Top Tweets for #Divgi

#Divgi Torqtransfer Systems Ltd

Very soon we can see in 4 digits

#Divgi Torqtransfer Systems Ltd

जब Price बढ़े और Volume भी बढ़े, तो इसे आमतौर पर Bullish Confirmation माना जाता है।

मतलब:

शेयर में खरीदार (Buyers) मजबूत हैं।

बड़ी मात्रा में खरीदारी हो रही है।

Price की तेजी को Volume support कर रहा है।

Trend आगे भी जारी रहने की संभावना बढ़ जाती है।

📈 Price ↑ + Volume ↑ = Strong Bullish Signal

उदाहरण:

शेयर ₹100 से ₹110 गया और Volume 5 लाख से बढ़कर 15 लाख हो गया।

इसका मतलब है कि केवल Price नहीं बढ़ा, बल्कि बहुत से लोग खरीद भी रहे हैं।

Technical Analysis में सबसे मजबूत संकेतों में से एक:

✅ Breakout + High Volume = Breakout के सफल होने की संभावना अधिक।

लेकिन ध्यान रखें:

यदि Price बहुत तेजी से बढ़ चुका हो और Volume अचानक असामान्य रूप से बहुत ज्यादा हो जाए, तो कभी-कभी यह Profit Booking या Climax Top का संकेत भी हो सकता है।

इसलिए हमेशा:

👉 Price Action + Volume + Trend तीनों को साथ में देखें।

#Divgi #DivgiTTS

Divgi-TTS is a structural play on three converging tailwinds in Indian auto — the SUV boom, EV transition, and "China+1" export reshoring. High-Precision Mechanics is the foundation across all three, while Embedded Hardware & Software is the extra weapon that specifically unlocks the EV opportunity and Divgi's move toward electronic Shift-on-the-Fly (ESOF) transfer cases for premium SUV trims. That combination is why an old-school gear company from the 1960s is now both India's dominant 4WD supplier and Tata's transmission partner for EVs.

What does it do

In the early 1960s, the Divgi family started out doing high-precision gear engineering. Nothing flashy. Just gears.

Then in 1995, they entered a 20-year joint venture with BorgWarner — one of the biggest drivetrain companies in the world. For two decades, Divgi sat inside BorgWarner's engineering playbook: friction material bonding, electron-beam welding, synchronizer design. The kind of manufacturing know-how that takes most companies generations to build organically.

When the JV ended in 2016, most companies would've gone back to being a contract manufacturer. Divgi did something different — they became a co-development partner.

Here's what that means: when Mahindra designs a Thar, or Tata builds a new EV, they don't go shopping for an off-the-shelf gearbox. Divgi's engineers are in the room at the concept stage — customizing, prototyping, testing the mechanism that gets power from the engine (or battery) to the wheels. That's "co-architect," not "vendor."

Moat

Divgi controls roughly 70-75% of India's 4WD/AWD transfer case market — currently the highest-margin, fastest-growing of its three segments (35-38% category CAGR). They're the only homegrown maker of interactive torque couplers. Gross margins run 60-63% — versus ~56% for Sona BLW and ~45-50% for traditional forging companies.

Why such fat margins for an "auto parts" company? Because the real product isn't the metal — it's the 3-5 year OEM qualification process baked into every platform. Once Divgi is validated on a vehicle program, switching suppliers costs the OEM ₹50-100 crore and 12-18 months of line shutdown. Nobody does that lightly. The margin gap over Sona BLW likely comes down to product mix: Divgi sells fully integrated, software-calibrated systems where it's often the only qualified domestic source, while Sona's portfolio leans more toward individual EV components in a more competitive field.

Underneath that lock-in sits a genuine technological edge. The 20-year BorgWarner JV left Divgi with proprietary process trade secrets and patents — not just product designs, but the manufacturing know-how and electronic software calibration needed to build integrated Shift-on-the-Fly transfer cases. That IP protects the process, which is far harder to reverse-engineer than a part.

This is also why the barrier to entry is so high — and it's not about money. Setting up a high-precision drivetrain plant costs ₹250-500 crore, which plenty of players can raise. The real wall is the 3-5 year, non-transferable OEM qualification cycle per platform. A great example: Ramkrishna Forgings has successfully scaled into component exports, but has never managed to break into the system-level 4WD transfer case market — they lack the ECU calibration capability and the multi-year co-development track record that OEMs like Mahindra demand. Capital alone can't buy that; only time and trust can.

