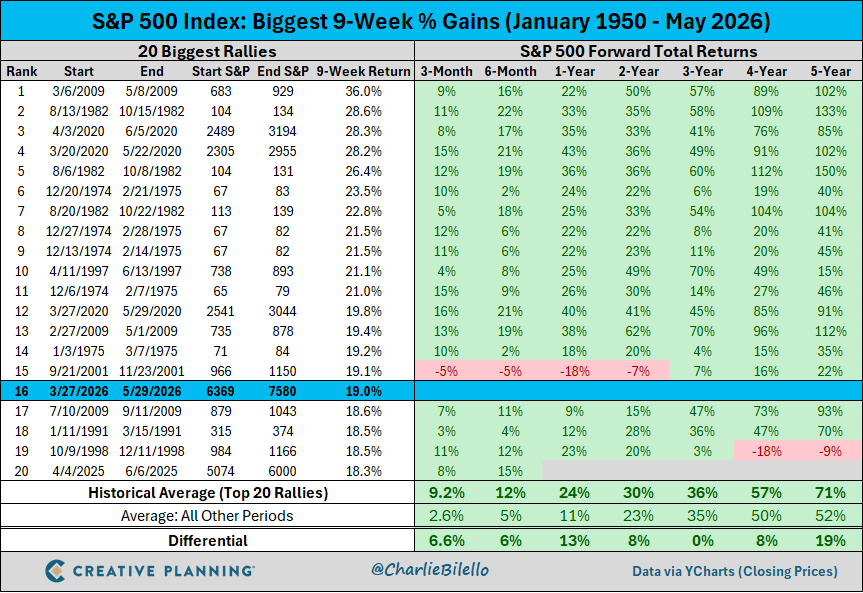

Misleading conclusions if you look at the forward returns. Only 97/98 were not major corrections/bear markets (and those were still more substantial crisis and vix spike corrections than march)

@P_Remarks I dont think many people actually believe this will happen though, it's a price go up gamma squeeze (now lacking weekly options). Just an excuse for people to chase momentum. This isnt an unknown name in retail (this isnt ZM vs ZOOM)

