Top Tweets for #InX

1ヶ月振りの夜活は弟夫婦と

ホームへ

ビーテスとサビアエヴォで

カサゴ10、メバル1

雨が降る前の1時間だけの短時間釣行だったけど楽しい釣りだった😆

納竿前に弟にエヴォ貸したら

感度に感動してたw

ムラソイ釣って喜んでた😏

#INX.label

#BeeTesller

#SABIAevolucion

#INX/USDT

🟢 Direction: short

📌 Entry 0.008030

Targets..

Target TP1: 0.007810

Target TP2: 0.007563

Target TP3: 0.007205

⛔️ SL: 0.008615

RISK MANAGEMENT IS KEY

Join our telegram community.

Click below ⬇️https://t.co/gUuvmXD1Aj

Short #INX

Entry 0.008030

Tp 0.007810

Join our telegram community.

Click below ⬇️https://t.co/gUuvmXD1Aj

Short #INX

Entry 0.008030

Tp 0.007810

Join our telegram community.

Click below ⬇️

https://t.co/c9OvHW52NW

📌 A Statement on INX Token Holder Rights, Disclosure, and Trust

Hi I'm FLIP

Before sharing an important and positive update about Korea’s security token market, I believe one unresolved issue must be addressed with clarity and seriousness.

For several years, I have helped organize STO SUMMIT, Korea’s dedicated Security Token and RWA event, together with Edaily.

This year, at the request of the Korean government, the Financial Services Commission, and Korea Exchange, we are preparing the STO sector program within Korea Premium Week, in a format similar in spirit to Japan Week.

Korea is entering a critical phase. Token securities legislation is expected to move into full implementation next year, and the Korean capital market is attracting unprecedented global attention.

For years, I have analyzed security token regulations, market structures, global case studies, and companies that could shape the future of Korea’s tokenized securities market.

INX has been one of the most important cases I have followed, because it was issued through an SEC-registered public offering and has been widely regarded as a reference case for regulated security tokens.

I am writing this as a market analyst who has studied INX deeply, and as someone who has worked to help Korea’s tokenized securities market develop and connect with the global market.

However, before celebrating Korea’s next chapter, one issue must be addressed.

That issue is:

⚖️ INX Token holder rights.

I believe INX Token holders have not yet received sufficient clarity.

In particular, INX Token holders in Korea, Japan, and globally now need clear, official, and legally grounded communication.

INX Token is not a simple utility token.

It was issued through an SEC-registered public offering as a blockchain security token. The rights of INX Token holders are described in the INX Prospectus / White Paper and SEC filings.

The INX Prospectus states:

“Each INX Token … will entitle its holder to receive pro rata distributions of 40% of the Company’s cumulative net cash flow from operating activities, excluding any cash proceeds from an initial sale by the Company of an INX Token (‘Adjusted Operating Cash Flow’).”

This means INX Token holders have a contractual right to receive pro rata distributions of 40% of INX Limited’s cumulative Adjusted Operating Cash Flow, or AOCF.

The Prospectus also states:

“The distribution to INX Token holders is a contractual obligation of the Company and a right of each INX Token holder…”

This is not merely a marketing statement.

It is described in the SEC-registered offering document as a contractual obligation of the Company.

The Prospectus also states:

“The pro rata distribution … is not self-executing and requires that our board of directors approve the Company’s financial statements and calculate such distribution in good faith.”

But this does not mean the Company has unlimited discretion to neutralize INX Token holder rights.

The key phrase is:

⚖️ good faith

INX Token holders have a legitimate right to ask:

1. How is AOCF being calculated?

2. Are INX revenues and costs being allocated fairly?

3. After the Republic acquisition, has the economic value of INX been shifted to another entity or structure?

4. Are revenues generated through INX’s ATS, broker-dealer, and secondary trading infrastructure properly reflected in INX Limited’s AOCF?

5. Are INX Token holder rights being preserved not only formally, but also substantively?

The INX Prospectus also contains a very important protection:

“The Company may not amend or modify the INX Token Purchase Agreement in a manner that would materially impair the rights of the INX Tokens without the express consent of INX Token Holders.”

And further:

“Any amendment or modification which would have the effect of materially and adversely amending or modifying the rights of the INX Tokens would need to be agreed to by each holder of INX Tokens.”

In other words, the rights of INX Token holders cannot be materially and adversely modified without holder consent.

After Republic’s acquisition of INX, these rights did not disappear.