The honest segment picture: synchronizer systems (the legacy, ICE-linked manual gearbox business) remains Divgi's largest revenue base today, but it's the structurally narrowing piece — BEVs use single-speed gearboxes, eliminating synchronizers entirely. EV/E-Gear is still small in absolute revenue but is where current RFQ momentum and future growth concentrate. Divgi is already a certified E-Gear supplier to Tata Motors, with a 120-kW EV transmission program hitting Start of Production. Narrow moat, but widening, not shrinking.

Valuation

FY26: revenue jumped 61% to ₹352.89 crore, profit grew 92% to ₹46.93 crore. They're sitting on a ₹380cr order book plus a freshly-won ₹800cr, 7-year global export contract for transfer cases — split between Mahindra's Scorpio pickup and Tata's Yodha platform, shipping out through Southeast Asia.

FY28E (20% CAGR model): revenue ₹508cr, EBITDA margin 27.6%, EPS ₹25.81, ROIC scaling from 14% to 19.4%.

The upside case — four catalysts that could compound together:

1. Export contract front-loads. Base case assumes slow ramp from H2FY27. Faster overseas platform adoption could mean skipping the "sample batch" phase and going straight to full-line shipments, filling Shirwal's spare capacity sooner.

2. Mix shifts toward "smart" hardware. Faster adoption of ESOF transfer cases and 120-kW EV modules (mechanics + Divgi-owned software) carries >65% gross margins vs standard parts — a structural margin lift, not just cyclical.

3. The 150,000-unit domestic RFQ converts. Tooling for these manual components is already fully depreciated at Sirsi/Shivare — near-zero incremental cost, almost pure profit if won.

4. Temporary input-cost windfall. Raw material pass-through clauses lag 3-6 months; softer steel/aluminum prices would let Divgi pocket the spread temporarily.

Stack all four: FY28E revenue could stretch toward ₹600-650cr (vs ₹508cr base), margins toward 29-30%, EPS toward ₹34-36 (vs ₹25.81 base) — a 35-40% EPS upside layered on an already-doubling earnings base.

Management

Run by the Divgi brothers — Jitendra (MD, UCSD-trained mechanical engineer, 30+ years in transmission design) and Hirendra (manufacturing, vendor development, shop floor automation). Promoter family holds ~60.5%, zero pledge. Through facility buildouts at Shirwal, EV ramp-ups, and export wins, they've stayed virtually debt-free. Engineers running the show — clean governance, no RPT red flags, board 50%+ independent.

Execution credibility check: management's export turnaround guidance (₹80-90cr annual run-rate) has played out as promised through FY26.

Watch items:

Top customer = 50%+ of revenue, top 5 = 90%+. Management's biggest job is diversification.

₹800cr export contract's H2FY27 SOP is management's own guidance — any client-side delay leaves Shirwal capacity underutilized.

IPO fund deployment for Shirwal extended into FY27 (Feb 2026) — framed as prudent validation-first, but worth watching for repeat pattern.

Closing

The biggest swing factor isn't the export contract or RFQ — it's drivetrain architecture. If single-motor EVs dominate (Divgi's mechanical transfer case carries over via E-Gear), Divgi's leadership extends into the EV era. If dual/quad-motor setups win (software coordinates independent axle motors, no physical transfer case needed), Divgi's core mechanical segment gets bypassed.

Worth contrasting with pure-play automotive software names like KPIT — KPIT posted FY26 revenue of $724.8 million with a 20.8% EBITDA margin, but FY26 was volatile for them, with PAT margins compressing from ~14% to ~11% YoY in Q3 as OEMs delayed software-defined-vehicle programs. KPIT owns the calibration/software layer but no hardware — if architecture shifts toward software-coordinated multi-motor EVs, KPIT-type players are direct beneficiaries, while Divgi's hardware-heavy model would need its software arm to carry more weight. Autocar ProfessionalMarkets Mojo

For now: a small gear shop absorbed two decades of BorgWarner's drivetrain DNA, built India's dominant 4WD systems business, and rides three tailwinds — SUVs for volume today, China+1 for exports today, EV for relevance tomorrow. The KPIT contrast is a useful lens for the one risk that matters most: whether Divgi's hardware-first model keeps pace if the industry's center of gravity shifts further toward software.