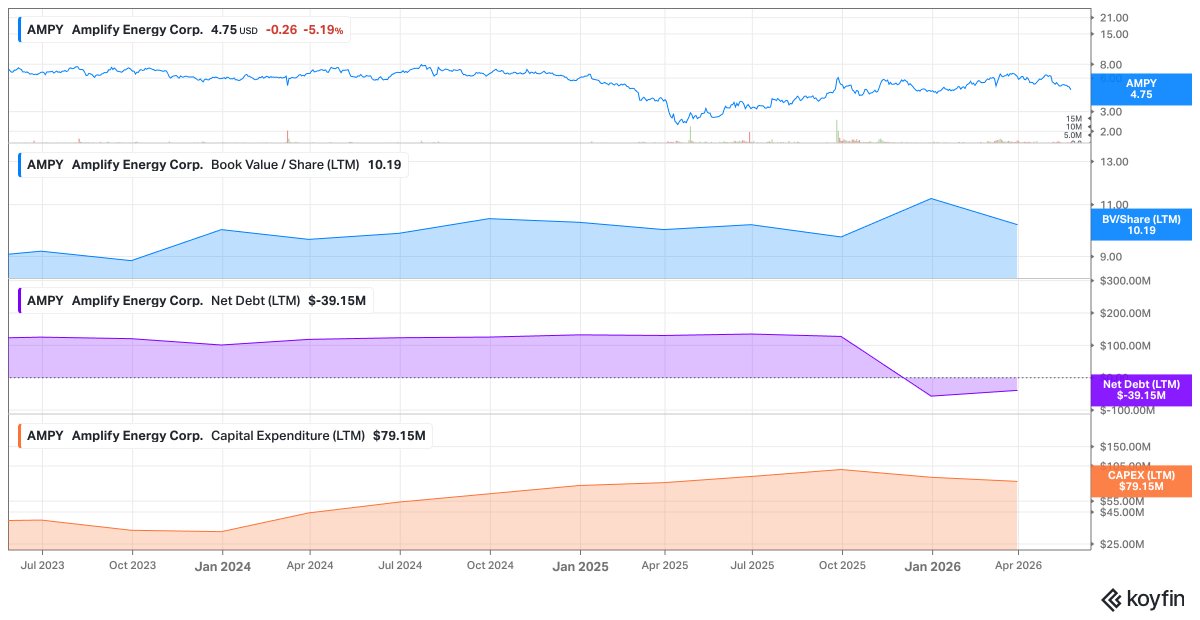

The $AMPY drilling program at beta so far has been on the lower end of the cone of probablities, however we knew that this was possible. They made a conscious decision to not spend 25m on new seismic on a 50 year old field. Better to find out drilling as you go and get a return on the wells. Drill bit just bad luck, the process will win out even if it would have been nice for it to hit more upfront and with the spike in oil prices. At 4.60 though you are not paying for anything to go well, the cash flow and clean financials are coming next, and capital return is the next step. Very interesting things coming here for those with patience. I also believe it is down here because a big holder sold 3M shares after buying in q4, thats 7.5% of the float more of the free trading in a very thin name wihtout much of a bid given lack of good oil upside right now nobody wants to own a low torque oil name. But the point is the price is reflecting flows not fundamentals. I get why it's a show me stock after years of lacking progress (mostly though with the prior management). But thats the opportunity.

I realized my ticker isnt in the timeline tagging here $AMPY. Happy to answer any dm's if anyone has any questions. This is one of the most asymmetric opportunities I've seen in my career. Nobody knows or cares, but the cash flow coming is unstoppable barring a Beta black swan.

I think the bear replies are annualizing the wrong quarter.

Q1 looked ugly: $3.8M EBITDA / -$18M FCF. But 2026 guidance is 6.7–7.9k bopd, $20–45M EBITDA and $45–65M capex. That is clearly a build year, not normalized earnings.

Production should ramp through the year as Beta wells come online. Royalty relief started May 1 and adds 600+ net bopd / $1M+ monthly revenue. New barrels also dilute the hedge book, so incremental production should be much more exposed to current oil prices.

If $AMPY exits 2026 with a higher oil base and capex drops to maintenance levels in 2027, I think this can do $40–50M FCF next year. With the balance sheet now debt-free, the historical reason they could not return capital is gone. If execution is even decent, capital return should follow.

This is new AMPY: new management, new board, directors actually owning stock, same too-cheap assets. Bairoil already has ~$10M/year LOE savings and free CCUS / power optionality that the market is valuing at basically zero.

There were specific reasons Q1 production and EBITDA were low that should reverse or improve in Q2/Q3. Those will be the first cleaner quarters for the new structure. By the time it is obvious, the stock likely will not be here.

At ~$4.50–5, I think downside is limited absent real execution failure/black swan tail risk at Beta, while upside to $7–10+ is very plausible. Frustrating name in this market, but extremely asymmetric if there are still investors willing to look past one ugly transition quarter. This is not really an oil bet, it's about cash flow and rerating through shareholder returns. Either the market will figure it out or the stock will be forced higher as it is being run like a private company now.

for me it wasnt even about the degree we were up, it was the sequencing and lack of almost any days that closed subtantially lower on the close than open (with big gaps at critical inlfections when there were any selloffs). Hardest period in my career as a largely dedicated junk/penny stock short seller

I think the bear replies are annualizing the wrong quarter.

Q1 looked ugly: $3.8M EBITDA / -$18M FCF. But 2026 guidance is 6.7–7.9k bopd, $20–45M EBITDA and $45–65M capex. That is clearly a build year, not normalized earnings.

Production should ramp through the year as Beta wells come online. Royalty relief started May 1 and adds 600+ net bopd / $1M+ monthly revenue. New barrels also dilute the hedge book, so incremental production should be much more exposed to current oil prices.

