Currently under GSM Stage IV with trading restrictions.

Normally, many investors would simply ignore such stocks.

But some recent developments made me add it to my watchlist:

• Onix Renewable has become the largest shareholder.

• ₹62.53 crore brought in through preferential warrant conversion.

• Authorised share capital increased from ₹13 crore to ₹100 crore.

• Entire top management has been reshuffled.

• Business objects are being changed.

• Proposed name change to Onix Power Ltd.

Interestingly, Onix Renewable is also associated with Onix Solar Energy, another listed company that has seen a strong re-rating over time.

That doesn’t mean the same outcome will happen here, but it makes this story worth following.

Read the announcements, connect the dots, and decide for yourself.

Company name :

Sarda Proteins Ltd

CMP: Rs 93

Mcap 83.60 Cr.

High Risk | High Reward | #DYOR

Everyone is calling defence textiles the next big thing.

Parachutes for Gaganyaan, stealth camo for the Army, decoy systems that fool enemy sensors.

- Kusumgar Ltd makes all of it, and it opens for IPO on July 8.

- In FY26, both its revenue and its profit went backwards...

Let's read the RHP properly.🧵 1/12

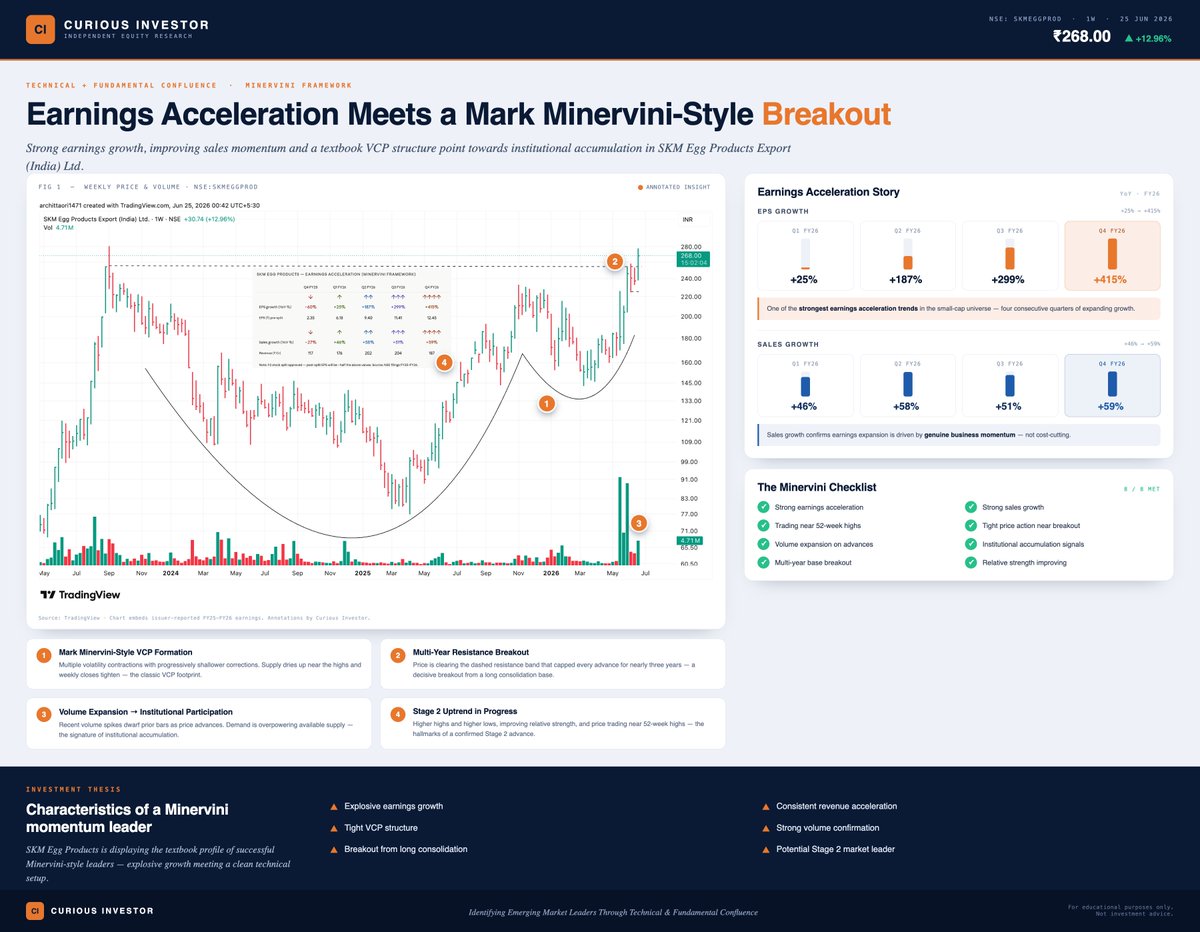

Mark Minervini says 90% of the biggest stock market winners show Earnings Acceleration before their big move.

SKM Egg Products (#SKMEGGPROD) is checking every box.

EPS growth: +25% → +187% → +299% → +415%

Sales growth: +46% → +58% → +51% → +59%

Four consecutive quarters. Zero exceptions.

This is what a momentum leader looks like before it moves.

THE CONVICTION

Kiri Industries.

CMP: ₹391 | Market cap: ₹2,572 Cr

49% below its 52-week high.

Received ₹6,200 Cr in cash — 2.4x its market cap.

Promoter just put ₹93 Cr of his own money in.

3 numbers that don't add up.

Here's what I found after

digging into this company. 🧵👇(1/12)

Mathew Cyriac — the man who keeps printing multibaggers.

#MTAR Technologies → 47x in 4 years

#DataPatterns → 21x in 2.5 years

#ideaForge → 6x (still holding 10.67%)

All in India's defence & deep tech space. All before the market even knew these names.

Currently betting on #TonboImaging (defence optics, pre-IPO) and just bought #Nitco in May 2026.

This is what pattern recognition looks like.