[Not investment advice, DYOR]

![ramesh_vd's tweet photo. #Divgi #DivgiTTS

Divgi-TTS is a structural play on three converging tailwinds in Indian auto — the SUV boom, EV transition, and "China+1" export reshoring. High-Precision Mechanics is the foundation across all three, while Embedded Hardware & Software is the extra weapon that specifically unlocks the EV opportunity and Divgi's move toward electronic Shift-on-the-Fly (ESOF) transfer cases for premium SUV trims. That combination is why an old-school gear company from the 1960s is now both India's dominant 4WD supplier and Tata's transmission partner for EVs.

What does it do

In the early 1960s, the Divgi family started out doing high-precision gear engineering. Nothing flashy. Just gears.

Then in 1995, they entered a 20-year joint venture with BorgWarner — one of the biggest drivetrain companies in the world. For two decades, Divgi sat inside BorgWarner's engineering playbook: friction material bonding, electron-beam welding, synchronizer design. The kind of manufacturing know-how that takes most companies generations to build organically.

When the JV ended in 2016, most companies would've gone back to being a contract manufacturer. Divgi did something different — they became a co-development partner.

Here's what that means: when Mahindra designs a Thar, or Tata builds a new EV, they don't go shopping for an off-the-shelf gearbox. Divgi's engineers are in the room at the concept stage — customizing, prototyping, testing the mechanism that gets power from the engine (or battery) to the wheels. That's "co-architect," not "vendor."

Moat

Divgi controls roughly 70-75% of India's 4WD/AWD transfer case market — currently the highest-margin, fastest-growing of its three segments (35-38% category CAGR). They're the only homegrown maker of interactive torque couplers. Gross margins run 60-63% — versus ~56% for Sona BLW and ~45-50% for traditional forging companies.

Why such fat margins for an "auto parts" company? Because the real product isn't the metal — it's the 3-5 year OEM qualification process baked into every platform. Once Divgi is validated on a vehicle program, switching suppliers costs the OEM ₹50-100 crore and 12-18 months of line shutdown. Nobody does that lightly. The margin gap over Sona BLW likely comes down to product mix: Divgi sells fully integrated, software-calibrated systems where it's often the only qualified domestic source, while Sona's portfolio leans more toward individual EV components in a more competitive field.

Underneath that lock-in sits a genuine technological edge. The 20-year BorgWarner JV left Divgi with proprietary process trade secrets and patents — not just product designs, but the manufacturing know-how and electronic software calibration needed to build integrated Shift-on-the-Fly transfer cases. That IP protects the process, which is far harder to reverse-engineer than a part.

This is also why the barrier to entry is so high — and it's not about money. Setting up a high-precision drivetrain plant costs ₹250-500 crore, which plenty of players can raise. The real wall is the 3-5 year, non-transferable OEM qualification cycle per platform. A great example: Ramkrishna Forgings has successfully scaled into component exports, but has never managed to break into the system-level 4WD transfer case market — they lack the ECU calibration capability and the multi-year co-development track record that OEMs like Mahindra demand. Capital alone can't buy that; only time and trust can.

The honest segment picture: synchronizer systems (the legacy, ICE-linked manual gearbox business) remains Divgi's largest revenue base today, but it's the structurally narrowing piece — BEVs use single-speed gearboxes, eliminating synchronizers entirely. EV/E-Gear is still small in absolute revenue but is where current RFQ momentum and future growth concentrate. Divgi is already a certified E-Gear supplier to Tata Motors, with a 120-kW EV transmission program hitting Start of Production. Narrow moat, but widening, not shrinking.

Valuation

FY26: revenue jumped 61% to ₹352.89 crore, profit grew 92% to ₹46.93 crore. They're sitting on a ₹380cr order book plus a freshly-won ₹800cr, 7-year global export contract for transfer cases — split between Mahindra's Scorpio pickup and Tata's Yodha platform, shipping out through Southeast Asia.

FY28E (20% CAGR model): revenue ₹508cr, EBITDA margin 27.6%, EPS ₹25.81, ROIC scaling from 14% to 19.4%.

The upside case — four catalysts that could compound together:

1. Export contract front-loads. Base case assumes slow ramp from H2FY27. Faster overseas platform adoption could mean skipping the "sample batch" phase and going straight to full-line shipments, filling Shirwal's spare capacity sooner.