If $AMPY exits 2026 with a higher oil base and capex drops to maintenance levels in 2027, I think this can do $40–50M FCF next year. With the balance sheet now debt-free, the historical reason they could not return capital is gone. If execution is even decent, capital return should follow.

This is new AMPY: new management, new board, directors actually owning stock, same too-cheap assets. Bairoil already has ~$10M/year LOE savings and free CCUS / power optionality that the market is valuing at basically zero.

There were specific reasons Q1 production and EBITDA were low that should reverse or improve in Q2/Q3. Those will be the first cleaner quarters for the new structure. By the time it is obvious, the stock likely will not be here.

At ~$4.50–5, I think downside is limited absent real execution failure/black swan tail risk at Beta, while upside to $7–10+ is very plausible. Frustrating name in this market, but extremely asymmetric if there are still investors willing to look past one ugly transition quarter. This is not really an oil bet, it's about cash flow and rerating through shareholder returns. Either the market will figure it out or the stock will be forced higher as it is being run like a private company now.

Anyone following $AMPY?

To summarize the last 12 months at this small-cap E&P...

1) Terminated merger

2) CEO replaced

3) Sold assets

4) Now have a net cash balance sheet,

5) Doubling down on remaining 2 assets (capex)

6) Trades at ~0.4x book value

I think the bear replies are annualizing the wrong quarter.

Q1 looked ugly: $3.8M EBITDA / -$18M FCF. But 2026 guidance is 6.7–7.9k bopd, $20–45M EBITDA and $45–65M capex. That is clearly a build year, not normalized earnings.

Production should ramp through the year as Beta wells come online. Royalty relief started May 1 and adds 600+ net bopd / $1M+ monthly revenue. New barrels also dilute the hedge book, so incremental production should be much more exposed to current oil prices.

If $AMPY exits 2026 with a higher oil base and capex drops to maintenance levels in 2027, I think this can do $40–50M FCF next year. With the balance sheet now debt-free, the historical reason they could not return capital is gone. If execution is even decent, capital return should follow.

This is new AMPY: new management, new board, directors actually owning stock, same too-cheap assets. Bairoil already has ~$10M/year LOE savings and free CCUS / power optionality that the market is valuing at basically zero.

There were specific reasons Q1 production and EBITDA were low that should reverse or improve in Q2/Q3. Those will be the first cleaner quarters for the new structure. By the time it is obvious, the stock likely will not be here.

At ~$4.50–5, I think downside is limited absent real execution failure/black swan tail risk at Beta, while upside to $7–10+ is very plausible. Frustrating name in this market, but extremely asymmetric if there are still investors willing to look past one ugly transition quarter. This is not really an oil bet, it's about cash flow and rerating through shareholder returns. Either the market will figure it out or the stock will be forced higher as it is being run like a private company now.

Added a bit of $sei.v at 43 cents.

Instead of CA$500k, the President and CEO invested US$500k (50/50) at 41 cents during the raise

There are many catalysts coming up.

In the next 6 months, there are likely 2-4 wells drilled and 1-2 farmouts. + Uruguay opening well + increasing interest in Namibia, which we are seeing + $100 oil, which at the moment doesn't seem to matter to Sintana until it does.

Many scenarios for 2-3x the stock price in the mid-term. The shareholder base is just sick of the stock at the moment, but the market has a short memory. We don't need much for the sentiment shift.

#SEI $SEI.V @sintanaenergy Good from Malcy. Sums up why they raised, the fabulous asssets which are now either carried or funded. The work programme and news flow is as good as it gets. Simple question, will the SP be higher or lower in 6,12 and 18 months time?

"This fundraise, which has raised some $11.5m at 22.5p, a 13.5% discount has been significantly supported by new and existing shareholders and was, I understand, heavily oversubscribed. Indeed the company had the opportunity to raise more but felt that this amount, being totally sufficient to fully fund all the company’s demands over the next two years, is the correct call.

