Top Tweets for #VisionInfra

#SME #VIESL #VisionInfra #VisionInfraEquipmentSolutions

Vision Infra Equipment Solutions H2 FY26 Earnings Call Highlights

👉 FY27 & Future Outlook:

▫️Revenue growth target ~25–30% Y-o-Y in FY27 with corresponding EBITDA margin (conservative guidance).

💠3-year ambition: Double revenue — fully achievable on infrastructure demand, equipment strength, execution capability and deep client relationships.

💠PAT margin expected to settle at ~12–13% (H2 FY26: 13.29%; full-year conservative view factoring seasonality; SLM depreciation now fully aligned).

💠Focus areas: fleet scaling, higher asset utilisation, operational efficiencies (ERP fully live), new verticals (mining), and debt reduction via strong cash flows + OEM credit terms.

👉 Current Order Book / Projects and Future Pipeline:

▫️Rental services order book (Mar 2026): ~₹250 crore (short-term, continuously renewable; not a one-time lump-sum visibility).

💠Pipeline of inquiries and discussions; management sees “no issue” in growth visibility despite fleet expansion from 425 → 545 machines.

💠Key executed / ongoing projects:

- Noida International Airport, Navi Mumbai Airport

- Ganga Expressway

- Reliance Jamnagar & Nagothane

- Somnath Highway 120 km overlay (captive end-to-end model)

💠Client base: L&T, Tata Projects, IRB, Kalpataru Group, Sam India, Megha Engineering + leading EPC players.

💠New growth avenues:

- Integrated asphalt & concrete paving + piling rigs (now operational)

- Mining vertical entry (iron-ore crushing & screening + Caterpillar tippers); first orders expected in coming quarter; rental-only model (direct to mine operators/contractors).

👉 Other Notable Points:

▫️ Cash flow from operations ~6x to ₹195 cr; Debtor days improved 16 days (120 → 104)

💠Gross block ₹603 cr (vs ₹419 cr); Net worth ₹263 cr (vs ₹165 cr); D/E improved 1.62x → 1.36x

💠Depreciation policy changed (WDV → SLM effective Oct 2025) to better match rental revenue pattern; one-time bottom-line impact ~₹20 cr already absorbed.

▫️Fleet & Operations: 545 machines (rental) + 200+ ancillary equipment (vs 425 + 150 last year); PAN-India presence in 24 states; >450 in-house professionals + 1,500+ deployed manpower

▫️Key Strategic Moves:

💠ERP implementation completed (efficiency & visibility boost)

💠Preferential warrants ₹134 cr raised (25% received in Q4 FY26)

💠Advisory board strengthened (Arun Savanur, Debashish Sarkar, Jay Singh Valunj)

▫️Q&A Highlights:

💠Other current liabilities jump (₹41 cr → ₹192 cr) explained as capital creditors (~₹120 cr) on extended OEM credit terms (360–720 days) for new fleet — not short-term borrowings; will be funded largely by internal accruals → debt-equity to improve further.

💠Refurbishment exports (Mexico/South America ~40%, Europe 30%, Australia balance): no impact from duties; margins stable (±1–2%).

💠FY27 Capex guidance: ₹100–150 cr.

💠Maharashtra / state infra payments: comfortable on MSRDC & ADB-funded projects (smooth cash flows, niche paver advantage).