2. Mix shifts toward "smart" hardware. Faster adoption of ESOF transfer cases and 120-kW EV modules (mechanics + Divgi-owned software) carries >65% gross margins vs standard parts — a structural margin lift, not just cyclical.

3. The 150,000-unit domestic RFQ converts. Tooling for these manual components is already fully depreciated at Sirsi/Shivare — near-zero incremental cost, almost pure profit if won.

4. Temporary input-cost windfall. Raw material pass-through clauses lag 3-6 months; softer steel/aluminum prices would let Divgi pocket the spread temporarily.

Stack all four: FY28E revenue could stretch toward ₹600-650cr (vs ₹508cr base), margins toward 29-30%, EPS toward ₹34-36 (vs ₹25.81 base) — a 35-40% EPS upside layered on an already-doubling earnings base.

Management

Run by the Divgi brothers — Jitendra (MD, UCSD-trained mechanical engineer, 30+ years in transmission design) and Hirendra (manufacturing, vendor development, shop floor automation). Promoter family holds ~60.5%, zero pledge. Through facility buildouts at Shirwal, EV ramp-ups, and export wins, they've stayed virtually debt-free. Engineers running the show — clean governance, no RPT red flags, board 50%+ independent.

Execution credibility check: management's export turnaround guidance (₹80-90cr annual run-rate) has played out as promised through FY26.

Watch items:

Top customer = 50%+ of revenue, top 5 = 90%+. Management's biggest job is diversification.

₹800cr export contract's H2FY27 SOP is management's own guidance — any client-side delay leaves Shirwal capacity underutilized.

IPO fund deployment for Shirwal extended into FY27 (Feb 2026) — framed as prudent validation-first, but worth watching for repeat pattern.

Closing

The biggest swing factor isn't the export contract or RFQ — it's drivetrain architecture. If single-motor EVs dominate (Divgi's mechanical transfer case carries over via E-Gear), Divgi's leadership extends into the EV era. If dual/quad-motor setups win (software coordinates independent axle motors, no physical transfer case needed), Divgi's core mechanical segment gets bypassed.

Worth contrasting with pure-play automotive software names like KPIT — KPIT posted FY26 revenue of $724.8 million with a 20.8% EBITDA margin, but FY26 was volatile for them, with PAT margins compressing from ~14% to ~11% YoY in Q3 as OEMs delayed software-defined-vehicle programs. KPIT owns the calibration/software layer but no hardware — if architecture shifts toward software-coordinated multi-motor EVs, KPIT-type players are direct beneficiaries, while Divgi's hardware-heavy model would need its software arm to carry more weight. Autocar ProfessionalMarkets Mojo

For now: a small gear shop absorbed two decades of BorgWarner's drivetrain DNA, built India's dominant 4WD systems business, and rides three tailwinds — SUVs for volume today, China+1 for exports today, EV for relevance tomorrow. The KPIT contrast is a useful lens for the one risk that matters most: whether Divgi's hardware-first model keeps pace if the industry's center of gravity shifts further toward software.

[Not investment advice, DYOR]](https://pbs.twimg.com/media/HK1CrhTbIAAnF7n.png)

#Divgi Torqtransfer Systems Ltd

जब Price बढ़े और Volume भी बढ़े, तो इसे आमतौर पर Bullish Confirmation माना जाता है।

मतलब:

शेयर में खरीदार (Buyers) मजबूत हैं।

बड़ी मात्रा में खरीदारी हो रही है।

Price की तेजी को Volume support कर रहा है।

Trend आगे भी जारी रहने की संभावना बढ़ जाती है।

📈 Price ↑ + Volume ↑ = Strong Bullish Signal

उदाहरण:

शेयर ₹100 से ₹110 गया और Volume 5 लाख से बढ़कर 15 लाख हो गया।

इसका मतलब है कि केवल Price नहीं बढ़ा, बल्कि बहुत से लोग खरीद भी रहे हैं।

Technical Analysis में सबसे मजबूत संकेतों में से एक:

✅ Breakout + High Volume = Breakout के सफल होने की संभावना अधिक।

लेकिन ध्यान रखें:

यदि Price बहुत तेजी से बढ़ चुका हो और Volume अचानक असामान्य रूप से बहुत ज्यादा हो जाए, तो कभी-कभी यह Profit Booking या Climax Top का संकेत भी हो सकता है।

इसलिए हमेशा:

👉 Price Action + Volume + Trend तीनों को साथ में देखें।

#Divgi Torqtransfer Systems Ltd

Very good result

#Divgi “Next orbit of growth” — management commentary is strong 🚀

But charts are now starting to confirm the story 👇

• Multi-month resistance zone around 780–820 being tested

• Price reclaiming 20 & 50 EMA → trend shift signs

• Strong bullish candle with volume expansion

• RSI moving above 60 → momentum improving

Automatic transmission theme = future growth driver

Price action = market starting to price that in

A clean breakout + sustain above 820 can open room for higher levels.