Sintana has important projects in a number of geographies and this raise will mean that, as requested by shareholders, and fully supported here, there is a long term visibility across each and every one of them is funded for any possible call on partners.

Starting in Namibia and with PEL 90, where operator Chevron has kicked off its programme with indications that the Nabba-1X exploration well will be drilled in 4Q 2026 and will be a net cost of c.$6-8m to Sintana. Given that this is about the only block in the substantial portfolio where Sintana are not carried it is wise to not go into that phase of the programme in a weak position.

Elsewhere in Namibia Sintana has progressed well on the acquisition of PEL 37 and the deal which will be funded 50/50 cash and equity is expected to sign before long. The block, in the Walvis basin is adjacent to Sintana’s block PEL 82 and notable as BP has recently farmed-in and where Chevron is anticipating drilling next year.

As for PEL 83 which contains the huge Mopane discovery where Total have farmed-in, looks to be becoming very active and with rigs to be hired and where the market thinks that a FID might come as soon as 2028. Total are also moving swiftly to FID at Venus, thought to be planned for as soon as this summer and will generate yet more interest as it will be the first Namibian discovery to be brought onstream.

Elsewhere Sintana are close to completing at KON-16, onshore Angola and drilling is likely after the extensive seismic programme is analysed later this year.

And in Uruguay there is a great deal happening, in OFF-1 the 3D the early seismic results are expected in 4Q 26 with final data in 2Q 27. Over at OFF-3 there is a great deal of interest, whilst the farm-out process continues I would suggest that with nearby activity discussions have changed somewhat. With activity in both OFF-2 and Off-7 which sandwich the block seeig farm-in activity and Qatar Energy, Shell and Chevron involved there must be more interesting conversations going on.

So, as a result of this raise the cash pile which was $8.2m, to be added to by the $6m due from Exxon this year will be further topped up, leading shareholders will be delighted that there is enough in the coffers for two years under pretty much any circumstances.

Add to that all the potential from the portfolio and others nearby will significantly add to the excitement, so anyway you slice and dice the exposure that Sintana has should be massively beneficial. My target price remains at 75p and the Bucket List is better for its inclusion."

Elon Musk just put an expiration date on the medical profession.

And he gave it three years.

The interviewer asked when Optimus would be a better surgeon than the best surgeons on Earth.

Musk didn’t hesitate.

Musk: “Three years. I’d say three years at scale.”

Not a prototype. Not a lab experiment. At scale.

To understand why that timeline is plausible, you have to understand the fundamental problem with human medicine.

Musk: “Takes a super long time to learn to be a good doctor. And even then, the knowledge is constantly evolving. It’s hard to keep up with everything.”

Musk: “Doctors have limited time. They make mistakes. How many great surgeons are there? Not that many.”

That is the brutal reality of the greatest healthcare system humanity has ever built.

It runs on exhausted humans with biological limits, trained over decades, who can only operate on one patient at a time.

Optimus has none of those constraints.

It doesn’t get tired.

It doesn’t forget a study published last week.

It doesn’t have an off day. It doesn’t have a caseload limit.

And once you train one, you can manufacture ten thousand more with identical precision.

Musk: “At that point, there will probably be more Optimus robots that are great surgeons than there are on Earth.”

Think about what that actually means.

The scarcity of elite surgical skill has been one of the defining limits of human healthcare since the beginning of medicine.

Geography determined your odds of survival.

Zip code determined your access to expertise.

That bottleneck disappears overnight.

Because you can’t train human surgeons fast enough to meet global demand.

But you can manufacture infinite robots running identical perfect code.

The most valuable skill in the world is about to become software.

Infinitely replicable. Infinitely scalable. Available to every human being on Earth regardless of where they were born.

Medical scarcity doesn’t fade gradually under that reality.

It ends.

And whoever controls that code controls healthcare access for billions.

For all of human history, the leading cause of preventable death wasn’t disease.

It was the shortage of great people to fight it.

That problem has a solution now.

And it ships in three years.