Vision Infra Equipment Solutions (SME) H2FY26 Results:-

#H2FY26 #Stockmarket #Nifty #Visioninfra

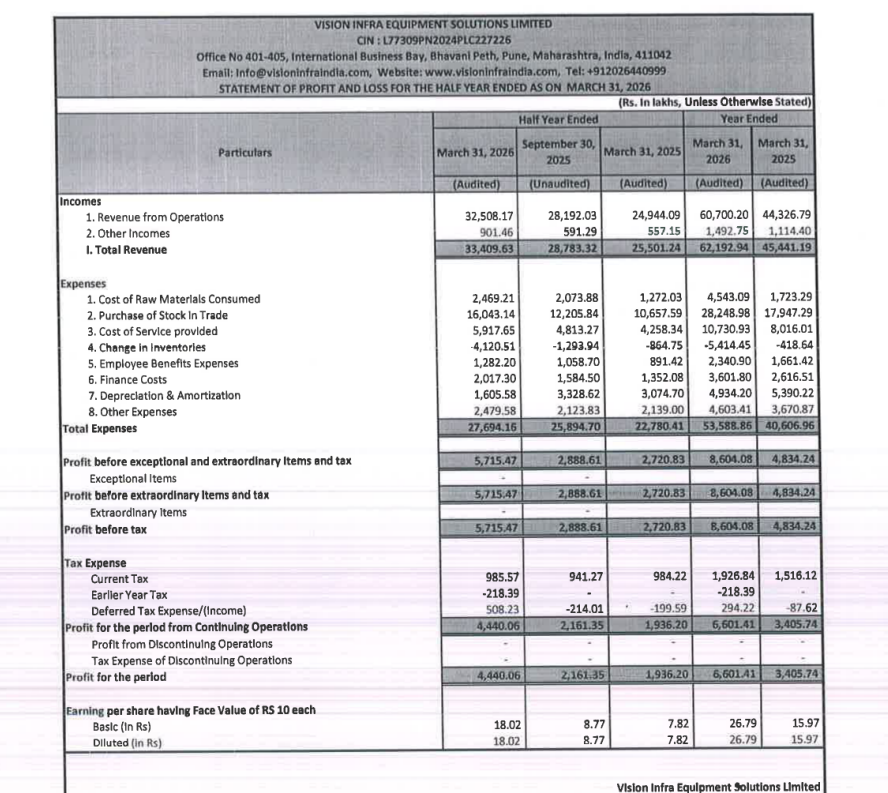

Revenue 325.08 Cr vs 249.44 Cr

(+30.32% YoY┃-12.38% QoQ)

EBITDA 84.37 Cr vs 65.90 Cr

(+28.02% YoY ┃+11.90% QoQ)

EBITDA Margin 25.95% vs 26.42% YoY & 20.32% QoQ

PBT 57.15 Cr vs 27.21 Cr

(+110.06% YoY┃-12.76% QoQ)

PAT 44.40 Cr vs 19.36 Cr

(+129.32% YoY┃+5.35% QoQ)

Other Income 9.01 Cr vs 5.57 Cr YoY & 1.97 Cr QoQ

#visioninfra Vision Infra Equipment Solutions Ltd - Super Duper results- UC loading tomorrow

#visioninfra

vision infra- i recommended this co at 160. now the result is awaited on monday. if i use the promoter's concall and the historical ratios, the h2 no should be 360 cr sth and profit for whole year should touch 50 cr.

this means that co is valued at 18 times PE.

now for future growth the co has acquired funds of 180 cr with promoters themselves investing 120 cr. with this infusion, even with a 50% growth in PAT to 75 cr in FY27, the co will be at forward PE of 12 so another 2-3x story from current levels.

New all time high.

#Viesl

Should be a bumper results.

Revenue should be 600cr+

53cr raised post IPO through pref, mukul mahavir agarwal participated along with promoters.

#visioninfra

63. Vision Infra Equipment lTd 🔖 Solutions Ltd

🔸Promoter Holding Increase (Sep) ~.02 %

🔸 Promoter Holding ~70.26%

🔸Sales Growth ~ 45.40 %

🔸Profit Growth ~47.01 %

🔸P/E ~ 15.8

#visioninfra #StocksToBuy #stockmarketsindia #StocksToWatch #OptionsTrading

#VISIONINFRA breakout and retest ... Check out my #VIESL analysis on @TradingView: https://t.co/jryIRx1oBq

#SME #VIESL #VisionInfra #VisionInfraEquipment

Vision Infra Equipment Solutions H1 FY26 Concall Highlights:

👉FY 2026 & Future Outlook :

▫️FY26 expected revenue ~₹550cr+

▫️EBITDA margins are expected to marginally improve

💠Expectation is 26–27%+ EBITDA margin for full FY26

💠PAT margin expected to remain stable to slightly higher

👉Order book / projects and pipeline:

▫️Current order book : ~215cr+ (pure rental; mostly executable in FY26)

💠₹25 Cr of this is specifically from the concrete paver segment; 26 concrete paver units currently

💠Good visibility in road maintenance, concrete road texturing, overlay works, end-to-end milling & crushing solutions

💠Order book pipeline will be maintained/growth continues, no slowdown visible at ground level, daily enquiries

👉 Others :

▫️Fleet Size & Age: 442 equipments

💠~85% of the fleet is less than 3 years old → young and efficient fleet (synergy with refurbishment vertical keeps fleet young)

▫️Refurbishment & Trading Vertical: Contributes 50%+ of revenue (sometimes higher)

💠80–85% is export (Europe 20–25%, Middle East + Africa 25%, South America 30–40%, Australia/NZ etc.)