For now → Story + Structure aligning 👀

#StocksToWatch #AutoAncillary #BreakoutStocks #TechnicalAnalysis

#DIVGI TORQTRANSFER SYSTEMS

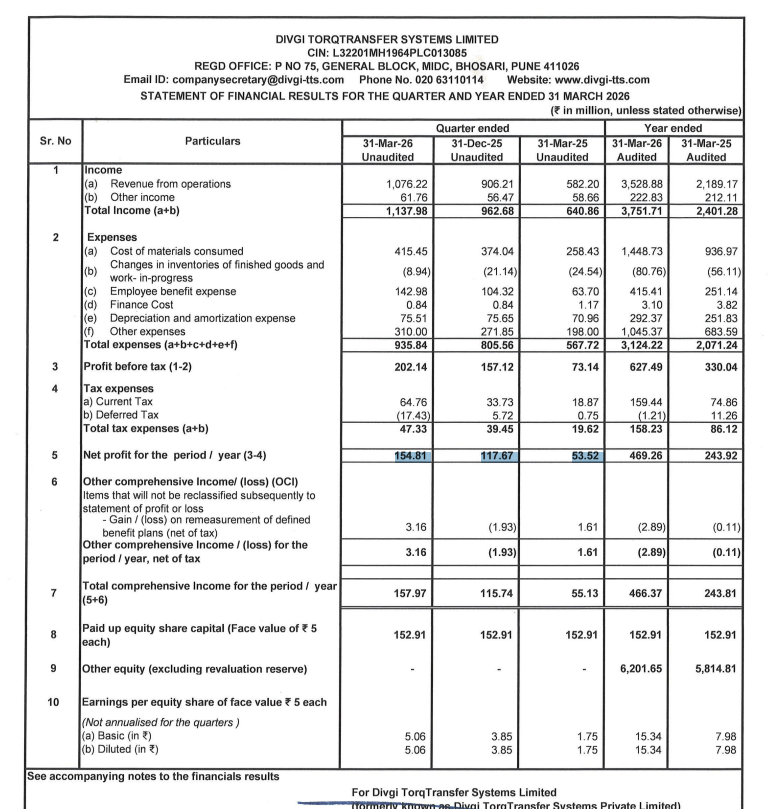

✅ Q4 Net Profit jumps to ₹15.5 Cr vs ₹5.4 Cr YoY

✅ Q4 Revenue rises sharply to ₹100 Cr vs ₹58.2 Cr YoY

✅ Q4 EBITDA surges to ₹21.6 Cr vs ₹8.6 Cr YoY

✅ EBITDA Margin expands to 20.1% vs 14.75% Yoy

#stockmarket

Divgi Torqtransfer Systems Limited Q4FY26 Results:-

#Q4Results #Q4FY26 #Stockmarket #Nifty #Divgi

Revenue 107.62 Cr vs 58.22 Cr

(+84.85% YoY┃+18.76% QoQ)

EBITDA 21.67 Cr vs 8.66 Cr

(+150.24% YoY ┃+22.35% QoQ)

EBITDA Margin 20.14% vs 14.88% YoY & 19.55% QoQ

PBT 20.21 Cr vs 7.31 Cr

(+176.37% YoY┃+28.65% QoQ)

PAT 15.48 Cr vs 5.35 Cr

(+189.26% YoY┃+31.56% QoQ)