INX’s 2026 Form 20-F states that INX Token was delisted from https://t.co/mSL4agjB3Z on February 15, 2026, but also clearly states:

“All existing INX Token rights remain unchanged.”

This sentence matters.

⚖️ Delisting is not the same as extinguishing holder rights.

INX itself disclosed to the SEC that all existing INX Token rights remain unchanged.

There is also another critical issue:

📄 Disclosure obligations.

INX Limited issued INX Token through an SEC-registered public offering and has filed reports with the SEC through Form 20-F and Form 6-K.

The fact that Republic is a private company should not mean that material information directly related to INX Token holder rights can disappear without explanation.

I am not saying Republic must disclose all of its private-company financials.

But if INX Limited remains subject to SEC reporting obligations, and if INX Token is a security token issued through an SEC-registered offering with a 40% AOCF participation right, then the following matters require clear disclosure or official explanation:

1. The current status of INX Token rights

2. The methodology for calculating AOCF

3. Revenue attribution between INX Limited and Republic

4. Whether revenues from INX’s ATS, broker-dealer, and regulated secondary trading infrastructure are attributed to INX Limited or its subsidiaries

5. Whether such revenues are reflected in AOCF

6. Cost allocation and intercompany arrangements between Republic and INX

7. The status of any INX Token buyback or Republic Note exchange

8. How Republic and INX will ensure that “All existing INX Token rights remain unchanged” is respected in substance

In particular, if INX’s regulated secondary trading infrastructure is central to Republic’s future strategy, then the revenues, costs, and AOCF treatment of that infrastructure should be disclosed or officially explained in a way that INX Token holders can understand and verify.

AOCF rights are not abstract rights.

They depend directly on operating cash flow, revenue attribution, cost allocation, and intercompany arrangements.

If Republic uses INX’s broker-dealer license, ATS, INX.One-related infrastructure, or secondary trading infrastructure to grow its business, holders deserve clarity on where the economic value is attributed, what costs are allocated to INX, and how those amounts affect AOCF.

This is not curiosity.

It is a basic request from holders of a security token issued under an SEC-registered offering.

Also, if an INX Token buyback or Republic Note exchange is actually pursued, it may involve a securities repurchase or exchange transaction. Under U.S. securities law, if an issuer or affiliate conducts a tender offer or exchange offer for an equity security, Rule 13e-4 and Schedule TO may become relevant.

This is no longer merely a community-management issue.

It is an issue of:

⚖️ security token rights

📄 disclosure

📊 AOCF

🏛️ regulated secondary market infrastructure

🤝 investor trust

Republic’s CEO has publicly explained that secondary trading infrastructure is the future of Republic. He also emphasized the significant value of that market and infrastructure.

Then the question becomes unavoidable:

If one of the core values of acquiring INX was its regulated secondary trading infrastructure, ATS, broker-dealer license, and INX.One-related infrastructure, how does the economic value generated from that infrastructure relate to INX Token holders’ AOCF rights?

INX Token holders do not have voting rights.

But INX Token is not just a coin. It was designed as a security token with contractual economic participation rights in INX’s operating cash flow.

This structure is closer to a contractual revenue-participation security than a typical utility token.

INX Token holders are not asking for control of the company.

They are asking how the rights clearly described in the Prospectus and SEC filings are being preserved in practice.

If Republic acquired INX because it sees regulated secondary market infrastructure as a key part of its future, and if Republic intends to use that infrastructure within its broader ecosystem, then Republic should clearly address the questions INX Token holders now have.

Republic and its executives also communicated that there would be follow-up measures for INX Token holders after delisting. It was also explained that INX Token would remain separate from Republic Note.

Based on public communications, holders understood that:

- Trading functionality may be integrated into https://t.co/5szsp5bMCP

- INX Token was delisted, and follow-up measures for holders were expected

- INX Token would remain separate from Republic Note

- Additional updates for INX Token holders could come within one to two weeks

That update was expected around early April.

However, INX Token holders have still not received a clear official update, timeline, terms, or action.

Republic’s February 2026 Form 6-K states:

“Republic continues to consider and intend to provide INX Token holders with an opportunity to participate in a voluntary repurchase or exchange offer…”

But it also states:

“No repurchase or exchange offer is being effectuated at this time.”

This is exactly why clarity is needed now.

If Republic is preparing an INX Token buyback or Republic Note exchange, holders deserve to know the expected timeline, terms, eligibility, legal process, and current status.