Murugappa Group is quietly tightening its grip on Wendt (India). 🔥

Via CUMI, they’ve now secured sole promoter control in Wendt (India)

German JV partner Wendt GmbH fully exited its 37.5% stake via OFS in May 2025.

Deal at discounted floor of ₹6,500/Share (₹487 Cr total offer size).

New structure in place with CUMI as sole promoter (37.5% holding).

What's interesting after the acquisition ?

Debt-free balance sheet

Cleaner ownership structure

Strong push into new products & exports

Focus on customer additions & market expansion

The First Few Quarters under a single-promoter structure could be worth tracking closely.

Mathew Cyriac — the man who keeps printing multibaggers.

#MTAR Technologies → 47x in 4 years

#DataPatterns → 21x in 2.5 years

#ideaForge → 6x (still holding 10.67%)

All in India's defence & deep tech space. All before the market even knew these names.

Currently betting on #TonboImaging (defence optics, pre-IPO) and just bought #Nitco in May 2026.

This is what pattern recognition looks like.

Latest additions to the portfolio

BMW- doing 1000 cr capex. Market cap is below 1000.

Guidance to grow above 50 to 70 percent

Patil automation - confident of doing 50 percent growth. Just completed new production facility

Mitsu chem- guidance improvement and 30 percent rev growth guided.

For fair values do visit fv group.

Not buy sell recco.

Looking for an undervalued and relatively less risky ethanol play? 👀

BCL Industries Ltd

CMP: ₹33.50

Market Cap: ₹989 Cr

FY2025 Numbers:

✅ Sales: ₹2,815 Cr

✅ Net Profit: ₹103 Cr

Just compare:

₹989 Cr market cap vs ₹2,815 Cr sales 👀

Face Value: ₹1

PE: 8.44

Business now transforming towards:

⚡ Ethanol

⚡ ENA

⚡ Biodiesel

⚡ Renewable energy-focused operations

Key developments:

• 150 KLPD ethanol expansion underway

• 75 KLPD biodiesel project coming up

• Gradually exiting low-margin edible oil business

• Increasing focus on higher-margin biofuel segment

Recent concall also highlighted:

✅ Extra Neutral Alcohol (ENA) volume growth

✅ Capacity utilization near 100%

✅ Exploring exports & industrial alcohol opportunities

✅ Long-term focus on clean energy and future fuels

If execution continues as planned and ethanol policy remains supportive, the market may start to value this company differently in the coming years.

Not a recommendation. DYOR.