Other Income 6.18 Cr vs 5.87 Cr YoY & 5.65 Cr QoQ

👏👏

#Divgi Torqtransfer Systems Ltd

Keep Eyes 👀

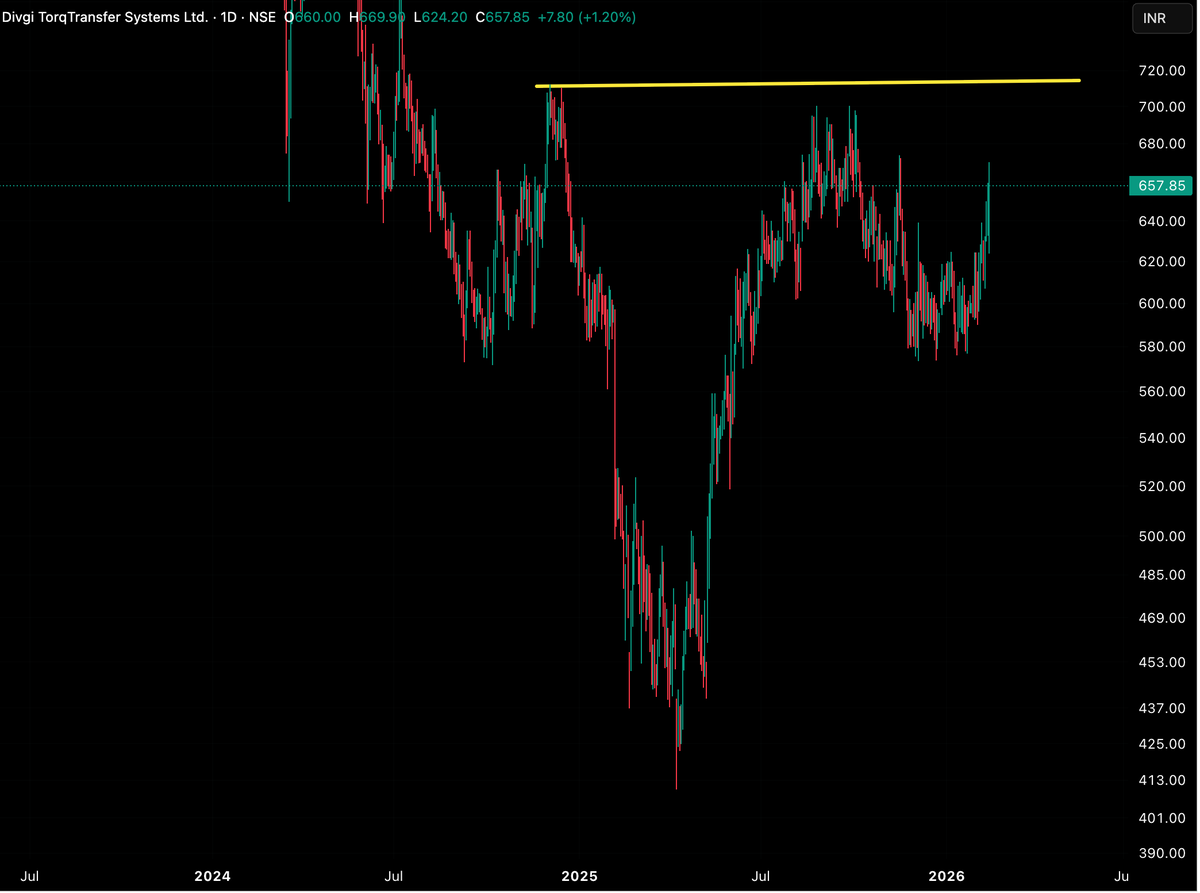

#Divgi Torqtransfer Systems Ltd

Sector :- Auto Ancillaries

Market Cap :- 2108 Cr

Debt / Eq :- 0

➡️ Nearby resistant 200DEMA (~705)

#KatoraPattern

#Divgi 📈

TorqTransfer horha

#Divgi TorQ

Kisne maal uthaya ?

#Divgi Torqtransfer Systems price volume breakout from inverse H&S pattern,support 700-690

~Volume up 20x

~India’s largest EV Transmission manufacturer

~Debt free

~Earnings turnaround after 4-5 quarters of lull,Free Cash flow

Divgi TorqTransfer Systems

#Divgi

ROI > 77% from lows 🔥

Finally the laggard takes off ..patience is what retail needed but fund managers held it through and through ..

SageOne Fund

🔸 Sageone Investment Advisors

🔸 Sageone Investment Managers

Note:

a. Goodluck India tanked till 567/sh down 8% from their buying price but still went up by 77% in a matter of few months!

b. Praveg, Shankara and Kirloskar Oil has not given much returns yet where one can study..

c. Divgi Torqtransfer Systems is trading very close to their buying price and recent 3050847 shares of public issue was done at 585/sh.