If Republic has decided not to proceed, holders deserve to know that as well.

I respectfully request Republic to clarify:

1. The current rights of INX Token holders

2. The status of any INX Token buyback or Republic Note exchange

3. Why the previously discussed holder update has been delayed

4. How INX Limited’s SEC reporting obligations will continue after the acquisition

5. How INX and Republic will disclose or officially explain INX Token rights, AOCF, secondary trading revenues, cost allocation, and intercompany arrangements

6. The role of INX’s ATS, broker-dealer, and secondary trading infrastructure in Republic’s future strategy

7. How that economic value connects to INX Token holders’ AOCF rights

8. The revenue allocation, cost allocation, and intercompany structure between INX Limited and Republic

9. Whether Republic and INX will provide distinguishable disclosure or explanation regarding secondary trading infrastructure accounting and AOCF treatment

10. The methodology for AOCF calculation and future disclosure

11. How Republic will ensure that “All existing INX Token rights remain unchanged” is respected not only in form, but also in substance

I am not writing this to attack Republic.

On the contrary, I believe Republic can become a major global infrastructure company in RWA and tokenized securities.

That is precisely why this issue must be clarified now.

If trust is lost, everything is lost.

The tokenized securities market cannot be built on technology alone.

It must be built on disclosure, legal rights, investor protection, contractual performance, and trust.

I have studied INX and other global security token cases from the early stage of Korea’s tokenized securities market, and I have worked to help Korea connect with the global market.

That is why I see this not merely as an issue of one token, but as an issue connected to the credibility of the entire tokenized securities market.

If Republic provides a clear and convincing explanation to INX Token holders and commits to maintaining transparent disclosure regarding INX Token rights and AOCF, I am willing to actively support Republic’s expansion in Korea’s token securities and RWA market through my network and role in the Korean ecosystem.

Korea’s market is about to open.

And I can help Republic become a trusted global player in Korea’s tokenized securities market.

But the condition is clear:

⚖️ Do not lose the trust of INX Token holders.

INX Token holders in Korea, Japan, and around the world are not asking for special treatment.

They are asking for clarity and transparent disclosure based on the White Paper and SEC filings.

If Republic wants to be trusted as a global RWA and tokenized securities infrastructure company, what is needed now is not silence, but:

📄 clear explanation

🕰️ official timeline

📊 continued disclosure

⚖️ respect for holder rights

🤝 protection of trust

INX Token holders deserve clarity. Republic should protect trust. Tokenized securities must be built on disclosure, investor rights, and trust — not uncertainty.

Korea Premium Week

STO SUMMIT Co-Host

FILP

@joinrepublic

@INX_Group

@KendrickEsq

@sdatika1

@republicnote

#INX #INXToken #Republic #RepublicNote #SecurityTokens #TokenizedSecurities #RWA #Tokenization #DigitalAssets #CapitalMarkets #SEC #ATS #BrokerDealer #InvestorRights #Disclosure #AOCF #STOSummit #KoreaPremiumWeek #Korea #Japan #TokenSecurities #FLIP

@HANA_REV_WEB3 @Securitize ありがとうございます、いえいえとても勉強になります🙏しかしセキュラタイズは未だ日本人取引できないんですよね😅昔 #INX で少しだけ購入したBCAP、SCI2が冬眠状態となってます😅

