HerkBath is starting with two value portfolios.

One is young, hungry, and cheap.

One is older, calmer, and pickier.

Think Graham’s bargain bin arguing with Munger’s quality filter in a room full of annual reports.

1/12

Alright guys. Here's a big one.

I spent years (15 now, to be exact) trying to figure out why some companies are almost impossible to kill

Not moats made of patents or switching costs. Those are in every textbook that we have all read 1,000 times

I'm talking about the ones built from something deeper. Memory. Identity. The feeling a brand leaves in your nervous system before your conscious mind ever runs the numbers.

That's what I wrote about in this book.

Memory Moat Investing.

I tried to find out what happens when you stop asking "what does this company do" and start asking "what does this company mean to the people who can't stop buying from it."

It pulls from Buffett. Jung. Behavioral psychology. Consumer neuroscience. And about a decade of me sitting in a small town on the California coast, watching billion dollar brands through a lens nobody taught me in a classroom.

If you've ever felt like the best investment insights live somewhere between a balance sheet and a therapy session, this might have been written for you.

I really hope you enjoy it. Please reach out to me with your comments, questions, or anything else. I'm always here to talk and learn. And of course, any Memory Moat businesses you find!

https://t.co/e3z88Ci0iB

What if I told you you could buy $MU for half off in a little over a year? You’d probably think i’m crazy. I invested in $MU at about $80 and sold my last tranche at an average of $840 which is still lower than today’s price. I think consolidation here is healthy and necessary and you might be able to snatch some shares up for <$500 in 27’. That’s not really the point though. Buy and hold forever is nice in theory but it doesn’t always work out that way. Sometimes stocks extend well beyond a reasonable valuation due to optimism and although much of it is warranted, I believe we have hit the plateau here in the short term. Conversely, opportunity cost is a hell of a drug, and there are some wonderful names right now trading below reasonable valuations and some with catalysts on the horizon $SLM

Stocks are the only thing that people run from when they go on sale. The sale is coming

If you ever wondered how a conversation with young partnership Buffett and modern Buffett about $LULU would go, read here 👇@lululemon@michaeljburry

https://t.co/3oGvrCsh28

@herkbath

@rja907 despite unit volume declines, which proves the buyer side of the network effect is intact and strengthening. management is buying back shares aggressively: over 43.4 million shares repurchased for over $1.6 billion fiscal year-to-date

@rja907 $CPRT is trading at its lowest ever forward P/E of ~20x. RB Global/IAA grew units 4.7% YoY while Copart contracted 2.8%, with Progressive moving meaningful volume to IAA. the hidden variable the market is underweighting is buyer liquidity: Copart’s ASPs are at all-time highs 1/2

@michaeljburry quality business at a statistically cheap price. Partnership Buffett would recognize this as a “Sanborn Map” type situation where the underlying value is being ignored.

@michaeljburry 9x trailing PE on a 30%+ ROIC brand is statistically cheap. North America stalled, but Chip Wilson proxy fight + Elliott position create activist workout dynamics. New CEO starts September 2026. At $120, the base IV of ~$180 gives genuine MOS. This is a hybrid:

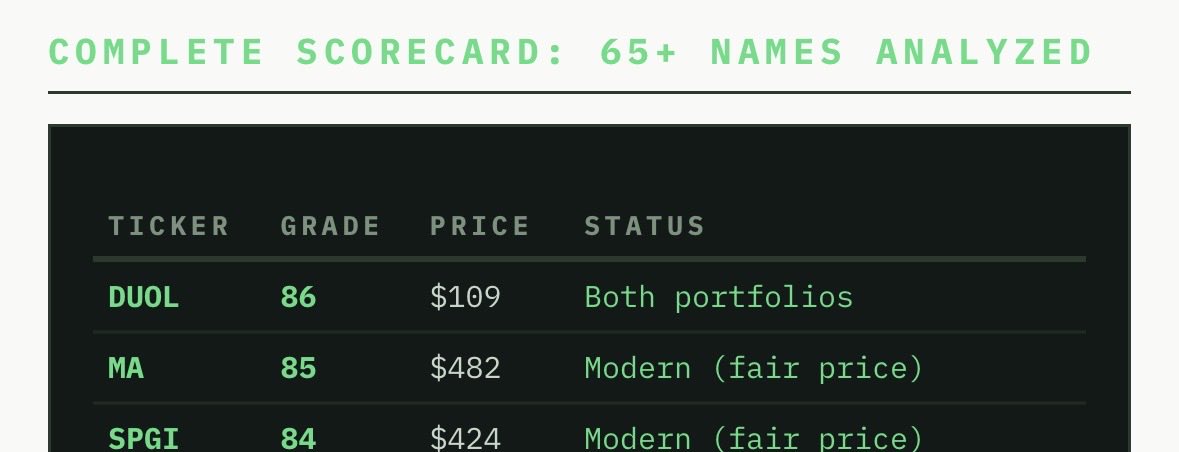

Here’s a little peek into the current modern portfolio’s allocation. The more companies we analyze, the better we get.

$ADBE $DUOL $BKNG $DECK $KKR $MELI $TEAM $VEEV $CPRT $KNSL $DPZ $NFLX

$SPGI $MA $PGR are 3 positions the modern portfolio has added as part of the “pay a fair price for a wonderful business” basket at 5% combined due to the thin margin of safety.

Right now, interestingly enough, the partnership portfolio is 73% generals and 10% in workouts

$SPGI $MA $PGR are 3 positions the modern portfolio has added as part of the “pay a fair price for a wonderful business” basket at 5% combined due to the thin margin of safety.

Right now, interestingly enough, the partnership portfolio is 73% generals and 10% in workouts

There are 10 stocks out of our investable universe so far that overlap in both the partnership portfolio and the modern portfolio

$ADBE $DUOL $TEAM $DECK $CPRT $CMG $DPZ $VEEV $POOL $NVO

Ideally the holding period on these stocks is forever, unless the thesis changes

If I could own one insurance business forever and never look at the price again, it is $PGR. Buffett’s GEICO was his version of the same idea: the low-cost auto insurer with a structural expense advantage that compounds market share relentlessly.

Most people think the key variable for $SLM is credit quality. The better interpretation is that the key variable is the irreversibility of the PLUS reform, because the system actually turns on political lock-in dynamics.

The OBBBA was a massive reconciliation bill that required extraordinary political capital to pass. Reversing the PLUS

elimination would require another reconciliation bill or bipartisan

legislation, neither of which is politically feasible within the next 4-6 years. This means the demand shift is not a one-year event. It is a structural, multi-year tailwind that compounds. By the time any future Congress could theoretically reverse it, $SLM will have originated $15-25B in new grad loans, built deep relationships with grad borrowers, and established the private market as the default funding source. The political lock in creates an economic moat extension that is not priced into a 6x multiple.

One more thing: $SLM is transitioning from a balance sheet lender

to a lending platform. Originate, sell to KKR, collect servicing fees, recycle capital into buybacks. This is the same business model evolution that made companies like Rocket Mortgage valuable: capital light origination with fee based income. The market is valuing $SLM as a capital heavy bank. It is becoming a capital light origination

platform. When that transition completes, the correct multiple is not

6-8x. It is 10-14x.