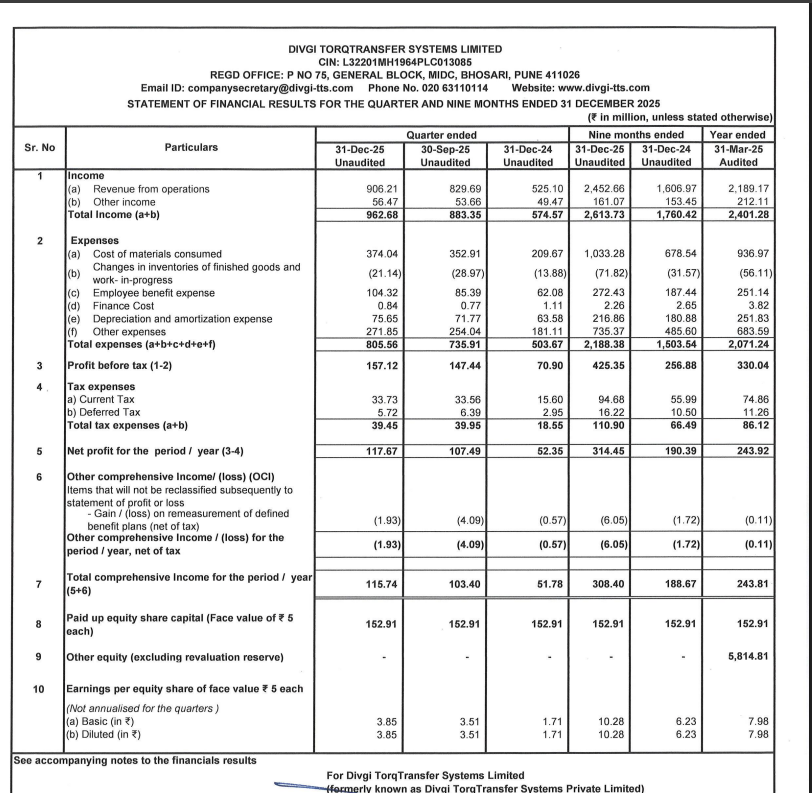

Divgi Torqtransfer Systems Limited Q3 FY26 Results:-

#Q3Results #Q3FY26 #Stockmarket #Nifty #divgi

Revenue 90.62 Cr vs 52.51 Cr

(+72.58% YoY┃+9.22% QoQ)

PBT 15.71 Cr vs 7.09 Cr

(+121.61% YoY┃+6.57% QoQ)

PAT 11.77 Cr vs 5.24 Cr

(+124.78% YoY┃+9.47% QoQ)

👏👏

Divgi Torqtransfer Systems Ltd | Q2 FY26 Results ⚙️

#Q2Results #Q2FY26 #StockMarket #Nifty #Divgi

✅ Revenue: ₹830 M vs ₹540 M (+53.70% YoY)

✅ EBITDA: ₹166 M vs ₹113 M (+46.02% YoY)

✅ EBITDA Margin: 19.98% vs 21.02% YoY

✅ Net Profit: ₹108 M vs ₹78 M (+38.46% YoY)

🗣️ Management Update: Strong YoY growth in revenue and PAT driven by higher order execution; slight dip in EBITDA margin reflects increased raw material costs.

#AutomotiveComponents #Earnings #Results #Q2Update

Last Seen Hashtags on Sotwe

Most Popular Users

Elon Musk

@elonmusk

240.4M followers

Barack Obama

@barackobama

119.3M followers

Donald J. Trump

@realdonaldtrump

111.7M followers

Cristiano Ronaldo

@cristiano

110.1M followers

Narendra Modi

@narendramodi

107M followers

Rihanna

@rihanna

97.5M followers

NASA

@nasa

92.1M followers

Justin Bieber

@justinbieber

90.8M followers

KATY PERRY

@katyperry

87.4M followers

Taylor Swift

@taylorswift13

81.2M followers

Lady Gaga

@ladygaga

72.8M followers

Kim Kardashian

@kimkardashian

69.7M followers

Virat Kohli

@imvkohli

69.5M followers

YouTube

@youtube

68.7M followers

Bill Gates

@billgates

63.7M followers

The Ellen Show

@theellenshow

62.5M followers

Neymar Jr

@neymarjr

62.2M followers

CNN

@cnn

61.9M followers

X

@x

60.8M followers

Selena Gomez

@selenagomez

60.5M followers