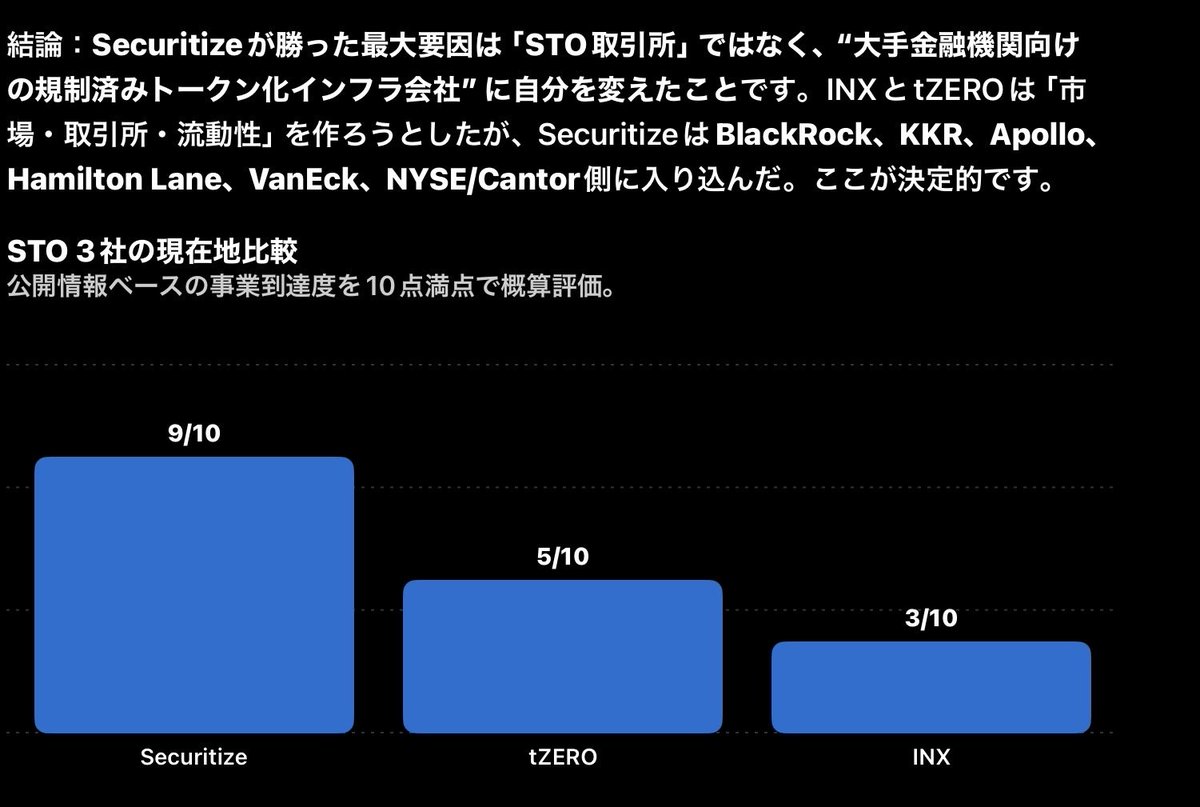

#INX 社 #Securitize 社、#TZERO 社、はSTO会社として同時期に立ち上がり同規模で企業活動して来たが、現在はセキュラタイズが市場シェア含め成功している。過去4年間の3社の活動を調査分析して、現在の企業価値になった要因や原因を教えて

ーーーーーーーチャッピー回答ーー

1. 現在の企業価値の差

Securitize

2026年7月1日にCantor Equity Partners IIとの統合完了を発表し、2026年7月2日からNYSEで SECZ として取引開始予定。発表では「オンチェーン化した資産4Bドル超」とされ、2025年のSPAC発表時点で評価額は12.5億ドル。

INX

2025年11月10日にRepublicがINXを約6,000万ドルで買収。2024年の取引・トランザクション手数料は約40万ドル、営業損失は約1,330万ドル。Q2 2025でも取引手数料は5.2万ドル、営業損失は420万ドル。つまり規制面では先行したが、収益化・流動性で伸びなかった。

tZERO

tZEROはATS、ブローカーディーラー、デジタル証券カストディなど規制インフラを持ち、2024年にデジタル証券カストディ承認、2025年に社債取引のFINRA承認、2025年末に取引時間拡大を進めた。ただしSecuritizeほど大手資産運用会社の主幹プラットフォームにはなれていない。

2. 4年間で起きた本質的な差

Securitize:B2B金融インフラに絞った

Securitizeは、個人投資家向けSTO取引所というより、大手資産運用会社がトークン化商品を出すための裏方インフラになった。2022年にKKR、2024年にBlackRockのBUIDL、さらにApollo、Hamilton Lane、VanEckなどと組み、2024年にはBlackRock主導で4,700万ドルを調達した。