💠No seasonality in refurbishment

💠Margins slightly lower in H1 FY26 due to mix, but working to bring them back to previous higher levels

💠Export demand remains strong

▫️Capex & Funding: Recent fund raise (~₹30–40 Cr via preferential issue/warrants) → 60–80% to be used for capex

💠Capex will be continuous and across segments (asphalt/concrete pavers, milling machines, crushing plants, piling rigs, etc.)

💠Debt/Equity target: ~1 or lower even after capex (post warrant conversion equity base will be ~₹300–325 Cr, net debt ~₹287 Cr currently → room for another ₹300 Cr+ asset addition with leverage)

▫️Working Capital: Low working capital requirement in rental (majority term loans for assets)

💠Refurbishment needs some working capital (90–100 days cycle), but overall cycle remains comfortable.

▫️Seasonality: H1 is normally leaner (monsoon), H2 stronger → FY26 H2 expected to be better than H1 (both revenue and margins)

#VISIONINFRA at 16 PE multiple. Check out my #VIESL analysis on @TradingView: https://t.co/qbZVrQGF4t

@RajStockWatch on expanded eq eps ttm sept would be 13

es 3.1 cr (eq shares) after warrants

🤞

#visioninfra #viesl

(TMT) VISION INFRA EQUITP (SME) (close 235) :- Breakout after multi week.

👉Now 210-205 act as a strong support zone.

👉Expected 350-500 (6 months)

👉Lot size 800 (SME GROUP stock).

#Visioninfra

Wishing you a blessed Eid Milad-un-Nabi! May this day’s wisdom illuminate your path.

Happy Milad un-Nabi!

#MiladunNabi2025 #VisionInfra #VsionArsha #VIDIPL #RealEstate #FlatsForSale #FlatsForSaleInHyderabad #LuxuryApartments

Vision infra equipment

#VisionInfra

#VIESL

Valuations:

EV/EBITDA at 5.2x FY25

P/E at 11x FY25

Inv PPT:

240cr orderbook

Rev 443cr⏫33%

EBITDA at 131cr⏫31%

OPM at 28.7%

FY21-25:

Rev CAGR 29%

PAT CAGR 60%

Strong growth in rental revenue

63cr in FY21 to 205cr in FY25

Refurbishment revenue:

Grew from 95cr in FY21 to 238cr in FY25

Strategic expansion into concrete pavers

High growth market opportunity

27cr orderbook with fleet strength of 21 units

FY26:

