Fed Fed funds rate to wind lower based on private equity Blackstone ($BX) co-founder and CEO Steven Schwarzman's Cantillon seating at Versailles last night.

If you think $BTC in 2036 has a 50 percent chance to be worth one-half the present value of global gold, as I do, but also a 50 percent of going to zero like Buffett, Munger, Schiff, and Hanke say, at its current $61,000 price per coin the positive asymmetry is outstanding, at 19 units of upside for every unit of downside. What else do you own that offers more reward for the risk, adjusted for the time value of money and chance of occurrence?

@Porter_and_Co My dear friend Thornton "Ted" Oglove ("Quality of Earnings") said more than a decade ago $BRK should deconglomerate https://t.co/9NYJQGmNTI. My two cents: the best managers want their own scorecard, just like Mr. Buffett wanted when he started his partnership in the mid-50s.

@RealRickRule@intlmandotcom The value of USA's monetary promise has plunged as much as 80 percent in the last 10 years when priced in real money, and as much as 95 percent in the last 30 years. https://t.co/KqsDza8znq

The 10-year Treasury yield is perhaps the most important financial benchmark in the global fiat system, as it drives valuations and market trends worldwide. It is widely—and erroneously—regarded as the risk-free rate of return.

The 10-year Treasury yield can be thought of as a key barometer of the US dollar-based fiat system—a critical measure akin to its beating heart.

Bond yields move inversely to bond prices. When bond prices fall, bond yields rise.

A rising 10-year Treasury yield signals trouble for the US dollar because it means investors are selling Treasuries, which pushes up the US government’s borrowing costs. That is why the 10-year Treasury yield is a major pain point for the US government.

The 10-year Treasury yield was 3.97% when the war started. Now it is around 4.60%, an increase of roughly 63 basis points.

I expect the 10-year Treasury yield to keep climbing over the coming weeks and months—until it forces the Fed’s hand. At that point, the intervention will be sold as “stability,” but the mechanism will be familiar: suppress yields by debasing the currency.

At today’s debt levels, every 1 basis point increase in the government’s average borrowing cost adds roughly $3.9 billion in annual interest expense. So a 63 bps rise is not trivial—it translates to nearly $250 billion in additional yearly interest costs, materially widening a 2025 budget deficit that was already around $1.8 trillion.

Higher yields mean the US government must pay tens or even hundreds of billions more in interest on its debt. At the same time, the global economy faces even greater added costs because Treasury rates serve as the benchmark for borrowing worldwide.

That is not an insignificant move. However, given all the headwinds I have discussed, I suspect the 10-year Treasury yield is headed much higher because investors will demand higher yields to compensate for rising inflation. Further, if Hormuz remains closed, drastically higher oil prices are all but certain. Higher energy prices mean higher prices across the economy and higher official inflation rates, which means investors will demand still higher yields to compensate.

The problem is that interest on the federal debt is already over $1.2 trillion and is now the second-largest item in the budget. The US government cannot afford yields going much higher because the interest expense would push it toward bankruptcy.

I am not sure how—or even if—the US government can manage this situation. Something has to give, and we will not have to wait long to find out what.

The Iran war may prove to be more than another foreign policy disaster. It could be the trigger that exposes the fragility of the entire dollar-based financial system.

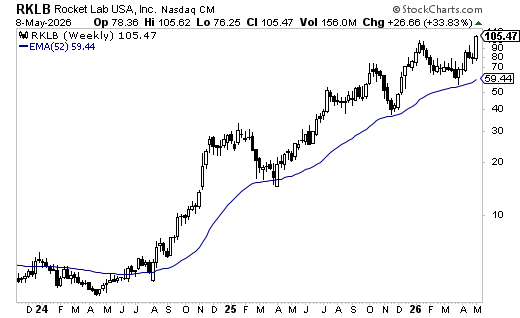

@DavidGFool@steven3ford My eventually-to-be-published book on expected value and how superinvestors decide has an appendix chapter on actors, behaviors, concepts, jargon, laws, memes and phenomenon to know. "Spiffy-pop" is in there. Conratulations @DavidGFool and @steve3ford on $RKLB

@mr_deepvalue Wa Po is best stock to learn how WEB decides. Reasons: 1) comp advantage (local monopoly), 2) rev model (gross profits royalty), 3) family owned (generational outlook), 4) edge (knew newspaper economics), 5) high EVM, and 6) sold when pricing power disappeared. 104x in 41 years.

@mr_deepvalue If Buffett believed Katharine Graham's media company offered $3 or more of upside reward for every dollar of downside risk, adjusted for the time value of money and chance of occurrence, he just needed to get a hit once every four swings of the bat. Here's the math: 1 / (1 + 3).

@mr_deepvalue The higher a stock's EV multiple, the greater the margin of safety to protect against what Ben Graham described as "miscalculation or worse-than-average luck."