ここが強い。

STO市場は「個人が謎の未上場トークンを買う市場」では伸びず、BlackRockのMMF、米国債、ファンド、上場株、ETF、社債の効率化として伸びた。

INX:規制では勝ったが、商品市場適合で負けた

INXはSEC登録済みINX Tokenという歴史的成果があった。2020年にSECがF-1を有効化し、SEC登録デジタル証券IPOを実現した点は本当に先駆的。

ただし、その後の問題はこれ。

「合法である」ことと「市場が使う」ことは別。

INXは規制面の正しさを証明したが、取引高・上場銘柄・機関投資家採用・手数料収益が弱かった。2024年の取引手数料40万ドル、2025年Q2の5.2万ドルという数字は、取引所ビジネスとしてはかなり小さい。

tZERO:技術と規制インフラは強いが、親会社色と再編で鈍かった

tZEROは早期からATSを持ち、技術・特許・規制インフラでは強かった。公式サイトでもデジタル証券取引・発行額、50M株超の取引、複数のSEC登録を掲げている。

ただしOverstock/Medici系の文脈が強く、暗号バブル・ICO期の印象も残った。2023年以降は再編し、2024〜2026年にカストディ、社債、取引時間延長、Nomyx連携などを進めているが、SecuritizeのようなBlackRock級の看板商品を持てなかった。

3. なぜSecuritizeだけ企業価値が跳ねたか

一番の理由はこれ。

Securitizeは「STO会社」から「金融機関のオンチェーン資本市場OS」へ変わった。

Stripeは「決済する会社」ではなく、ネット企業の決済インフラになった。

Coinbaseは「仮想通貨販売所」から、カストディ・上場・機関向けインフラになった。

Palantirは「分析ツール」ではなく、政府・大企業の意思決定インフラになった。

Securitizeも同じで、個人向けSTO販売ではなく、BlackRockやNYSEが使う制度対応インフラになった。

4. 成否を分けた6要因

① 顧客選定

Securitize:BlackRock、KKR、Apollo、Hamilton Lane、VanEck、NYSE。

INX:個人・暗号投資家・小型STO寄り。

tZERO:発行体・ATS中心だが、大手金融商品の主戦場化が遅い。

② 収益の質

SecuritizeはAUM型・発行体向け・管理インフラ型。

INX/tZEROは取引所型なので、流動性がないと収益が出ない。

③ 信用の獲得順序

Securitizeは「大手金融機関の信用」を先に取った。

INXは「規制の正しさ」を先に取った。

tZEROは「技術とATS」を先に取った。

市場が一番高く評価したのは、大手金融機関の信用だった。

④ 商品選定

勝ち筋は未上場STOではなく、米国債・MMF・ファンド・株式・ETFだった。BlackRock BUIDLはその象徴。

⑤ 規制地域展開

Securitizeは米国に加え、EUでもCNMV承認を取り、Avalanche上で欧州の取引・決済システムを進めている。

⑥ 上場ストーリー

Securitizeは「トークン化会社が自社株もトークン化して上場」という物語を作った。これは投資家に非常に分かりやすい。

5見立て

INXは正しすぎたが、早すぎた。

tZEROは技術と市場インフラはあったが、主役商品を取れなかっ

Securitizeは制度・大手金融・商品・資本市場のタイミングが噛み合った。

一言で言うと、

INXは「規制済みSTO取引所」を作った。

tZEROは「デジタル証券ATS」を作った。

Securitizeは「BlackRock時代のトークン化資本市場インフラ」になった。

$INX 8h 💰 - #INX is currently in wave B of a ABC pattern, which looks like a triangle, and is in the final part of it, and is also near the 200MA, so keep an eye out, wave C could be up. 📈

$INX 8h 💰 - #INX is currently in wave B of a ABC pattern, which looks like a triangle, and is in the final part of it, and is also near the 200MA, so keep an eye out, wave C could be up. 📈

🔗 https://t.co/HBbKoOBgUB

Most Popular Users

Elon Musk

@elonmusk

240.7M followers

Barack Obama

@barackobama

119.2M followers

Donald J. Trump

@realdonaldtrump

111.7M followers

Cristiano Ronaldo

@cristiano

110.9M followers

Narendra Modi

@narendramodi

107M followers

Rihanna

@rihanna

97.7M followers

NASA

@nasa

92.2M followers

Justin Bieber

@justinbieber

91M followers

KATY PERRY

@katyperry

87.8M followers

Taylor Swift

@taylorswift13

81.7M followers

Lady Gaga

@ladygaga

73.2M followers

Virat Kohli

@imvkohli

70.2M followers

Kim Kardashian

@kimkardashian

69.9M followers

YouTube

@youtube

68.7M followers

Bill Gates

@billgates

64M followers

Neymar Jr

@neymarjr

62.9M followers

The Ellen Show

@theellenshow

62.4M followers

CNN

@cnn

61.9M followers

Selena Gomez

@selenagomez

60.9M followers

X

@x

60.8M followers