Expects revenue to conservatively grow at 20%+ with 27%+ OPM

RoCE 22%

2.8x interest coverage

Vision infra equipment

#VisionInfra

#VIESL

Good FY25 to end with solid H2FY25 and good H2FY25

12 P/E

H2 EBITDA of 67cr

H1 EBITDA of 52cr

FY25 EBITDA at 119cr with 27% OPM

Rev at 443cr vs 333cr

EBITDA at 119cr vs 82cr

PBT at 48cr vs 39cr

PAT at 34cr vs 27cr

RoCE 25%

RoE 36%

62cr FCF

Ev/EBITDA 5x

Mktcap of 430cr

Higher debt with D/E at 1.8x

Vision Infra Equipment

#VisionInfra

Blockbuster set👏

Solid traction vs H1FY25

Rev at 249cr vs 69cr, H1 at 194cr

PBT at 27cr vs 9cr, H1 at 21cr

PAT at 20cr vs 6cr, H1 at 15cr

FY25 PBT at 48cr vs 32cr

FY25 PAT at 34cr vs 26cr

OCF at 40cr vs 14cr👏🔥

Solid cash flows

Blockbuster Results for today

17 May 2025

1. Vision Infra Equipment (#VisionInfra)

• Rev: 249cr vs 69cr

• PAT: 20cr vs 6cr

2. Zen Technologies (#ZenTech, #ZenTec)

• Rev: 324cr vs 141cr

• PAT: 113cr vs 37cr

3. Banco Products (#Banco)

• Rev: 868cr vs 717cr

• PAT: 153cr vs 68cr

4. Data Patterns (#DataPatterns)

• Rev: 396cr vs 182cr

• PAT: 114cr vs 71cr

Good #Q4FY25-17/05/2025 till 9pm

Vision Infra Equipment

#VisionInfra

Blockbuster set👏

Solid traction vs H1FY25

Rev at 249cr vs 69cr, H1 at 194cr

PBT at 27cr vs 9cr, H1 at 21cr

PAT at 20cr vs 6cr, H1 at 15cr

FY25 PBT at 48cr vs 32cr

FY25 PAT at 34cr vs 26cr

OCF at 40cr vs 14cr👏🔥

Solid cash flows

Premier Energies

#PremierEnergies

Another stellar quarter

Solid margin expansion QoQ and YoY

Rev at 1620cr vs 1126cr, Q3 at 1713cr

PBT at 368cr vs 114c4, Q3 at 350cr

PAT at 278cr vs 104cr, Q3 at 255cr

FY25 PBT at 1239cr vs 289cr

FY25 PAT at 937cr vs 231cr

OCF at 1348cr vs 90cr👏🔥

JG Chemicals

#JGChem

#JGChemicals

Ends FY25 with 2x PBT and 2x PAT growth over FY24

Some margin pressure QoQ

Healthy set YoY

Rev at 224cr vs 181cr, Q3 at 209cr

PBT at 21.5cr vs 18cr, Q3 at 24cr

PAT at 16cr vs 13cr, Q3 at 18cr

FY25 PBT at 90cr vs 44cr

FY25 PAT at 67cr vs 32cr

OCF at -11cr vs 76cr mainly due to inventories at 111cr vs 55cr

Zen Technologies

#ZenTech

#ZenTec

Blockbuster Q4FY25 🔥 👏

Exponential growth

Highest ever revenue, EBITDA PBT and PAT in comps history

Rev at 324cr vs 141cr, Q3 at 152cr

PBT at 154cr vs 52cr, Q3 at 59cr

PAT at 113cr vs 37cr, Q3 at 43cr

OCF at -146cr vs 13cr

Banco Products

#Banco

Blockbuster Q4FY25 🔥 👏

Record set

Highest ever revenue, EBITDA, PBT and PAT in comps history

Rev at 868cr vs 7171cr, Q3 at 632cr

Solid margin expansion QoQ and YoY

PBT at 190cr vs 85cr, Q3 at 39cr

PAT at 153cr vs 68cr, Q3 at 31cr

OCF at 164cr vs 458cr

Data Patterns

#DataPatterns

Blockbuster Q4FY25 👏 🔥

Solid solid execution in Q4

Rev at 396cr vs 182cr, Q3 at 117cr

PBT at 153cr vs 95cr, Q3 at 59cr

Margin compression YoY

PAT at 114cr vs 71cr, Q3 at 45cr

OCF at -90cr vs 139cr

As most of the revenues came in Q4

Brahmaputra Infrastructure

#Brahmaputra

#BrahmInfra

Solid, blockbuster Q4FY25 🔥 👏

Rev at 103cr vs 54cr, Q3 at 29cr

PBT at 22cr vs 5cr, Q3 at 1cr

PAT at 22cr vs 4cr, Q3 at 0.4cr

OCF at 64cr vs -126cr

Divis Laboratories

#Divis

Solid Q4FY25 👏

Rev at 2585cr vs 2303cr, Q3 at 2319cr

PBT at 864cr vs 713cr, Q3 at 726cr

PAT at 662cr vs 538cr, Q3 at 589cr

OCF at 1653cr vs 1261cr

Sat Kartar Shopping

#SatKartar

Rev at 87cr vs 75cr, H1 at 76cr

PBT at 8cr vs 5cr, H1 at 5cr

PAT at 6cr vs 3.7cr, H1 at 3.8cr

OCF at -5cr vs 7cr

Precision Wires

#PrecWires

Solid Q4FY25

Rev at 1045cr vs 878cr, Q3 at 979cr

PBT at 40cr vs 29cr, Q3 at 25cr

PAT at 30cr vs 22cr, Q3 at 19cr

OCF at 168cr vs 60cr👏

Solid QoQ and YoY uptick in all parameters

Bhageria Industries

#Bhageria

Topline flat at 183cr

Solid margin expansion QoQ and YoY

PBT at 22cr vs 10cr, Q3 at 16cr

PAT at 15cr vs 6cr, Q3 at 11cr

OCF at 52cr vs 23cr👏

Arvind Fashions

#ArvindFashion

Rev at 1189cr vs 1094cr, Q3 at 1203cr

PBT at 66cr vs 54cr, Q3 at 68.5cr

OCF at 530cr vs 434cr

Pritika Engineering Components

#PritikaEngg

Rev at 34cr vs 21cr, Q3 at 28cr

PBT at 2.2cr vs 0.4cr, Q3 at 1.6cr

PAT at 1.7cr vs 0.3cr, Q3 at 1.4cr

OCF at 22cr vs -6cr

Remus Pharma

#Remus

Solid topline growth, margin compression sharply

Rev at 347cr vs 184cr, H1 at 272cr

PBT at 25cr vs 20cr, H1 at 22cr

PAT at 21cr vs 19cr H1 at 18cr

OCF at 7cr vs 1cr

Bombay Super Hybrid Seeds

#BSHH

Seasonality in the business

Rev at 46cr vs 30cr

PBT at 4.6cr vs 2.6cr

PAT at 4.2cr vs 3cr

OCF at -31cr vs 11cr

Decent/Average:

#IceMake

Big increase other expenses and big increase in depreciation leads to PBT degrowth

Depreciation at 4cr vs 1cr

Employee expenses at 8cr vs 5cr

Other expenses at 29cr vs 19cr

Rev at 180cr vs 140cr, Q3 at 110cr

PBT at 16cr vs 19cr, Q3 at 4cr

OCF at 30cr vs 10cr

#ArrowGreentech

Rev at 57cr vs 51cr, Q3 at 55cr

PBT at 16cr vs 15cr, Q3 at 18cr

OCF at 68cr vs 18cr

#Visioninfra results are out

H225 VsH125

Rev : 255.30 Cr Vs 199.39 Cr (up 28%)

EBITA: 27.29 Cr Vs 20.95 (up 30.2%)

PAT : 19.53 Cr Vs 14.52 Cr (up 34.5%)

25 Vs 24

Rev : 454.80 Cr Vs 72.83 Cr (up 🚀 524%)

EBITA : 48.25 Cr Vs 8.04 Cr ( up 🚀 500%)

PAT : 34.05 Cr vs 5.75Cr up 🚀492%

Vision infra explosive growth 🚀🚀

Both topline and bottom line grew by 4x yoy

New PE 11-12

PAT exactly 35 cr, as told in 2nd october 😅

#visioninfra

#SME #VIESL #VISIONINFRA #VISIONINFRAEQUIPMENT

Vision Infra Equipment Solutions FY25 Results :

👉H2 FY25 revenues at 239cr, H1 was 192cr.

Full FY25 revenues at 443cr; 33% growth YoY. Better than estimates of ~25% growth

👉Valuations down to 11 P/E; ~6 times EV/EBITDA

👉Blended EBITDA improves ~27% from earlier 25%

👉PAT ~8% maintained

👉Receivables increase minimal, positive cashflow from operations

Most Popular Users

Elon Musk

@elonmusk

240.6M followers

Barack Obama

@barackobama

119.3M followers

Donald J. Trump

@realdonaldtrump

111.7M followers

Cristiano Ronaldo

@cristiano

110.4M followers

Narendra Modi

@narendramodi

107M followers

Rihanna

@rihanna

97.6M followers

NASA

@nasa

92.2M followers

Justin Bieber

@justinbieber

90.9M followers

KATY PERRY

@katyperry

87.6M followers

Taylor Swift

@taylorswift13

81.4M followers

Lady Gaga

@ladygaga

72.9M followers

Kim Kardashian

@kimkardashian

69.7M followers

Virat Kohli

@imvkohli

69.7M followers

YouTube

@youtube

68.7M followers

Bill Gates

@billgates

63.8M followers

Neymar Jr

@neymarjr

62.5M followers

The Ellen Show

@theellenshow

62.5M followers

CNN

@cnn

61.9M followers

X

@x

60.8M followers

Selena Gomez

@selenagomez

60.7M followers